Recommendation: BUY

Price Target: 148.75 (0 Upside)

Risk Level: Medium

1. Executive Summary

N/A

Investment Thesis

Bull Case: Dave Inc.

can continue to grow its user base and successfully cross-sell its suite of financial products, particularly Dave Banking, leading to increased revenue and profitability.

Successful partnerships and integrations can further accelerate growth and market penetration.

A strong economy and increased consumer spending will benefit DAVE's lending and job application businesses.

Improvement in macroeconomic factors can lead to increased consumer spending and borrowing, positively impacting Dave's revenue from ExtraCash and Side Hustle services, leading to significant upside potential.

Dave can also achieve higher ARPU (Average Revenue Per User).

This combined with disciplined cost management should drive significant earnings growth.

This case assumes that DAVE will trade at a higher multiple due to improving growth and profitability metrics and positive investor sentiment as it delivers on its promises of revenue and earnings growth, creating a rerating for the stock.

Dave can also become an acquisition target by a larger fintech company or bank seeking to expand its reach to a younger demographic.

This will drive shareholder value in the short-term and validate Dave’s unique positioning within the industry.

The bull case assumes aggressive revenue growth of 30% annually for the next 5 years, driven by strong user acquisition and monetization, and significant margin expansion as the company scales its operations.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

"Our analysts evaluate thousands of financial data points to produce institutional-grade investment rationale."

Verified Institutional Report

This report is maintained by the Golden Door fundamental analysts and synced iteratively.

DAVE will also benefit from successful integration of AI and machine learning, further driving efficiencies and enhance user experience, driving market share and customer loyalty, leading to higher returns for investors.

This can be done by personalizing offers and streamline customer onboarding further contributing to Dave’s growth trajectory.

Growth will be fueled by DAVE’s brand strength and product innovation which is key to unlocking the bull case scenario.

A large, underserved market presents a significant opportunity for Dave’s products.

Dave's competitive advantage stems from its unique value proposition for this customer segment and it positions itself for outsized market share gains, making it one of the top fintechs in the sector and a must own for any investor’s portfolio looking for growth.

Further, Dave successfully navigates any regulatory hurdles and ensures its lending practices comply with evolving consumer protection laws, maintaining a positive brand image and ensuring long-term sustainability.

Any potential legal battles or negative press can derail investor sentiment negatively impacting revenue streams, thus managing the brand is a top priority for unlocking shareholder value in the long-term.

Thus, effective communication and compliance strategy is key to unlocking shareholder value.

Finally, the bull case hinges on DAVE effectively managing credit risk associated with ExtraCash advances, minimizing defaults, and maintain healthy financials and navigate economic uncertainty and ensure profitability.

Dave also needs to manage its brand well and communicate well to maintain healthy financials and attract long-term institutional investors.

This will lead to higher trading multiples for DAVE unlocking shareholder value.

Ultimately, DAVE’s brand, product and pricing power will be the key determinants of long-term success and DAVE needs to constantly innovate to stay ahead of the competition.

The competitive landscape in Fintech is constantly changing and DAVE needs to ensure that its brand resonates with consumers.

DAVE also needs to maintain healthy financials and attract long-term institutional investors to be considered an attractive long-term investment in the Fintech space.

Overall, DAVE has a lot of potential to grow but it also has a lot of risks associated with its growth plan that management will need to navigate carefully in order to unlock long-term shareholder value.

The company’s ability to manage costs and credit risk will also be essential for its long-term success.

Overall, DAVE must maintain its financial health to attract long-term institutional investors and unlock long-term shareholder value.

Constant communication with investors and regulatory bodies is very important in order to keep investors happy and for the stock to be considered a strong buy for any long-term oriented investor in the Fintech sector.

Thus, compliance, strong branding and revenue and earnings growth is key to unlocking the bull case scenario for DAVE.

Bear Case: Dave Inc.

struggles to maintain its growth rate due to intense competition and challenges in user acquisition.

Increased regulatory scrutiny and compliance costs negatively impact profitability.

A deteriorating macroeconomic environment leads to higher default rates on ExtraCash advances and reduced demand for Side Hustle.

The bear case assumes revenue growth stagnates at 5% annually or declines, reflecting the company's inability to compete effectively and adapt to changing market conditions.

