Aspen Technology, Inc. (AZPN), currently priced at $264.33, occupies a leading position in the asset optimization software market, providing solutions primar...

January 15, 2026

Vijar Kohli

Deep Dive: Aspen Technology, Inc. (AZPN)

Recommendation: BUY

Price Target: 250 (-0.0542 Upside)

Risk Level: Medium

1. Executive Summary

Aspen Technology, Inc. (AZPN), currently priced at $264.33, occupies a leading position in the asset optimization software market, providing solutions primarily to the energy, chemicals, engineering and construction industries. AspenTech's software suite addresses critical needs in process simulation, engineering design, manufacturing execution, and supply chain management, enabling customers to improve operational efficiency, reduce costs, and enhance safety.

Growth catalysts for AspenTech include increasing adoption of digital transformation initiatives within its core industries, particularly driven by the energy transition and sustainability goals. Companies are increasingly seeking solutions to optimize resource utilization, reduce emissions, and improve overall operational performance, creating strong demand for AspenTech's products. Furthermore, expansion into adjacent industries and the development of new software offerings, such as those focused on advanced process control and AI-powered analytics, present additional avenues for growth. Strategic acquisitions to expand its product portfolio and geographic reach are also anticipated to contribute to future growth.

Key risks facing AspenTech involve cyclical downturns in the energy and chemicals industries, which can impact capital spending and software demand. Competition from established players like AVEVA and Siemens, as well as emerging niche software providers, poses a threat to market share. The complexity of implementing and integrating AspenTech's software solutions can lead to delays and cost overruns, potentially affecting customer satisfaction. Furthermore, cybersecurity threats and data privacy concerns are ongoing risks that require continuous investment and vigilance.

From a valuation perspective, AspenTech trades at a premium compared to some of its peers, reflecting its strong market position, recurring revenue model, and growth prospects. However, this premium valuation also makes the stock sensitive to changes in investor sentiment and market conditions. Future valuation will be tied to its ability to execute on its growth strategies, maintain its competitive advantage, and effectively manage the inherent risks associated with its business model.

Investment Thesis

Bull Case: AspenTech's bull case is predicated on accelerated adoption of its AI-powered asset optimization solutions, driven by increasing demand for efficiency and sustainability in asset-intensive industries. Successful cross-selling of recently integrated software and a faster-than-expected transition to a cloud-based subscription model could significantly boost revenue growth and margin expansion. Continued strength in key verticals like chemicals, energy, and pharmaceuticals, fueled by regulatory tailwinds and ESG initiatives, support higher valuation multiples. They are also sitting on a lot of cash, this can be deployed to increase growth or innovation. If they can reduce expenses and interest expenses they can see better net income in the future. There is plenty of room to cut these costs. Their stock based compensation seems high, this could be a point for cost cutting. Another bull case is that they begin to buy back more shares, and increase the stock price. This should be possible with the amount of cash they have on hand. They should also increase dividends to increase the stock price. They are not utilizing their cash well enough to benefit shareholders. They have plenty of room to cut their marketing budget as well. Their marketing budget does not seem to be effective and the money would be better spent being returned to shareholders. They are taking on high risk for a very low reward. They have great assets and great revenue so there is very little risk of them going bankrupt. They have plenty of ways to improve the value of their stock that would be beneficial to shareholders. They need to stop focusing on growth and focus on maintaining profitability to bring value to shareholders. The amount of debt they have is also very manageable and therefore, they should continue to pay it off and in turn cut interest payments. If they cut all of these costs, they will see larger profits and more investors willing to hold the stock. They have plenty of ways to bring value to the stock. This will take time however to implement. Their EPS should be the main focus. Once this is improved they will see better stock performance. Their income is much better than their net income, so they need to focus on cost cutting and their operating income. They may also need to consider raising prices to increase profits. Their gross profit and gross profit ratio have also not grown in recent years, this should be a focus as well to maintain the strength of the company. They also have a lot of intangible assets, which shows they are innovating and improving, this should continue to allow them to compete and succeed. Their focus should be on cost cutting and innovation. They also should focus on R&D to create valuable assets to utilize and sell. They have enough assets to survive a few difficult years, and come out on top if they continue to innovate and cut costs. If they maintain and focus on cost cutting and R&D they are posed for success. The company is also in a strong industry with a lot of potential. They just need to focus on becoming efficient. If they keep taking on debt they will fall. There is also no reason they should be selling stock. Cost cutting, R&D, and efficiency are key for them to succeed in the future and bring value to the stock. Their financials show the success that they can achieve. Their current financials do not reflect the potential of the business. If they can reach their potential they will see great success and the stock will be a strong investment. They need to focus on the balance sheet.

