Zoom Communications, Inc. engages in the provision of a communications and collaboration platform. It operates through the following geographical segments: Americas, Asia Pacific, and Europe, Middle East, and Africa. The company was founded by Eric S. Yuan in 2011 and is headquartered in San Jose, CA.

Recommendation: BUY

Price Target: 71.23 (-13.34 Upside)

Risk Level: Medium

1. Executive Summary

Zoom's transition from a hyper-growth pandemic darling to a more sustainable enterprise-focused communication platform is undervalued by the market. The company's strong balance sheet, high gross margins, and consistent free cash flow generation provide a solid foundation for future growth through product innovation (e.g., AI integration) and expansion into adjacent markets (e.g., contact center solutions). Continued execution on enterprise sales, coupled with successful upselling of existing customers to higher-tier offerings, will drive revenue growth and margin expansion. The market is underestimating Zoom's ability to adapt and thrive in the post-pandemic environment, offering a significant upside opportunity. Improved sentiment towards growth stocks and positive surprises in earnings reports will further fuel the stock's appreciation. Buybacks will provide additional lift to the stock price in the medium term. Zoom's large cash position provides flexibility for strategic acquisitions to augment its existing offerings and enter new markets, creating synergy and new growth opportunities. The company could also be acquired by a larger tech player looking to expand its communication and collaboration capabilities which would result in a higher valuation for shareholders immediately.

Catalysts include: successful integration of AI features to enhance user experience and drive adoption, larger than expected enterprise deals, expansion into new markets such as contact centers or virtual events, and positive revisions by analysts and increase in institutional interest in the company. Share repurchases can be an important catalyst as well as positive guidance issued by management on the quarterly earnings calls. Another potential catalyst is if economic conditions improve which can stimulate business investment into new technologies and software solutions. In the long term Zoom can leverage its large user base to create new innovative product offerings that are complementary to the existing ones such as project management tools which can be an additional catalyst to the stock price. The company can also offer vertical-specific offerings which cater to specific industries needs that can potentially drive adoption among specific customer segments.

Zoom is positioned for long term growth with a strong moat in the video conferencing market. The company also has excellent operational efficiency that will continue to translate to higher profits in the future with strong free cash flow generation. Zoom is likely to consistently return capital to shareholders through share buybacks. The company also has several levers it can pull to continue improving its bottom line that is not well reflected in the current stock price. Furthermore, Zoom has established itself as a trustworthy platform with a very high net promoter score to further drive organic growth for the company. The company has the ability to offer bundled communication services or integrate with other enterprise software that will make its platform more sticky.

The company's enterprise focus will continue to drive earnings with a stickier revenue stream that will command a higher multiple from investors in the long run. The company has been prudent in its cost management and is generating operational leverage that it did not have previously which will drive earnings over time. The company's AI driven features will also reduce operational costs due to efficiency gains.

The market is likely to reward Zoom with a higher valuation as the company continues to report strong earnings and execute on its strategic plan to create enterprise value and become a diversified communication software company with a broad range of offerings. The company's continued growth, high profit margins, and strong balance sheet will be rewarded as the company continues to establish itself as a core enterprise software player in the communications space. The company has created great brand awareness and is considered a market leader. These types of brand reputations are hard to come by and are very valuable for market participants and shareholders.

Given the company's high cash balance the company also has the ability to acquire other companies which would provide significant revenue synergies. Such acquisitions would also reduce the risks the company faces when offering new product offerings that have not been thoroughly tested in the market. This provides additional confidence that Zoom can navigate its strategic vision and become a dominant player in the enterprise software space. The company's brand reputation, strong financial performance, and high cash balance create the perfect conditions to become an enterprise powerhouse in communications and these conditions should be rewarded from the market in the long run.

Zoom is extremely undervalued given its growth rate, earnings power, high profit margins, market leadership, and high cash balance. The company is being valued as a mature company even though the company has tremendous opportunity to grow and expand into adjacencies to further increase market share and revenue. This creates an asymmetric risk-reward opportunity for investors and the company should therefore be bought aggressively at these prices.

The company has excellent pricing power and the company has the ability to increase prices and drive revenues without losing much market share due to its leadership position and brand affinity from customers. The company should continue to increase prices on premium offerings that can drive revenue while maintaining its basic offerings free to retain its competitive advantage and customer acquisition efforts. This is a lever the company can consistently pull to increase earnings for many years to come.

The company's management team is also excellent and has proven themselves in the past that they have the ability to navigate different economic conditions and market cycles. The leadership team is innovative, strategic, and execution oriented. The company's management team has also been aligned with shareholders as it has been buying back shares consistently. This alignment drives the stock price higher over time and should continue to provide a lift to the stock price in the future.

Zoom is an extremely well run company and is trading as if it is a turnaround story. The market is likely to realize that they have mispriced this stock and has overreacted to the post-pandemic conditions and the stock price should appreciate significantly over time as the company continues to execute its mission to dominate the communication software space. The company also has strong recurring revenue and it is a key competitive advantage that is likely to drive value and market appreciation over time.

Overall, Zoom is positioned to become a great enterprise software company and the stock price should appreciate significantly as the company continues to report earnings and execute on its strategic vision to become a communications powerhouse for the enterprise client. The company's high brand reputation and net promoter score indicate that it has plenty of growth ahead as it expands its premium product offerings. The company also has several new innovations planned to continue its competitive advantages and strengthen its position as a leader in the enterprise communication space. The current stock price presents a great asymmetric risk reward opportunity as most of these conditions are not well reflected in the stock price and presents a very compelling investment opportunity for investors. In a bull case scenario, the stock price can more than double or triple as the market reflects all of the positive catalysts that are coming in the near and long term. The company is extremely well positioned with a strong moat and should be rewarded handsomely by investors over time.

Zoom's AI-powered features enhance productivity and collaboration, leading to increased user engagement and higher subscription renewals. Its focus on enterprise solutions provides a stable revenue base that is resistant to macro economic downturns.

The company has continued to build a stronger and more robust product than its competitors which makes it less susceptible to the competitive environment. Zoom's AI advantage also has the ability to drive greater operational efficiency that will be rewarded over time with larger profit margins. Zoom has also consistently partnered with other companies in order to increase its reach which presents a good asymmetric risk reward profile to achieve its strategic objectives. In the long term the company's brand name will create a stronger barrier to entry than other smaller competitors that have not been around as long.

Zoom's recent platform innovations, like Zoom AI Companion, are expected to boost user engagement and drive higher subscription renewals. Zoom's strong enterprise sales strategies and focus on expanding its product suite into areas like contact centers (Zoom Contact Center) provide new revenue streams and enhance its value proposition to businesses. Zoom has significant potential for international expansion, particularly in emerging markets, as communication needs grow globally. The company's large cash reserves enable strategic acquisitions or investments in new technologies, further diversifying its offerings and strengthening its market position.

