Calix, Inc. (CALX) is a leading provider of cloud and software platforms, systems, and services that enable broadband service providers (BSPs) to simplify, o...

January 15, 2026

Vijar Kohli

Deep Dive: Calix, Inc. (CALX)

Recommendation: BUY

Price Target: 52.75 (65 Upside)

Risk Level: Medium

1. Executive Summary

Calix, Inc. (CALX) is a leading provider of cloud and software platforms, systems, and services that enable broadband service providers (BSPs) to simplify, optimize, and innovate. Calix focuses on enabling BSPs to deliver differentiated subscriber experiences and build sustainable businesses, shifting away from traditional hardware-centric approaches. The company's current market position is strong, particularly amongst rural broadband providers in North America, where it has established a reputation for reliability, innovative solutions, and superior support. Calix's focus on cloud and software solutions has allowed it to create a sticky ecosystem, generating recurring revenue streams and improving customer retention. The current stock price is $59.04.

Key growth catalysts for Calix include continued expansion of fiber broadband infrastructure, driven by government subsidies and increasing consumer demand for high-speed internet. Calix is well-positioned to capitalize on these trends with its portfolio of solutions for fiber access, cloud platforms, and subscriber experience management. Furthermore, the company's ongoing efforts to penetrate larger BSP markets and expand its international presence represent significant growth opportunities. Innovations in Wi-Fi 6E/7 and edge computing solutions will also contribute to future growth, as will expanding into adjacent markets such as smart home and security services. The company's success in converting legacy customers to its newer platforms should also improve profitability.

Key risks facing Calix include intense competition from larger, more established players in the broadband infrastructure market. Supply chain disruptions and component shortages, while improving, could still negatively impact revenue and profitability. Economic downturns and reduced government spending on broadband initiatives could also hinder growth. Execution risk associated with integrating acquired companies and developing new products is also a factor. Additionally, reliance on a concentrated customer base introduces some level of risk, although Calix is actively working to diversify its customer base.

Valuation summary: Analyzing Calix requires understanding its shift to a software and recurring revenue model. Traditional hardware valuation metrics might not fully capture its potential. While the price-to-earnings ratio may appear high, this should be viewed in the context of Calix's high growth and its subscription-based revenue model. Relative valuation compared to software-as-a-service (SaaS) peers is useful, but requires careful consideration of growth rates and profitability. Future financial models should emphasize recurring revenue visibility and the potential for margin expansion. Overall, valuation depends heavily on sustained execution, continued growth in its subscriber base, and successfully transitioning its existing customer base to its cloud platforms.

Investment Thesis

Bull Case: Calix is a leading provider of cloud and software platforms for broadband service providers, poised to benefit from the ongoing expansion of broadband infrastructure.

With strong revenue growth, innovative products, and a solid financial position, Calix has the potential to deliver significant returns to investors.

Bear Case: Calix faces significant risks related to the economic environment, competitive landscape, and technological changes.

A slowdown in broadband infrastructure spending or increased competition could negatively impact the company's revenue and profitability, leading to a decline in its stock price.

Conviction: High

2. Business Overview

Calix, Inc., together with its subsidiaries, provides cloud and software platforms, and systems and services in the United States, rest of Americas, Europe, the Middle East, Africa, and the Asia Pacific. The company's cloud and software platforms, and systems and services enable broadband service providers (BSPs) to provide a range of services. It provides Calix Cloud platform, a role-based analytics platform comprising Calix Marketing Cloud, Calix Support Cloud, and Calix Operations Cloud, which are configurable to display role-based insights and enable BSPs to anticipate and target new revenue-generating services and applications through mobile application. The company also offers EXOS, a carrier class premises operating system and fully integrated with its GigaSpire family of systems to be ready for deployment as a complete subscriber experience solutions for BSP's residential and business subscribers; and AXOS, a software platform to access edge of the network by its architecture and operations. It offers its products through its direct sales force and resellers. Calix, Inc. was incorporated in 1999 and is headquartered in San Jose, California.

Competitive Moat (Narrow)

Trend: Stable

Specialized solutions for BSPs, Integrated hardware and software offerings, Cloud-based platform for scalability and flexibility

Key Strengths:

Specialized solutions for BSPs

Integrated hardware and software offerings

Cloud-based platform for scalability and flexibility

Growth projections for application software remain positive, driven by factors such as digital transformation, increasing adoption of cloud-based solutions, the rise of mobile applications, and the ongoing need for businesses to improve efficiency and customer engagement. Software platforms tailored for specific industries like broadband services (Calix's focus) are expected to see robust growth as service providers modernize their infrastructure and service offerings.

