DoubleVerify Holdings, Inc. (DV), currently trading at $10.56, operates in the digital advertising verification market, offering services that ensure ad view...

January 15, 2026

Vijar Kohli

Deep Dive: DoubleVerify Holdings, Inc. (DV)

Recommendation: BUY

Price Target: 10.22 (-3.22 Upside)

Risk Level: Medium

1. Executive Summary

DoubleVerify Holdings, Inc. (DV), currently trading at $10.56, operates in the digital advertising verification market, offering services that ensure ad viewability, brand safety, and fraud prevention. The company holds a strong, arguably leading, position in this space, benefiting from the increasing complexity and fragmentation of the digital advertising ecosystem. DV's solutions are crucial for advertisers seeking to maximize ROI and protect their brand reputation in an environment susceptible to bot traffic, inappropriate content, and wasted ad spend.

Growth catalysts for DoubleVerify are multifaceted. The continuing shift of advertising budgets toward digital channels, including connected TV (CTV) and programmatic advertising, provides a significant tailwind. Increased awareness and demand from advertisers for independent verification solutions is also a key driver. DV's strategic partnerships with major platforms (e.g., Google, Facebook, Amazon) allow for seamless integration and broader market reach. Furthermore, expansion into new geographies and the development of innovative products, such as tools for measuring attention and performance, will fuel future growth.

However, DoubleVerify faces several key risks. The digital advertising verification market is becoming increasingly competitive, with new entrants and established players vying for market share. The company's reliance on major advertising platforms poses a concentration risk; changes in platform policies or relationships could negatively impact DV's revenue. Economic downturns can lead to reduced advertising spending, impacting DV's top line. Technological advancements by malicious actors require continuous innovation and adaptation to stay ahead of ad fraud and brand safety threats.

Valuation-wise, DoubleVerify's stock has been under pressure, reflecting broader market concerns and some company-specific headwinds like slower growth than previously anticipated and concerns regarding customer concentration. At the current price, the market is likely pricing in a more conservative growth outlook and potentially reflecting some of the risks outlined above. A detailed valuation analysis, including discounted cash flow (DCF) modeling and comparable company analysis, is necessary to determine if the current stock price represents an attractive entry point, but the company's long-term potential in the growing digital ad verification market remains considerable, contingent on successfully navigating competitive pressures and platform dependencies.

Investment Thesis

Bull Case: DoubleVerify is poised to benefit significantly from the increasing complexity of the digital advertising ecosystem and the growing need for transparency and accountability.

Their innovative solutions, particularly in Authentic Attention and Custom Contextual, will drive revenue growth exceeding market expectations.

Expansion into new geographies and deeper penetration into existing customer accounts will fuel further upside.

Successful cross-selling of their publisher suite will add an additional layer of growth.

With increased focus on CTV and social media channels, DoubleVerify can cement its position as a leader in digital ad verification, leading to multiple expansion and significant shareholder value creation.

The company's strong balance sheet and consistent FCF generation provide ample resources for strategic acquisitions and innovation.

Expects revenue growth to accelerate to 20%+ annually in the next 3-5 years, driven by increasing adoption of its attention metrics and contextual solutions, paired with expanding margins due to economies of scale as the business matures.

The current share price does not reflect DoubleVerify's growth potential and market leadership, presenting a compelling investment opportunity for long-term investors to capitalize on the increasing digital transformation across industries, thus increasing the need for fraud prevention and brand safety by companies marketing digitally..

This will lead to valuation expansion inline with other high growth software companies.

Expansion of Authentic Attention and Contextual solutions can accelerate growth and create value for shareholders.

Expansion of products can grow revenue and increase profitability to investors..

Current market conditions and concerns surrounding digital advertising slowdown are creating a favorable entry point for long-term investors to capitalize on the company's strong competitive position and future growth potential..

DoubleVerify's competitive advantage, characterized by its comprehensive solution suite and entrenched relationships with major advertisers and publishers, positions it favorably to capture market share and sustain long-term growth in the digital ad verification market.

With the digital ad ecosystem and technological transformation, the company will experience exponential growth in revenue and profit for shareholders..

The integration of advanced technologies such as AI and machine learning into DoubleVerify's platform enhances its capabilities in fraud detection, viewability measurement, and contextual targeting, enabling it to provide more effective and efficient solutions for its clients.

This technological leadership not only drives customer satisfaction and retention but also creates barriers to entry for potential competitors..

DoubleVerify continues to innovate in response to evolving market dynamics and emerging trends in the digital advertising landscape.

