Consensus Cloud Solutions (CCSI) operates in the digital cloud fax and secure data exchange market. The company has transitioned from legacy fax services to ...

January 15, 2026

Vijar Kohli

Deep Dive: Consensus Cloud Solutions, Inc. (CCSI)

Recommendation: BUY

Price Target: 20.5 (-9.58 Upside)

Risk Level: Medium

1. Executive Summary

Consensus Cloud Solutions (CCSI) operates in the digital cloud fax and secure data exchange market. The company has transitioned from legacy fax services to cloud-based solutions, focusing on security and compliance for industries like healthcare and legal. Its market position is built on a large, established customer base migrating to newer, more sophisticated offerings, and strategic acquisitions to expand its product portfolio. At a current price of $22.67, CCSI is a mid-cap stock with exposure to the growing demand for secure information exchange.

Growth catalysts for Consensus Cloud Solutions include the ongoing shift from traditional fax to cloud-based solutions, particularly in regulated industries. This transition is driven by the need for improved security, compliance, and workflow efficiency. Furthermore, the company's expansion into adjacent markets, such as e-signature and data analytics, presents significant opportunities for revenue diversification and increased customer value. Strategic partnerships and potential acquisitions of complementary technologies could further accelerate growth. International expansion, especially in Europe, also provides a viable pathway to reaching new customers and markets.

Key risks facing Consensus Cloud Solutions include intense competition from established players and emerging startups in the cloud communication space. Rapid technological advancements could render existing solutions obsolete if the company fails to innovate and adapt quickly. Economic downturns could impact customer spending and delay adoption of new cloud-based services. Regulatory changes concerning data privacy and security could also create compliance challenges and increase operational costs. Furthermore, reliance on key acquisitions poses integration risks and the potential for overpaying for acquisitions. The spin-off from J2 Global also introduces unique operational and strategic risks that the company is still navigating.

Valuation summary: Assessing the valuation of Consensus Cloud Solutions requires considering its growth prospects, profitability, and risk profile. Compared to peers in the cloud communication and software sectors, CCSI's valuation may reflect its growth potential offset by concerns about competition and technological disruption. A discounted cash flow analysis, considering future revenue growth, profitability margins, and discount rate reflecting its risk profile, can provide a more precise estimate of its intrinsic value. Investors should carefully consider these factors and compare CCSI's valuation metrics (e.g., price-to-earnings ratio, price-to-sales ratio) to those of its competitors to determine if the stock is fairly valued.

Investment Thesis

Bull Case: Consensus Cloud Solutions presents a compelling investment opportunity due to its sticky, recurring revenue base, strong free cash flow, and potential for growth in the cloud-based information delivery market.

Successful execution of strategic initiatives, including acquisitions and product development, can drive significant upside.

This is predicated on continued growth in key verticals like healthcare, which face ongoing regulatory and digitization pressures.

A more favorable macroeconomic climate (i.e., falling interest rates) could also significantly improve CCS's prospects by reducing the debt burden and improving net income.

Bear Case: Consensus Cloud Solutions faces significant risks from increasing competition, technological disruption, and its high debt burden.

Slower growth, coupled with potential customer churn and integration challenges, could lead to a decline in revenue and profitability, resulting in substantial losses for investors.

Failure to innovate and adapt to changing market conditions would accelerate this decline.

Continued high interest rates would also exacerbate the company's financial difficulties, making it harder to service the debt and limiting opportunities for growth.