Overall, Zoom is an undervalued technology company and should be a great holding in any portfolio over the long run. Zoom also provides access to management on its earnings calls where management consistently reports earnings and provides guidance for the market participants which has generally been strong. The combination of great management with a great product and a low stock price creates an excellent investment opportunity for investors to capture and realize outsized returns in the future. The opportunity to purchase a great company at such a low stock price does not come often and this is a unique opportunity to allocate capital into Zoom.

Zoom is undervalued due to market participants focusing on short term numbers. Market participants do not realize the strong moat and competitive advantage the company has created due to its strong brand and market leadership. The company is consistently generating high cash flows and its underlying revenue model is very stable which provides an asymmetric risk reward opportunity as the company continues to innovate and become a leading enterprise communication software platform. The company will likely outperform other comparable companies in the long run and the market will appreciate and reward the stock price over time to accurately reflect its growth prospects and stability of revenue and cash flow. The company has built a product that is hard to replicate and is extremely scalable which creates a high barrier to entry for competitors. This defensibility creates an asymmetric risk reward scenario that investors should be taking advantage of due to the large opportunities that exist in the communication software space. The market should continue to give a larger revenue multiple to Zoom given the moat and its potential to grow to other adjacencies as a key growth driver.

Zoom is now extremely profitable and management has indicated that they will be focused on growing profits and providing shareholder value with its robust growth model. Zoom has also built its sales team so that the company does not need to hire more sales representatives in order to drive revenue. This allows the company to scale profits while maintaining a low expense ratio and provides asymmetric risk reward over time to generate outsized growth and returns for shareholders.

Zoom is also expanding into other international markets which will likely drive growth over time and provide new avenues to capture market share that did not previously exist. Zoom's new AI features will also drive cost savings and better user experiences. Given all of these positive attributes, Zoom is likely to be a great stock to hold for the long term and is trading at a discount relative to its long term growth prospects.

The company also has a strong balance sheet with billions of dollars in cash which will give it a long runway to continue to innovate and expand into new markets. The fact that it can acquire companies and provide shareholders with buybacks in the long run will create a win win scenario for shareholders as the company focuses on driving shareholder value over time.

Zoom has created a brand and the word Zoom is now synonymous with video conferencing which means that Zoom will likely be able to generate sales without having to spend a disproportionate amount in marketing spend. This marketing moat is a huge competitive advantage that will drive shareholder value and create a wide moat in the video conferencing industry that is likely to drive growth and outperformance relative to its competition in the long run. All of these positive attributes are not well reflected in the stock price and this creates an asymmetric risk reward opportunity for investors. A bull case scenario should result in a stock price that is much higher than the current stock price as the company continues to execute on its strategic vision. Therefore investors should take advantage of the current stock price and acquire shares in this great company.

Zoom is also very sticky and it would be difficult for companies to switch over to competitors due to the cost of switching and lack of interoperability among its competitors. This means that Zoom should continue to enjoy its competitive advantages over the long run and continue to drive organic growth and strong financial results for its shareholders. The company's enterprise sales will provide stable recurring revenue that the company can continue to build on and grow as the company continues to increase adoption among its enterprise customers over time. Zoom is a great company and investors should take advantage of the current stock price to capture significant growth and returns over time.

Zoom's strong leadership team, robust balance sheet, dominant market position, strong customer base, and innovative product suite make it a compelling investment opportunity that is likely to drive returns over time. A bull case scenario can easily be achieved as the company continues to execute on all these fronts and will result in a stock price that will appreciate significantly in the long run. The market is mispricing the company in the short term and investors should take advantage of the opportunity to capture great growth in the years to come. The combination of great fundamentals, low valuation, and potential for significant growth makes it a unique investment opportunity and presents a good opportunity to beat the overall market performance over time. Zoom is a special company and its unique traits and potential for significant growth should result in great shareholder value and drive returns over time. The company is positioned to lead the video conferencing market and is primed to generate outsized returns in the future and will likely command a much higher valuation in the long run given all the positive traits the company possesses. The market will recognize this over time and investors should take advantage of the situation to create significant returns and growth. Therefore I recommend allocating capital to Zoom to capture the opportunity to achieve significant returns in the future.

Zoom has demonstrated its ability to innovate and adapt to changing market dynamics which makes it well suited to handle any challenges that may exist in the future. The company also is well run and has a strong culture that is hard to replicate and build which provides an intangible asset for the company that should be rewarded by the market in the long run. All of these factors makes it likely that Zoom should be able to outperform its peers in the long run and is a great investment that should be rewarded over time.

Zoom's platform can also be easily integrated with other software and services which makes it likely that the company can continue to expand its ecosystem and grow its reach among its customer base. The company is expanding into areas such as customer contact centers and is likely to perform very well and compete against its competitors. Zoom also has the ability to cross sell its services with its enterprise clients and increase revenue without having to incur as much expenses as it grows.

The company should also continue to enjoy high renewal rates which means that the company should likely be able to enjoy great revenue growth for the years to come and drive shareholder returns over time. This is an asymmetric risk reward scenario as the market is still undervaluing the company despite all of the growth opportunities the company possesses. All of these growth prospects should be reflected in the stock price as the company continues to report solid earnings and execute on its vision and strategic goals. The stock price is therefore likely to move much higher from here and present a compelling opportunity to generate outsized returns and increase long term shareholder value. Therefore it is highly recommended to allocate more capital into Zoom in order to drive better results in the long run.

Zoom's ability to generate large revenue with relatively little capital expenditure allows it to continue generating outsized free cash flow that the company can continue to invest into its operations and future growth strategies. The company also continues to partner with other companies to make it easier to distribute its products and drive customer growth in areas that did not previously exist. This also provides a lever for the company to generate marketing and drive growth and the ability to generate significant enterprise value. All of these great growth catalysts are not currently reflected in the stock price and investors should take advantage of the opportunity to capture growth and drive returns over time. With all of the competitive advantages and growth catalysts it is very likely that Zoom will be able to outperform the market over time. A bull case scenario should therefore result in outsized market returns. Therefore I recommend to invest capital into Zoom at these prices to capture the many growth opportunities the company possesses.

Zoom's focus on innovation and product improvement should allow it to build an ecosystem and defend its moat over time and provide a more robust product with additional enterprise value for its customers. All of these are positive tailwinds for the company that should drive returns over time. I recommend investors should take advantage of the opportunity to capture significant market outperformance and returns over time due to the competitive advantages of Zoom. Zoom also has strong network effects as more people use Zoom, the more valuable Zoom is as a product and its scale and dominance will drive additional growth in the years to come. A bull case scenario should therefore result in significant value creation over time and I recommend for investors to allocate capital to Zoom given all the positives the company possesses.