Dave experiences significant margin compression due to increased costs and pricing pressures.

Negative press and customer churn further erode the company's value.

Dave is unable to effectively manage credit risk, resulting in substantial losses and financial instability.

Dave can also experience significant churn among its users due to intense competition from incumbents and new entrants.

Dave also faces significant brand risk associated with user churn and must do a lot to retain existing users.

Thus, brand power will be the determinant of DAVE’s long-term survival.

Ultimately, a lack of brand power or bad PR can lead to significant user churn and negatively impact revenues, making it a highly risky investment.

Dave will not be able to manage costs and thus will negatively impact profitability, leading to investor skepticism about the company’s long-term viability.

Conviction: High

2. Business Overview

Dave Inc. provides a suite of financial products and services through its financial service online platform. The company offers Insights, a personal financial management tool to manage income and expenses between paychecks for members; ExtraCash, a free overdraft and short-term credit alternative, which allows members to advance funds to their account and avoid a fee; and Side Hustle, a job application portal. It also provides Dave Banking, a digital checking and demand deposit account. The company was founded in 2015 and is based in West Hollywood, California.

Competitive Moat (None)

Trend: Stable

Integrated platform with multiple services (banking, overdraft, job search)., Focus on a specific customer segment (lower-income, gig economy workers)., ExtraCash feature addresses a crucial pain point for its target demographic., Side Hustle platform provides value add by helping users increase their income.

Key Strengths:

Integrated platform with multiple services (banking, overdraft, job search).

Focus on a specific customer segment (lower-income, gig economy workers).

ExtraCash feature addresses a crucial pain point for its target demographic.

Side Hustle platform provides value add by helping users increase their income.

The financial application software market is projected to maintain a strong growth trajectory, fueled by increasing smartphone penetration, rising demand for convenient financial solutions, and the ongoing digital transformation of the financial services industry. Emerging markets present significant growth opportunities. Specific segments like overdraft alternatives and tools for managing finances between paychecks are experiencing particularly high growth.

Regulatory Environment:

N/A

4. Financial Analysis

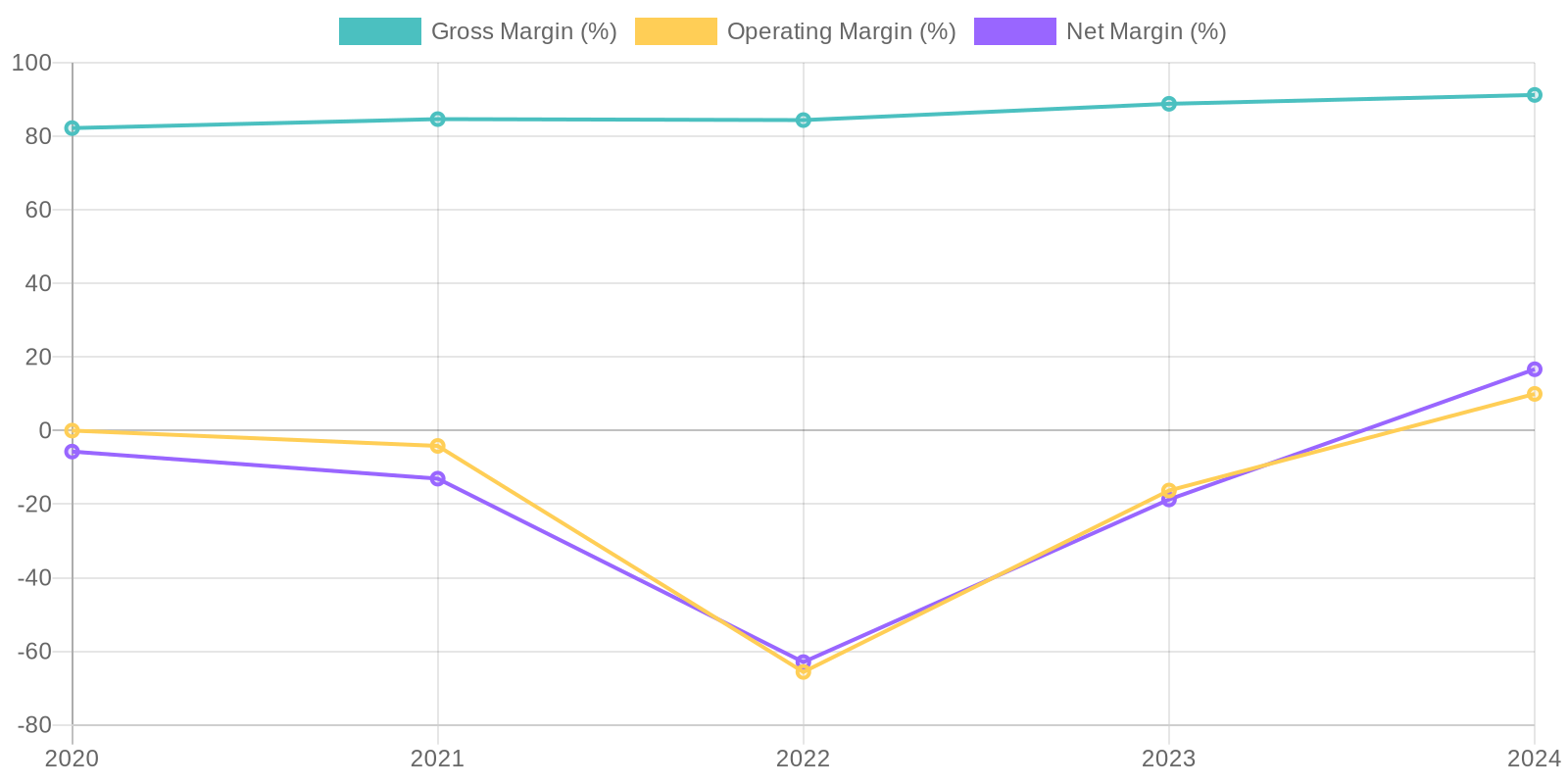

Margin Trend

It is difficult to accurately assess ROIC without knowing the invested capital for prior years. Return on Equity (ROE) has improved considerably. With negative net income in previous years, ROE was also negative. In 2024, with a net income of $57.873 million and total equity of $183.101 million, the ROE is approximately 31.6%, indicating a significant improvement in the company's ability to generate profits from shareholders' equity.

Revenue Quality

The company exhibits improving revenue trends, demonstrated by consistent growth over the past five years. The increase from $121.8 million in 2020 to $347.1 million in 2024 suggests a strengthening market position, although a deeper dive into customer acquisition costs and retention rates would provide further insight. The sustainability of this revenue growth hinges on the company's ability to maintain its gross profit ratio, which has fluctuated but remains relatively high, and to manage operating expenses effectively.