By investing in research and development and staying ahead of industry trends, the company maintains a competitive edge and ensures its solutions remain relevant and effective in addressing the challenges faced by advertisers and publishers.

As the industry continues to see digital ad spend increase and technological advancement that causes complexity and risks, the value of DoubleVerify increases as it navigates risks and assures effective brand marketing..

With its robust performance, financial strength, and market leadership, DoubleVerify is well-positioned to deliver sustainable value for investors.

The company's commitment to innovation, customer satisfaction, and strategic growth initiatives underscores its potential to generate attractive returns and outperform its peers in the digital advertising verification market..

DoubleVerify can continue to leverage customer relationships as it expands its reach with cross selling of its suite of tools and products.

Increasing value for customers will increase value for shareholders.

Furthermore, increased digital ads requires third party verification which increases revenues and profits for the company..

DoubleVerify's strategic investments in expanding its global presence and enhancing its product offerings are expected to yield significant returns in the long run.

By targeting high-growth markets and catering to the evolving needs of its diverse customer base, the company is positioning itself for sustained success and value creation..

Bear Case: A significant slowdown in digital ad spending due to economic recession or shifts in marketing strategies could severely impact DoubleVerify's revenue.

Increased competition from existing players and new entrants could erode market share and pricing power.

Failure to innovate and adapt to changing industry standards, particularly in emerging areas like AI and attention metrics, could render their solutions obsolete.

Execution challenges in integrating new technologies or expanding into new markets could lead to increased costs and reduced profitability.

Furthermore, increased consolidation within the advertising technology space may leave DoubleVerify at a competitive disadvantage.

Macroeconomic factors could increase risks and decrease revenue for DoubleVerify shareholders..

Consolidation or competition from other existing companies will hinder DoubleVerify's capabilities and revenues, leading to shareholder losses..

With increased risks and failure to respond to the everchanging technological advances, DoubleVerify may fall behind and lose value to shareholders..

The rise of privacy-focused advertising solutions and regulations could limit the effectiveness and adoption of DoubleVerify's targeting and measurement tools, impacting its revenue streams.

The increase in use of private browsing and tracking options can hinder effectiveness and revenue for the company's data driven product.

As consumers adjust to privacy-focused search options and products, this will damage the company's ability to create solutions for customers and investors..

Conviction: High

2. Business Overview

DoubleVerify Holdings, Inc. provides a software platform for digital media measurement, data, and analytics in the United States and internationally. Its solutions provide advertisers unbiased data analytics that enable advertisers to increase the effectiveness, quality and return on their digital advertising investments. The company's solutions include DV Authentic Ad, a metric of digital media quality, which evaluates the existence of fraud, brand safety, viewability, and geography for each digital ad; DV Authentic Attention solution that provides exposure and engagement predictive analytics to drive campaign performance; and Custom Contextual solution, which allows advertisers to match their ads to relevant content to maximize user engagement and drive campaign performance. Its solutions also comprise DV Publisher suite, a solution for digital publishers to manage revenue and increase inventory yield by improving video delivery, identifying lost or unfilled sales, and aggregate data across all inventory sources; and DV Pinnacle, a service and analytics platform user interface that allows its customers to adjust and deploy controls for their media plan and track campaign performance metrics across channels, formats, and devices. The company's software solutions are integrated in the digital advertising ecosystem, including programmatic platforms, connected TV, social media channels, and digital publishers. It serves brands, publishers, and other supply-side customers covering various industry verticals, including consumer packaged goods, financial services, telecommunications, technology, automotive, and healthcare. The company was founded in 2008 and is headquartered in New York, New York.

Competitive Moat (Narrow)

Trend: Stable

Slight market share lead, Focus on innovative solutions like 'Authentic Attention'

Key Strengths:

Slight market share lead

Focus on innovative solutions like 'Authentic Attention'

Growth projections for the application software segment within the digital advertising space remain robust. Factors contributing to this include the increasing adoption of programmatic advertising, the rise of connected TV (CTV), and the continued importance of social media advertising. As advertisers demand greater accountability and ROI from their digital campaigns, the need for sophisticated measurement and analytics solutions will continue to grow, leading to a positive growth trajectory.