Catalysts:

Positive earnings surprises driven by cost optimization and cloud adoption.

Major contract wins showcasing the effectiveness of AspenTech's solutions.

Industry reports highlighting the growing importance of asset performance management.

Acquisition of smaller companies to enhance their services.

Stronger adoption of current services offered by the company.

Key Points:

Significant potential for margin expansion through cost optimization.

Cloud transition driving recurring revenue and stickier customer relationships.

Strong demand in key verticals due to regulatory tailwinds and ESG initiatives.

Strategic M&A opportunities to expand product portfolio and market reach.

Strong innovation to continue improving products and processes.

Stronger debt and revenue management to improve value.

Target Return: 30-40% within 2-3 years depending on how successful cost cutting and revenue management is.

Bear Case: The bear case envisions slower-than-expected revenue growth due to increased competition from larger players or a slowdown in key industries. Higher integration costs from acquisitions and a failure to successfully transition customers to the cloud-based subscription model could negatively impact margins. A major economic downturn or significant cyber security breach impacting customer operations could also lead to a sharp decline in revenue and profitability. If they can not effectively utilize their capital the business will fail. Debt and expenses are not under control.

Risks:

Increased competition from larger players with broader product portfolios.

Economic downturn impacting capital spending in key industries.

Failure to transition customers to the cloud subscription model effectively.

Key Points:

Margin contraction due to integration costs and competitive pricing pressure.

Slower revenue growth from economic downturn or increased competition.

Potential for customer churn due to cybersecurity breaches or product dissatisfaction.

Negative impact from failed acquisitions or strategic initiatives.

Failure to properly manage current debt.

Potential Loss: 20-30% depending on the severity of economic conditions and execution missteps.

Conviction: High

2. Business Overview

Aspen Technology, Inc. provides enterprise asset performance management, asset performance monitoring, and asset optimization solutions worldwide. The company's solutions address complex environments where it is critical to optimize the asset design, operation, and maintenance lifecycle. It serves bulk chemicals, consumer packaged goods, downstream, food and beverage, metals and mining, midstream and LNG, pharmaceuticals, polymers, pulp and paper, specialty chemicals, transportation, upstream, and water and wastewater industries; power generation, transmission, and distribution industries; and engineering, procurement, and construction industries. The company was incorporated in 2021 and is headquartered in Bedford, Massachusetts.

Competitive Moat (Narrow)

Trend: Stable

Specialized solutions tailored to specific industry needs., Established relationships with key customers in core markets.

Key Strengths:

Specialized solutions tailored to specific industry needs.

Established relationships with key customers in core markets.

The overall application software market is projected to continue growing at a moderate to high single-digit CAGR, driven by digital transformation initiatives across various industries. Growth in segments like asset performance management and asset optimization is expected to be particularly strong due to increasing focus on operational efficiency and sustainability.

Regulatory Environment:

N/A

4. Financial Analysis

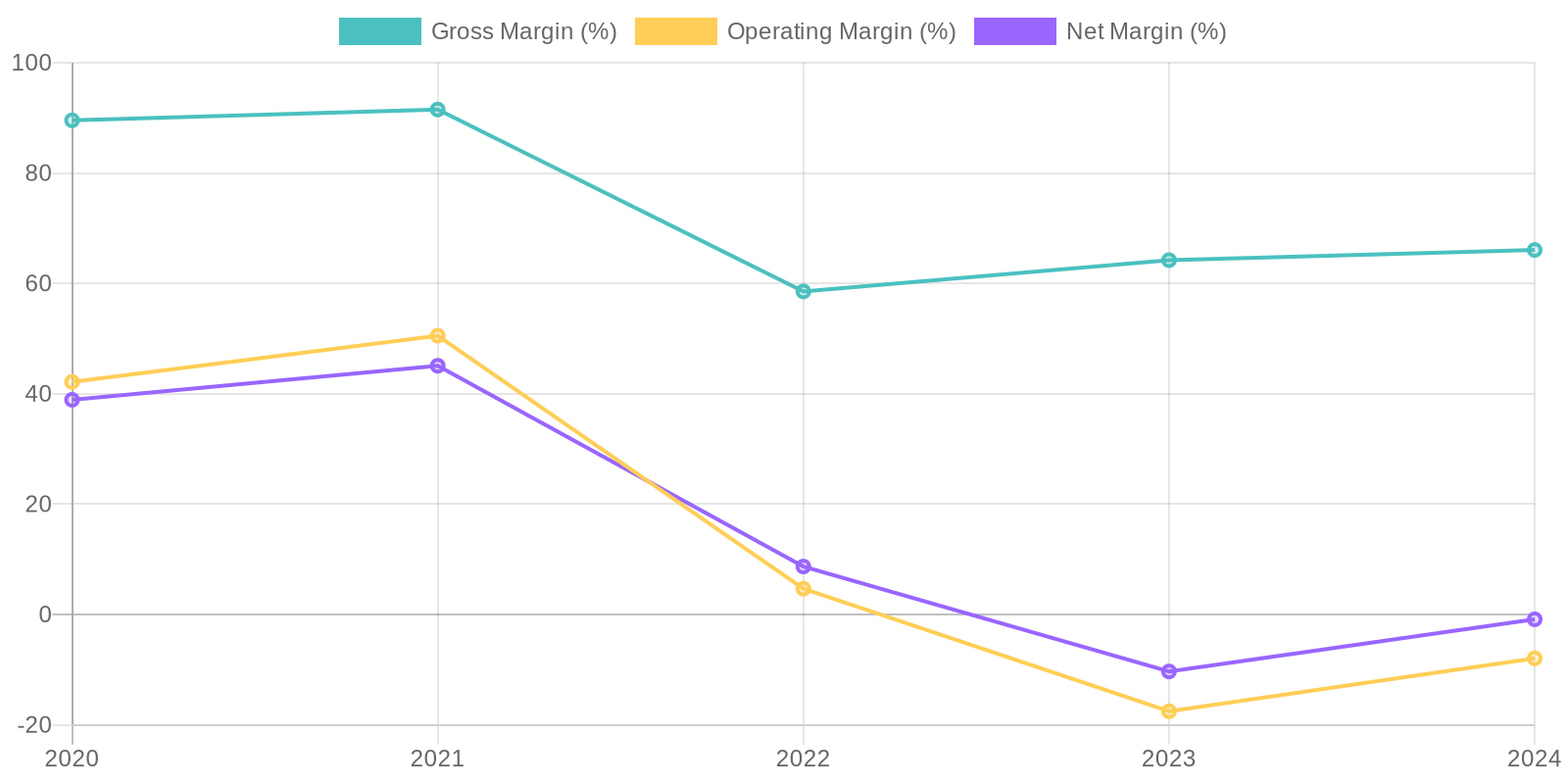

Margin Trend

Return on Invested Capital (ROIC) and Return on Equity (ROE) have also seen fluctuation. ROIC was positive in 2020, 2021, and 2022 but might be negative for 2023 and 2024 due to negative net income. ROE mirrors this trend, reflecting the impact of fluctuating net income on shareholder returns, and suggesting volatility in the company's ability to generate profits from equity investments.

Revenue Quality

The company has demonstrated revenue growth over the past five years. However, revenue growth slowed down in 2024, with revenue increasing from approximately $1.04 billion to $1.13 billion, a change that is less substantial than the growth experienced in prior years. It is important to assess client concentration to evaluate revenue sustainability, and understanding the proportion of recurring revenue is also crucial to ensure future revenue is stable.