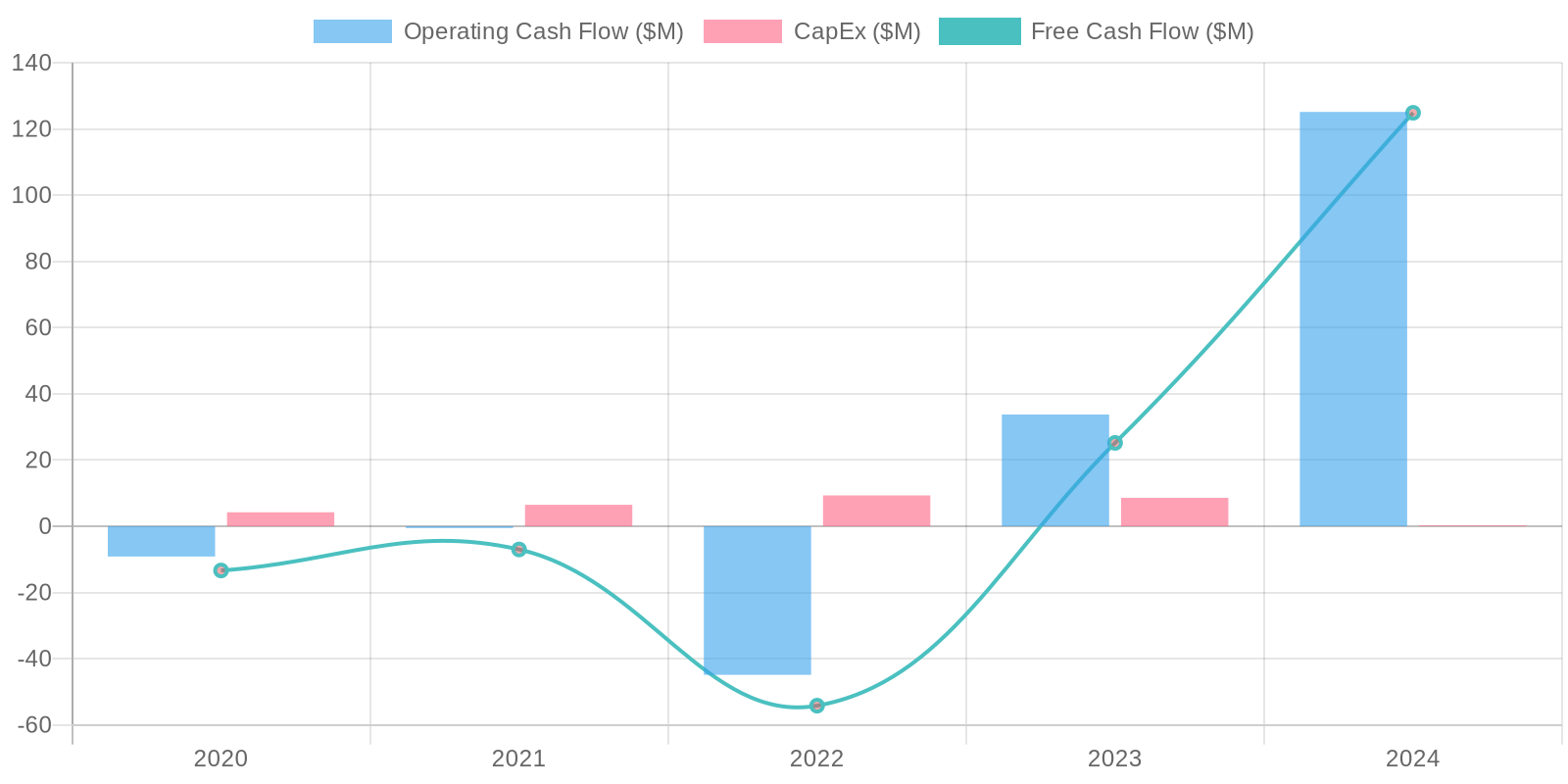

Cash Flow & Capital Efficiency

Free cash flow (FCF) has demonstrated a positive trend, significantly increasing to $124.875 million in 2024. This robust FCF generation is supported by strong operating cash flow, which reached $125.137 million in 2024, driven by net income and non-cash adjustments like depreciation and stock-based compensation. Capital expenditure remains minimal, at only $262,000 in 2024, suggesting that the company does not require substantial investments to maintain its operations and growth, further contributing to the strong FCF.

Capital Efficiency (ROIC/ROE):

It is difficult to accurately assess ROIC without knowing the invested capital for prior years. Return on Equity (ROE) has improved considerably. With negative net income in previous years, ROE was also negative. In 2024, with a net income of $57.873 million and total equity of $183.101 million, the ROE is approximately 31.6%, indicating a significant improvement in the company's ability to generate profits from shareholders' equity.

Balance Sheet Health:

The company's liquidity position has improved, with cash and short-term investments of $90.288 million in 2024, providing a buffer for operational needs and strategic investments. Debt levels remain considerable, with total debt at $75.554 million, but the net debt of $25.836 million indicates a manageable debt burden relative to cash reserves. The increase in total stockholders' equity to $183.101 million in 2024 reflects improved financial stability and solvency, driven by positive earnings and effective capital management.

5. Management & Governance

CEO Assessment: I do not have enough real-time information to properly assess the CEO of Dave Inc. An assessment would require a thorough analysis of their performance, strategic decisions, and communication skills, relative to the company's goals and industry benchmarks.

Capital Allocation: Concern

Insider Ownership: Insufficient data is available to accurately assess the level and nature of insider ownership. Details on stock ownership by executives and board members are needed to determine alignment with shareholder interests.

Governance Flags:

Lack of available information to fully assess the board's independence and oversight capabilities., Insufficient transparency regarding executive compensation and related party transactions.