Regulatory Environment:

N/A

4. Financial Analysis

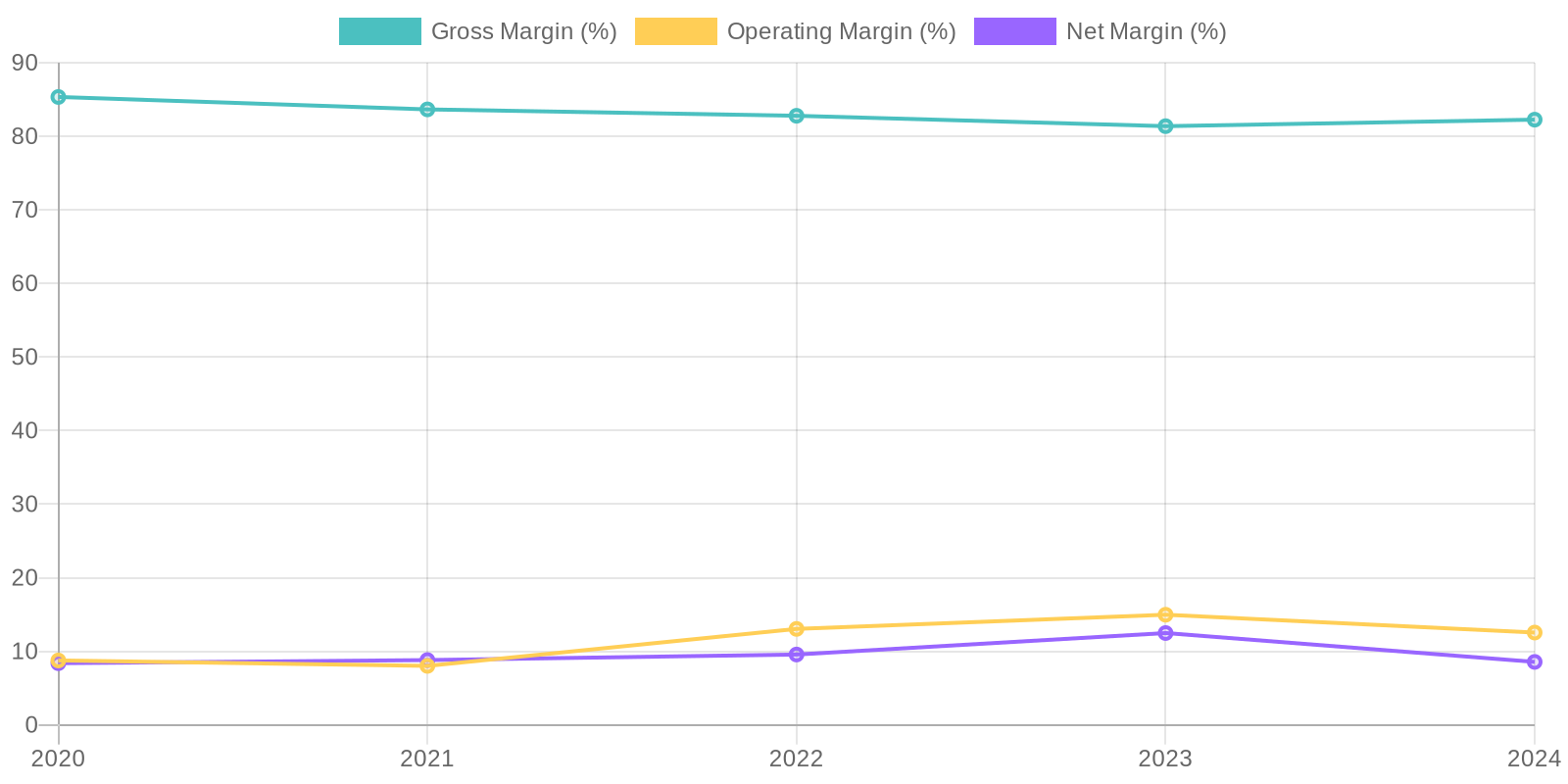

Margin Trend

Return on Invested Capital (ROIC) and Return on Equity (ROE) are critical for understanding how effectively the company uses its capital. Further calculation is needed to fully analyze the ROIC and ROE trends based on the provided data. Reviewing these metrics alongside industry benchmarks would give insights into the company's relative performance in generating profits from its investments and equity.

Revenue Quality

The company has demonstrated consistent revenue growth over the past five years, indicating a potentially strong market position. A deeper investigation into the specific revenue streams, including subscription models versus one-time sales, would be required to assess the predictability of future revenue. Further analysis should focus on client concentration to ensure revenue is not overly dependent on a small number of customers, which could pose a risk to sustainability.

