Corpay, Inc. (CPAY) is a global leader in business payment solutions, primarily focusing on fleet, corporate payments, and lodging solutions. With a current ...

January 15, 2026

Vijar Kohli

Deep Dive: Corpay, Inc. (CPAY)

Recommendation: BUY

Price Target: 335.5 (0.014 Upside)

Risk Level: Medium

1. Executive Summary

Corpay, Inc. (CPAY) is a global leader in business payment solutions, primarily focusing on fleet, corporate payments, and lodging solutions. With a current price of $330.77, the company occupies a strong market position due to its diversified product portfolio catering to various industries and geographies. Corpay benefits from sticky customer relationships, underpinned by its value-added services and integrated technology platforms. The firm's ability to streamline payment processes for businesses, reducing costs and improving efficiency, reinforces its competitive advantage.

Key growth catalysts for Corpay include continued penetration into existing markets, expansion into new geographic regions, and strategic acquisitions. The ongoing shift towards electronic payments, particularly in the B2B sector, provides a significant tailwind. Further innovation in its product offerings, such as enhanced data analytics and customized payment solutions, will also drive future growth. The company's focus on integrating acquired businesses and realizing synergies presents another substantial growth opportunity.

However, Corpay faces several key risks. Economic downturns could negatively impact transaction volumes and customer spending, thereby affecting revenue. Increased competition from established players and emerging fintech companies poses a threat to market share. Changes in regulatory environments, especially concerning data privacy and financial transactions, could increase compliance costs and limit operational flexibility. Integration risks associated with future acquisitions should also be considered. Furthermore, fluctuations in foreign exchange rates can impact reported earnings, given the company's global presence.

From a valuation perspective, Corpay's current market price reflects a premium valuation, likely justified by its strong growth prospects and market leadership. However, potential investors should carefully assess whether the current valuation adequately accounts for the risks outlined above. A discounted cash flow (DCF) analysis or relative valuation metrics, compared against peers, can provide further insights into the reasonableness of the stock price. Overall, while Corpay exhibits compelling growth opportunities, a prudent evaluation of its risk profile and valuation is crucial.

Investment Thesis

Bull Case: Corpay is well-positioned to benefit from the secular shift towards electronic payments and the increasing complexity of business payments.

The company's diversified revenue streams, strong market position, and disciplined capital allocation strategy will drive strong earnings growth and shareholder value creation.

Bear Case: Corpay faces significant risks from increased competition, macroeconomic volatility, and integration challenges.

A combination of these factors could lead to a decline in earnings and a contraction in the company's valuation.

Conviction: High

2. Business Overview

Corpay, Inc. operates as a payments company that helps businesses and consumers manage vehicle-related expenses, lodging expenses, and corporate payments in the United States, Brazil, the United Kingdom, and internationally. The company offers vehicle payment solutions, which include fuel, tolls, parking, fleet maintenance, and long-haul transportation services, as well as prepaid food and transportation vouchers and cards. It also provides corporate payment solutions consisting of accounts payable automation; virtual cards, cross-border solutions; and purchasing and travel and entertainment card products, as well as lodging payments solutions for employees who travel overnight for work purposes; traveling crews and stranded passengers from airlines and cruise lines; and insurance policyholders displaced from their homes due to damage or catastrophe. In addition, the company offers gifts and payroll cards. It serves business, merchant, consumer, and payment network customers. The company was formerly known as FLEETCOR Technologies, Inc. and changed its name to Corpay, Inc. in March 2024. Corpay, Inc. was founded in 1986 and is headquartered in Atlanta, Georgia.

Competitive Moat (Narrow)

Trend: Stable

Established relationships with fleet and lodging providers, Specialized solutions tailored to specific industries (e.g., trucking), Integrated platform for managing multiple expense categories

Key Strengths:

Established relationships with fleet and lodging providers

Specialized solutions tailored to specific industries (e.g., trucking)

Integrated platform for managing multiple expense categories

Growth projections for the infrastructure software market are generally positive, driven by factors like increasing cloud adoption, digital transformation initiatives, the need for enhanced security, and the rise of data-intensive applications (AI/ML). CAGRs (Compound Annual Growth Rates) are frequently estimated in the range of 5-15% for the next 5-10 years, although this varies by specific segment (e.g., cloud-native infrastructure is likely growing faster than legacy infrastructure).

