Backblaze, Inc. (BLZE) operates in the cloud storage market, providing simple and affordable cloud storage and backup services primarily to small and medium-...

January 15, 2026

Vijar Kohli

Deep Dive: Backblaze, Inc. (BLZE)

Recommendation: HOLD

Price Target: 3.82 (-0.22 Upside)

Risk Level: Medium

1. Executive Summary

Backblaze, Inc. (BLZE) operates in the cloud storage market, providing simple and affordable cloud storage and backup services primarily to small and medium-sized businesses (SMBs) and individuals. While competing with larger players like Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform (GCP), Backblaze differentiates itself through its focus on simplicity, ease of use, transparent pricing, and a strong reputation for customer service. Its market position is primarily as a value-oriented provider, attracting customers who prioritize cost-effectiveness and straightforward solutions over the feature-rich ecosystems offered by larger competitors. The company has successfully carved out a niche by catering to a specific segment of the market seeking accessible and reliable cloud storage solutions.

Several growth catalysts could propel Backblaze forward. Firstly, the increasing demand for cloud storage solutions generally, driven by data generation and digital transformation across various industries, provides a favorable macro environment. Secondly, Backblaze's efficient cost structure and transparent pricing model positions it well to capture market share from customers dissatisfied with the complexity and cost of larger cloud providers. Thirdly, the company's ongoing investments in product development, such as enhancements to its object storage and backup services, and expansion into adjacent areas like server backup, can attract new customers and increase retention. Strategic partnerships and integrations with other software platforms also represent a potential avenue for growth.

Key risks facing Backblaze include intense competition from larger, well-resourced cloud providers. These companies possess significant scale, allowing them to offer aggressive pricing and bundle storage solutions with other services. Furthermore, Backblaze's reliance on third-party infrastructure providers, such as data centers, exposes it to potential disruptions and cost increases. A failure to maintain its competitive pricing advantage or to innovate and adapt to changing customer needs could also negatively impact its growth prospects. Economic downturns could reduce SMB spending on cloud services, impacting revenue. Data breaches or security incidents could damage the company's reputation and erode customer trust.

At a current price of $4.89, assessing Backblaze's valuation requires careful consideration of its growth potential and risk profile. While the company exhibits promising growth catalysts and a differentiated market position, the competitive landscape presents a significant challenge. A valuation based on revenue multiples, comparing Backblaze to other cloud storage and SaaS companies, suggests potential upside if the company can maintain its growth trajectory and improve profitability. However, a discounted cash flow (DCF) analysis would be prudent to account for the inherent risks and uncertainties associated with the company's future performance. Ultimately, the attractiveness of Backblaze's valuation depends on an investor's assessment of its ability to execute its growth strategy and navigate the competitive environment, along with their risk tolerance.

Investment Thesis

Bull Case: N/A

Bear Case: N/A

Conviction: High

2. Business Overview

Backblaze, Inc., a storage cloud platform, provides businesses and consumers cloud services to store, use, and protect data in the United States and internationally. The company offers cloud services through a web-scale software infrastructure built on commodity hardware. It also provides Backblaze B2 Cloud Storage, which enables customers to store data, developers to build applications, and partners to expand their use cases. This service is offered as a consumption-based Infrastructure-as-a-Service (IaaS) and serves use cases, such as backups, multi-cloud, application development, and ransomware protection. In addition, the company offers Backblaze Computer Backup that automatically backs up data from laptops and desktops for businesses and individuals, which provides a subscription-based Software-as-a-Service and serves use cases, including computer backup, ransomware protection, theft and loss protection, and remote access. It serves the public cloud IaaS storage and Data-Protection-as-a-Service markets. The company was incorporated in 2007 and is headquartered in San Mateo, California.

Competitive Moat (Narrow)

Trend: Stable

Cost-effective solution for specific use cases (backup, archiving)., Ease of integration and use compared to larger, more complex platforms., Strong focus on customer support and satisfaction (relative to larger players).

Key Strengths:

Cost-effective solution for specific use cases (backup, archiving).

Ease of integration and use compared to larger, more complex platforms.

Strong focus on customer support and satisfaction (relative to larger players).

The cloud storage and data protection markets are projected to continue growing at a rapid pace driven by increasing data volumes, the need for robust backup and disaster recovery solutions, and the shift towards cloud-based infrastructure. Specific growth rates can be found in the aforementioned market reports. Expect double-digit percentage growth for the foreseeable future.