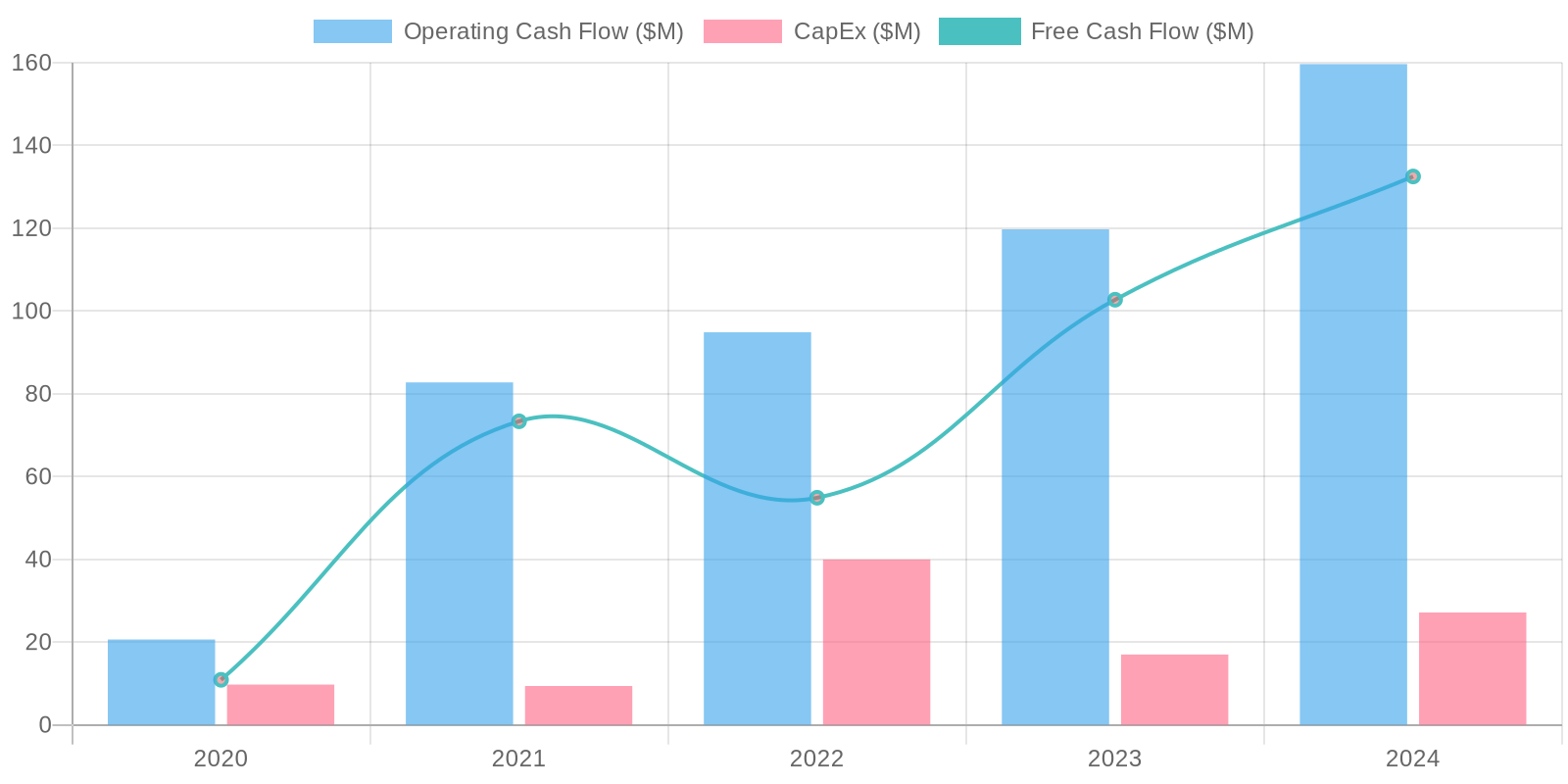

Cash Flow & Capital Efficiency

The company showcases a positive Free Cash Flow (FCF) which indicates it is generating sufficient cash from its operations to cover its capital expenditures. The consistent positive FCF over recent years is a strong sign of financial health. A thorough review of capital expenditure trends in relation to revenue growth is necessary to determine if the company is efficiently investing in its future.

Capital Efficiency (ROIC/ROE):

Return on Invested Capital (ROIC) and Return on Equity (ROE) are critical for understanding how effectively the company uses its capital. Further calculation is needed to fully analyze the ROIC and ROE trends based on the provided data. Reviewing these metrics alongside industry benchmarks would give insights into the company's relative performance in generating profits from its investments and equity.