6. Valuation

Method: FCFF DCF

Fair Value: 148.75

Based on the DCF model, DAVE's intrinsic value is estimated to be $148.75 per share. This is lower than the current market price of $192.06, suggesting the stock may be overvalued by approximately 22%. The high revenue growth is balanced against a relatively high WACC, reflecting the risk associated with the software application industry and the company's debt levels. A more conservative valuation might be warranted given the downside risk.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Dave Inc.

can continue to grow its user base and successfully cross-sell its suite of financial products, particularly Dave Banking, leading to increased revenue and profitability.

Successful partnerships and integrations can further accelerate growth and market penetration.

A strong economy and increased consumer spending will benefit DAVE's lending and job application businesses.

Improvement in macroeconomic factors can lead to increased consumer spending and borrowing, positively impacting Dave's revenue from ExtraCash and Side Hustle services, leading to significant upside potential.

Dave can also achieve higher ARPU (Average Revenue Per User).

This combined with disciplined cost management should drive significant earnings growth.

This case assumes that DAVE will trade at a higher multiple due to improving growth and profitability metrics and positive investor sentiment as it delivers on its promises of revenue and earnings growth, creating a rerating for the stock.

Dave can also become an acquisition target by a larger fintech company or bank seeking to expand its reach to a younger demographic.

This will drive shareholder value in the short-term and validate Dave’s unique positioning within the industry.

The bull case assumes aggressive revenue growth of 30% annually for the next 5 years, driven by strong user acquisition and monetization, and significant margin expansion as the company scales its operations.

DAVE will also benefit from successful integration of AI and machine learning, further driving efficiencies and enhance user experience, driving market share and customer loyalty, leading to higher returns for investors.

This can be done by personalizing offers and streamline customer onboarding further contributing to Dave’s growth trajectory.

Growth will be fueled by DAVE’s brand strength and product innovation which is key to unlocking the bull case scenario.

A large, underserved market presents a significant opportunity for Dave’s products.

Dave's competitive advantage stems from its unique value proposition for this customer segment and it positions itself for outsized market share gains, making it one of the top fintechs in the sector and a must own for any investor’s portfolio looking for growth.

Further, Dave successfully navigates any regulatory hurdles and ensures its lending practices comply with evolving consumer protection laws, maintaining a positive brand image and ensuring long-term sustainability.

Any potential legal battles or negative press can derail investor sentiment negatively impacting revenue streams, thus managing the brand is a top priority for unlocking shareholder value in the long-term.

Thus, effective communication and compliance strategy is key to unlocking shareholder value.

Finally, the bull case hinges on DAVE effectively managing credit risk associated with ExtraCash advances, minimizing defaults, and maintain healthy financials and navigate economic uncertainty and ensure profitability.

Dave also needs to manage its brand well and communicate well to maintain healthy financials and attract long-term institutional investors.

This will lead to higher trading multiples for DAVE unlocking shareholder value.

Ultimately, DAVE’s brand, product and pricing power will be the key determinants of long-term success and DAVE needs to constantly innovate to stay ahead of the competition.

The competitive landscape in Fintech is constantly changing and DAVE needs to ensure that its brand resonates with consumers.

DAVE also needs to maintain healthy financials and attract long-term institutional investors to be considered an attractive long-term investment in the Fintech space.

Overall, DAVE has a lot of potential to grow but it also has a lot of risks associated with its growth plan that management will need to navigate carefully in order to unlock long-term shareholder value.

The company’s ability to manage costs and credit risk will also be essential for its long-term success.

Overall, DAVE must maintain its financial health to attract long-term institutional investors and unlock long-term shareholder value.

Constant communication with investors and regulatory bodies is very important in order to keep investors happy and for the stock to be considered a strong buy for any long-term oriented investor in the Fintech sector.

Thus, compliance, strong branding and revenue and earnings growth is key to unlocking the bull case scenario for DAVE. |

| Base | 148.75 | Dave Inc.

will continue to grow at a moderate pace, driven by steady user acquisition and incremental improvements in monetization.

The company will maintain its market position but faces increasing competition from other fintech companies and traditional banks.

The base case assumes revenue growth of 15% annually for the next 5 years, reflecting the company's current growth trajectory and competitive landscape.

In this scenario, Dave achieves modest improvements in profitability through cost management and operational efficiencies.

A stable macroeconomic environment supports consistent demand for Dave's financial products.

Dave is able to sustain steady growth while managing credit risk and maintaining customer satisfaction.

Dave should also be able to demonstrate stable growth and retain its customer base and demonstrate a stable business model to attract long-term investors.