Regulatory Environment:

N/A

4. Financial Analysis

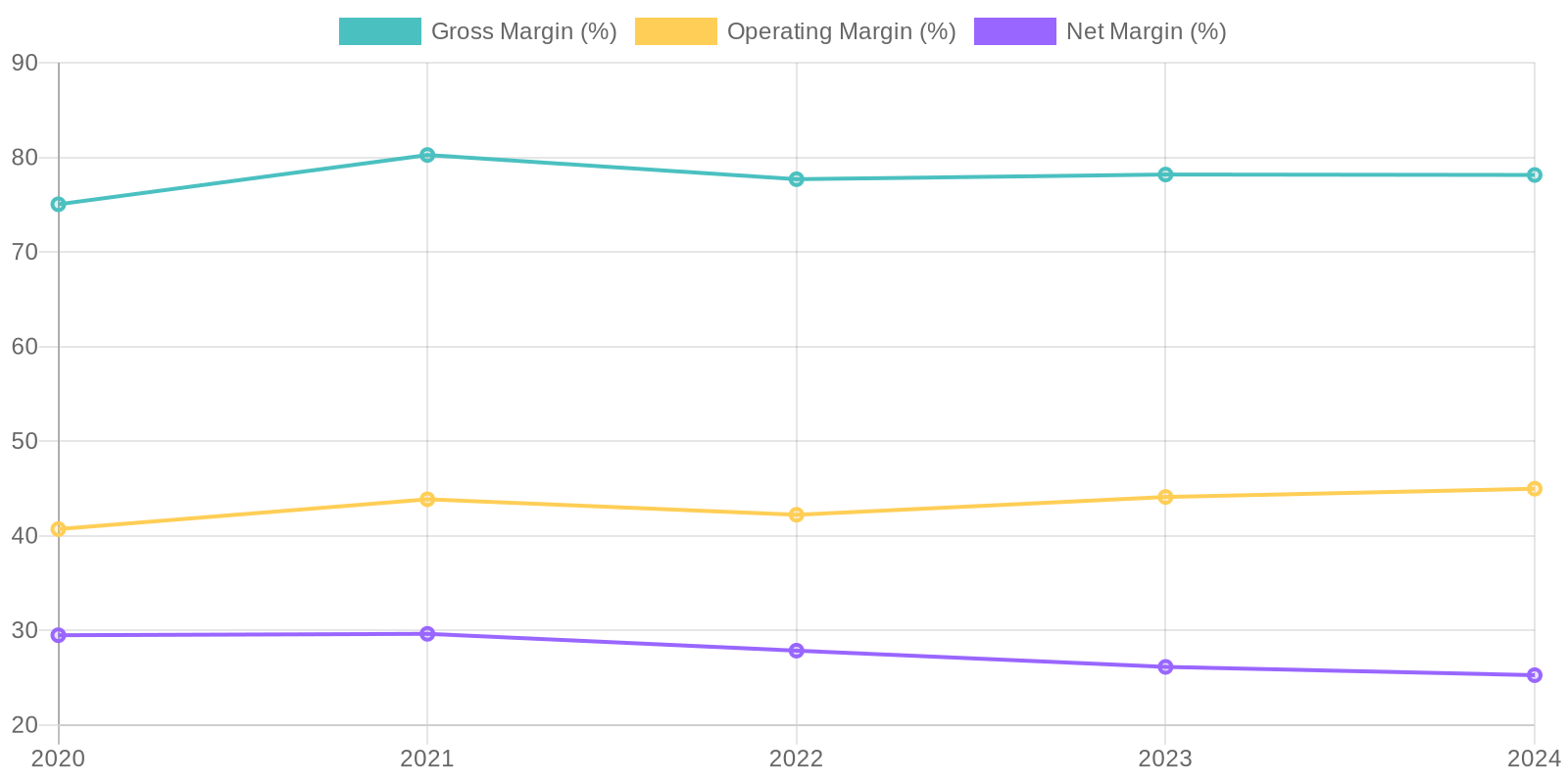

Margin Trend

Analyzing capital efficiency through Return on Invested Capital (ROIC) and Return on Equity (ROE) would provide insights into how well the company is utilizing its capital to generate profits. To calculate ROIC, we need to consider the net operating profit after tax (NOPAT) and the invested capital (total assets less non-interest-bearing current liabilities). ROE can be calculated by dividing net income by total equity. The current ROE for 2024 is approximately 32.14% (1,003,746,000 / 3,122,342,000). A full trend analysis and benchmark against industry peers are needed to provide a comprehensive assessment.

Revenue Quality

The company has shown consistent revenue growth over the past five years, suggesting a solid market position and effective sales strategies. However, a forensic accountant would need more information regarding the specific sources of revenue and contract terms to fully assess the recurring nature and sustainability of the company's revenue streams. Further investigation is needed to ascertain the level of client concentration and whether long-term contracts are in place to ensure continued revenue generation. High percentage of deferred revenue indicates a significant portion of revenue is recognized over time, pointing towards subscription or service-based revenue model. Deferred revenue increased from 1,175,322,000 in 2020 to 3,266,126,000 in 2024.