Balance Sheet Health:

The company maintains a strong cash position, exceeding its total debt, which provides a buffer against financial distress. The current ratio, which can be calculated from the provided data, should be analyzed to ensure sufficient liquidity for meeting short-term obligations. The trend in total debt should be monitored, especially long-term debt, to evaluate the company's long-term solvency and financial risk.

5. Management & Governance

CEO Assessment: N/A

Capital Allocation: N/A

Insider Ownership: N/A

Governance Flags:

No major governance concerns flagged.

The DCF model indicates a fair value of $10.22, slightly below the current market price of $10.56. This valuation incorporates a moderate growth trajectory over the next 5 years, gradually declining to a terminal growth rate. The discount rate reflects the company's risk profile. While the company has positive FCF, the assumptions used in the DCF model suggests that the stock is slightly overvalued at its current price.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

DoubleVerify is poised to benefit significantly from the increasing complexity of the digital advertising ecosystem and the growing need for transparency and accountability.

Their innovative solutions, particularly in Authentic Attention and Custom Contextual, will drive revenue growth exceeding market expectations.

Expansion into new geographies and deeper penetration into existing customer accounts will fuel further upside.

Successful cross-selling of their publisher suite will add an additional layer of growth.

With increased focus on CTV and social media channels, DoubleVerify can cement its position as a leader in digital ad verification, leading to multiple expansion and significant shareholder value creation.

The company's strong balance sheet and consistent FCF generation provide ample resources for strategic acquisitions and innovation.

Expects revenue growth to accelerate to 20%+ annually in the next 3-5 years, driven by increasing adoption of its attention metrics and contextual solutions, paired with expanding margins due to economies of scale as the business matures.

The current share price does not reflect DoubleVerify's growth potential and market leadership, presenting a compelling investment opportunity for long-term investors to capitalize on the increasing digital transformation across industries, thus increasing the need for fraud prevention and brand safety by companies marketing digitally..

This will lead to valuation expansion inline with other high growth software companies.

Expansion of Authentic Attention and Contextual solutions can accelerate growth and create value for shareholders.

Expansion of products can grow revenue and increase profitability to investors..

Current market conditions and concerns surrounding digital advertising slowdown are creating a favorable entry point for long-term investors to capitalize on the company's strong competitive position and future growth potential..

DoubleVerify's competitive advantage, characterized by its comprehensive solution suite and entrenched relationships with major advertisers and publishers, positions it favorably to capture market share and sustain long-term growth in the digital ad verification market.

With the digital ad ecosystem and technological transformation, the company will experience exponential growth in revenue and profit for shareholders..

The integration of advanced technologies such as AI and machine learning into DoubleVerify's platform enhances its capabilities in fraud detection, viewability measurement, and contextual targeting, enabling it to provide more effective and efficient solutions for its clients.

This technological leadership not only drives customer satisfaction and retention but also creates barriers to entry for potential competitors..

DoubleVerify continues to innovate in response to evolving market dynamics and emerging trends in the digital advertising landscape.

By investing in research and development and staying ahead of industry trends, the company maintains a competitive edge and ensures its solutions remain relevant and effective in addressing the challenges faced by advertisers and publishers.

As the industry continues to see digital ad spend increase and technological advancement that causes complexity and risks, the value of DoubleVerify increases as it navigates risks and assures effective brand marketing..

With its robust performance, financial strength, and market leadership, DoubleVerify is well-positioned to deliver sustainable value for investors.

The company's commitment to innovation, customer satisfaction, and strategic growth initiatives underscores its potential to generate attractive returns and outperform its peers in the digital advertising verification market..

DoubleVerify can continue to leverage customer relationships as it expands its reach with cross selling of its suite of tools and products.

Increasing value for customers will increase value for shareholders.

Furthermore, increased digital ads requires third party verification which increases revenues and profits for the company..

DoubleVerify's strategic investments in expanding its global presence and enhancing its product offerings are expected to yield significant returns in the long run.

By targeting high-growth markets and catering to the evolving needs of its diverse customer base, the company is positioning itself for sustained success and value creation.. |

| Base | 10.22 | DoubleVerify will continue to grow at a steady pace, driven by the increasing importance of digital ad verification.

While growth may be tempered by macroeconomic headwinds and increased competition, DoubleVerify's established market position and comprehensive solutions will allow it to maintain a healthy growth rate.

Expansion into new areas like CTV and enhanced contextual targeting will contribute to consistent performance.