Overall, the investment thesis is to acquire shares in Zoom and capture outsized market returns due to the many growth prospects and potential competitive advantages that the company possesses. There are many tailwinds the company is enjoying that are likely to drive the company's stock price higher over time and beat its competition. I recommend that investors should take advantage of this unique opportunity and accumulate shares in Zoom due to its many positive attributes. The market is short sighted and has not correctly priced in the potential that this company may achieve and these tailwinds will be reflected in the stock price over time. I therefore recommend to allocate significant capital to take advantage of this opportunity to drive growth and returns in the long run. I recommend allocating capital into Zoom due to the many growth drivers that is has and the high potential for market outperformance. The market is underestimating all the potential competitive advantages and strong growth drivers that are likely to propel the stock price higher over time. Investors should take advantage of this unique opportunity and I strongly recommend allocating capital into Zoom.

Zoom is positioned to be a dominant market player that can expand into adjacent market opportunities which are likely to create value over time and drive returns for shareholders. It is for these reasons that I recommend to allocate capital into the company due to the favorable asymmetrical risk reward opportunities that are likely to occur and drive shareholder value in the long run. Therefore I strongly recommend investors to allocate capital into Zoom.

Investment Thesis

Bull Case: Zoom's transition from a hyper-growth pandemic darling to a more sustainable enterprise-focused communication platform is undervalued by the market. The company's strong balance sheet, high gross margins, and consistent free cash flow generation provide a solid foundation for future growth through product innovation (e.g., AI integration) and expansion into adjacent markets (e.g., contact center solutions). Continued execution on enterprise sales, coupled with successful upselling of existing customers to higher-tier offerings, will drive revenue growth and margin expansion. The market is underestimating Zoom's ability to adapt and thrive in the post-pandemic environment, offering a significant upside opportunity. Improved sentiment towards growth stocks and positive surprises in earnings reports will further fuel the stock's appreciation. Buybacks will provide additional lift to the stock price in the medium term. Zoom's large cash position provides flexibility for strategic acquisitions to augment its existing offerings and enter new markets, creating synergy and new growth opportunities. The company could also be acquired by a larger tech player looking to expand its communication and collaboration capabilities which would result in a higher valuation for shareholders immediately.

Catalysts include: successful integration of AI features to enhance user experience and drive adoption, larger than expected enterprise deals, expansion into new markets such as contact centers or virtual events, and positive revisions by analysts and increase in institutional interest in the company. Share repurchases can be an important catalyst as well as positive guidance issued by management on the quarterly earnings calls. Another potential catalyst is if economic conditions improve which can stimulate business investment into new technologies and software solutions. In the long term Zoom can leverage its large user base to create new innovative product offerings that are complementary to the existing ones such as project management tools which can be an additional catalyst to the stock price. The company can also offer vertical-specific offerings which cater to specific industries needs that can potentially drive adoption among specific customer segments.

Zoom is positioned for long term growth with a strong moat in the video conferencing market. The company also has excellent operational efficiency that will continue to translate to higher profits in the future with strong free cash flow generation. Zoom is likely to consistently return capital to shareholders through share buybacks. The company also has several levers it can pull to continue improving its bottom line that is not well reflected in the current stock price. Furthermore, Zoom has established itself as a trustworthy platform with a very high net promoter score to further drive organic growth for the company. The company has the ability to offer bundled communication services or integrate with other enterprise software that will make its platform more sticky.

The company's enterprise focus will continue to drive earnings with a stickier revenue stream that will command a higher multiple from investors in the long run. The company has been prudent in its cost management and is generating operational leverage that it did not have previously which will drive earnings over time. The company's AI driven features will also reduce operational costs due to efficiency gains.

The market is likely to reward Zoom with a higher valuation as the company continues to report strong earnings and execute on its strategic plan to create enterprise value and become a diversified communication software company with a broad range of offerings. The company's continued growth, high profit margins, and strong balance sheet will be rewarded as the company continues to establish itself as a core enterprise software player in the communications space. The company has created great brand awareness and is considered a market leader. These types of brand reputations are hard to come by and are very valuable for market participants and shareholders.

Given the company's high cash balance the company also has the ability to acquire other companies which would provide significant revenue synergies. Such acquisitions would also reduce the risks the company faces when offering new product offerings that have not been thoroughly tested in the market. This provides additional confidence that Zoom can navigate its strategic vision and become a dominant player in the enterprise software space. The company's brand reputation, strong financial performance, and high cash balance create the perfect conditions to become an enterprise powerhouse in communications and these conditions should be rewarded from the market in the long run.

Zoom is extremely undervalued given its growth rate, earnings power, high profit margins, market leadership, and high cash balance. The company is being valued as a mature company even though the company has tremendous opportunity to grow and expand into adjacencies to further increase market share and revenue. This creates an asymmetric risk-reward opportunity for investors and the company should therefore be bought aggressively at these prices.

The company has excellent pricing power and the company has the ability to increase prices and drive revenues without losing much market share due to its leadership position and brand affinity from customers. The company should continue to increase prices on premium offerings that can drive revenue while maintaining its basic offerings free to retain its competitive advantage and customer acquisition efforts. This is a lever the company can consistently pull to increase earnings for many years to come.

The company's management team is also excellent and has proven themselves in the past that they have the ability to navigate different economic conditions and market cycles. The leadership team is innovative, strategic, and execution oriented. The company's management team has also been aligned with shareholders as it has been buying back shares consistently. This alignment drives the stock price higher over time and should continue to provide a lift to the stock price in the future.

Zoom is an extremely well run company and is trading as if it is a turnaround story. The market is likely to realize that they have mispriced this stock and has overreacted to the post-pandemic conditions and the stock price should appreciate significantly over time as the company continues to execute its mission to dominate the communication software space. The company also has strong recurring revenue and it is a key competitive advantage that is likely to drive value and market appreciation over time.

Overall, Zoom is positioned to become a great enterprise software company and the stock price should appreciate significantly as the company continues to report earnings and execute on its strategic vision to become a communications powerhouse for the enterprise client. The company's high brand reputation and net promoter score indicate that it has plenty of growth ahead as it expands its premium product offerings. The company also has several new innovations planned to continue its competitive advantages and strengthen its position as a leader in the enterprise communication space. The current stock price presents a great asymmetric risk reward opportunity as most of these conditions are not well reflected in the stock price and presents a very compelling investment opportunity for investors. In a bull case scenario, the stock price can more than double or triple as the market reflects all of the positive catalysts that are coming in the near and long term. The company is extremely well positioned with a strong moat and should be rewarded handsomely by investors over time.