Cash Flow & Capital Efficiency

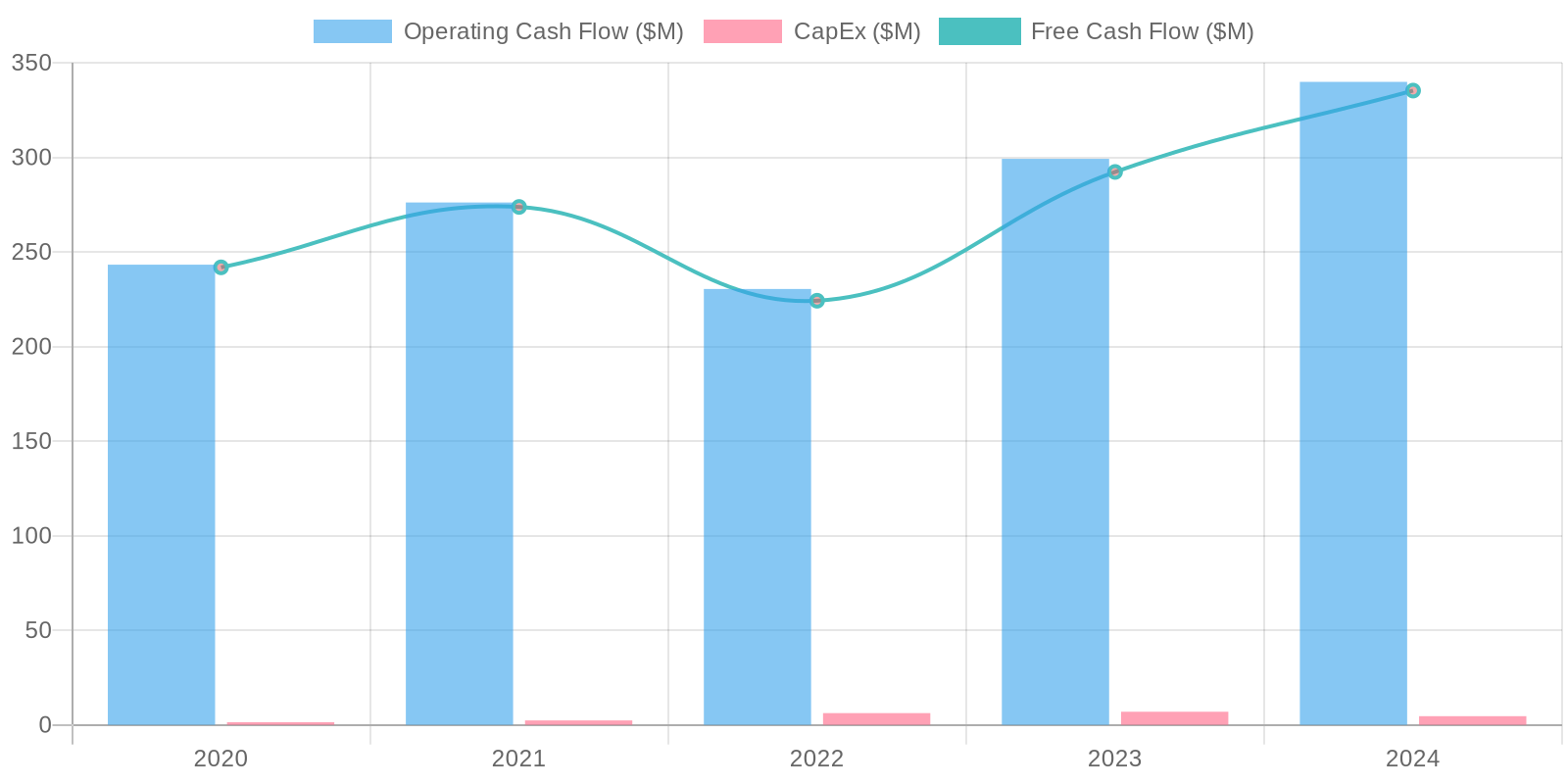

The company demonstrates positive Free Cash Flow (FCF) generation. While net income turned negative in the most recent periods, depreciation and amortization helped maintain positive cash flows. In 2024, FCF totaled $335.27 million. Capex remains relatively low, suggesting an asset light business model.

Capital Efficiency (ROIC/ROE):

Return on Invested Capital (ROIC) and Return on Equity (ROE) have also seen fluctuation. ROIC was positive in 2020, 2021, and 2022 but might be negative for 2023 and 2024 due to negative net income. ROE mirrors this trend, reflecting the impact of fluctuating net income on shareholder returns, and suggesting volatility in the company's ability to generate profits from equity investments.