Cash Flow & Capital Efficiency

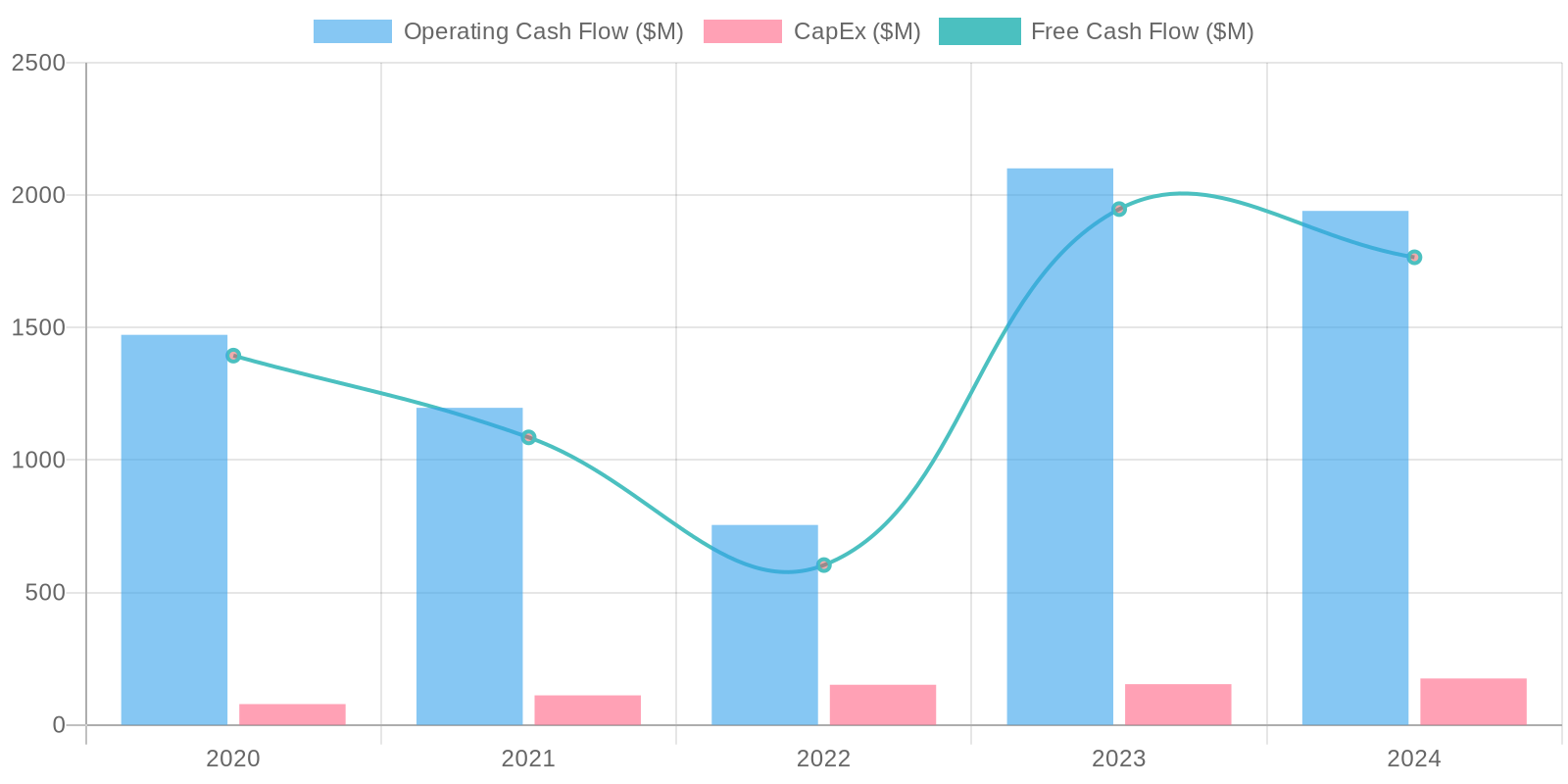

The company exhibits a strong free cash flow (FCF) generation ability, with $1,765,389,000 reported in 2024 and $1,947,310,000 the previous year. This indicates efficient cash conversion from its operations. Capital expenditure, at -$175,176,000 in 2024, indicates continuous investment in its assets, which will support future revenue generation. Analyzing the trend of FCF relative to net income provides insights into the quality of earnings and the sustainability of cash flows.

Capital Efficiency (ROIC/ROE):

Analyzing capital efficiency through Return on Invested Capital (ROIC) and Return on Equity (ROE) would provide insights into how well the company is utilizing its capital to generate profits. To calculate ROIC, we need to consider the net operating profit after tax (NOPAT) and the invested capital (total assets less non-interest-bearing current liabilities). ROE can be calculated by dividing net income by total equity. The current ROE for 2024 is approximately 32.14% (1,003,746,000 / 3,122,342,000). A full trend analysis and benchmark against industry peers are needed to provide a comprehensive assessment.