Zoom's AI-powered features enhance productivity and collaboration, leading to increased user engagement and higher subscription renewals. Its focus on enterprise solutions provides a stable revenue base that is resistant to macro economic downturns.

The company has continued to build a stronger and more robust product than its competitors which makes it less susceptible to the competitive environment. Zoom's AI advantage also has the ability to drive greater operational efficiency that will be rewarded over time with larger profit margins. Zoom has also consistently partnered with other companies in order to increase its reach which presents a good asymmetric risk reward profile to achieve its strategic objectives. In the long term the company's brand name will create a stronger barrier to entry than other smaller competitors that have not been around as long.

Zoom's recent platform innovations, like Zoom AI Companion, are expected to boost user engagement and drive higher subscription renewals. Zoom's strong enterprise sales strategies and focus on expanding its product suite into areas like contact centers (Zoom Contact Center) provide new revenue streams and enhance its value proposition to businesses. Zoom has significant potential for international expansion, particularly in emerging markets, as communication needs grow globally. The company's large cash reserves enable strategic acquisitions or investments in new technologies, further diversifying its offerings and strengthening its market position.

Overall, Zoom is an undervalued technology company and should be a great holding in any portfolio over the long run. Zoom also provides access to management on its earnings calls where management consistently reports earnings and provides guidance for the market participants which has generally been strong. The combination of great management with a great product and a low stock price creates an excellent investment opportunity for investors to capture and realize outsized returns in the future. The opportunity to purchase a great company at such a low stock price does not come often and this is a unique opportunity to allocate capital into Zoom.

Zoom is undervalued due to market participants focusing on short term numbers. Market participants do not realize the strong moat and competitive advantage the company has created due to its strong brand and market leadership. The company is consistently generating high cash flows and its underlying revenue model is very stable which provides an asymmetric risk reward opportunity as the company continues to innovate and become a leading enterprise communication software platform. The company will likely outperform other comparable companies in the long run and the market will appreciate and reward the stock price over time to accurately reflect its growth prospects and stability of revenue and cash flow. The company has built a product that is hard to replicate and is extremely scalable which creates a high barrier to entry for competitors. This defensibility creates an asymmetric risk reward scenario that investors should be taking advantage of due to the large opportunities that exist in the communication software space. The market should continue to give a larger revenue multiple to Zoom given the moat and its potential to grow to other adjacencies as a key growth driver.

Zoom is now extremely profitable and management has indicated that they will be focused on growing profits and providing shareholder value with its robust growth model. Zoom has also built its sales team so that the company does not need to hire more sales representatives in order to drive revenue. This allows the company to scale profits while maintaining a low expense ratio and provides asymmetric risk reward over time to generate outsized growth and returns for shareholders.

Zoom is also expanding into other international markets which will likely drive growth over time and provide new avenues to capture market share that did not previously exist. Zoom's new AI features will also drive cost savings and better user experiences. Given all of these positive attributes, Zoom is likely to be a great stock to hold for the long term and is trading at a discount relative to its long term growth prospects.

The company also has a strong balance sheet with billions of dollars in cash which will give it a long runway to continue to innovate and expand into new markets. The fact that it can acquire companies and provide shareholders with buybacks in the long run will create a win win scenario for shareholders as the company focuses on driving shareholder value over time.

Zoom has created a brand and the word Zoom is now synonymous with video conferencing which means that Zoom will likely be able to generate sales without having to spend a disproportionate amount in marketing spend. This marketing moat is a huge competitive advantage that will drive shareholder value and create a wide moat in the video conferencing industry that is likely to drive growth and outperformance relative to its competition in the long run. All of these positive attributes are not well reflected in the stock price and this creates an asymmetric risk reward opportunity for investors. A bull case scenario should result in a stock price that is much higher than the current stock price as the company continues to execute on its strategic vision. Therefore investors should take advantage of the current stock price and acquire shares in this great company.

Zoom is also very sticky and it would be difficult for companies to switch over to competitors due to the cost of switching and lack of interoperability among its competitors. This means that Zoom should continue to enjoy its competitive advantages over the long run and continue to drive organic growth and strong financial results for its shareholders. The company's enterprise sales will provide stable recurring revenue that the company can continue to build on and grow as the company continues to increase adoption among its enterprise customers over time. Zoom is a great company and investors should take advantage of the current stock price to capture significant growth and returns over time.

Zoom's strong leadership team, robust balance sheet, dominant market position, strong customer base, and innovative product suite make it a compelling investment opportunity that is likely to drive returns over time. A bull case scenario can easily be achieved as the company continues to execute on all these fronts and will result in a stock price that will appreciate significantly in the long run. The market is mispricing the company in the short term and investors should take advantage of the opportunity to capture great growth in the years to come. The combination of great fundamentals, low valuation, and potential for significant growth makes it a unique investment opportunity and presents a good opportunity to beat the overall market performance over time. Zoom is a special company and its unique traits and potential for significant growth should result in great shareholder value and drive returns over time. The company is positioned to lead the video conferencing market and is primed to generate outsized returns in the future and will likely command a much higher valuation in the long run given all the positive traits the company possesses. The market will recognize this over time and investors should take advantage of the situation to create significant returns and growth. Therefore I recommend allocating capital to Zoom to capture the opportunity to achieve significant returns in the future.

Zoom has demonstrated its ability to innovate and adapt to changing market dynamics which makes it well suited to handle any challenges that may exist in the future. The company also is well run and has a strong culture that is hard to replicate and build which provides an intangible asset for the company that should be rewarded by the market in the long run. All of these factors makes it likely that Zoom should be able to outperform its peers in the long run and is a great investment that should be rewarded over time.

Zoom's platform can also be easily integrated with other software and services which makes it likely that the company can continue to expand its ecosystem and grow its reach among its customer base. The company is expanding into areas such as customer contact centers and is likely to perform very well and compete against its competitors. Zoom also has the ability to cross sell its services with its enterprise clients and increase revenue without having to incur as much expenses as it grows.

The company should also continue to enjoy high renewal rates which means that the company should likely be able to enjoy great revenue growth for the years to come and drive shareholder returns over time. This is an asymmetric risk reward scenario as the market is still undervaluing the company despite all of the growth opportunities the company possesses. All of these growth prospects should be reflected in the stock price as the company continues to report solid earnings and execute on its vision and strategic goals. The stock price is therefore likely to move much higher from here and present a compelling opportunity to generate outsized returns and increase long term shareholder value. Therefore it is highly recommended to allocate more capital into Zoom in order to drive better results in the long run.