Regulatory Environment:

N/A

4. Financial Analysis

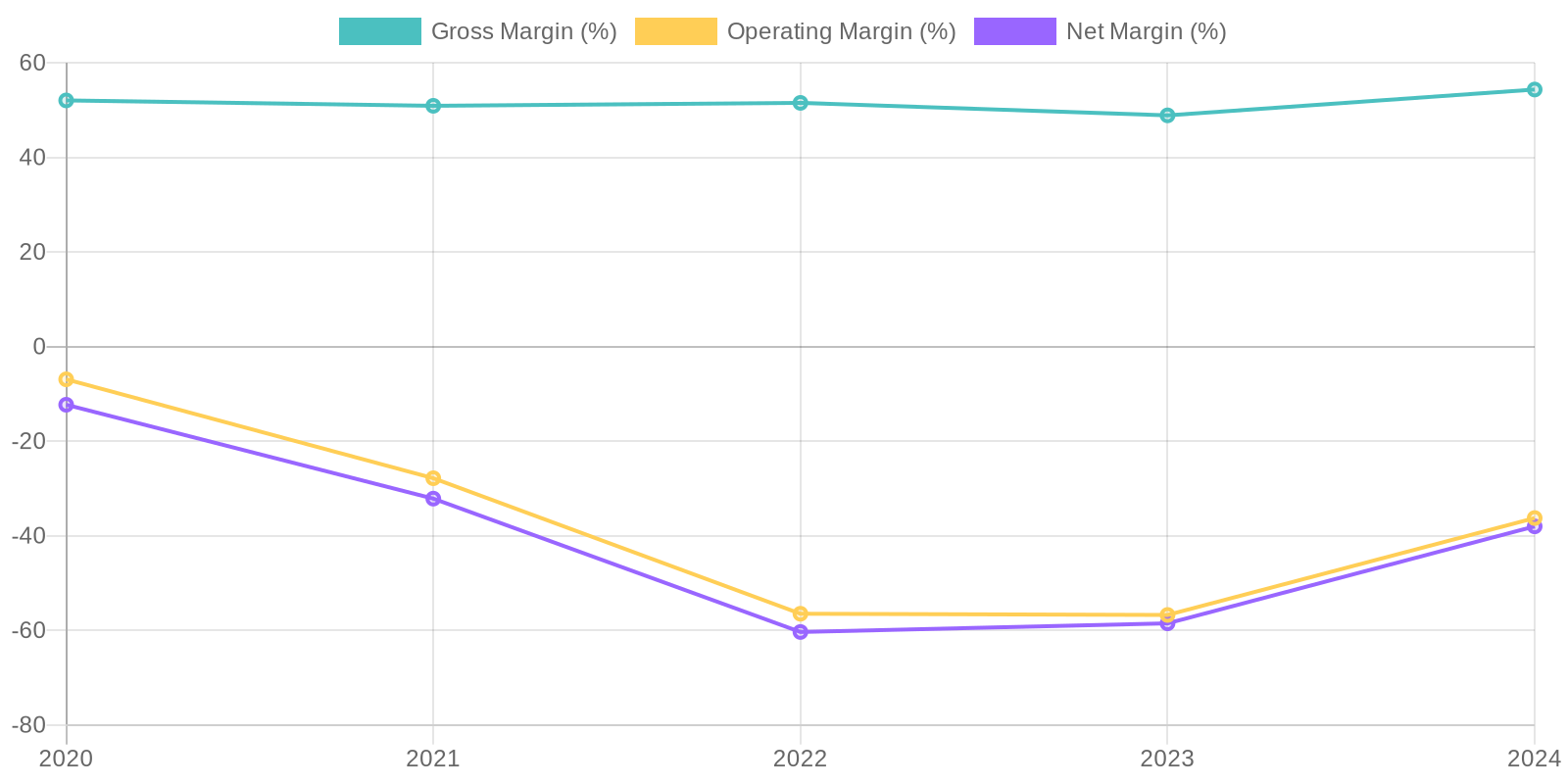

Margin Trend

Given the company's negative net income in recent years, a traditional Return on Invested Capital (ROIC) calculation would yield negative results, highlighting the company's current inefficiency in generating profits from its invested capital. Similarly, the Return on Equity (ROE) is also negative due to the negative net income and fluctuating equity, signaling that the company is not effectively utilizing shareholder investments to generate returns. A more in-depth analysis of asset turnover and profitability ratios would be needed to pinpoint the specific areas of inefficiency and potential improvements.

