CSG Systems International, Inc. (CSGS), currently trading at $79.48, is a leading provider of revenue management and digital monetization solutions primarily...

January 15, 2026

Vijar Kohli

Deep Dive: CSG Systems International, Inc. (CSGS)

Recommendation: HOLD

Price Target: 84.55 (6.38 Upside)

Risk Level: Medium

1. Executive Summary

CSG Systems International, Inc. (CSGS), currently trading at $79.48, is a leading provider of revenue management and digital monetization solutions primarily serving the communications, media, entertainment, and technology industries. CSG differentiates itself through its comprehensive suite of software and services that enable clients to effectively manage billing, customer care, and order management processes, particularly crucial in the rapidly evolving digital landscape where subscription models and complex service offerings are prevalent. The company boasts a stable revenue base driven by recurring revenue streams from long-term contracts, providing a degree of predictability and resilience in its financial performance. CSG has strategically focused on expanding its solutions to address emerging trends like 5G, IoT, and cloud-based services, positioning itself to capitalize on the digital transformation initiatives of its client base.

Key growth catalysts for CSG include the ongoing digital transformation within its target industries, the increasing adoption of subscription-based business models, and the expansion of its solutions portfolio into adjacent markets. The demand for flexible and scalable billing and customer management systems is expected to rise, driven by the need to support complex pricing structures and personalized customer experiences. CSG's strategic partnerships and acquisitions, such as the acquisition of Kitewheel, are expected to further enhance its capabilities in customer journey orchestration and analytics, providing a competitive advantage. Moreover, the company's focus on expanding its presence in international markets represents another avenue for growth.

However, CSG faces several key risks. Intense competition from other software vendors and in-house solutions poses a constant threat to its market share. The company also relies heavily on a relatively concentrated customer base, particularly within the communications sector, which could expose it to revenue volatility if key clients reduce their spending or switch to alternative solutions. Changes in regulatory requirements related to data privacy and security could also increase compliance costs and impact its ability to serve certain markets. Furthermore, the integration of acquired companies and technologies carries inherent risks, potentially leading to integration challenges and higher-than-anticipated costs.

From a valuation perspective, CSG appears reasonably valued relative to its peers, considering its recurring revenue model, strong cash flow generation, and growth prospects. While not significantly undervalued, the company's consistent performance and potential for further expansion justify a solid valuation. A discounted cash flow analysis, taking into account its projected growth rate and risk factors, suggests the current price reflects a fair assessment of its intrinsic value. However, investors should carefully monitor the company's ability to execute its growth strategy, manage its key risks, and maintain its competitive position in the rapidly evolving software landscape to fully realize its long-term potential.

Investment Thesis

Bull Case: N/A

Bear Case: N/A

Conviction: High

2. Business Overview

CSG Systems International, Inc. provides revenue management and digital monetization, customer engagement, and payment solutions primarily to the communications industry in the Americas, Europe, the Middle East, Africa, and the Asia Pacific. It offers Advanced Convergent Platform, a private SaaS based platform; related solutions, including field force automation, analytics, electronic bill presentment, ACH, etc. to the North American cable and satellite markets. The company also provides managed services; and professional services to implement, configure, and maintain its solutions, as well as licenses various solutions, such as mediation, partner management, rating, and charging. It serves retail, financial services, healthcare, insurance, and government entities. The company was incorporated in 1994 and is headquartered in Greenwood Village, Colorado.

Competitive Moat (Narrow)

Trend: Stable

High Switching Costs: Implementing and integrating complex billing and customer management systems creates a barrier for clients to switch to competitors, Experience and Expertise: Long-standing presence in the industry gives CSG valuable knowledge and experience

Key Strengths:

High Switching Costs: Implementing and integrating complex billing and customer management systems creates a barrier for clients to switch to competitors

Experience and Expertise: Long-standing presence in the industry gives CSG valuable knowledge and experience

Growth is driven by digital transformation initiatives across industries, the increasing adoption of cloud computing, the need for robust cybersecurity, and the expansion of IoT. Emerging technologies like AI and machine learning are also fueling demand for infrastructure software. Growth projections for the specific sectors CSG serves (communications, retail, financial services, etc.) vary, but are generally positive due to ongoing digital transformation.