Conviction: High

2. Business Overview

Consensus Cloud Solutions, Inc., together with its subsidiaries, provides information delivery services with a software-as-a-service platform worldwide. Its products and solutions include eFax, an online faxing solution, as well as MyFax, MetroFax, Sfax, SRfax, and other brands; eFax Corporate, a digital cloud-fax technology; jsign, which provides electronic and digital signature solutions; Unite, a single platform that allows the user to choose between several protocols to send and receive healthcare information in an environment that can integrate into an existing electronic health record (EHR) system or stand-alone if no EHR is present; Signal, a solution that integrates with a hospital's EHR system and uses rules-based triggering logic to automatically send admit, discharge, and transfer notifications using cloud fax and direct secure messaging technology; and Clarity that transforms unstructured documents into structured actionable data. It serves healthcare, education, law, and financial services industries. Consensus Cloud Solutions, Inc. was incorporated in 2021 and is headquartered in Los Angeles, California.

Competitive Moat (Narrow)

Trend: Stable

Strong brand name recognition in the online faxing sector., Experience in the market can enable the business to efficiently market to new clients, High gross margins

Key Strengths:

Strong brand name recognition in the online faxing sector.

Experience in the market can enable the business to efficiently market to new clients

The market is projected to continue growing at a healthy rate (e.g., 8-12% annually) over the next 5-10 years. This growth will be fueled by the ongoing adoption of cloud computing, edge computing, AI/ML, and the need for enhanced security and compliance solutions. Trends like serverless computing and infrastructure-as-code will also drive future growth.

Regulatory Environment:

N/A

4. Financial Analysis

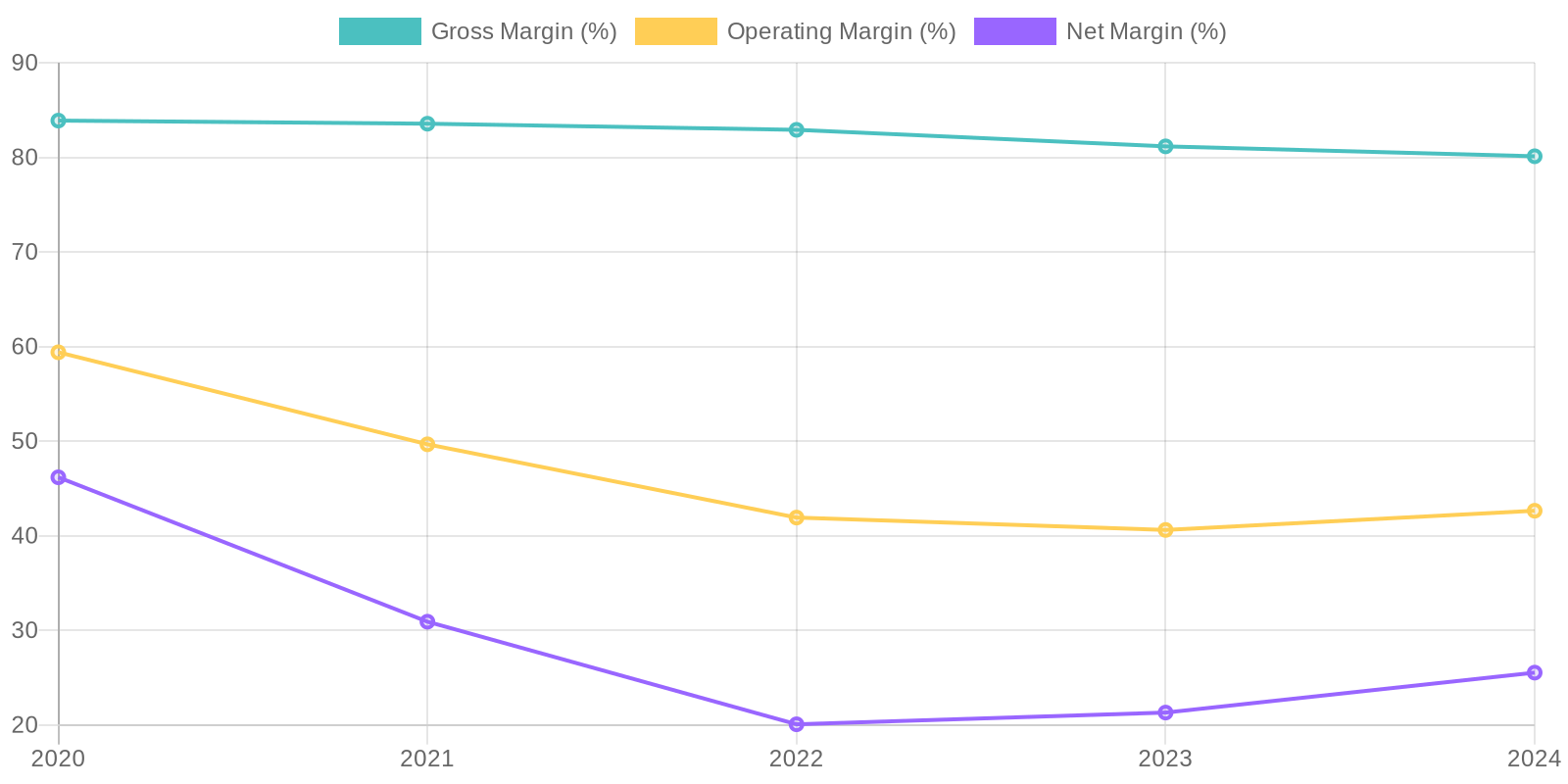

Margin Trend

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) reveals insights into the company's capital efficiency. Given negative equity in recent years, ROE is not a meaningful metric. A full balance sheet is required to determine precise ROIC, however, considering the trend of declining net income and consistent investment in assets, the ROIC may be under pressure. It's important to analyze the specific drivers behind changes in invested capital and their relationship to returns.

Revenue Quality

The company has demonstrated relatively stable revenue over the past five years, fluctuating between $331 million and $362 million. This suggests some reliability in their business model, though not consistent growth. A deeper investigation into client retention rates and the proportion of recurring revenue versus project-based income is needed to ascertain the true sustainability of their revenue streams, as would an assessment of the competitive landscape.