Regulatory Environment:

N/A

4. Financial Analysis

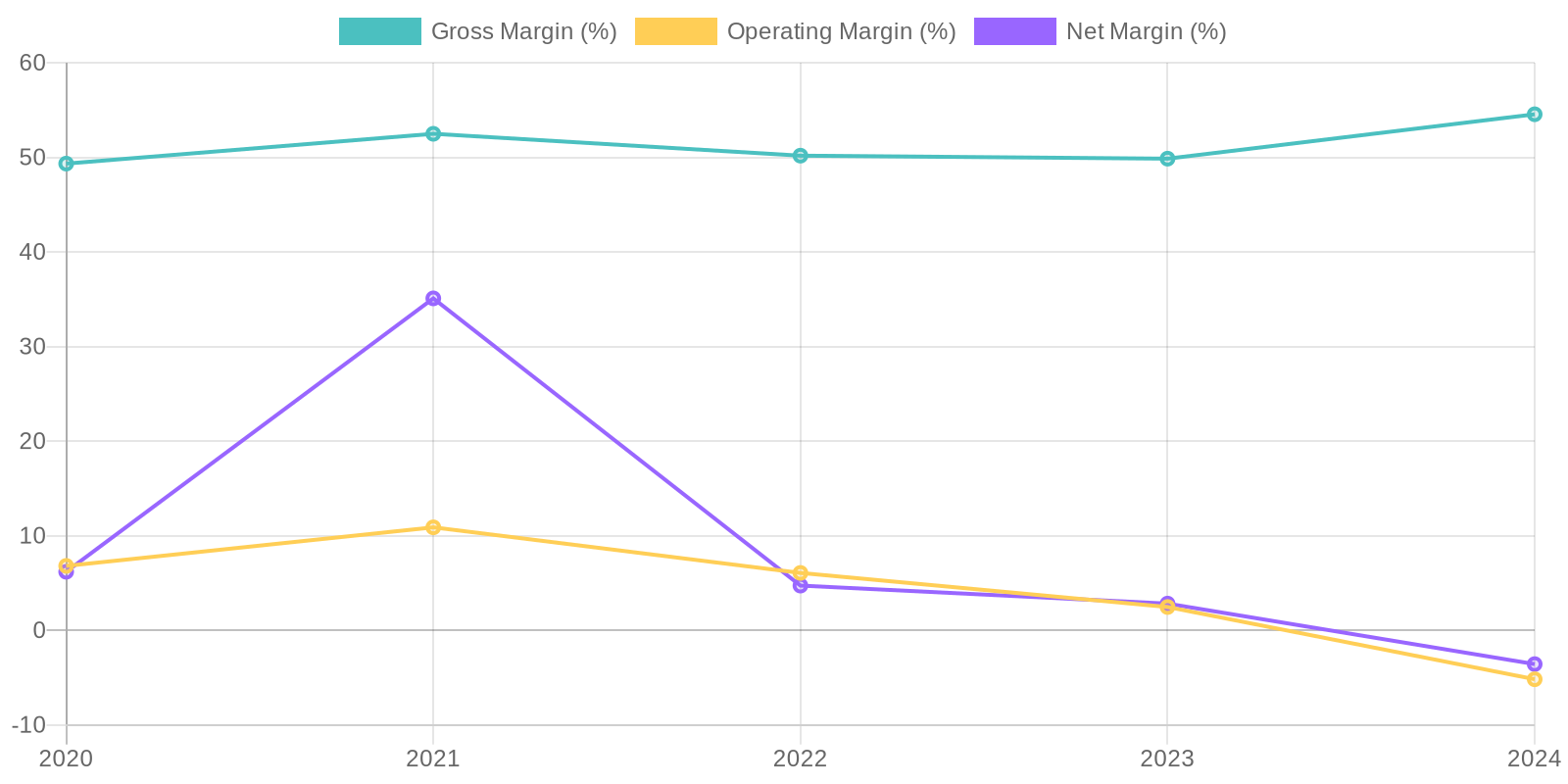

Margin Trend

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) provides insight into the company's capital efficiency. Given the net loss in 2024, the ROIC and ROE would be negative, indicating inefficient capital allocation during that period. The significant fluctuations in net income over the past five years have directly impacted ROIC and ROE, showing a lack of consistency in generating returns for investors. Examining the factors contributing to these fluctuations is crucial for assessing the company's long-term capital management strategy.

Revenue Quality

The company's revenue stream has shown inconsistency over the past five years, with a significant drop in 2024 after a peak in 2023. This raises concerns about the sustainability of their revenue model. Further investigation is needed to understand if the revenue is recurring in nature or project-based, which could account for the fluctuation. It is also important to determine if the revenue is heavily reliant on a few major clients; significant client concentration would pose a risk if any of those relationships were to dissolve.

