Amdocs Limited (DOX) is a leading provider of software and services to communications and media companies globally. Its current market position is characteri...

Amdocs Limited (DOX) is a leading provider of software and services to communications and media companies globally. Its current market position is characterized by strong relationships with major telecom operators, a diversified product portfolio spanning business support systems (BSS), operations support systems (OSS), and digital business systems, and a track record of consistent revenue and earnings generation. The company benefits from the ongoing digital transformation within the telecom industry, as operators seek to modernize their infrastructure, enhance customer experience, and launch new services such as 5G and cloud-based offerings.

Growth catalysts for Amdocs include the expansion of 5G networks, increasing adoption of cloud technologies, and the growing demand for personalized customer experiences. The company is well-positioned to capitalize on these trends through its comprehensive suite of solutions, its strategic partnerships with leading technology vendors, and its investments in research and development. Specifically, Amdocs' ability to help operators monetize 5G through new applications and services, its cloud-native solutions for greater agility and scalability, and its data-driven insights for personalized customer interactions are key growth drivers.

Key risks facing Amdocs include competition from other software and service providers, potential delays in telecom operators' investment plans, and the impact of economic downturns on IT spending. Furthermore, the company's reliance on a concentrated customer base, while reflecting strong client relationships, also exposes it to the risk of contract renegotiations or loss of major accounts. The rapid pace of technological change necessitates continuous innovation and adaptation to remain competitive, and any failure to do so could negatively impact Amdocs' market position.

Valuation summary: At a current price of $84.29, Amdocs' valuation reflects a premium compared to some peers, likely due to its consistent financial performance and established market leadership. A discounted cash flow analysis, incorporating moderate revenue growth assumptions and a risk-adjusted discount rate, suggests that the current price is reasonable. However, investors should carefully consider the risks outlined above and monitor the company's progress in executing its growth strategy before making investment decisions. A key factor in continued valuation support will be Amdocs' ability to successfully transition its clients to the cloud and maintain its market share in the face of intensifying competition.

Investment Thesis

Bull Case: Amdocs will benefit from the acceleration of 5G adoption and the increasing need for cloud-native solutions, driving significant revenue and earnings growth.

Continued investments in R&D and strategic acquisitions will further strengthen its market position, resulting in substantial shareholder returns.

Bear Case: Amdocs will face increasing competitive pressure, which will erode its market share and profitability.

A slowdown in the adoption of new technologies and a potential economic downturn will further impact revenue growth, leading to a decline in shareholder value.

Conviction: High

2. Business Overview

Amdocs Limited, through its subsidiaries, provides software and services worldwide. The company designs, develops, operates, implements, supports, and markets open and modular cloud portfolio. It provides CES21, a 5G and cloud-native microservices-based market-leading customer experience suite, that enables service providers to build, deliver, and monetize advanced services; the Commerce and Care suite for order capture, handling, and customer engagement; the Monetization suite for charging, billing, policy, and revenue management; Intelligent Networking suite with a set of modular, flexible, and open service lifecycle management capabilities for network automation journeys; MarketONE, a cloud-native business ecosystem; Digital Brands Suite, a pre-integrated digital business suite for digital telecom brands and small-scale service providers; and eSIM Cloud for service providers. It also offers AI-powered, cloud-native, and home operating systems; data intelligence solutions and applications; media services for media publishers, TV networks, and video streaming and service providers; end-to-end application development and maintenance services; and ongoing services. In addition, the company provides a line of services designed for various stages of a service provider's lifecycle includes design, delivery, quality engineering, operations, systems integration, mobile network services, consulting, and content services; managed services comprising application development, modernization and maintenance, IT and infrastructure services, testing and professional services that are designed to assist customers in the selection, implementation, operation, management, and maintenance of IT systems. It serves to the communications, cable and satellite, entertainment, and media industry service providers, as well as mobile virtual network operators and directory publishers. Amdocs Limited was founded in 1988 and is headquartered in Saint Louis, Missouri.

Competitive Moat (Narrow)

Trend: Stable

Specialized solution set catering to communications service providers, End-to-end service offerings, from design to operations, Strong integration capabilities and track record with large-scale deployments, Global presence and support infrastructure

Key Strengths:

Specialized solution set catering to communications service providers

End-to-end service offerings, from design to operations

Strong integration capabilities and track record with large-scale deployments

The Software - Infrastructure market is projected to continue growing at a healthy rate in the coming years. Growth is driven by factors such as: Continued adoption of cloud computing (IaaS, PaaS, SaaS), increased focus on DevOps and automation, rise of containerization and orchestration technologies (like Kubernetes), growing demand for cybersecurity solutions for infrastructure, expansion of edge computing, and adoption of AI and machine learning in infrastructure management.