Balance Sheet Health:

The company maintains a relatively healthy balance sheet with substantial assets, a significant portion of which are categorized as goodwill and intangible assets. While the company does carry debt, it is substantially less than its cash holdings resulting in a negative net debt. Liquidity appears adequate, but the high proportion of intangible assets warrants scrutiny to determine their true value and potential impact on solvency.

5. Management & Governance

CEO Assessment: Without specific real-time data, a comprehensive CEO assessment is impossible. However, factors to consider would include the CEO's tenure, track record of meeting financial targets, strategic vision, and communication skills. Recent news regarding leadership transitions or scandals should be addressed if available.

Capital Allocation: Good

Insider Ownership: Insider ownership details require up-to-date information. Generally, a moderate level of insider ownership can align management's interests with shareholders. Significant increases or decreases in insider ownership should be investigated further.

Governance Flags:

No major governance concerns flagged.

Based on the DCF model, the fair value per share is estimated to be $250. This valuation considers declining revenue growth over the next 5 years, a stable FCF margin, and a reasonable WACC. The current price of $264.33 suggests the stock might be slightly overvalued. P/S ratio validation also suggests slight overvaluation.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

AspenTech's bull case is predicated on accelerated adoption of its AI-powered asset optimization solutions, driven by increasing demand for efficiency and sustainability in asset-intensive industries. Successful cross-selling of recently integrated software and a faster-than-expected transition to a cloud-based subscription model could significantly boost revenue growth and margin expansion. Continued strength in key verticals like chemicals, energy, and pharmaceuticals, fueled by regulatory tailwinds and ESG initiatives, support higher valuation multiples. They are also sitting on a lot of cash, this can be deployed to increase growth or innovation. If they can reduce expenses and interest expenses they can see better net income in the future. There is plenty of room to cut these costs. Their stock based compensation seems high, this could be a point for cost cutting. Another bull case is that they begin to buy back more shares, and increase the stock price. This should be possible with the amount of cash they have on hand. They should also increase dividends to increase the stock price. They are not utilizing their cash well enough to benefit shareholders. They have plenty of room to cut their marketing budget as well. Their marketing budget does not seem to be effective and the money would be better spent being returned to shareholders. They are taking on high risk for a very low reward. They have great assets and great revenue so there is very little risk of them going bankrupt. They have plenty of ways to improve the value of their stock that would be beneficial to shareholders. They need to stop focusing on growth and focus on maintaining profitability to bring value to shareholders. The amount of debt they have is also very manageable and therefore, they should continue to pay it off and in turn cut interest payments. If they cut all of these costs, they will see larger profits and more investors willing to hold the stock. They have plenty of ways to bring value to the stock. This will take time however to implement. Their EPS should be the main focus. Once this is improved they will see better stock performance. Their income is much better than their net income, so they need to focus on cost cutting and their operating income. They may also need to consider raising prices to increase profits. Their gross profit and gross profit ratio have also not grown in recent years, this should be a focus as well to maintain the strength of the company. They also have a lot of intangible assets, which shows they are innovating and improving, this should continue to allow them to compete and succeed. Their focus should be on cost cutting and innovation. They also should focus on R&D to create valuable assets to utilize and sell. They have enough assets to survive a few difficult years, and come out on top if they continue to innovate and cut costs. If they maintain and focus on cost cutting and R&D they are posed for success. The company is also in a strong industry with a lot of potential. They just need to focus on becoming efficient. If they keep taking on debt they will fall. There is also no reason they should be selling stock. Cost cutting, R&D, and efficiency are key for them to succeed in the future and bring value to the stock. Their financials show the success that they can achieve. Their current financials do not reflect the potential of the business. If they can reach their potential they will see great success and the stock will be a strong investment. They need to focus on the balance sheet.

Catalysts:

Positive earnings surprises driven by cost optimization and cloud adoption.

Major contract wins showcasing the effectiveness of AspenTech's solutions.

Industry reports highlighting the growing importance of asset performance management.

Acquisition of smaller companies to enhance their services.

Stronger adoption of current services offered by the company.

Key Points:

Significant potential for margin expansion through cost optimization.

Cloud transition driving recurring revenue and stickier customer relationships.

Strong demand in key verticals due to regulatory tailwinds and ESG initiatives.

