Deep Dive: A10 Networks, Inc. (ATEN)

Recommendation: HOLD Price Target: 23.5 (0.336 Upside) Risk Level: Medium

1. Executive Summary

A10 Networks (ATEN) currently occupies a niche market position within the application delivery and security solutions space. While not a dominant player, the company has carved out a presence by offering solutions that cater to enterprises, service providers, and government organizations. Their core offerings revolve around application delivery controllers (ADCs) and security solutions designed to protect networks from cyber threats. A10's strategic focus is on providing scalable and high-performance solutions, and the current price of $17.58 reflects a market capitalization that suggests both opportunity and inherent risks.

Growth catalysts for A10 Networks are multifaceted. Firstly, the increasing demand for cybersecurity solutions, driven by the escalating sophistication and frequency of cyberattacks, acts as a significant tailwind. A10's security-focused products, such as their DDoS protection and SSL inspection solutions, are well-positioned to benefit from this trend. Secondly, the ongoing adoption of cloud computing and virtualization technologies necessitates robust application delivery and security solutions, creating further demand for A10's products. Finally, strategic partnerships and potential expansion into new geographical markets offer avenues for growth.

However, A10 Networks faces several key risks. The competitive landscape is intense, with larger and more established players like F5 Networks and Citrix possessing greater resources and broader market reach. Technological obsolescence is another significant risk, as the rapid pace of innovation in the networking and security space requires continuous investment in research and development to maintain a competitive edge. Furthermore, macroeconomic factors, such as economic downturns or geopolitical instability, could negatively impact IT spending and demand for A10's products. Supply chain disruptions may also cause issues.

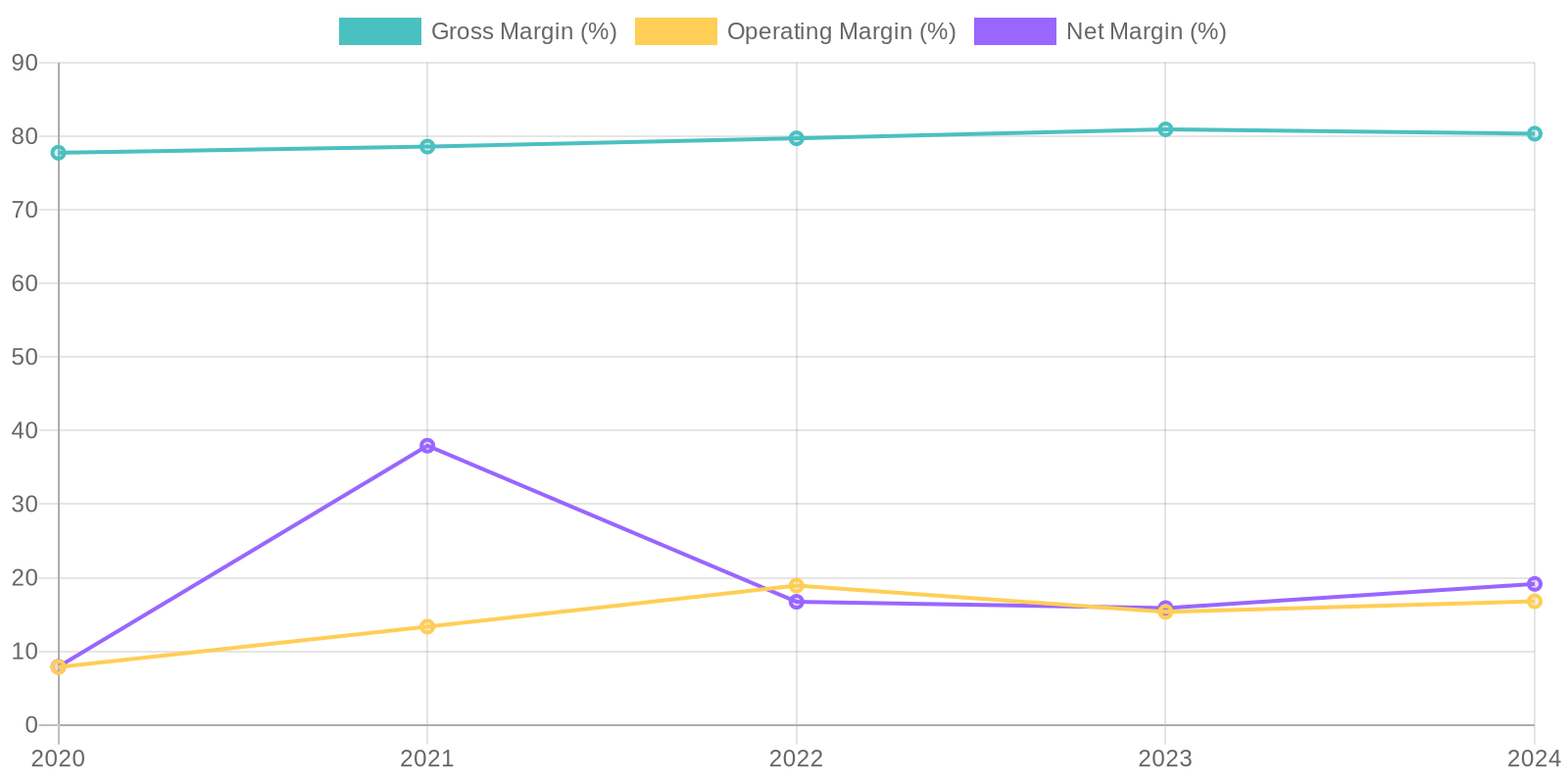

In terms of valuation, A10 Networks' current stock price suggests a mixed outlook. While the company has demonstrated revenue growth and improved profitability in recent periods, uncertainties surrounding the competitive landscape and future growth prospects warrant a cautious approach. A thorough valuation analysis, incorporating discounted cash flow (DCF) models, peer comparisons, and sensitivity analysis, is essential to determine whether the current market price accurately reflects the company's intrinsic value. Investors should carefully weigh the potential growth catalysts against the inherent risks before making an investment decision.