Regulatory Environment:

N/A

4. Financial Analysis

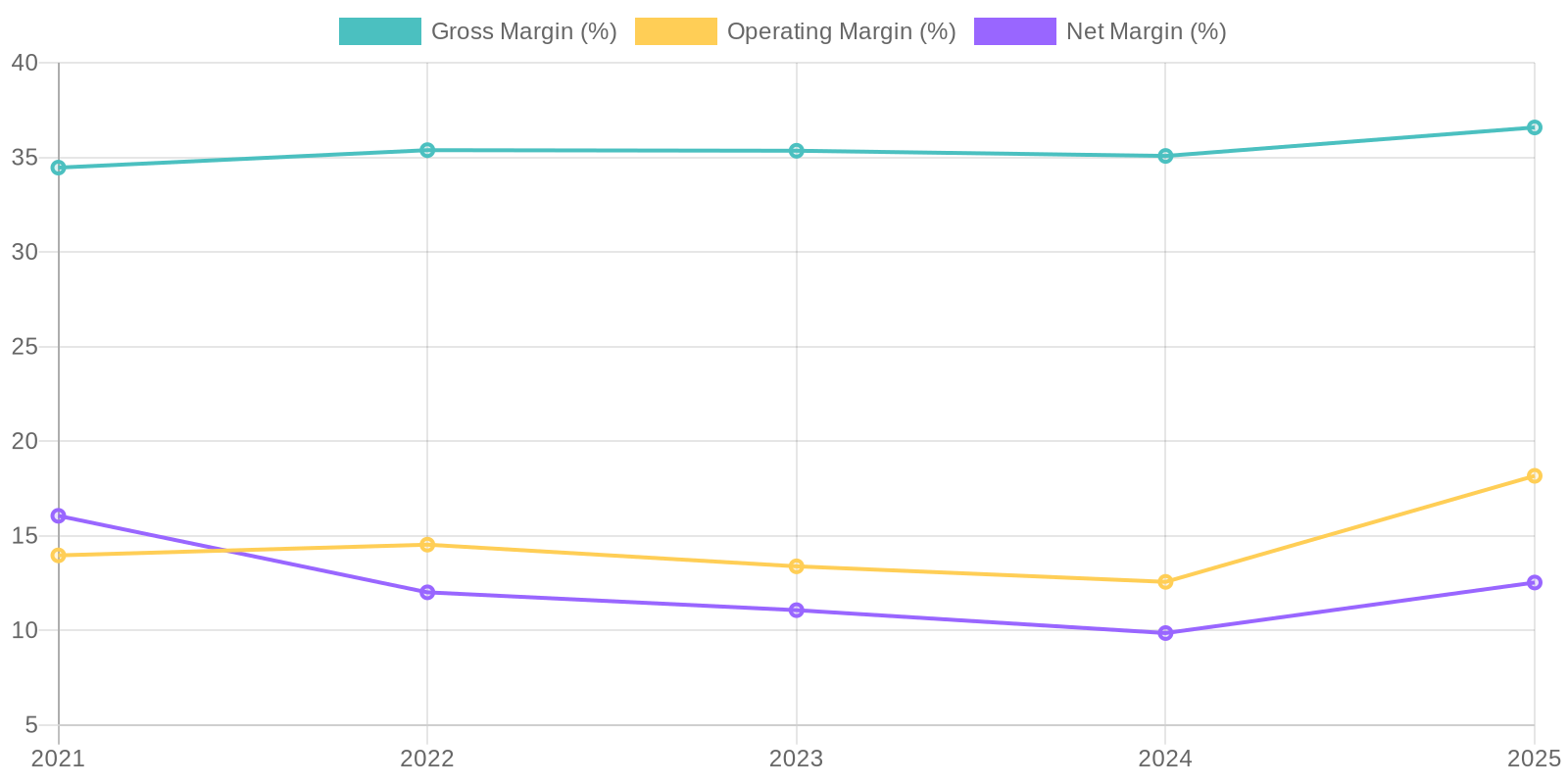

Margin Trend

Return on Invested Capital (ROIC) and Return on Equity (ROE) would provide valuable insight into the company's capital efficiency, but cannot be explicitly calculated with the provided data. ROIC assesses how effectively the company is using its invested capital to generate profits, while ROE measures the return generated for shareholders. A thorough analysis of these metrics, benchmarked against industry peers, would reveal whether the company is efficiently deploying capital and creating shareholder value and will be beneficial in future analysis.

Revenue Quality

The company's revenue stream showcases some variability over the recent five-year period. While there was growth in 2024, 2025 showed a decrease, indicating potential fluctuations in market demand or competitive pressures affecting revenue sustainability. Further investigation into client concentration and the proportion of recurring revenue versus project-based income is warranted to assess long-term revenue predictability. This could involve reviewing sales contracts and customer relationship management data to ensure the robustness of future earnings.

