Deep Dive: Bandwidth Inc. (BAND)

Recommendation: HOLD Price Target: 15.75 (16.41 Upside) Risk Level: Medium

1. Executive Summary

Bandwidth Inc. (BAND), currently trading at $13.53, operates in the Communications Platform as a Service (CPaaS) market, providing cloud-based communication APIs for software developers. While an early leader, Bandwidth's market position has become increasingly challenged by larger, well-funded competitors like Twilio and Vonage (now part of Ericsson). They primarily focus on providing communication services (voice, messaging, and 911 access) to enterprises, enabling them to embed communication functionalities directly into their applications and workflows. The company's historical strength lies in its direct ownership of a significant portion of its network infrastructure, giving it some control over quality and cost. However, recent performance indicates struggles to maintain market share and achieve consistent profitability.

Growth catalysts for Bandwidth are limited but potentially include expansion of their enterprise customer base, strategic partnerships with complementary technology providers, and successful navigation of regulatory complexities, particularly related to 911 access. The increasing adoption of cloud communications and the growing demand for embedded communication features within applications remain secular tailwinds for the broader CPaaS market, which Bandwidth could potentially leverage with effective strategy execution. Furthermore, successful innovation in new product offerings or targeted solutions could rejuvenate growth.

Key risks confronting Bandwidth are substantial. Intense competition within the CPaaS market is a primary concern, with competitors possessing greater scale, resources, and innovation capabilities. Customer concentration poses another significant risk, as the loss of a major client could materially impact revenue. Regulatory hurdles, particularly in the area of 911 compliance, can also lead to increased costs and operational challenges. The company's debt load and limited profitability create financial risks, constraining their ability to invest in growth and innovation. Furthermore, technological advancements by competitors could render Bandwidth's existing infrastructure and offerings less competitive.

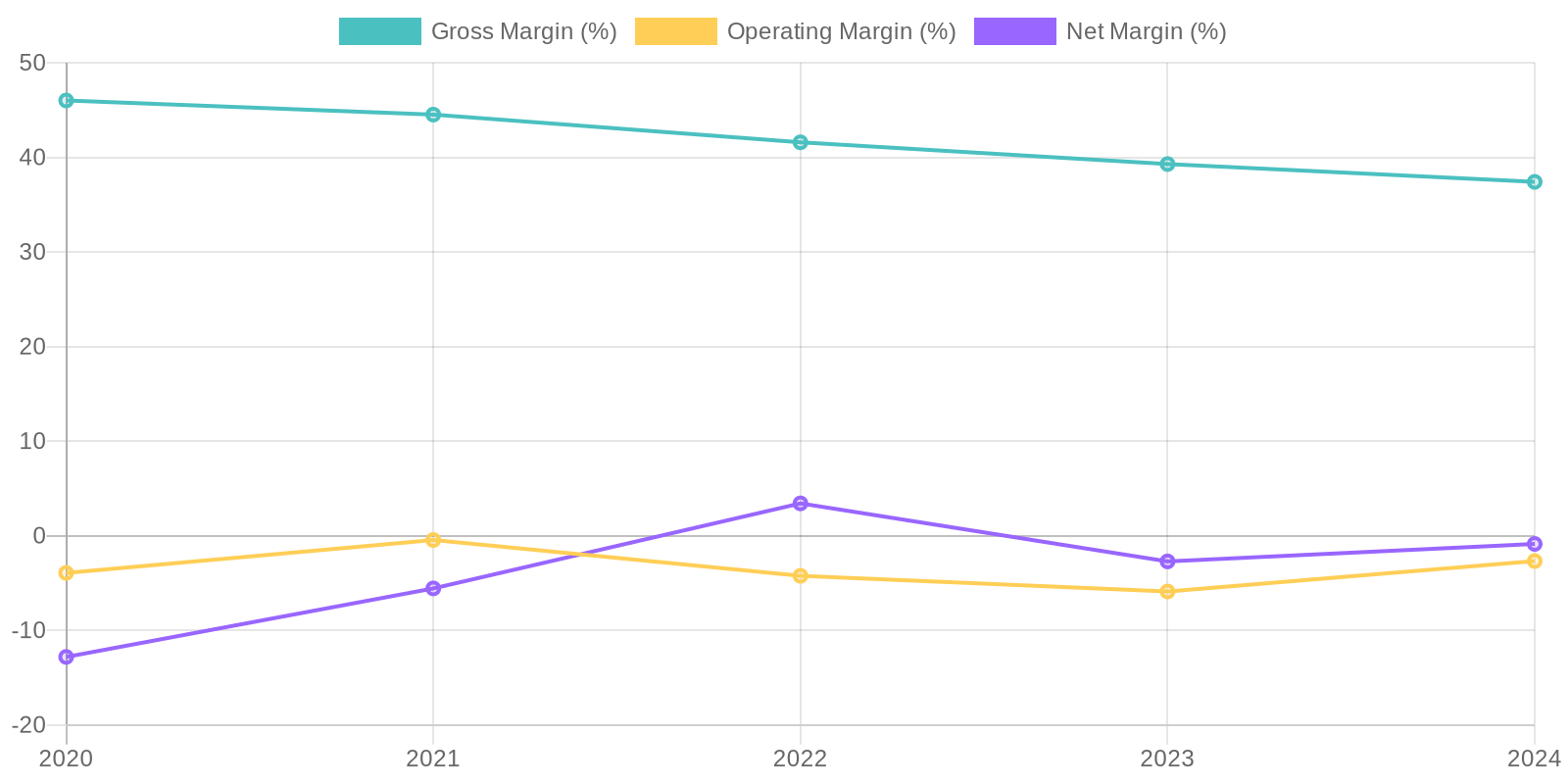

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) is crucial, but the provided data shows inconsistent profitability and negative income in several years, making a standard ROIC/ROE analysis less meaningful without further context. The negative net income figures in 2020, 2021, 2023 and 2024 directly impact these metrics, suggesting inefficient capital allocation or operational challenges. Deeper investigation into asset utilization and capital structure is needed to understand the true drivers behind these returns.