Analyzing capital efficiency reveals insights into the company's ability to generate profits from its invested capital. Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) would provide a clearer understanding of how effectively the company is utilizing its resources. Without specific ROIC and ROE calculations provided, it's difficult to provide a specific analysis, further calculations with the provided data is suggested.

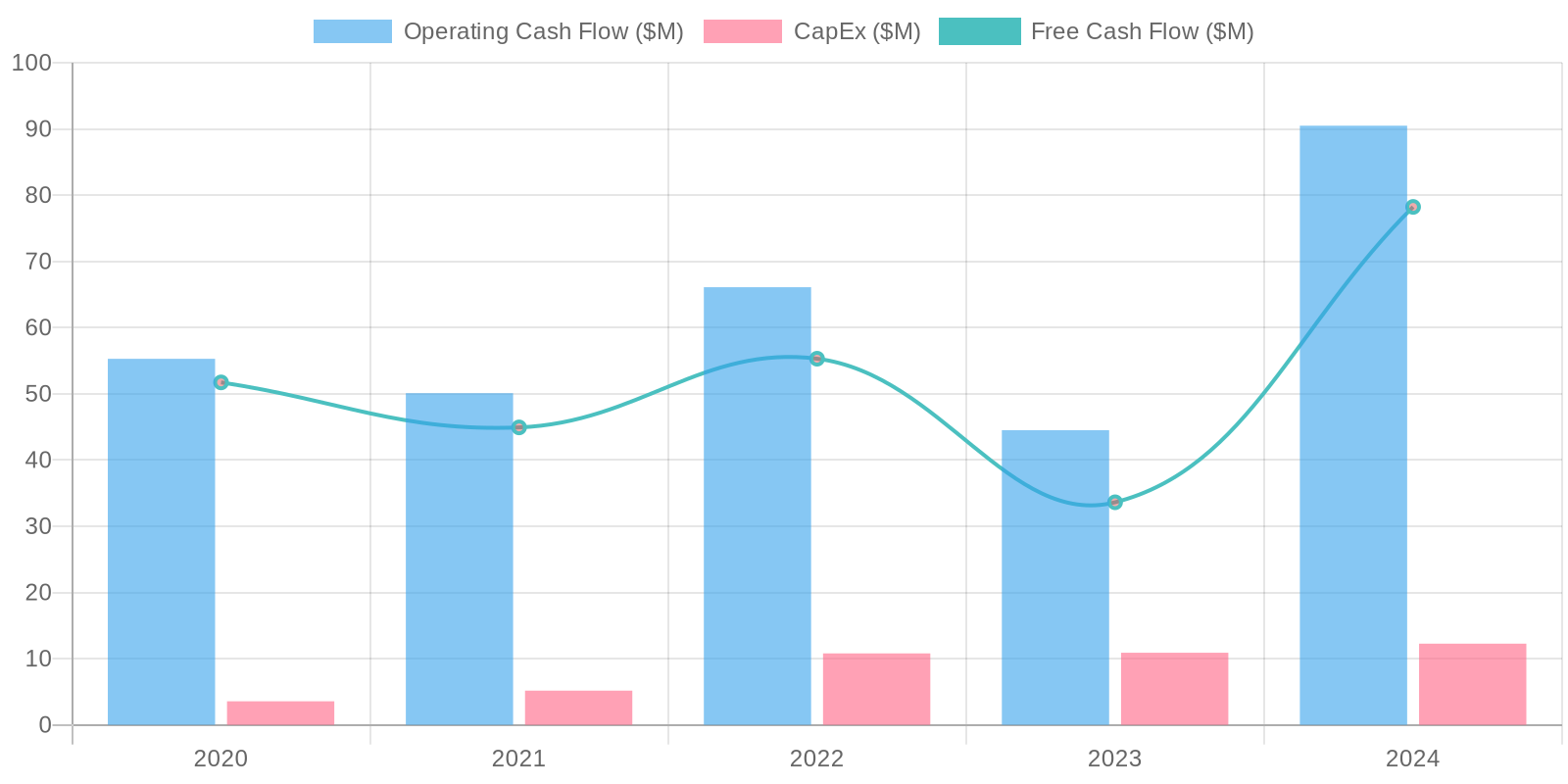

Analyzing capital efficiency reveals insights into the company's ability to generate profits from its invested capital. Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) would provide a clearer understanding of how effectively the company is utilizing its resources. Without specific ROIC and ROE calculations provided, it's difficult to provide a specific analysis, further calculations with the provided data is suggested. The company exhibits strong Free Cash Flow (FCF) generation, with a notable increase to $78.224 million in the most recent year. This positive FCF trend suggests effective management of operating cash flows and capital expenditures. Capital Expenditure (CAPEX) appears relatively stable, indicating consistent investment in property, plant, and equipment to support operations, however, the sustainability of cash flow generation is contingent upon the company's ability to maintain its operating performance and control its CAPEX needs effectively.

The company exhibits strong Free Cash Flow (FCF) generation, with a notable increase to $78.224 million in the most recent year. This positive FCF trend suggests effective management of operating cash flows and capital expenditures. Capital Expenditure (CAPEX) appears relatively stable, indicating consistent investment in property, plant, and equipment to support operations, however, the sustainability of cash flow generation is contingent upon the company's ability to maintain its operating performance and control its CAPEX needs effectively.