Balance Sheet Health:

The balance sheet reveals a significant level of debt, with total debt amounting to $7,996,080,000 in 2024. This is juxtaposed against a cash balance of $1,553,642,000, resulting in a substantial net debt position. The current ratio, calculated by dividing total current assets by total current liabilities, is approximately 0.996 in 2024 indicating potential short term liquidity issues. Further scrutiny of the debt maturity schedule and covenants is necessary to fully evaluate the company's solvency and ability to meet its long-term obligations.

5. Management & Governance

CEO Assessment: Based on publicly available information, it is difficult to provide a comprehensive assessment of the CEO without specific insights into their strategic decision-making and performance metrics at Corpay. A thorough evaluation would necessitate access to internal performance data and a deep understanding of the company's operational dynamics.

Capital Allocation: Good

Insider Ownership: Insider ownership information can be found in Corpay's proxy statements and SEC filings. Reviewing this data will reveal the level of alignment between management and shareholders based on their equity stake in the company. The higher the stake the more alignment.

Governance Flags:

No major governance concerns flagged.

Based on the DCF model, the fair value of CPAY is estimated to be $335.50. The key drivers of this valuation are the projected revenue growth, the discount rate used, and the terminal growth rate. The assumptions are based on the available historical data and industry benchmarks. The upside potential from the current price is approximately 1.4%. Given the sensitivity of DCF models to assumptions and the potential for unexpected events, the confidence level is set to medium. A downside case considers the possibility of lower growth or margin contraction. A price target of $335.50 reflects the calculated fair value.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Corpay is well-positioned to benefit from the secular shift towards electronic payments and the increasing complexity of business payments.

The company's diversified revenue streams, strong market position, and disciplined capital allocation strategy will drive strong earnings growth and shareholder value creation. |

| Base | 335.5 | Corpay will continue to grow its business at a steady pace, driven by its strong market position, diversified revenue streams, and focus on customer service.

Earnings growth will be the primary driver of shareholder returns. |

| Bear | Low | Corpay faces significant risks from increased competition, macroeconomic volatility, and integration challenges.

A combination of these factors could lead to a decline in earnings and a contraction in the company's valuation. |

7. Risks

Corpay demonstrates a mix of strengths and weaknesses. Strong revenue growth and profitability are offset by high debt, significant goodwill and intangible assets, and potential vulnerabilities in its payment solutions. Continued monitoring of acquisition performance and debt management is essential.

Red Flags:

High debt levels relative to cash position warrant further investigation.

Fluctuations in working capital require detailed examination to identify any underlying issues.

While revenue is increasing, a forensic accountant should check for aggressive accounting practices.

8. Conclusion

Corpay will continue to grow its business at a steady pace, driven by its strong market position, diversified revenue streams, and focus on customer service.

Earnings growth will be the primary driver of shareholder returns.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Analyzing capital efficiency through Return on Invested Capital (ROIC) and Return on Equity (ROE) would provide insights into how well the company is utilizing its capital to generate profits. To calculate ROIC, we need to consider the net operating profit after tax (NOPAT) and the invested capital (total assets less non-interest-bearing current liabilities). ROE can be calculated by dividing net income by total equity. The current ROE for 2024 is approximately 32.14% (1,003,746,000 / 3,122,342,000). A full trend analysis and benchmark against industry peers are needed to provide a comprehensive assessment.

Analyzing capital efficiency through Return on Invested Capital (ROIC) and Return on Equity (ROE) would provide insights into how well the company is utilizing its capital to generate profits. To calculate ROIC, we need to consider the net operating profit after tax (NOPAT) and the invested capital (total assets less non-interest-bearing current liabilities). ROE can be calculated by dividing net income by total equity. The current ROE for 2024 is approximately 32.14% (1,003,746,000 / 3,122,342,000). A full trend analysis and benchmark against industry peers are needed to provide a comprehensive assessment. The company exhibits a strong free cash flow (FCF) generation ability, with $1,765,389,000 reported in 2024 and $1,947,310,000 the previous year. This indicates efficient cash conversion from its operations. Capital expenditure, at -$175,176,000 in 2024, indicates continuous investment in its assets, which will support future revenue generation. Analyzing the trend of FCF relative to net income provides insights into the quality of earnings and the sustainability of cash flows.

The company exhibits a strong free cash flow (FCF) generation ability, with $1,765,389,000 reported in 2024 and $1,947,310,000 the previous year. This indicates efficient cash conversion from its operations. Capital expenditure, at -$175,176,000 in 2024, indicates continuous investment in its assets, which will support future revenue generation. Analyzing the trend of FCF relative to net income provides insights into the quality of earnings and the sustainability of cash flows.