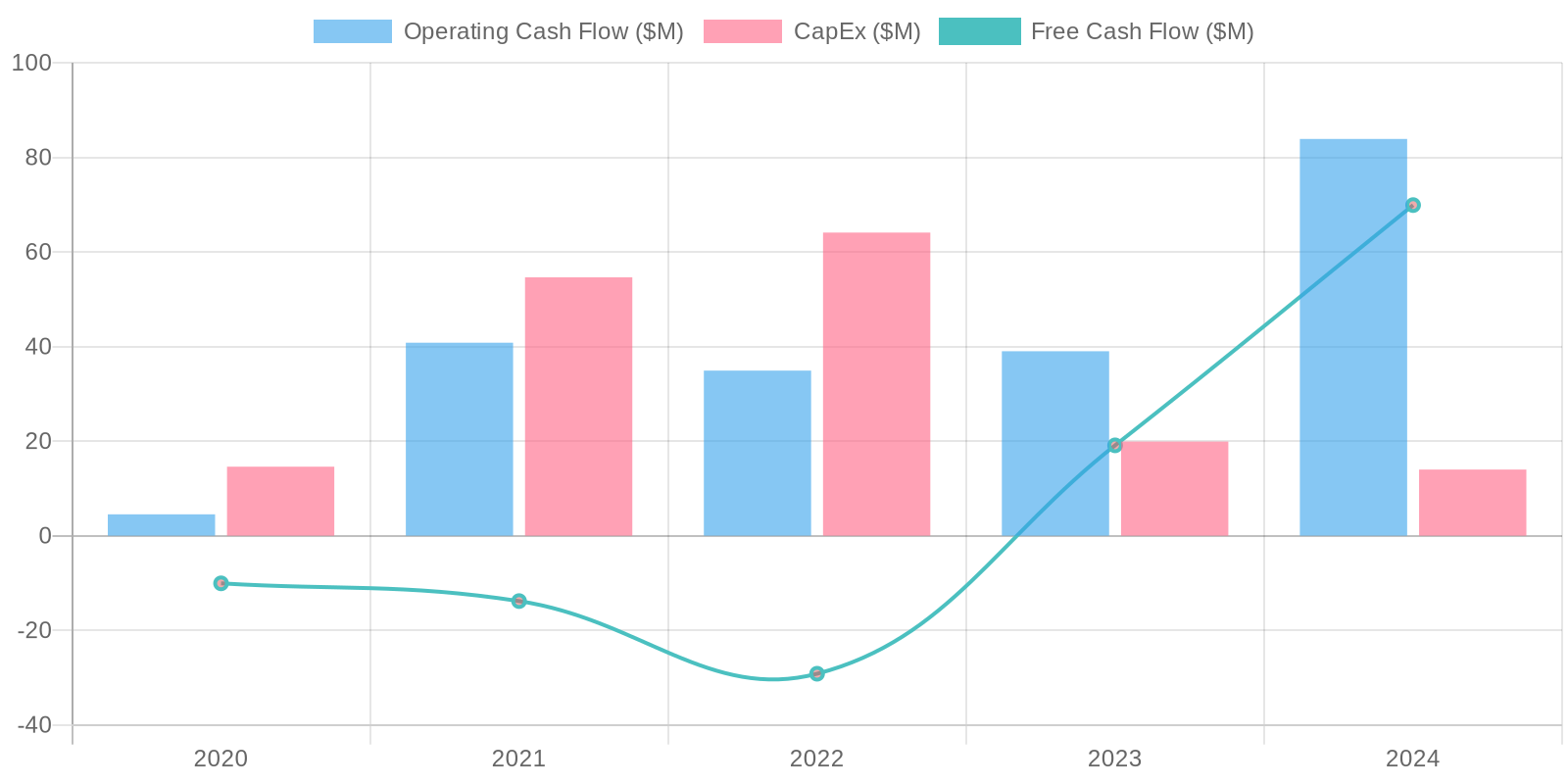

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) is crucial, but the provided data shows inconsistent profitability and negative income in several years, making a standard ROIC/ROE analysis less meaningful without further context. The negative net income figures in 2020, 2021, 2023 and 2024 directly impact these metrics, suggesting inefficient capital allocation or operational challenges. Deeper investigation into asset utilization and capital structure is needed to understand the true drivers behind these returns. The company's free cash flow (FCF) generation has been volatile, with a recent increase to $69.9 million in 2024 following periods of lower or even negative FCF. Capital expenditures (CAPEX) appear relatively controlled, but the variability in FCF suggests potential inconsistencies in operational efficiency or working capital management. Analyzing the components of operating cash flow, especially changes in working capital, is important to understand the underlying drivers of cash flow generation.

The company's free cash flow (FCF) generation has been volatile, with a recent increase to $69.9 million in 2024 following periods of lower or even negative FCF. Capital expenditures (CAPEX) appear relatively controlled, but the variability in FCF suggests potential inconsistencies in operational efficiency or working capital management. Analyzing the components of operating cash flow, especially changes in working capital, is important to understand the underlying drivers of cash flow generation.