Deep Dive: Webull Corporation Class A Ordinary Shares (BULL)

Recommendation: BUY Price Target: 4.64 (-0.43 Upside) Risk Level: Medium

1. Executive Summary

Webull Corporation Class A Ordinary Shares (BULL) currently trade at $8.18. The company operates a digital brokerage platform, catering primarily to retail investors, offering trading in stocks, ETFs, options, and cryptocurrencies. Webull's market position is defined by its commission-free trading model, user-friendly mobile platform, and focus on attracting a younger, tech-savvy demographic. Competition in the online brokerage space is intense, with established players like Robinhood, Charles Schwab, and Interactive Brokers vying for market share. Webull differentiates itself through its robust charting tools, real-time market data, and paper trading capabilities, appealing to both novice and experienced traders.

Growth catalysts for Webull include further expansion into international markets, the introduction of new financial products and services (such as robo-advisory or lending products), and strategic partnerships to enhance its platform offerings. Increasing user engagement through gamified features and educational resources could also drive growth. Furthermore, rising interest rates may improve net interest income on customer cash balances, positively impacting profitability. Successful marketing campaigns targeted at underserved investor segments could expand its user base.

Key risks facing Webull include intense competition, regulatory scrutiny, and cybersecurity threats. The company's reliance on transaction-based revenue makes it vulnerable to market volatility and trading volume fluctuations. Changes in regulations related to payment for order flow or cryptocurrency trading could significantly impact its business model. Maintaining platform stability and preventing security breaches are critical to preserving user trust and avoiding financial losses. Furthermore, macroeconomic factors, such as economic downturns or inflationary pressures, could negatively affect investor sentiment and trading activity.

The valuation of Webull is complex due to its relatively short operating history and the rapidly evolving nature of the online brokerage industry. A definitive valuation conclusion requires comprehensive financial modeling incorporating future growth assumptions, profitability projections, and risk assessments. However, current market sentiment appears cautious, reflected in the current stock price, suggesting investors are factoring in both the growth potential and the inherent risks associated with the company's business model. A detailed comparative analysis against peers, considering factors such as price-to-sales ratio, user growth, and profitability metrics, would be necessary for a more robust valuation assessment.

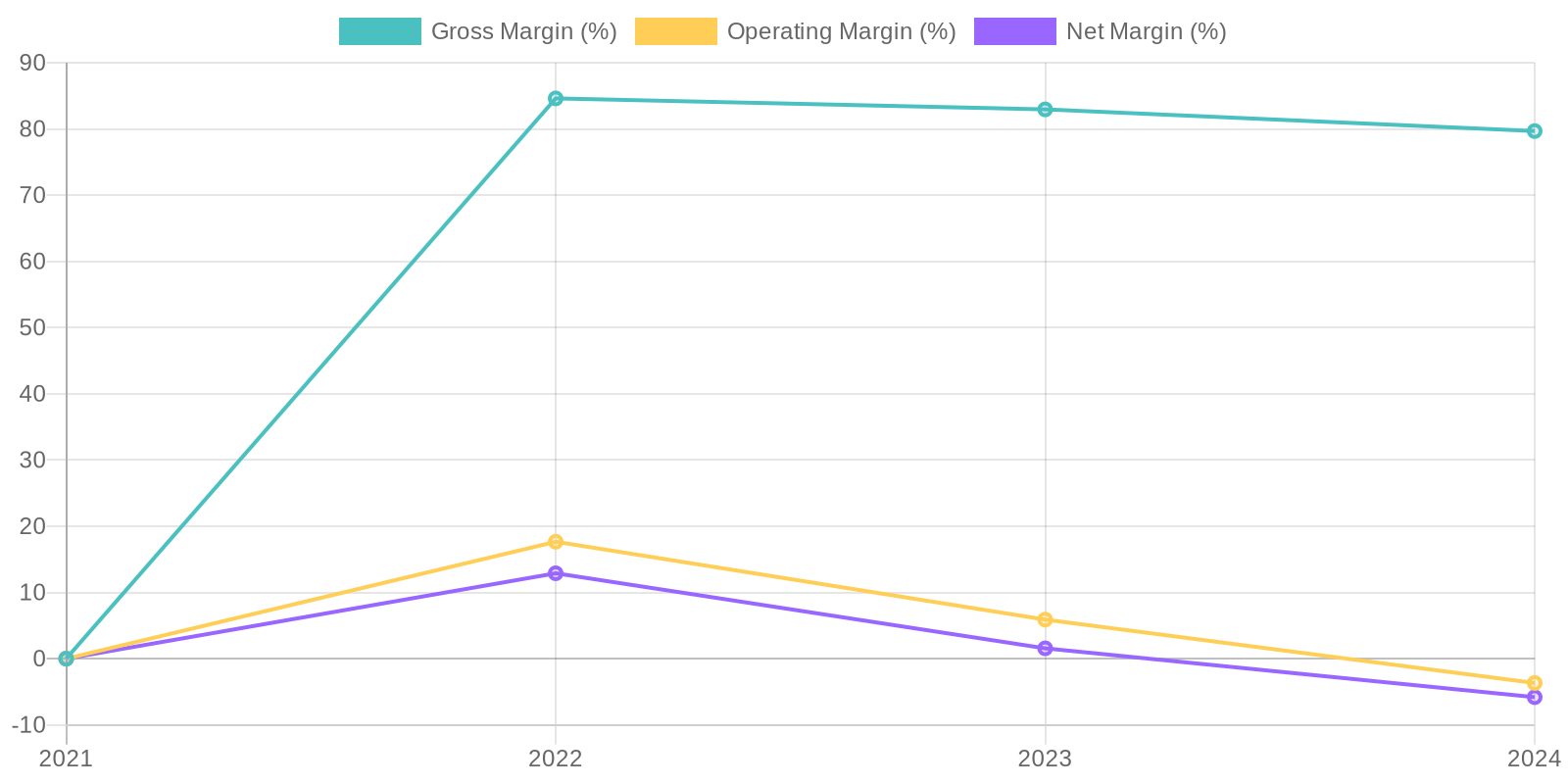

It is difficult to analyze ROIC given the negative operating income in 2024 and fluctuating results in previous years. The company's ROE is also heavily impacted by net losses, which are skewing the result. The company needs to show a consistent profit before any meaningful capital efficiency metric can be calculated.