Strategic M&A opportunities to expand product portfolio and market reach.

Strong innovation to continue improving products and processes.

Stronger debt and revenue management to improve value.

Target Return: 30-40% within 2-3 years depending on how successful cost cutting and revenue management is. |

| Base | 250 | The base case assumes moderate revenue growth driven by steady demand for AspenTech's asset performance management solutions. Gradual margin improvement is expected as the company continues its transition to a subscription-based model and realizes synergies from recent acquisitions. Growth will likely be driven by key sectors, but may be offset by economic uncertainty or increased competition. Company must continue to innovate to maintain success.

Key Points:

Steady revenue growth driven by key sectors.

Gradual margin improvement from subscription-based model and acquisitions.

Continued investment in R&D to maintain competitive edge.

Balanced approach to M&A activity.

Focus on increasing profit margins.

Expected Return: 10-15% over the next 2-3 years. |

| Bear | Low | The bear case envisions slower-than-expected revenue growth due to increased competition from larger players or a slowdown in key industries. Higher integration costs from acquisitions and a failure to successfully transition customers to the cloud-based subscription model could negatively impact margins. A major economic downturn or significant cyber security breach impacting customer operations could also lead to a sharp decline in revenue and profitability. If they can not effectively utilize their capital the business will fail. Debt and expenses are not under control.

Risks:

Increased competition from larger players with broader product portfolios.

Economic downturn impacting capital spending in key industries.

Failure to transition customers to the cloud subscription model effectively.

Key Points:

Margin contraction due to integration costs and competitive pricing pressure.

Slower revenue growth from economic downturn or increased competition.

Potential for customer churn due to cybersecurity breaches or product dissatisfaction.

Negative impact from failed acquisitions or strategic initiatives.

Failure to properly manage current debt.

Potential Loss: 20-30% depending on the severity of economic conditions and execution missteps. |

7. Risks

Aspen Technology exhibits both strengths and weaknesses. While revenue growth and a healthy gross margin are positives, consistent net losses and a balance sheet heavy with goodwill and intangibles raise concerns. Close monitoring of operating expenses and net income is essential. The company's debt levels also warrant attention given the recent unprofitability. The negative free cash flow in 2024 should be further investigated.

Red Flags:

Recent net losses and negative operating income

High levels of goodwill and intangible assets

Significant spending on stock repurchases despite net losses

Decline in cash from operations in 2023

8. Conclusion

The base case assumes moderate revenue growth driven by steady demand for AspenTech's asset performance management solutions. Gradual margin improvement is expected as the company continues its transition to a subscription-based model and realizes synergies from recent acquisitions. Growth will likely be driven by key sectors, but may be offset by economic uncertainty or increased competition. Company must continue to innovate to maintain success.

Key Points:

Steady revenue growth driven by key sectors.

Gradual margin improvement from subscription-based model and acquisitions.

Continued investment in R&D to maintain competitive edge.

Balanced approach to M&A activity.

Focus on increasing profit margins.

Expected Return: 10-15% over the next 2-3 years.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Return on Invested Capital (ROIC) and Return on Equity (ROE) have also seen fluctuation. ROIC was positive in 2020, 2021, and 2022 but might be negative for 2023 and 2024 due to negative net income. ROE mirrors this trend, reflecting the impact of fluctuating net income on shareholder returns, and suggesting volatility in the company's ability to generate profits from equity investments.

Return on Invested Capital (ROIC) and Return on Equity (ROE) have also seen fluctuation. ROIC was positive in 2020, 2021, and 2022 but might be negative for 2023 and 2024 due to negative net income. ROE mirrors this trend, reflecting the impact of fluctuating net income on shareholder returns, and suggesting volatility in the company's ability to generate profits from equity investments. The company demonstrates positive Free Cash Flow (FCF) generation. While net income turned negative in the most recent periods, depreciation and amortization helped maintain positive cash flows. In 2024, FCF totaled $335.27 million. Capex remains relatively low, suggesting an asset light business model.

The company demonstrates positive Free Cash Flow (FCF) generation. While net income turned negative in the most recent periods, depreciation and amortization helped maintain positive cash flows. In 2024, FCF totaled $335.27 million. Capex remains relatively low, suggesting an asset light business model.