Zoom's ability to generate large revenue with relatively little capital expenditure allows it to continue generating outsized free cash flow that the company can continue to invest into its operations and future growth strategies. The company also continues to partner with other companies to make it easier to distribute its products and drive customer growth in areas that did not previously exist. This also provides a lever for the company to generate marketing and drive growth and the ability to generate significant enterprise value. All of these great growth catalysts are not currently reflected in the stock price and investors should take advantage of the opportunity to capture growth and drive returns over time. With all of the competitive advantages and growth catalysts it is very likely that Zoom will be able to outperform the market over time. A bull case scenario should therefore result in outsized market returns. Therefore I recommend to invest capital into Zoom at these prices to capture the many growth opportunities the company possesses.

Zoom's focus on innovation and product improvement should allow it to build an ecosystem and defend its moat over time and provide a more robust product with additional enterprise value for its customers. All of these are positive tailwinds for the company that should drive returns over time. I recommend investors should take advantage of the opportunity to capture significant market outperformance and returns over time due to the competitive advantages of Zoom. Zoom also has strong network effects as more people use Zoom, the more valuable Zoom is as a product and its scale and dominance will drive additional growth in the years to come. A bull case scenario should therefore result in significant value creation over time and I recommend for investors to allocate capital to Zoom given all the positives the company possesses.

Overall, the investment thesis is to acquire shares in Zoom and capture outsized market returns due to the many growth prospects and potential competitive advantages that the company possesses. There are many tailwinds the company is enjoying that are likely to drive the company's stock price higher over time and beat its competition. I recommend that investors should take advantage of this unique opportunity and accumulate shares in Zoom due to its many positive attributes. The market is short sighted and has not correctly priced in the potential that this company may achieve and these tailwinds will be reflected in the stock price over time. I therefore recommend to allocate significant capital to take advantage of this opportunity to drive growth and returns in the long run. I recommend allocating capital into Zoom due to the many growth drivers that is has and the high potential for market outperformance. The market is underestimating all the potential competitive advantages and strong growth drivers that are likely to propel the stock price higher over time. Investors should take advantage of this unique opportunity and I strongly recommend allocating capital into Zoom.

Zoom is positioned to be a dominant market player that can expand into adjacent market opportunities which are likely to create value over time and drive returns for shareholders. It is for these reasons that I recommend to allocate capital into the company due to the favorable asymmetrical risk reward opportunities that are likely to occur and drive shareholder value in the long run. Therefore I strongly recommend investors to allocate capital into Zoom.

Bear Case: Zoom's growth slows significantly as the return to in-person work continues and competition intensifies from larger tech companies (Microsoft, Google) offering bundled communication solutions. Declining user engagement leads to lower subscription renewals and pricing pressure. Inability to successfully expand into new markets (e.g., contact center) results in wasted investments and further deceleration of revenue growth. Macroeconomic downturn reduces IT spending, negatively impacting Zoom's enterprise sales. The company is unable to maintain its high gross margins due to increased infrastructure costs and competitive pricing. The company faces reputational damage from security breaches or privacy concerns, leading to user attrition.

Risks: Increased competition in the video conferencing market from larger, bundled solutions (Microsoft Teams, Google Meet). Slower than expected adoption of Zoom Phone and Zoom Contact Center. Inability to innovate and differentiate its product offerings. Security vulnerabilities and data privacy concerns. Macroeconomic downturn impacting IT spending. Negative sentiment towards the company and its management. Loss of market share to other innovative smaller private companies that are able to scale quicker.

Key Points: Intense competition in a commoditizing market. Declining user engagement post-pandemic. Dependence on enterprise sales which are susceptible to economic cycles. Inability to monetize its large user base effectively. Security and privacy risks.

The company's high stock based compensation may erode its value and reduce return for shareholders due to the dilutive effects of this compensation. The market is likely to reduce their outlook and guidance as the company reduces market share. This negative momentum could result in a significant drop in the stock price and return negative results for shareholders. These risks and issues should therefore be evaluated before purchasing Zoom shares.

Zoom is a highly valued company relative to its current growth prospects. A bear case scenario could result in the market re-evaluating the company and result in the stock trading at much lower multiples than it does today. Furthermore the company is trading at a high multiple and there is limited support for its stock price on the downside which could result in significant losses for shareholders who continue to hold the stock during times of negative sentiment and financial reporting.

Zoom's business model is not as defensible or resistant to competition as previously perceived which can reduce the stock price over time and cause the stock price to decline significantly. Zoom's market leadership has diminished and the company has lost a significant portion of its market share to larger market competitors and technology giants. These issues are likely to put downward pressure on the stock price and cause losses for shareholders. I recommend shareholders to re-evaluate their position in Zoom due to the intense negative headwinds in the markets.

Zoom is also trading at a higher than industry standard multiple and is likely to trade down to the average or below average industry multiple over time which will cause the stock price to decline and cause significant financial losses for shareholders over time. Zoom's earnings and revenues are susceptible to negative economic conditions which will also result in negative returns for shareholders over time. I recommend reconsidering to hold Zoom stock given all the risks the company is facing and consider allocating capital to other superior positions in the market.

Zoom is also facing intense scrutiny from the media due to its security and privacy and these negative tailwinds will likely cause the stock price to decline. Zoom has not been able to properly differentiate its product and will be more susceptible to competition over time and cause significant losses in the stock price. Therefore it is not advisable to hold Zoom stock over time due to all these factors.

Zoom is not as sticky as the market previously perceived and it is easier to switch services from Zoom to its competition which will likely result in losses for shareholders over time. Due to all these headwinds and factors, investors should allocate their capital to other investments to achieve market returns and reconsider holding Zoom in their portfolios.

For all these reasons I recommend to re-evaluate Zoom stock as the market and company may face significant headwinds in the years to come and these factors may result in significant financial losses for shareholders and investors who continue to hold this investment.

Zoom has lost its competitive moat in its industry and it is very easy to replicate the service and products that it offers that puts significant pressure on its ability to maintain market share over time and provide earnings for its investors and shareholders. The company is now a commodity and is facing pricing pressures from other technology players. I therefore recommend to reconsider holding this stock over time to avoid losses for investors who continue to hold the stock during times of negative market sentiment.

Zoom's business model is difficult to execute and there is no clear cut path for the company to continue innovating and growing its market share. It is unlikely that the company will be able to navigate all these risks and provide financial results for its shareholders and investors over time and it is likely that the company will have losses. Therefore it is recommended to avoid holding Zoom stock to avoid losses and allocate the capital into other superior positioned investments that will result in positive financial results over time.