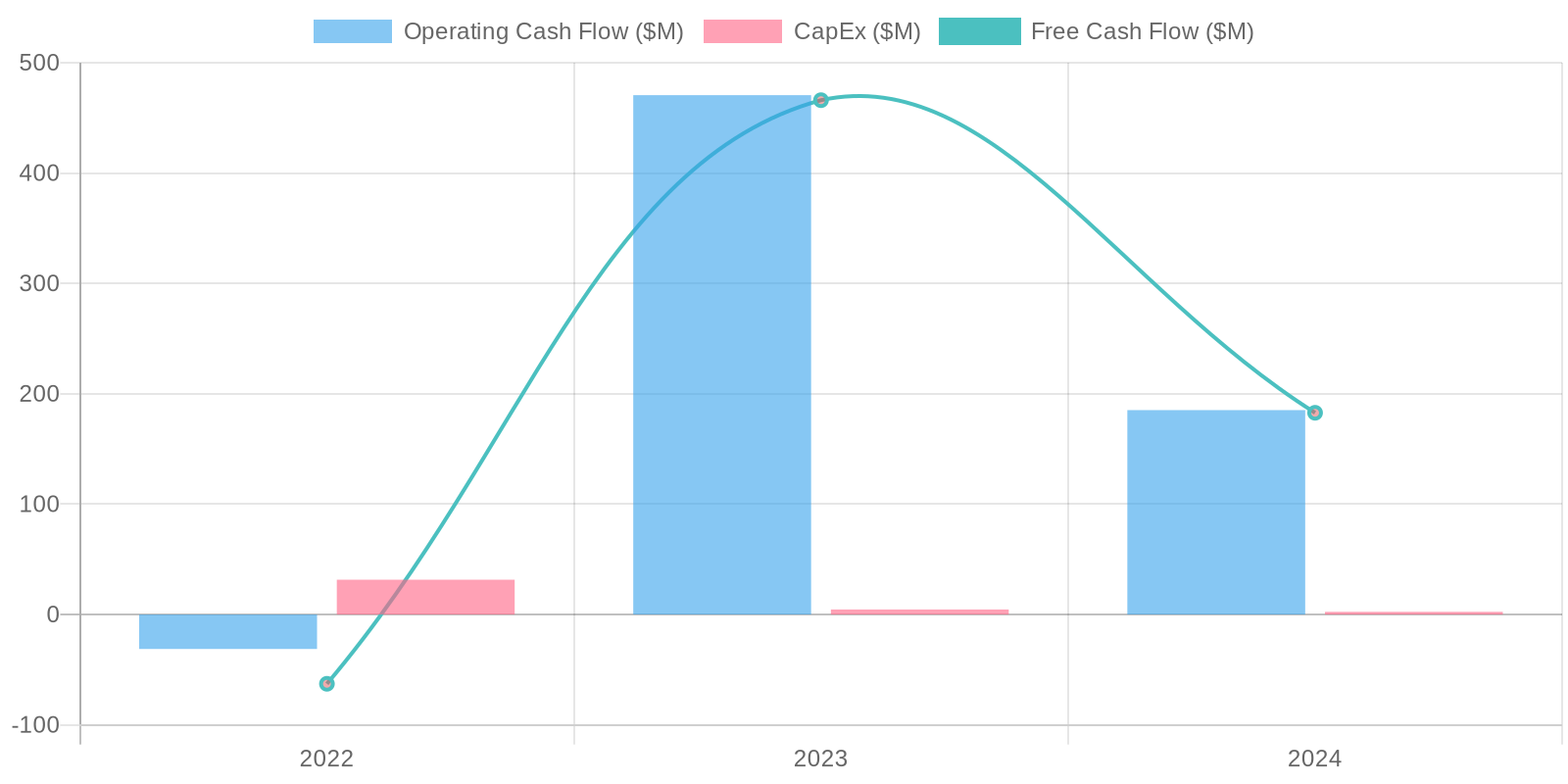

It is difficult to analyze ROIC given the negative operating income in 2024 and fluctuating results in previous years. The company's ROE is also heavily impacted by net losses, which are skewing the result. The company needs to show a consistent profit before any meaningful capital efficiency metric can be calculated. The company exhibits strong free cash flow (FCF) generation in 2023 and 2024, with a decrease in 2024 as compared to 2023. Capital expenditure appears well managed, remaining relatively low compared to revenue, indicating effective use of existing assets. However, in 2022, the company had a negative operating and free cash flow, indicating that the company was struggling to generate profits.

The company exhibits strong free cash flow (FCF) generation in 2023 and 2024, with a decrease in 2024 as compared to 2023. Capital expenditure appears well managed, remaining relatively low compared to revenue, indicating effective use of existing assets. However, in 2022, the company had a negative operating and free cash flow, indicating that the company was struggling to generate profits.