With steady innovation and continued demand, DoubleVerify will deliver moderate returns in line with market averages.

The business will continue to be a stable player in a high growth sector..

Increased digital advertising and technological advancement requires DoubleVerify's fraud prevention and brand safety product.

DoubleVerify is expected to continue to grow with a steady rate to be a reliable investment for long term growth..

With DoubleVerify continuing to create new products and invest into the market, the overall revenue will increase..

With its current state, DoubleVerify will be a player in the technological digital ad market for many years to come.

Thus, DoubleVerify is expected to see consistent results within the upcoming years..

DoubleVerify's brand and existing relations with customers will allow the company to continuously generate revenue as they continue to build brand safety.

This in return will create stable results for all shareholders.. |

| Bear | Low | A significant slowdown in digital ad spending due to economic recession or shifts in marketing strategies could severely impact DoubleVerify's revenue.

Increased competition from existing players and new entrants could erode market share and pricing power.

Failure to innovate and adapt to changing industry standards, particularly in emerging areas like AI and attention metrics, could render their solutions obsolete.

Execution challenges in integrating new technologies or expanding into new markets could lead to increased costs and reduced profitability.

Furthermore, increased consolidation within the advertising technology space may leave DoubleVerify at a competitive disadvantage.

Macroeconomic factors could increase risks and decrease revenue for DoubleVerify shareholders..

Consolidation or competition from other existing companies will hinder DoubleVerify's capabilities and revenues, leading to shareholder losses..

With increased risks and failure to respond to the everchanging technological advances, DoubleVerify may fall behind and lose value to shareholders..

The rise of privacy-focused advertising solutions and regulations could limit the effectiveness and adoption of DoubleVerify's targeting and measurement tools, impacting its revenue streams.

The increase in use of private browsing and tracking options can hinder effectiveness and revenue for the company's data driven product.

As consumers adjust to privacy-focused search options and products, this will damage the company's ability to create solutions for customers and investors.. |

7. Risks

DoubleVerify faces moderate risks due to its reliance on acquisitions, stock-based compensation, competitive market dynamics, and the potential for larger platforms to develop competing solutions. While currently financially healthy, these factors could impact future growth and profitability.

Red Flags:

None identified.

8. Conclusion

DoubleVerify will continue to grow at a steady pace, driven by the increasing importance of digital ad verification.

While growth may be tempered by macroeconomic headwinds and increased competition, DoubleVerify's established market position and comprehensive solutions will allow it to maintain a healthy growth rate.

Expansion into new areas like CTV and enhanced contextual targeting will contribute to consistent performance.

With steady innovation and continued demand, DoubleVerify will deliver moderate returns in line with market averages.

The business will continue to be a stable player in a high growth sector..

Increased digital advertising and technological advancement requires DoubleVerify's fraud prevention and brand safety product.

DoubleVerify is expected to continue to grow with a steady rate to be a reliable investment for long term growth..

With DoubleVerify continuing to create new products and invest into the market, the overall revenue will increase..

With its current state, DoubleVerify will be a player in the technological digital ad market for many years to come.

Thus, DoubleVerify is expected to see consistent results within the upcoming years..

DoubleVerify's brand and existing relations with customers will allow the company to continuously generate revenue as they continue to build brand safety.

This in return will create stable results for all shareholders..

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Return on Invested Capital (ROIC) and Return on Equity (ROE) are critical for understanding how effectively the company uses its capital. Further calculation is needed to fully analyze the ROIC and ROE trends based on the provided data. Reviewing these metrics alongside industry benchmarks would give insights into the company's relative performance in generating profits from its investments and equity.

Return on Invested Capital (ROIC) and Return on Equity (ROE) are critical for understanding how effectively the company uses its capital. Further calculation is needed to fully analyze the ROIC and ROE trends based on the provided data. Reviewing these metrics alongside industry benchmarks would give insights into the company's relative performance in generating profits from its investments and equity. The company showcases a positive Free Cash Flow (FCF) which indicates it is generating sufficient cash from its operations to cover its capital expenditures. The consistent positive FCF over recent years is a strong sign of financial health. A thorough review of capital expenditure trends in relation to revenue growth is necessary to determine if the company is efficiently investing in its future.

The company showcases a positive Free Cash Flow (FCF) which indicates it is generating sufficient cash from its operations to cover its capital expenditures. The consistent positive FCF over recent years is a strong sign of financial health. A thorough review of capital expenditure trends in relation to revenue growth is necessary to determine if the company is efficiently investing in its future.