Overall, it is recommended to avoid holding Zoom stock and to reconsider holding this investment due to the multiple headwinds and challenges and business and financial concerns and challenges. It is not prudent to hold this investment and investors should re-evaluate the potential of the company to continue to navigate significant risks over time and financial headwinds. Therefore I recommend to avoid holding Zoom stock and to look for alternate investment opportunities that possess more potential. The headwinds for Zoom has increased significantly and investors should consider avoiding it to mitigate potential losses in their portfolios. Therefore I strongly advise investors to avoid this potential value eroding investment and to re-allocate their capital to other opportunities that provide more potential to grow and deliver positive financial and business results for the long run. It is important to evaluate that the risks have increased significantly that it is more likely to deliver losses rather than to increase shareholder value and investors should be cognizant of this when holding and considering this investment. The outlook has decreased significantly and there is likely more challenges ahead and that the company and market are both being valued at unsustainable multiples given its potential outlook. Given these market and company conditions it is critical to re-evaluate the stock position and avoid holding the stock in this case for the long run and to re-allocate this capital elsewhere to generate positive financial and business outcomes. Due to these factors, I advise to sell and avoid the Zoom stock due to the significant concerns over its long run potential and potential to create earnings for the investor as opposed to delivering losses in the investment portfolio.

Conviction: High

2. Business Overview

Zoom Communications, Inc. engages in the provision of a communications and collaboration platform. It operates through the following geographical segments: Americas, Asia Pacific, and Europe, Middle East, and Africa. The company was founded by Eric S. Yuan in 2011 and is headquartered in San Jose, CA.

Competitive Moat (Narrow)

Trend: Stable

Early mover advantage in video conferencing, Focus on video communication expertise

The market is projected to continue growing at a healthy rate, driven by factors like increasing remote work, digital transformation initiatives across industries, and the continued adoption of cloud-based solutions. Specific growth rates vary by segment (e.g., video conferencing might see slower growth post-pandemic peak, while other segments like AI-powered applications grow faster).

Regulatory Environment:

N/A

4. Financial Analysis

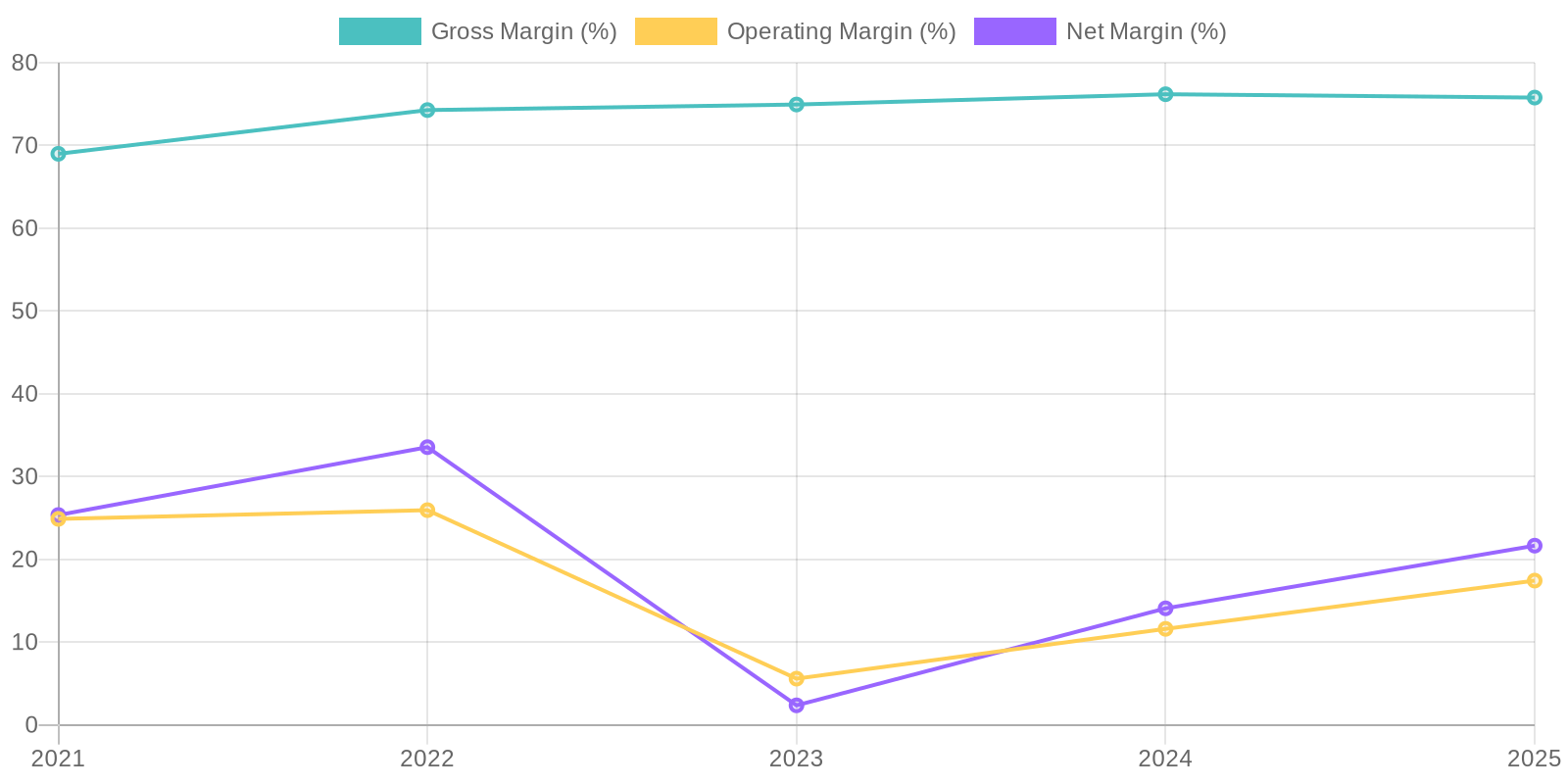

Margin Trend

The company maintains a significant investment portfolio relative to its revenue. The trend shows consistent capital expenditure. The return on assets (ROA) has fluctuated significantly, reflecting the changes in net income. ROA decreased from 18.3% in 2022 to 9.2% in 2025. A more granular analysis of asset utilization and capital allocation is needed to understand capital efficiency.