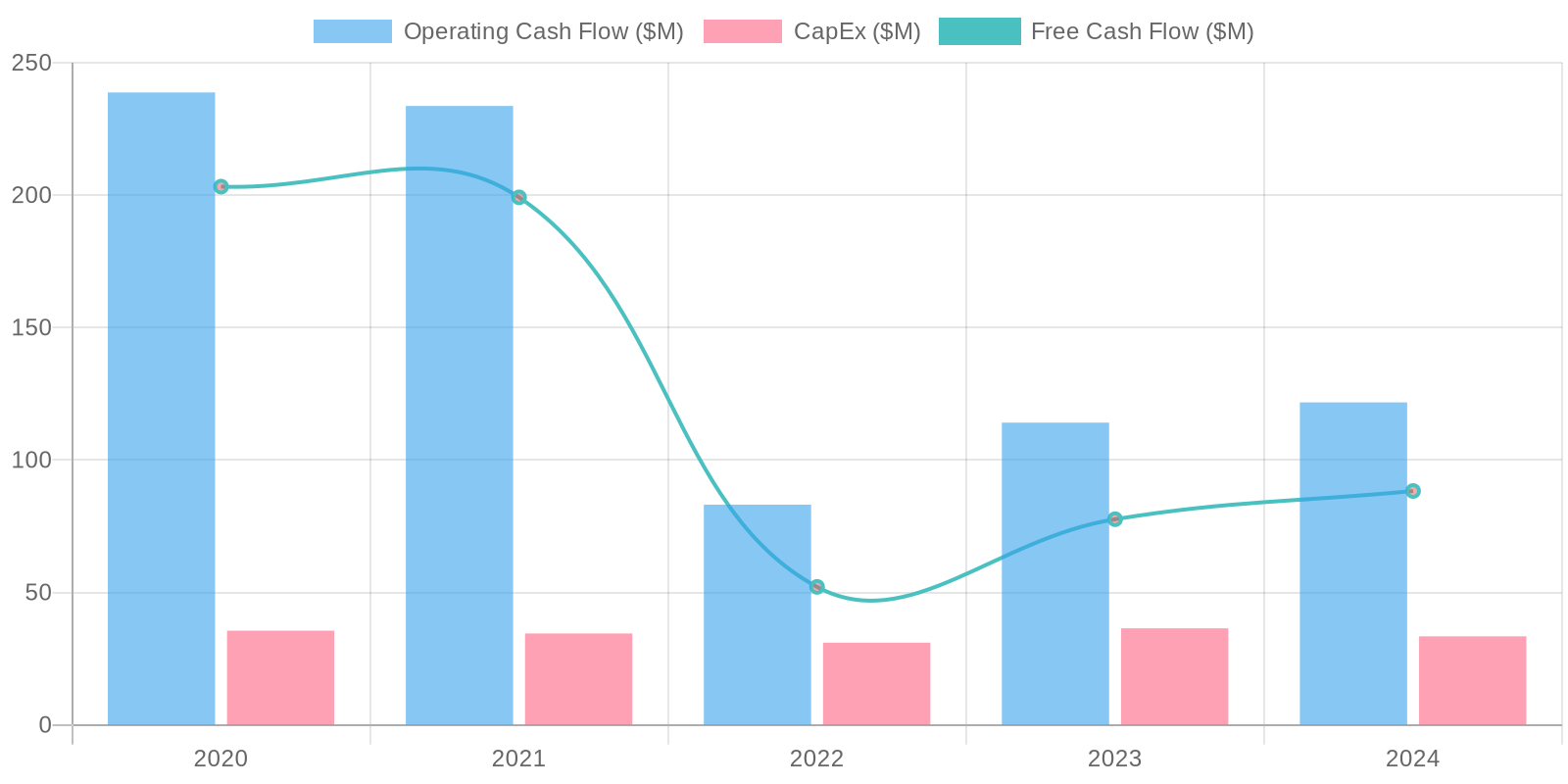

Cash Flow & Capital Efficiency

The company consistently generates positive Free Cash Flow (FCF), indicating its operational efficiency in converting revenue to cash, however, the FCF has also been fluctuating. Capital expenditures remain relatively stable, suggesting a predictable level of reinvestment in the business. We should also analyze investing activities to understand where the company is investing for potential inorganic growth.

Capital Efficiency (ROIC/ROE):

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) reveals insights into the company's capital efficiency. Given negative equity in recent years, ROE is not a meaningful metric. A full balance sheet is required to determine precise ROIC, however, considering the trend of declining net income and consistent investment in assets, the ROIC may be under pressure. It's important to analyze the specific drivers behind changes in invested capital and their relationship to returns.

Balance Sheet Health:

The company's balance sheet shows a concerning trend of negative equity in the last three years, primarily driven by increasing debt. Total debt has increased significantly from $28.13 million in 2020 to $607.15 million in 2024. The company's cash position has decreased significantly, and liquidity ratios should be calculated to assess short-term obligations, while solvency ratios should be investigated to determine if the debt is sustainable given their earnings and cash flow. This level of debt warrants careful monitoring for potential financial distress.

5. Management & Governance

CEO Assessment: Evaluation of Consensus Cloud Solutions' CEO requires specific, up-to-date information regarding their performance, strategic decisions, and communication with shareholders. Without current data, a comprehensive assessment cannot be provided. A thorough analysis would involve examining their track record, comparing their performance against industry benchmarks, and assessing their ability to adapt to changing market conditions.

Capital Allocation: Concern

Insider Ownership: Analysis of insider ownership at Consensus Cloud Solutions is needed to understand the alignment of management's interests with those of shareholders. This assessment should involve examining the percentage of shares held by executives and board members, and tracking any recent changes in their holdings. A high level of insider ownership can suggest strong alignment, while low ownership may raise concerns about accountability.