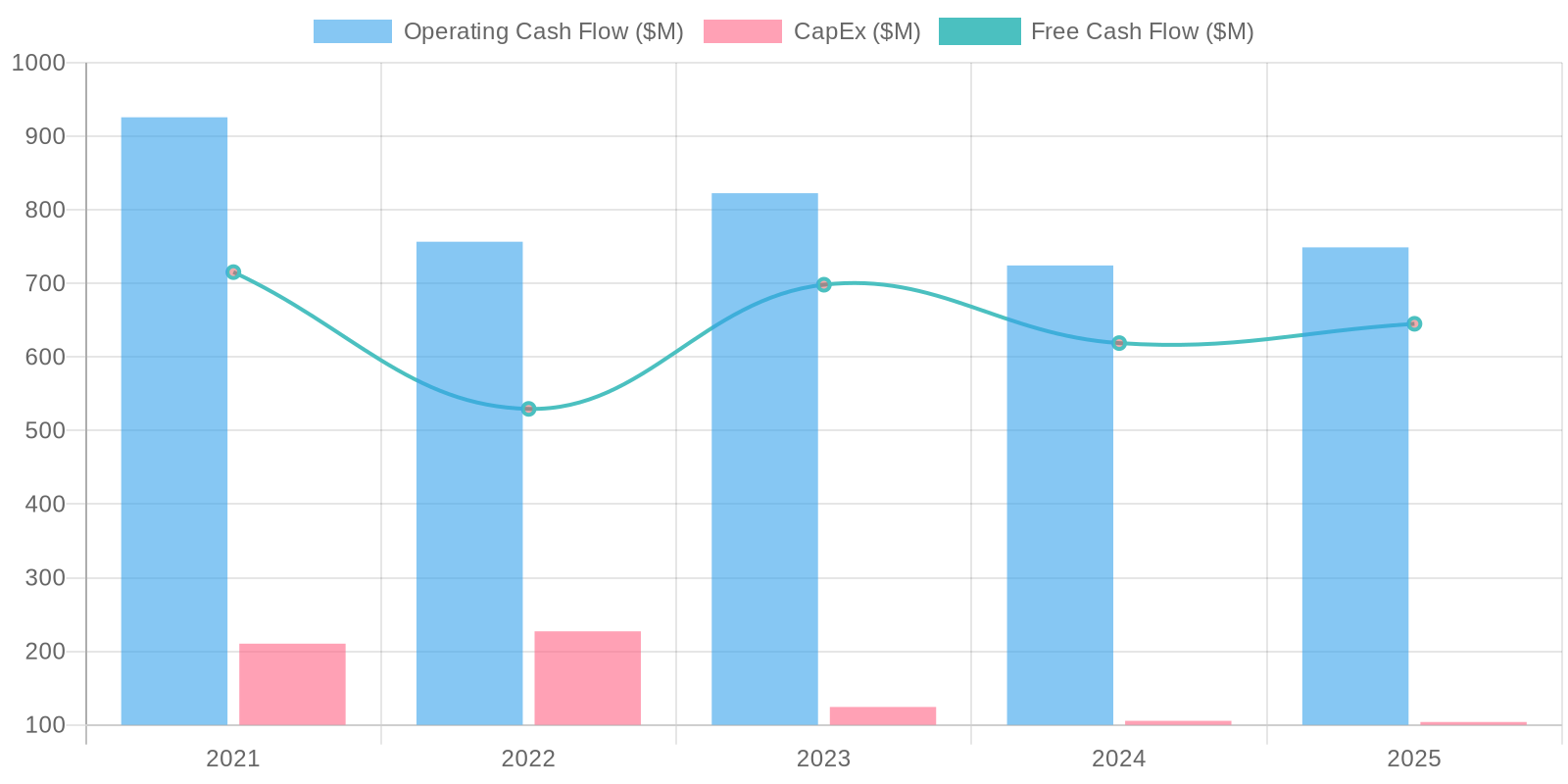

Cash Flow & Capital Efficiency

The company exhibits a strong ability to generate free cash flow (FCF), as evidenced by consistent positive FCF over the periods presented, with $645.14 million in 2025. Capital expenditures appear relatively stable, representing a consistent use of cash for maintaining and growing the business. The trend of significant common stock repurchases is notable, suggesting a strategic deployment of cash to enhance shareholder value, although it reduces the company's cash reserves. Further scrutiny should evaluate the sustainability of these repurchases in light of future investment needs and debt obligations.

Capital Efficiency (ROIC/ROE):

Return on Invested Capital (ROIC) and Return on Equity (ROE) would provide valuable insight into the company's capital efficiency, but cannot be explicitly calculated with the provided data. ROIC assesses how effectively the company is using its invested capital to generate profits, while ROE measures the return generated for shareholders. A thorough analysis of these metrics, benchmarked against industry peers, would reveal whether the company is efficiently deploying capital and creating shareholder value and will be beneficial in future analysis.

