Deep Dive: Enfusion, Inc. (ENFN)

Recommendation: HOLD Price Target: 12.5 (0.16 Upside) Risk Level: N/A

1. Executive Summary

Enfusion, Inc. (ENFN) is a provider of cloud-native investment management software and services for hedge funds, asset managers, and other financial institutions. Its platform integrates portfolio management, order and execution management, accounting, and investor relations functionalities, offering a streamlined and comprehensive solution for investment operations. At a current price of $10.76, Enfusion is navigating a competitive landscape while pursuing growth through product innovation and market expansion.

Enfusion's growth is fueled by several key catalysts. The increasing complexity of investment strategies and regulatory requirements drives demand for integrated, cloud-based solutions. The company's ability to win larger enterprise clients and cross-sell additional modules to existing customers is also a significant growth driver. Further, geographic expansion, particularly in the Asia-Pacific region, presents a substantial opportunity.

However, Enfusion faces several key risks. Intense competition from established players and emerging fintech firms poses a continuous threat to market share. The company's reliance on key personnel and its ability to retain talent are crucial. Macroeconomic headwinds, such as rising interest rates and inflation, could negatively impact investment firms' budgets and, consequently, Enfusion's sales cycle. Cybersecurity risks and data privacy regulations also present ongoing challenges.

Valuation-wise, Enfusion's current stock price reflects a blend of optimism regarding its growth potential and caution concerning its profitability and competition. A comprehensive valuation would require a detailed analysis of its revenue growth rate, profitability margins, and comparable company multiples, considering its current market position and the outlined risks and opportunities. Ultimately, the market's perception of Enfusion's ability to execute its growth strategy and achieve sustainable profitability will be critical in determining its future stock performance.

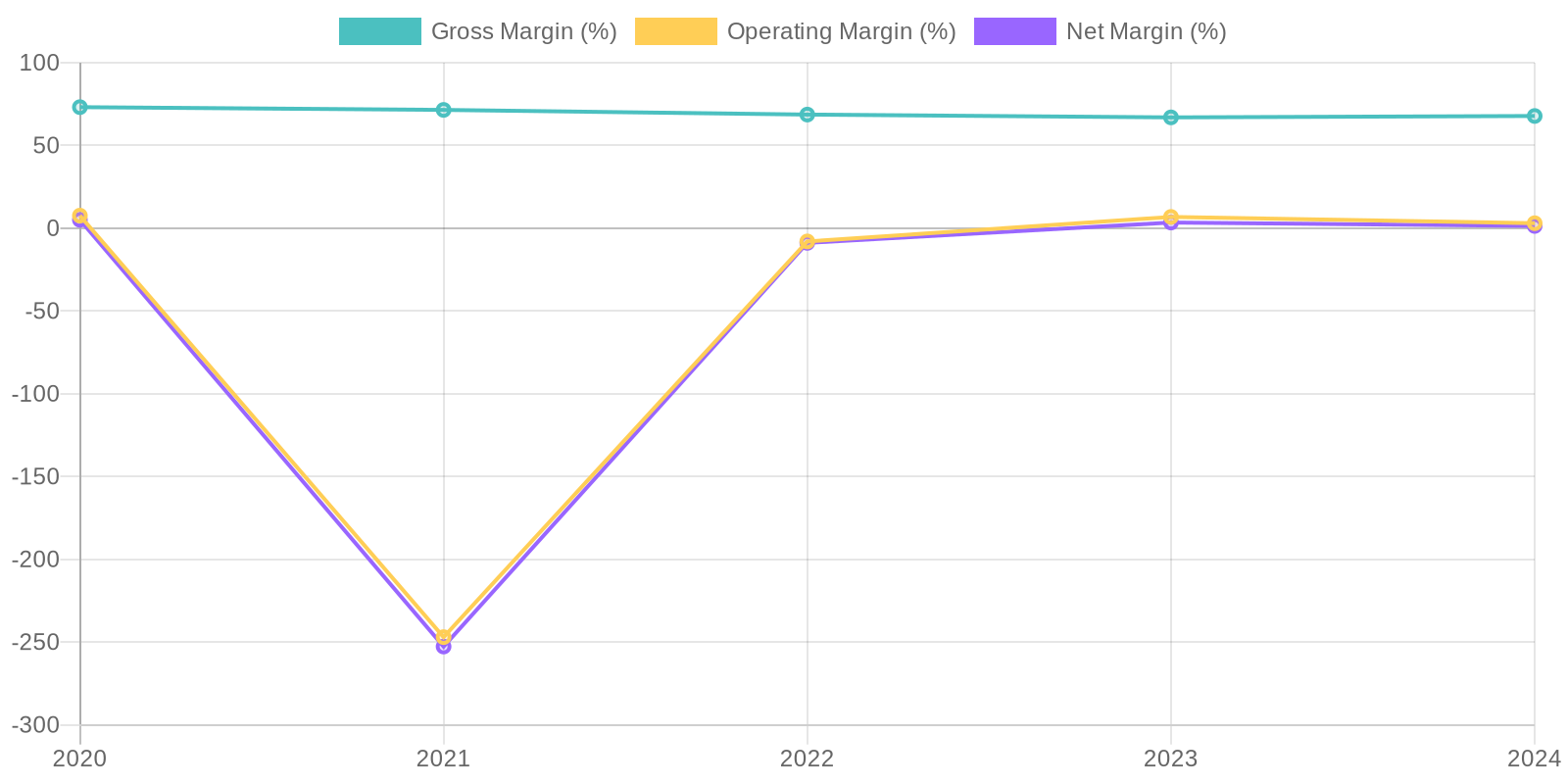

Calculating ROIC is difficult without invested capital details but analyzing available data suggests concerns. The company has demonstrated fluctuating profitability relative to its equity, with negative ROE in 2021 and 2022, meaning the company was losing money on shareholder investment. The ROE increased in 2023 as the company returned to profitability, but decreased again in 2024.