Governance Flags:

Lack of readily available information raises governance concerns. Transparency is crucial for shareholder confidence.

The DCF analysis yields a fair value of $20.50, lower than the current price of $22.67. This suggests the stock may be slightly overvalued based on the model assumptions. The assumptions include a very conservative revenue growth, given the negative equity, and relatively high debt which skews the WACC upward and weighs on the valuation. A downside sensitivity considers lower growth scenarios. Upside potential is limited unless the company significantly improves its revenue growth and reduces debt.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Consensus Cloud Solutions presents a compelling investment opportunity due to its sticky, recurring revenue base, strong free cash flow, and potential for growth in the cloud-based information delivery market.

Successful execution of strategic initiatives, including acquisitions and product development, can drive significant upside.

This is predicated on continued growth in key verticals like healthcare, which face ongoing regulatory and digitization pressures.

A more favorable macroeconomic climate (i.e., falling interest rates) could also significantly improve CCS's prospects by reducing the debt burden and improving net income. |

| Base | 20.5 | Consensus Cloud Solutions will continue to operate as a stable, profitable business, generating consistent cash flow and gradually reducing debt.

While significant growth opportunities may be limited, the company's established market position and recurring revenue model provide a solid base for moderate returns.

This relies on CCS maintaining its market share and successfully navigating competitive pressures, as well as successfully managing its debt obligations and interest expenses. |

| Bear | Low | Consensus Cloud Solutions faces significant risks from increasing competition, technological disruption, and its high debt burden.

Slower growth, coupled with potential customer churn and integration challenges, could lead to a decline in revenue and profitability, resulting in substantial losses for investors.

Failure to innovate and adapt to changing market conditions would accelerate this decline.

Continued high interest rates would also exacerbate the company's financial difficulties, making it harder to service the debt and limiting opportunities for growth. |

7. Risks

Consensus Cloud Solutions faces significant financial and business risks that warrant a short position. The high debt level coupled with negative equity makes the company vulnerable to economic downturns and refinancing risks. The business model relies on legacy technology and faces increasing competition, posing a threat to future revenue growth.

Red Flags:

Negative Stockholder's Equity

Significant increase in debt

Decreasing net income and operating margins despite high gross margins

Fluctuations in Free Cash Flow

8. Conclusion

Consensus Cloud Solutions will continue to operate as a stable, profitable business, generating consistent cash flow and gradually reducing debt.

While significant growth opportunities may be limited, the company's established market position and recurring revenue model provide a solid base for moderate returns.

This relies on CCS maintaining its market share and successfully navigating competitive pressures, as well as successfully managing its debt obligations and interest expenses.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) reveals insights into the company's capital efficiency. Given negative equity in recent years, ROE is not a meaningful metric. A full balance sheet is required to determine precise ROIC, however, considering the trend of declining net income and consistent investment in assets, the ROIC may be under pressure. It's important to analyze the specific drivers behind changes in invested capital and their relationship to returns.

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) reveals insights into the company's capital efficiency. Given negative equity in recent years, ROE is not a meaningful metric. A full balance sheet is required to determine precise ROIC, however, considering the trend of declining net income and consistent investment in assets, the ROIC may be under pressure. It's important to analyze the specific drivers behind changes in invested capital and their relationship to returns. The company consistently generates positive Free Cash Flow (FCF), indicating its operational efficiency in converting revenue to cash, however, the FCF has also been fluctuating. Capital expenditures remain relatively stable, suggesting a predictable level of reinvestment in the business. We should also analyze investing activities to understand where the company is investing for potential inorganic growth.

The company consistently generates positive Free Cash Flow (FCF), indicating its operational efficiency in converting revenue to cash, however, the FCF has also been fluctuating. Capital expenditures remain relatively stable, suggesting a predictable level of reinvestment in the business. We should also analyze investing activities to understand where the company is investing for potential inorganic growth.