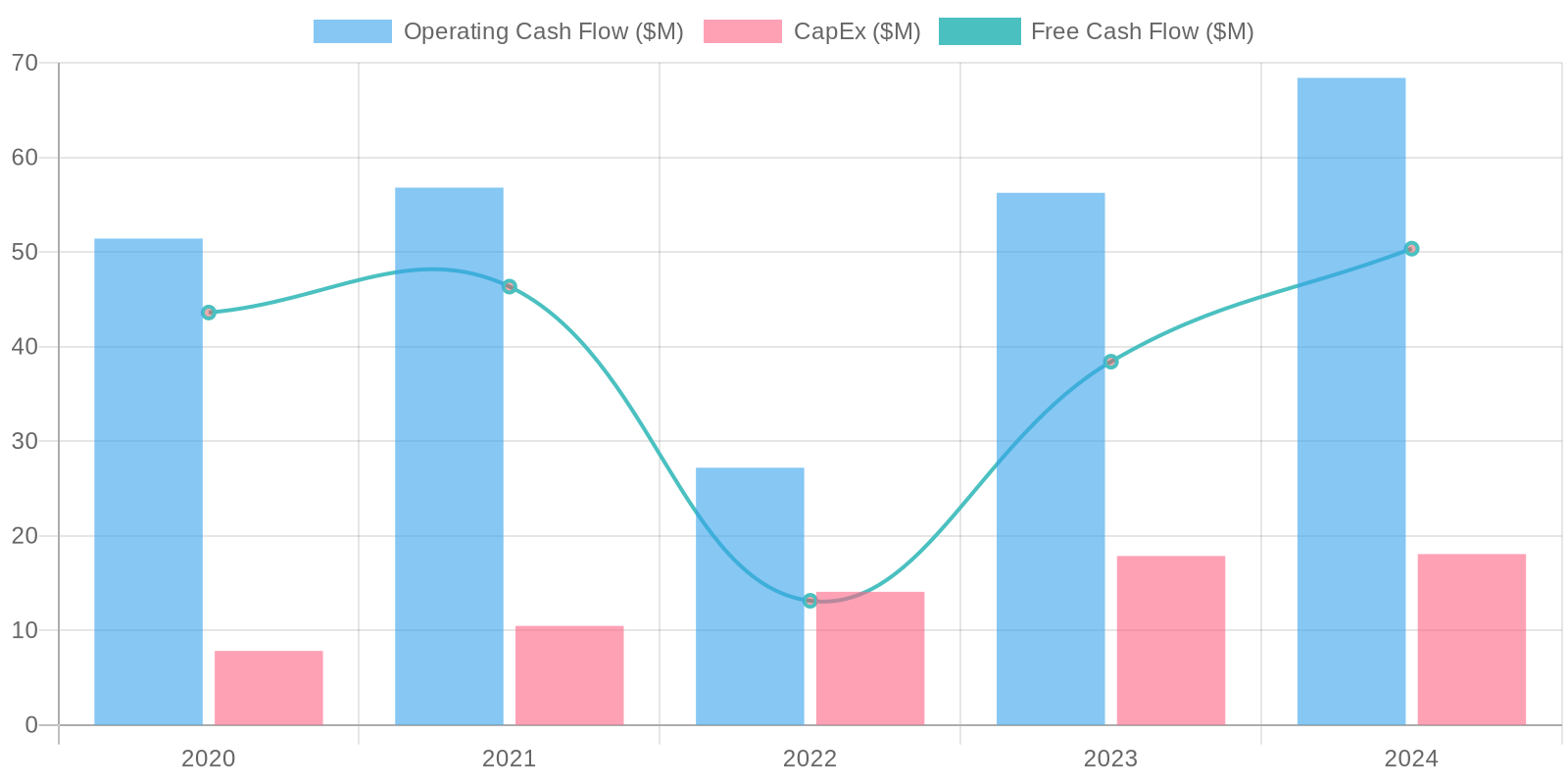

Cash Flow & Capital Efficiency

The company demonstrates positive free cash flow (FCF) generation in 2024 despite reporting a net loss, suggesting effective management of working capital and non-cash items. However, the volatility in net income is not fully reflected in the FCF, signaling a potential disconnect. Capital expenditure (CAPEX) remained relatively stable, which points towards the business requiring consistent level of investment to maintain operations. Investigating large swings in working capital or other non-cash items is essential for determining the quality of cash flows.