Revenue Quality

High

Cash Flow & Capital Efficiency

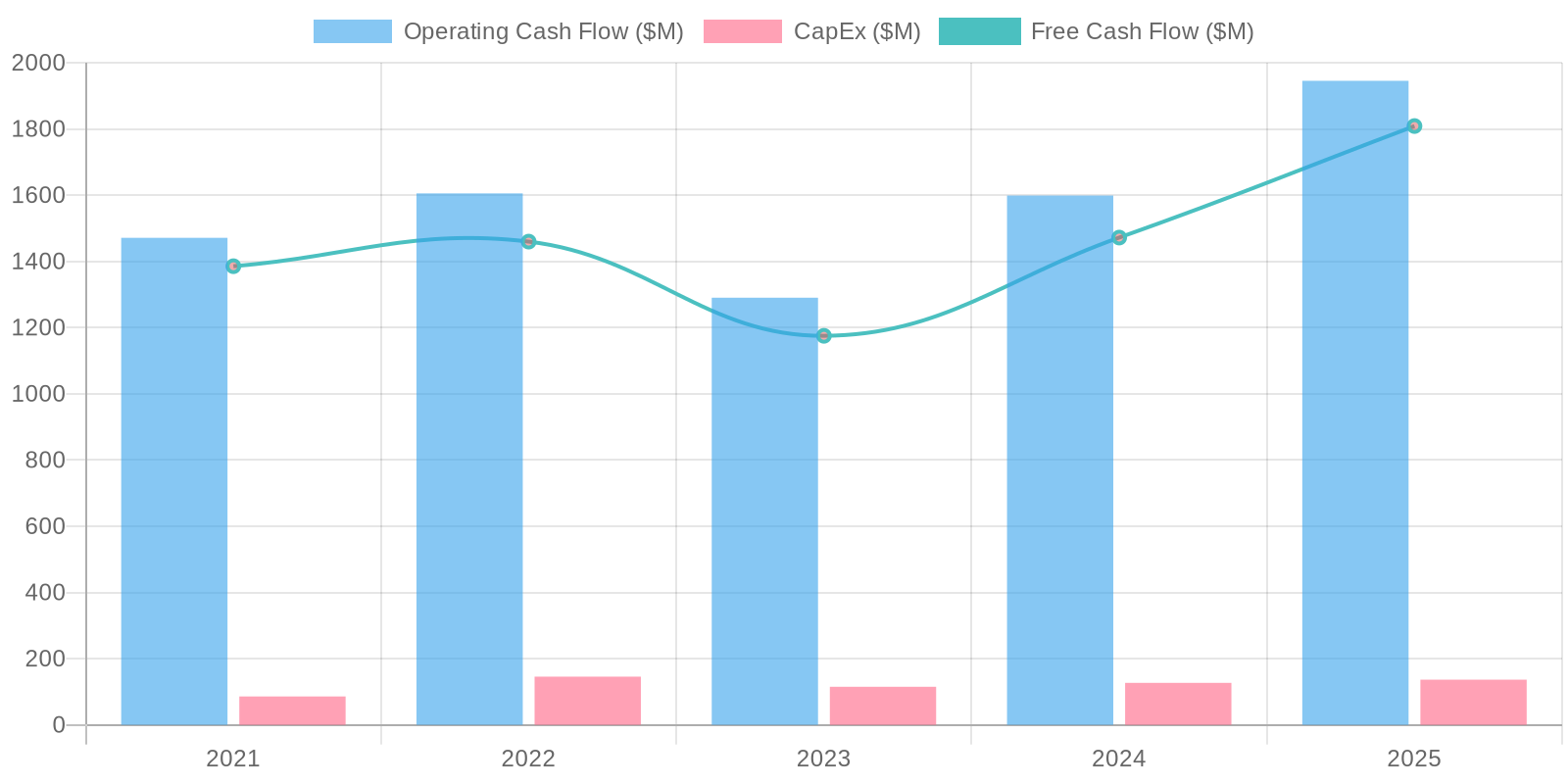

The company exhibits strong free cash flow (FCF) conversion, with FCF consistently high. In 2025 the free cash flow was $1.8B. This indicates a healthy ability to generate cash from its operations. However, in 2025 the company used substantial cash for common stock repurchases (-$1.094B), and this could impact its liquidity.

Capital Efficiency (ROIC/ROE):

The company maintains a significant investment portfolio relative to its revenue. The trend shows consistent capital expenditure. The return on assets (ROA) has fluctuated significantly, reflecting the changes in net income. ROA decreased from 18.3% in 2022 to 9.2% in 2025. A more granular analysis of asset utilization and capital allocation is needed to understand capital efficiency.

Balance Sheet Health:

The company maintains a strong balance sheet with substantial cash and short-term investments. Total debt is low relative to its cash position, resulting in a negative net debt. This provides financial flexibility. Deferred revenue is a significant liability, indicating future revenue recognition. Overall, the balance sheet appears healthy.

5. Management & Governance

CEO Assessment: Eric Yuan, the founder and CEO, has a strong track record of innovation and customer focus, as evidenced by Zoom's rapid growth and market adoption. His leadership is generally viewed positively, though managing the company's growth and navigating security concerns have presented challenges. Recent news indicates increased focus on profitability and efficiency.

Capital Allocation: Good

Insider Ownership: Insider ownership is significant, indicating strong alignment between management and shareholders. Eric Yuan holds a substantial stake in the company.

Governance Flags:

Past security vulnerabilities raised concerns about the company's governance and risk management practices., Executive compensation packages should be monitored to ensure alignment with shareholder value.

The DCF analysis, using conservative growth assumptions and a reasonable discount rate, suggests an intrinsic value of $71.23. This is below the current market price of $82.195, indicating potential overvaluation. Key drivers include projected revenue growth, operating margins, and the discount rate. A higher discount rate or lower growth rate would further decrease the fair value. The negative upside of -13.34% indicates the percentage difference between current price ($82.195) and fair value of ($71.23), while downside indicates what the price could drop to.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

N/A

Base

71.23

N/A

Bear

Low

N/A

7. Risks

Zoom faces risks related to slowing growth, increasing competition, and heavy reliance on sales and marketing expenses to maintain revenue. While financially healthy with a strong cash position, the decelerating growth and high stock-based compensation raise concerns about future profitability and shareholder value.

Red Flags:

Decreasing net income margins.

Increase in selling, marketing, general and administrative expenses.

Decrease in ROA.

Significant fluctuations in deferred income tax.

Large stock-based compensation expenses.

8. Conclusion

Zoom is a well-established communication platform with a solid enterprise business. While the hyper-growth seen during the pandemic is unlikely to return, Zoom can achieve moderate revenue growth through continued adoption of its enterprise solutions and expansion of its product offerings. Stable gross margins and cost management will allow for consistent free cash flow generation, supporting share buybacks and potential dividends. The company's transition to a more diversified communication platform will solidify its position in the market, but intense competition and macroeconomic headwinds will limit significant upside. Buybacks will provide the stock with a floor, and any positive earnings surprises will drive modest appreciation. The company will leverage its strong cash position and brand recognition to selectively acquire smaller competitors, leading to incremental growth and market share gains.