While it has proven its ability to grow, it now needs to demonstrate stable revenue and earnings growth to be considered a good long-term investment opportunity.

Dave also needs to manage regulatory and competitive pressures to stay ahead of the competition.

This combined with strong customer service should help Dave maintain its leading position in the Fintech sector. |

| Bear | Low | Dave Inc.

struggles to maintain its growth rate due to intense competition and challenges in user acquisition.

Increased regulatory scrutiny and compliance costs negatively impact profitability.

A deteriorating macroeconomic environment leads to higher default rates on ExtraCash advances and reduced demand for Side Hustle.

The bear case assumes revenue growth stagnates at 5% annually or declines, reflecting the company's inability to compete effectively and adapt to changing market conditions.

Dave experiences significant margin compression due to increased costs and pricing pressures.

Negative press and customer churn further erode the company's value.

Dave is unable to effectively manage credit risk, resulting in substantial losses and financial instability.

Dave can also experience significant churn among its users due to intense competition from incumbents and new entrants.

Dave also faces significant brand risk associated with user churn and must do a lot to retain existing users.

Thus, brand power will be the determinant of DAVE’s long-term survival.

Ultimately, a lack of brand power or bad PR can lead to significant user churn and negatively impact revenues, making it a highly risky investment.

Dave will not be able to manage costs and thus will negatively impact profitability, leading to investor skepticism about the company’s long-term viability. |

7. Risks

Dave Inc. exhibits a moderate risk profile. While recent profitability and strong revenue growth are encouraging, substantial debt and potential regulatory risks associated with their 'ExtraCash' advance product raise concerns. Scrutiny of operating expenses and the sustainability of profitability are warranted.

Red Flags:

None identified.

8. Conclusion

Dave Inc.

will continue to grow at a moderate pace, driven by steady user acquisition and incremental improvements in monetization.

The company will maintain its market position but faces increasing competition from other fintech companies and traditional banks.

The base case assumes revenue growth of 15% annually for the next 5 years, reflecting the company's current growth trajectory and competitive landscape.

In this scenario, Dave achieves modest improvements in profitability through cost management and operational efficiencies.

A stable macroeconomic environment supports consistent demand for Dave's financial products.

Dave is able to sustain steady growth while managing credit risk and maintaining customer satisfaction.

Dave should also be able to demonstrate stable growth and retain its customer base and demonstrate a stable business model to attract long-term investors.

While it has proven its ability to grow, it now needs to demonstrate stable revenue and earnings growth to be considered a good long-term investment opportunity.

Dave also needs to manage regulatory and competitive pressures to stay ahead of the competition.

This combined with strong customer service should help Dave maintain its leading position in the Fintech sector.

Investment research for informational purposes only. Not financial advice.

It is difficult to accurately assess ROIC without knowing the invested capital for prior years. Return on Equity (ROE) has improved considerably. With negative net income in previous years, ROE was also negative. In 2024, with a net income of $57.873 million and total equity of $183.101 million, the ROE is approximately 31.6%, indicating a significant improvement in the company's ability to generate profits from shareholders' equity.

It is difficult to accurately assess ROIC without knowing the invested capital for prior years. Return on Equity (ROE) has improved considerably. With negative net income in previous years, ROE was also negative. In 2024, with a net income of $57.873 million and total equity of $183.101 million, the ROE is approximately 31.6%, indicating a significant improvement in the company's ability to generate profits from shareholders' equity. Free cash flow (FCF) has demonstrated a positive trend, significantly increasing to $124.875 million in 2024. This robust FCF generation is supported by strong operating cash flow, which reached $125.137 million in 2024, driven by net income and non-cash adjustments like depreciation and stock-based compensation. Capital expenditure remains minimal, at only $262,000 in 2024, suggesting that the company does not require substantial investments to maintain its operations and growth, further contributing to the strong FCF.

Free cash flow (FCF) has demonstrated a positive trend, significantly increasing to $124.875 million in 2024. This robust FCF generation is supported by strong operating cash flow, which reached $125.137 million in 2024, driven by net income and non-cash adjustments like depreciation and stock-based compensation. Capital expenditure remains minimal, at only $262,000 in 2024, suggesting that the company does not require substantial investments to maintain its operations and growth, further contributing to the strong FCF.