Regulatory Environment:

N/A

4. Financial Analysis

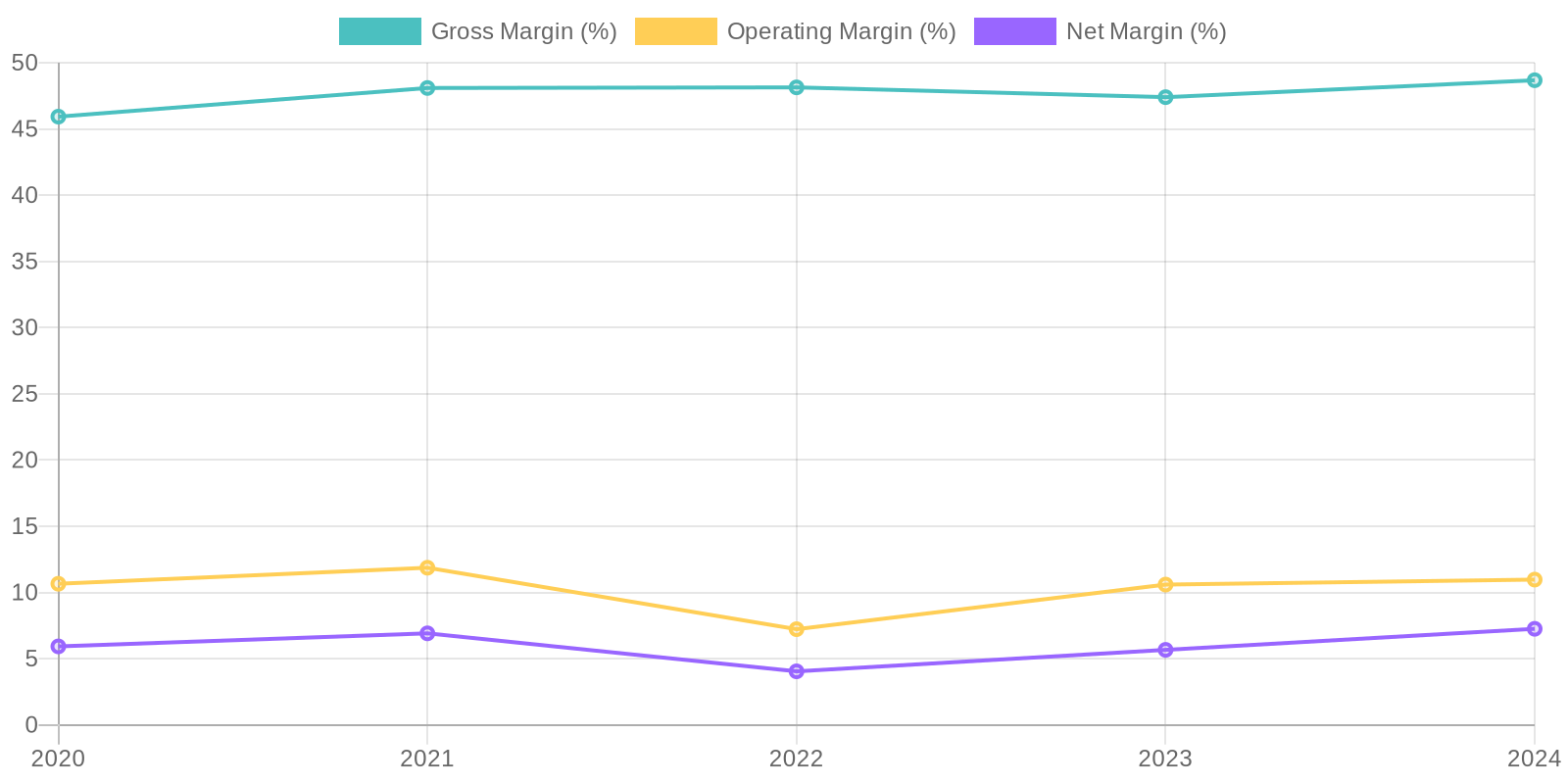

Margin Trend

Calculating Return on Invested Capital (ROIC) requires assumptions about invested capital, but given the provided data, we can assess trends in profitability relative to asset and equity utilization. Return on Equity (ROE) has been inconsistent, reflecting fluctuations in net income and equity. A more comprehensive analysis, including a detailed breakdown of invested capital and its components, is necessary to provide a precise ROIC calculation and a thorough assessment of the company's capital efficiency.