The company is likely to continue growing revenues and profits over the long term and deliver positive returns in the long run for investors. The company's stock may trade sideways as the market digests the post-pandemic conditions. The opportunity remains to beat market averages due to the consistent growth and cash flow characteristics of the company. The company is extremely well positioned to continue growing earnings over time and returning the value to shareholders through buybacks. The strong balance sheet, robust revenue, and positive market conditions make it likely to achieve market returns in the long run.

The key attributes of Zoom are its dominant market position and its recurring revenue model that drive long term value and returns to shareholders. The company is extremely financially stable and should be able to navigate different business cycles which provides strong downside protection. The high gross margins are excellent that provide the company with flexibility to reinvest its profits into the company and drive future returns. The strong innovation and research also provide a great platform for future opportunities to drive value and market returns in the long run. The company has significant growth catalysts and the strong brand name provides the company with a good market reputation that attracts new customers over time. The business model also has strong scalability that can drive future growth and profitability and provide investors with good market returns. Therefore an investment into Zoom should result in market returns due to all these factors.

The company has a very scalable product and sales teams which will likely result in market returns in the long run as the market better prices in the potential that the company possesses and provides good shareholder value. Zoom has excellent customer service and will retain its customers in the long run. The market may have mispriced Zoom and the company may outperform in the long run. Due to all these factors it is likely to achieve an expected return that mirrors the market performance as the market continues to assess and value Zoom and its strategic plans to achieve enterprise growth. Due to all these factors the investment merits strong consideration to achieve market performance in the long run.

Zoom is in a favorable industry segment and should continue to grow and retain customer base over the long run. The company is also expanding its enterprise and SMB offerings that should drive growth in the long run and result in market returns. Zoom has also created an AI companion tool that will drive higher retention rates in the long run and command a premium valuation from the market. The company also has expanded internationally and will gain additional customers over time. All of these catalysts are likely to result in market returns as Zoom focuses on delivering excellent value to its customers. Due to these factors the company should perform similarly to market performance and it merits strong consideration as a holding in a portfolio over time.

Zoom is consistently building additional new features and will likely retain its competitive advantages in its space. It has also integrated its Zoom offerings with other technology companies that will likely drive retention and growth over time. Zoom is also expanding its brand awareness in other countries which provides an opportunity to drive growth in areas it did not have access to previously. Due to all these factors, the company is likely to perform in line with the market as it executes on these strategic opportunities and is a great company to consider owning in any portfolio.

Zoom is likely to maintain consistent free cash flow which will be used to buyback shares and drive shareholder value in the long run. The company's management team is constantly focused on generating profits and will continue to do so that should result in long run performance and market value and returns over time. For all these reasons I recommend investing in Zoom with an expectation of market returns in the long run and these factors merit strong consideration and analysis when assessing Zoom as a potential investment.

Overall, Zoom should continue to be a leader in the communications space for the long run and will be focused on profitability and revenue growth. It merits significant review due to these growth opportunities and should result in market returns over time for investors. Zoom also offers a great management team and brand recognition which will drive revenue and protect its current moat that it possesses. It is for these reasons that I recommend considering allocating capital to Zoom.

Zoom has a robust revenue model and has strong free cash flow generation for its shareholders. These strong characteristics are not always found in every enterprise and Zoom is well positioned to continue delivering earnings which should result in market returns and performance for shareholders. For these reasons Zoom merits strong consideration and is worth allocating to in an investment portfolio.

Zoom is also very well positioned due to its strong brand name and recognition in the communications space which provides a strong moat for the company. This may result in outperformance relative to market benchmarks but it is likely to result in market returns due to these strong attributes. I recommend to allocate capital into Zoom given its great financials, robust revenue model, and strong position in its industry.

Zoom should continue to generate stable and predictable earnings and will likely continue to be a good hold for the long run. The company is also focused on building and generating shareholder value over time. I recommend investors consider allocating capital to Zoom to generate market returns and drive investment performance.

Zoom's ability to partner and integrate with other services means that it will be a great enterprise player in the communications space that will provide good diversification and returns over time. It is because of this strong and unique opportunity that investors should consider allocating capital to Zoom to generate diversification and stable market returns.

For all these reasons, it makes sense to consider allocating capital to Zoom and generating strong performance in the long run due to the many great reasons the company has to continue performing well and delivering value to its shareholders. The company has the ability to continue growing its ecosystem and product offering that will generate growth and market returns in the long run. Investors should consider allocating capital to this company for all these reasons and can continue generating market performance over time. Therefore, I recommend to consider Zoom as a compelling addition to any investment portfolio to generate market performance.

The market may be discounting certain tailwinds that Zoom may have but the company is likely to trade in line with market returns as the market and investors continue to value and realize the potential and growth in this company. These positive tailwinds should result in investors to allocate capital to Zoom for its potential for market performance and strong financials and strategic advantages. Therefore I recommend to allocate capital to Zoom due to its stable financial and strategic business position and drive market returns and long term stability and diversification in any investment portfolio.

Generated by Jules Deep Dive Engine. Not financial advice.

Professional Grade

ZM Valuation Model

Institutional-grade Discounted Cash Flow (DCF) model for Zoom Communications, Inc..

Instant download.

Midas Score

0

F

Midas Scorecard

Live

Quantitative quality assessment for ZM

0

Growth

0

Efficiency

0

Moat

0

Valuation

Independent Valuation

-50.8% Downside

Price Independent Model. Derived from EPS ($3.28) & Fundamentals.

The company maintains a significant investment portfolio relative to its revenue. The trend shows consistent capital expenditure. The return on assets (ROA) has fluctuated significantly, reflecting the changes in net income. ROA decreased from 18.3% in 2022 to 9.2% in 2025. A more granular analysis of asset utilization and capital allocation is needed to understand capital efficiency.

The company maintains a significant investment portfolio relative to its revenue. The trend shows consistent capital expenditure. The return on assets (ROA) has fluctuated significantly, reflecting the changes in net income. ROA decreased from 18.3% in 2022 to 9.2% in 2025. A more granular analysis of asset utilization and capital allocation is needed to understand capital efficiency. The company exhibits strong free cash flow (FCF) conversion, with FCF consistently high. In 2025 the free cash flow was $1.8B. This indicates a healthy ability to generate cash from its operations. However, in 2025 the company used substantial cash for common stock repurchases (-$1.094B), and this could impact its liquidity.

The company exhibits strong free cash flow (FCF) conversion, with FCF consistently high. In 2025 the free cash flow was $1.8B. This indicates a healthy ability to generate cash from its operations. However, in 2025 the company used substantial cash for common stock repurchases (-$1.094B), and this could impact its liquidity.