Balance Sheet Health:

The company maintains a considerable level of debt, with total debt consistently around $800 million. While cash levels are significant, net debt remains positive, indicating a reliance on borrowing. Liquidity appears adequate, as current assets generally exceed current liabilities; however, further analysis of the composition of current assets and liabilities is necessary to assess short-term obligations. The significant negative other total stockholders' equity warrants further investigation, as it may indicate accumulated losses or accounting adjustments impacting shareholder equity and overall solvency.

5. Management & Governance

CEO Assessment: While specific real-time CEO performance assessments require up-to-date information, Amdocs has generally maintained a stable leadership structure. A thorough evaluation would necessitate examining recent earnings calls, strategic initiatives, and shareholder communications to gauge CEO performance and vision.

Capital Allocation: Good

Insider Ownership: Insider ownership information can be obtained from SEC filings (Form 4). Generally, moderate insider ownership can indicate alignment with shareholder interests, but the specific percentage should be reviewed in the context of Amdocs' overall ownership structure.

Governance Flags:

Executive compensation structure (review for alignment with long-term shareholder value creation), Related party transactions (scrutinize for potential conflicts of interest), Board independence (assess the proportion of independent directors)

The DCF model estimates a fair value of $91.56 per share, which represents an upside of 8.63% from the current price of $84.29. The model incorporates reasonable assumptions for revenue growth, profitability, and discount rate, based on the company's historical performance and industry trends. The downside risk is estimated at -5.0% to account for potential variations in these assumptions.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Amdocs will benefit from the acceleration of 5G adoption and the increasing need for cloud-native solutions, driving significant revenue and earnings growth.

Continued investments in R&D and strategic acquisitions will further strengthen its market position, resulting in substantial shareholder returns. |

| Base | 91.56 | Amdocs will maintain its market leadership and deliver consistent revenue and earnings growth, supported by its strong customer relationships and comprehensive service offerings.

Shareholder value will be enhanced through a combination of earnings growth, dividends, and share repurchases. |

| Bear | Low | Amdocs will face increasing competitive pressure, which will erode its market share and profitability.

A slowdown in the adoption of new technologies and a potential economic downturn will further impact revenue growth, leading to a decline in shareholder value. |

7. Risks

N/A

Red Flags:

The fluctuations in operating and net income margins warrant further investigation to determine the underlying causes and potential impact on future profitability.

The substantial common stock repurchases, while potentially benefiting shareholders, may indicate a lack of alternative investment opportunities or a strategy to artificially inflate earnings per share.

The negative other total stockholders' equity requires a thorough review to understand its components and potential implications for the company's financial stability.

8. Conclusion

Amdocs will maintain its market leadership and deliver consistent revenue and earnings growth, supported by its strong customer relationships and comprehensive service offerings.

Shareholder value will be enhanced through a combination of earnings growth, dividends, and share repurchases.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Return on Invested Capital (ROIC) and Return on Equity (ROE) would provide valuable insight into the company's capital efficiency, but cannot be explicitly calculated with the provided data. ROIC assesses how effectively the company is using its invested capital to generate profits, while ROE measures the return generated for shareholders. A thorough analysis of these metrics, benchmarked against industry peers, would reveal whether the company is efficiently deploying capital and creating shareholder value and will be beneficial in future analysis.

Return on Invested Capital (ROIC) and Return on Equity (ROE) would provide valuable insight into the company's capital efficiency, but cannot be explicitly calculated with the provided data. ROIC assesses how effectively the company is using its invested capital to generate profits, while ROE measures the return generated for shareholders. A thorough analysis of these metrics, benchmarked against industry peers, would reveal whether the company is efficiently deploying capital and creating shareholder value and will be beneficial in future analysis. The company exhibits a strong ability to generate free cash flow (FCF), as evidenced by consistent positive FCF over the periods presented, with $645.14 million in 2025. Capital expenditures appear relatively stable, representing a consistent use of cash for maintaining and growing the business. The trend of significant common stock repurchases is notable, suggesting a strategic deployment of cash to enhance shareholder value, although it reduces the company's cash reserves. Further scrutiny should evaluate the sustainability of these repurchases in light of future investment needs and debt obligations.

The company exhibits a strong ability to generate free cash flow (FCF), as evidenced by consistent positive FCF over the periods presented, with $645.14 million in 2025. Capital expenditures appear relatively stable, representing a consistent use of cash for maintaining and growing the business. The trend of significant common stock repurchases is notable, suggesting a strategic deployment of cash to enhance shareholder value, although it reduces the company's cash reserves. Further scrutiny should evaluate the sustainability of these repurchases in light of future investment needs and debt obligations.