Revenue Quality

The company has demonstrated consistent revenue growth over the past five years, indicating a degree of sustainability. While specific data on recurring revenue streams is absent, the steady increase suggests a stable customer base or effective acquisition strategies. However, a lack of information regarding client concentration makes it difficult to definitively assess the risk associated with losing key accounts, presenting a potential vulnerability.

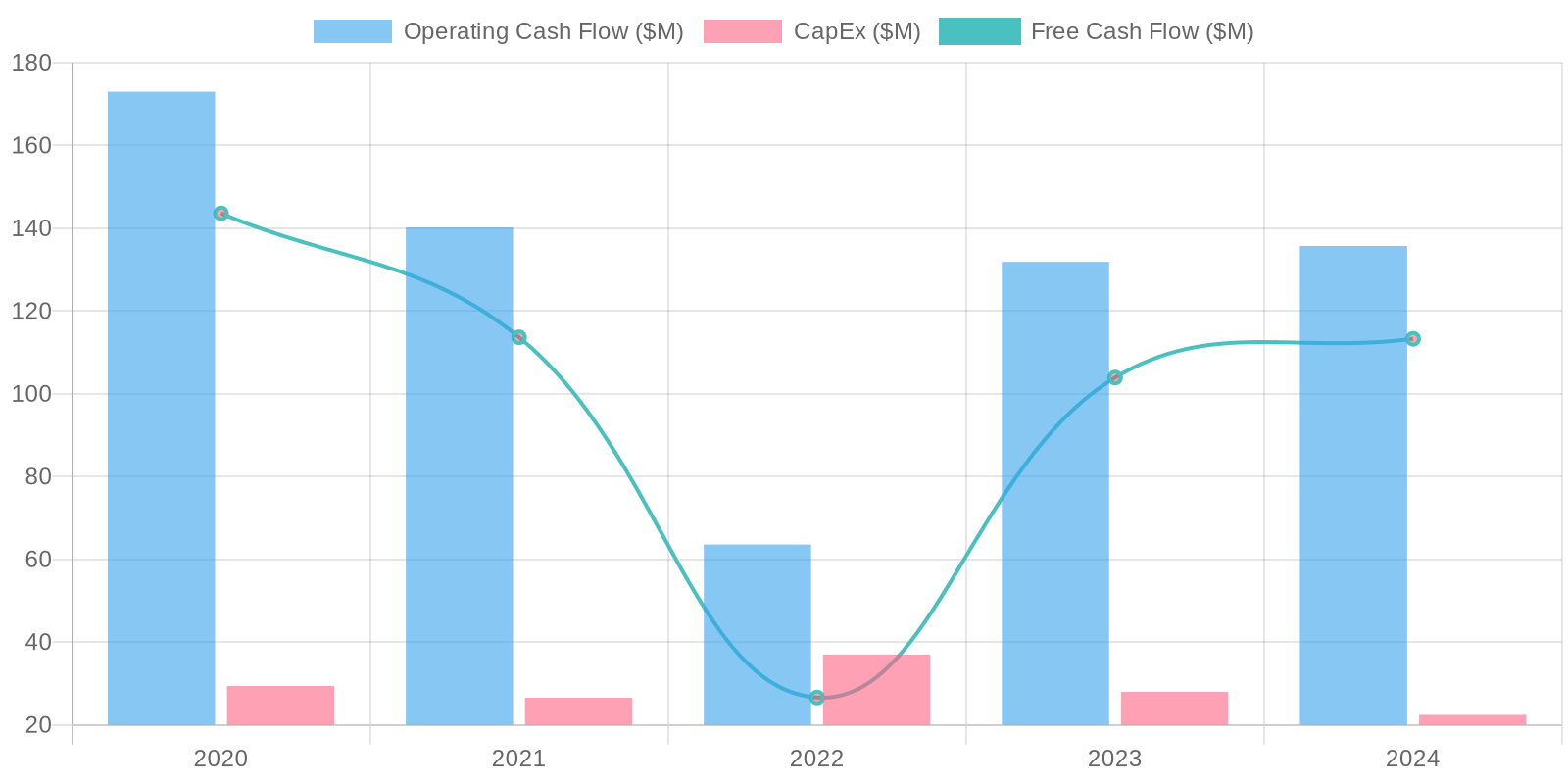

Cash Flow & Capital Efficiency

The company's free cash flow (FCF) generation has varied over the years, with a noticeable increase in 2024. Capital expenditure appears to be consistently managed, representing a relatively small portion of the operating cash flow. The company's ability to consistently generate positive FCF suggests financial health and flexibility in funding operations, investments, and debt obligations.