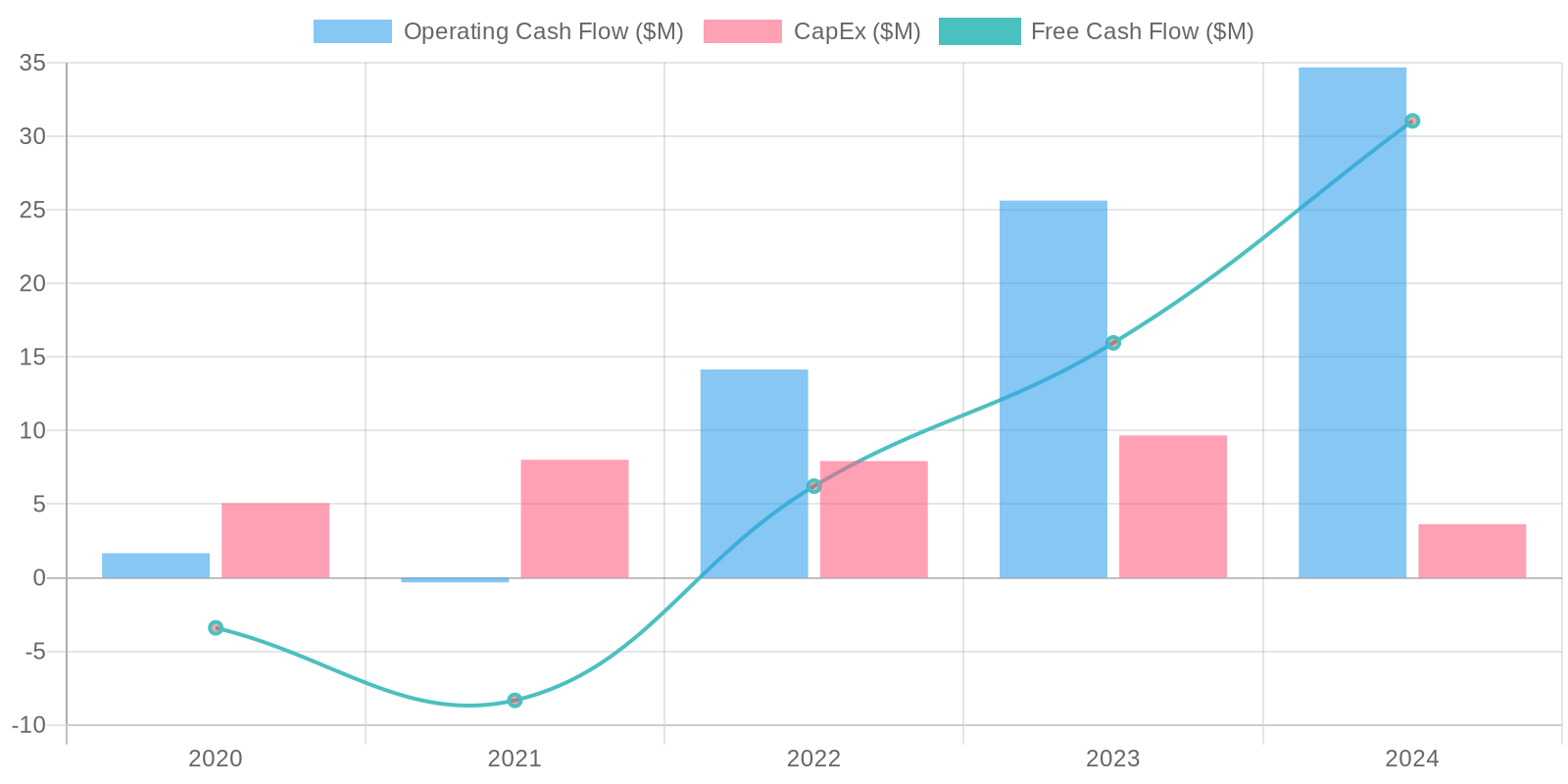

Calculating ROIC is difficult without invested capital details but analyzing available data suggests concerns. The company has demonstrated fluctuating profitability relative to its equity, with negative ROE in 2021 and 2022, meaning the company was losing money on shareholder investment. The ROE increased in 2023 as the company returned to profitability, but decreased again in 2024. The company's free cash flow (FCF) generation has improved significantly in recent years, with a substantial increase in 2024. This positive trend suggests better cash management and operational efficiency. Capital expenditures appear well-managed relative to operating cash flow, indicating prudent investment in property, plant, and equipment.

The company's free cash flow (FCF) generation has improved significantly in recent years, with a substantial increase in 2024. This positive trend suggests better cash management and operational efficiency. Capital expenditures appear well-managed relative to operating cash flow, indicating prudent investment in property, plant, and equipment.