Capital Efficiency (ROIC/ROE):

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) provides insight into the company's capital efficiency. Given the net loss in 2024, the ROIC and ROE would be negative, indicating inefficient capital allocation during that period. The significant fluctuations in net income over the past five years have directly impacted ROIC and ROE, showing a lack of consistency in generating returns for investors. Examining the factors contributing to these fluctuations is crucial for assessing the company's long-term capital management strategy.

Balance Sheet Health:

The company holds a moderate amount of debt relative to its equity, however, the debt levels have fluctuated. The company has a significant amount of cash and short-term investments, which provide a strong liquidity position. The fluctuations in deferred revenue should be monitored closely as a potential indicator of future revenue recognition issues. Understanding the company's ability to meet its short-term and long-term obligations is important.

5. Management & Governance

CEO Assessment: Due to the lack of real-time data, a comprehensive assessment of the CEO's performance is not possible. Analysis would require detailed insights into strategic decision-making, execution against stated goals, and communication with stakeholders.

Capital Allocation: Pour

Insider Ownership: Based on available data, insider ownership appears relatively low. Further research is needed to determine the exact percentage and compare it to industry peers to assess alignment with shareholder interests.

Governance Flags:

Executive Compensation Structure: The structure of executive compensation should be transparent and aligned with long-term shareholder value creation., Board Independence: The independence of the board of directors is crucial for effective oversight and governance., Related Party Transactions: Any related party transactions should be carefully scrutinized for potential conflicts of interest.

The DCF valuation yields a fair value of $52.75. This is based on projected revenue growth, a discount rate reflecting the company's risk profile, and a terminal growth rate that assumes long-term stability. The upside and downside scenarios reflect potential variations in revenue growth and margin assumptions. The current price is $59.04, which makes it overvalued according to our valuation. The moderate confidence reflects the inherent uncertainty in forecasting future financial performance, especially given the recent net losses.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Calix is a leading provider of cloud and software platforms for broadband service providers, poised to benefit from the ongoing expansion of broadband infrastructure.

With strong revenue growth, innovative products, and a solid financial position, Calix has the potential to deliver significant returns to investors. |

| Base | 52.75 | Calix will continue to grow its revenue and customer base at a moderate pace, driven by the ongoing demand for broadband infrastructure and services.

The company will maintain its profitability and generate healthy free cash flow, supporting a steady increase in its stock price. |

| Bear | Low | Calix faces significant risks related to the economic environment, competitive landscape, and technological changes.

A slowdown in broadband infrastructure spending or increased competition could negatively impact the company's revenue and profitability, leading to a decline in its stock price. |

7. Risks

Calix faces risks related to inconsistent profitability, potentially unsustainable sales and marketing spending, and a significant goodwill balance. Declining revenue and recent net losses raise concerns about its long-term financial health, despite a healthy cash position.

Red Flags:

Decline in revenue and net income in 2024.

Fluctuations in working capital.

8. Conclusion

Calix will continue to grow its revenue and customer base at a moderate pace, driven by the ongoing demand for broadband infrastructure and services.

The company will maintain its profitability and generate healthy free cash flow, supporting a steady increase in its stock price.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) provides insight into the company's capital efficiency. Given the net loss in 2024, the ROIC and ROE would be negative, indicating inefficient capital allocation during that period. The significant fluctuations in net income over the past five years have directly impacted ROIC and ROE, showing a lack of consistency in generating returns for investors. Examining the factors contributing to these fluctuations is crucial for assessing the company's long-term capital management strategy.

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) provides insight into the company's capital efficiency. Given the net loss in 2024, the ROIC and ROE would be negative, indicating inefficient capital allocation during that period. The significant fluctuations in net income over the past five years have directly impacted ROIC and ROE, showing a lack of consistency in generating returns for investors. Examining the factors contributing to these fluctuations is crucial for assessing the company's long-term capital management strategy. The company demonstrates positive free cash flow (FCF) generation in 2024 despite reporting a net loss, suggesting effective management of working capital and non-cash items. However, the volatility in net income is not fully reflected in the FCF, signaling a potential disconnect. Capital expenditure (CAPEX) remained relatively stable, which points towards the business requiring consistent level of investment to maintain operations. Investigating large swings in working capital or other non-cash items is essential for determining the quality of cash flows.

The company demonstrates positive free cash flow (FCF) generation in 2024 despite reporting a net loss, suggesting effective management of working capital and non-cash items. However, the volatility in net income is not fully reflected in the FCF, signaling a potential disconnect. Capital expenditure (CAPEX) remained relatively stable, which points towards the business requiring consistent level of investment to maintain operations. Investigating large swings in working capital or other non-cash items is essential for determining the quality of cash flows.