Revenue Quality

The company has demonstrated consistent revenue growth over the past five years, indicating a positive trend. However, a deeper investigation into the specific contracts and customer relationships would be necessary to fully assess the recurring nature and sustainability of this revenue. Analyzing the concentration of revenue among key clients is crucial to determine the potential impact of losing one or more major customers. Further information on contract terms, renewal rates, and customer churn is required for a more definitive judgment.

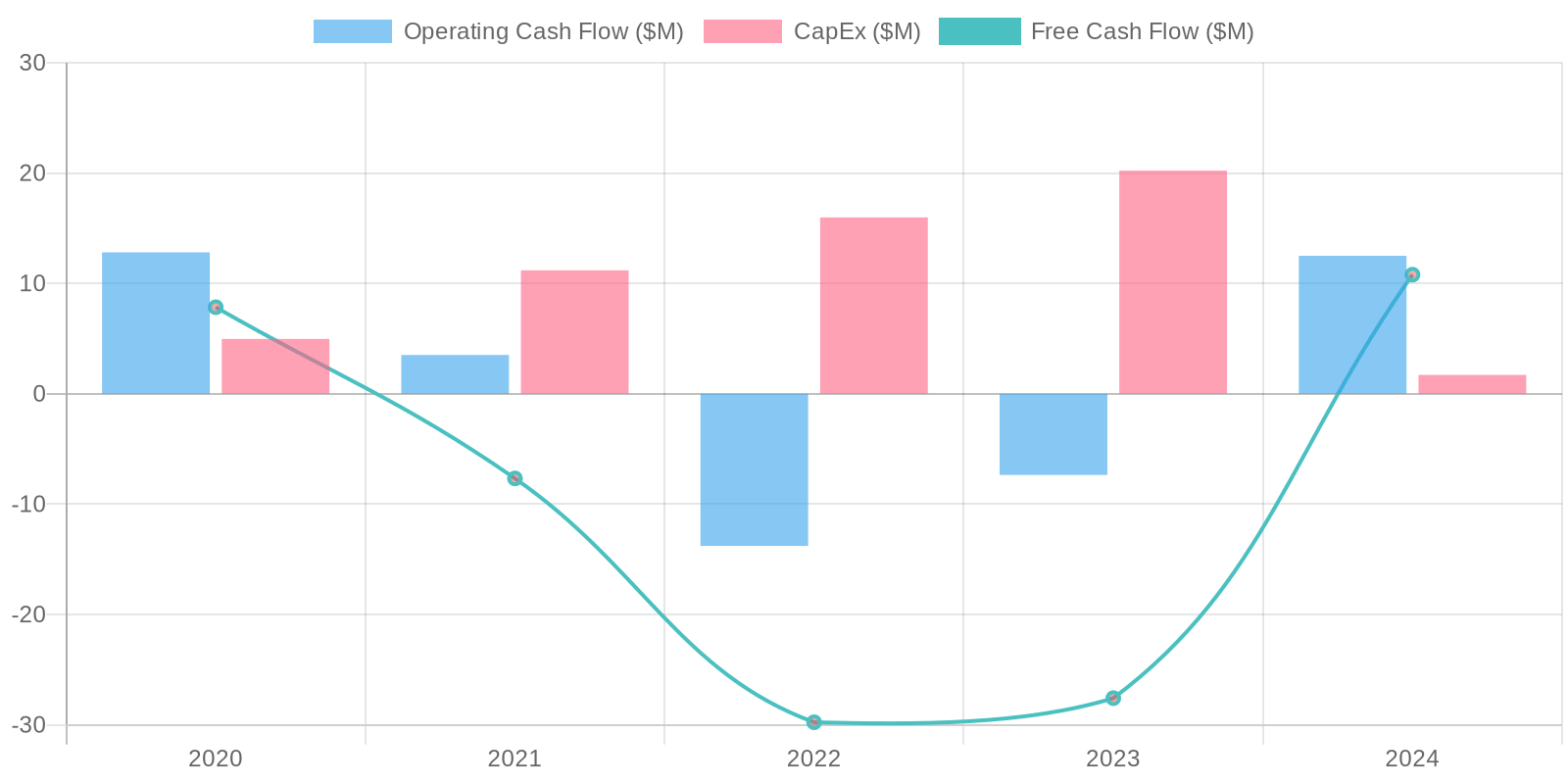

Cash Flow & Capital Efficiency

While the company reported positive Free Cash Flow (FCF) of $10.794 million in 2024, it experienced negative FCF in the preceding years, suggesting volatility in its cash-generating abilities. Capital expenditures (Capex) have been relatively consistent but substantial, indicating ongoing investments in property, plant, and equipment. Further examination into the nature and necessity of these capital expenditures is warranted to determine their long-term impact on the company's financial health. It's important to evaluate the sustainability of the positive FCF in 2024 in light of the historical negative trends.