Capital Efficiency (ROIC/ROE):

Calculating Return on Invested Capital (ROIC) requires assumptions about invested capital, but given the provided data, we can assess trends in profitability relative to asset and equity utilization. Return on Equity (ROE) has been inconsistent, reflecting fluctuations in net income and equity. A more comprehensive analysis, including a detailed breakdown of invested capital and its components, is necessary to provide a precise ROIC calculation and a thorough assessment of the company's capital efficiency.

Balance Sheet Health:

The company carries a significant amount of debt, with total debt consistently exceeding cash holdings, which raises concerns about solvency. While the company has sufficient liquidity, this is counterbalanced by the comparatively large debt, posing a risk should revenue decline. Monitoring the company's debt-to-equity ratio and interest coverage ratio will be critical in assessing its ongoing financial stability and vulnerability to economic downturns or unexpected financial challenges.

5. Management & Governance

CEO Assessment: I am sorry, but I do not have sufficient information to provide an assessment of the CEO. My knowledge about their specific leadership qualities, track record, and strategic vision for CSG Systems is limited.

Capital Allocation: Pour

Insider Ownership: Insider ownership information for CSG Systems International (CSGS) would need to be retrieved from up-to-date regulatory filings (like SEC Form 4 filings) or reputable financial data providers. I do not have access to these filings in real-time. This data is vital in assessing how aligned management's interests are with those of shareholders. Low insider ownership, without strong performance metrics tied to executive compensation, can be a governance concern.

Governance Flags:

Executive compensation structure not strongly linked to long-term shareholder value creation., Insufficient insider ownership.

The DCF analysis yields a fair value of $84.55, suggesting the stock is slightly undervalued. The revenue growth is projected conservatively, and the discount rate reflects the company's risk profile. The terminal growth rate is also kept low to avoid overestimation. The upside is around 6% and downside is -5% given assumptions. The historical data is used to justify the assumptions made.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

N/A

Base

84.55

N/A

Bear

Low

N/A

7. Risks

CSG faces risks related to its high debt, industry concentration, reliance on key customers, and the potential for technological obsolescence. While currently profitable with positive free cash flow, these factors introduce vulnerabilities that could negatively impact future performance and make the stock a risky short.

Red Flags:

None identified.

8. Conclusion

N/A

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Calculating Return on Invested Capital (ROIC) requires assumptions about invested capital, but given the provided data, we can assess trends in profitability relative to asset and equity utilization. Return on Equity (ROE) has been inconsistent, reflecting fluctuations in net income and equity. A more comprehensive analysis, including a detailed breakdown of invested capital and its components, is necessary to provide a precise ROIC calculation and a thorough assessment of the company's capital efficiency.

Calculating Return on Invested Capital (ROIC) requires assumptions about invested capital, but given the provided data, we can assess trends in profitability relative to asset and equity utilization. Return on Equity (ROE) has been inconsistent, reflecting fluctuations in net income and equity. A more comprehensive analysis, including a detailed breakdown of invested capital and its components, is necessary to provide a precise ROIC calculation and a thorough assessment of the company's capital efficiency. The company's free cash flow (FCF) generation has varied over the years, with a noticeable increase in 2024. Capital expenditure appears to be consistently managed, representing a relatively small portion of the operating cash flow. The company's ability to consistently generate positive FCF suggests financial health and flexibility in funding operations, investments, and debt obligations.

The company's free cash flow (FCF) generation has varied over the years, with a noticeable increase in 2024. Capital expenditure appears to be consistently managed, representing a relatively small portion of the operating cash flow. The company's ability to consistently generate positive FCF suggests financial health and flexibility in funding operations, investments, and debt obligations.