Capital Efficiency (ROIC/ROE):

Given the company's negative net income in recent years, a traditional Return on Invested Capital (ROIC) calculation would yield negative results, highlighting the company's current inefficiency in generating profits from its invested capital. Similarly, the Return on Equity (ROE) is also negative due to the negative net income and fluctuating equity, signaling that the company is not effectively utilizing shareholder investments to generate returns. A more in-depth analysis of asset turnover and profitability ratios would be needed to pinpoint the specific areas of inefficiency and potential improvements.

Balance Sheet Health:

The company's debt levels are considerable, with a total debt of $46.339 million against a cash balance of $45.776 million. While the net debt is low, indicating some capability to cover debt with available cash, it is important to review the debt maturity schedule and associated interest rates to fully understand the company's repayment obligations. The current ratio, calculated by dividing current assets by current liabilities, is approximately 1.1, suggesting a limited but acceptable level of short-term liquidity, although further analysis of the composition of current assets and liabilities is crucial for a more comprehensive assessment.

5. Management & Governance

CEO Assessment: Backblaze's CEO, Gleb Budman, has been with the company since its inception and has a deep understanding of the cloud storage market. His continued leadership provides stability, but his performance should be consistently monitored against the company's growth and profitability targets.

Capital Allocation: Good

Insider Ownership: Insider ownership appears reasonably aligned with shareholders' interests based on available data, providing incentive for long-term value creation. Specific details can be found in the company's proxy statements and SEC filings.

Governance Flags:

No major governance concerns flagged.

Based on the DCF analysis, the fair value is estimated at $3.82. Considering the current price of $4.89, the stock seems overvalued. Given the assumptions made for revenue growth and FCF margin, there's potential downside if BLZE fails to achieve these targets. The high beta contributes to a significant discount rate, further impacting the valuation.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

N/A

Base

3.82

N/A

Bear

Low

N/A

7. Risks

Backblaze faces medium risk due to consistent net losses, debt, and strong competition in the cloud storage market. While revenue is growing and recent FCF is positive, the company needs to demonstrate sustained profitability to ensure long-term financial health.

Red Flags:

Consistent Net Losses

High Operating Expenses

Volatile Free Cash Flow

Significant Debt Levels

Reliance on Stock Based Compensation

8. Conclusion

N/A

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Given the company's negative net income in recent years, a traditional Return on Invested Capital (ROIC) calculation would yield negative results, highlighting the company's current inefficiency in generating profits from its invested capital. Similarly, the Return on Equity (ROE) is also negative due to the negative net income and fluctuating equity, signaling that the company is not effectively utilizing shareholder investments to generate returns. A more in-depth analysis of asset turnover and profitability ratios would be needed to pinpoint the specific areas of inefficiency and potential improvements.

Given the company's negative net income in recent years, a traditional Return on Invested Capital (ROIC) calculation would yield negative results, highlighting the company's current inefficiency in generating profits from its invested capital. Similarly, the Return on Equity (ROE) is also negative due to the negative net income and fluctuating equity, signaling that the company is not effectively utilizing shareholder investments to generate returns. A more in-depth analysis of asset turnover and profitability ratios would be needed to pinpoint the specific areas of inefficiency and potential improvements. While the company reported positive Free Cash Flow (FCF) of $10.794 million in 2024, it experienced negative FCF in the preceding years, suggesting volatility in its cash-generating abilities. Capital expenditures (Capex) have been relatively consistent but substantial, indicating ongoing investments in property, plant, and equipment. Further examination into the nature and necessity of these capital expenditures is warranted to determine their long-term impact on the company's financial health. It's important to evaluate the sustainability of the positive FCF in 2024 in light of the historical negative trends.

While the company reported positive Free Cash Flow (FCF) of $10.794 million in 2024, it experienced negative FCF in the preceding years, suggesting volatility in its cash-generating abilities. Capital expenditures (Capex) have been relatively consistent but substantial, indicating ongoing investments in property, plant, and equipment. Further examination into the nature and necessity of these capital expenditures is warranted to determine their long-term impact on the company's financial health. It's important to evaluate the sustainability of the positive FCF in 2024 in light of the historical negative trends.