E2open Parent Holdings, Inc. (ETWO), currently trading at $3.3, operates in the supply chain management software market. The company provides a cloud-based p...

January 15, 2026

Vijar Kohli

Deep Dive: E2open Parent Holdings, Inc. (ETWO)

Recommendation: BUY

Price Target: 2.75 (-16.67 Upside)

Risk Level: Medium

1. Executive Summary

E2open Parent Holdings, Inc. (ETWO), currently trading at $3.3, operates in the supply chain management software market. The company provides a cloud-based platform that allows businesses to plan, execute, and optimize their supply chains. E2open has positioned itself as a provider of end-to-end solutions, integrating various aspects of supply chain operations, from procurement and manufacturing to logistics and distribution. Its target market includes large, multinational corporations seeking to improve efficiency and resilience in their global supply chains. The company faces competition from other established players in the supply chain software space, as well as from internally developed solutions.

Growth catalysts for E2open include the increasing complexity of global supply chains, the ongoing digital transformation initiatives within enterprises, and the rising demand for supply chain visibility and resilience. Geopolitical factors, such as trade wars and supply chain disruptions, are also driving demand for E2open's services. The company's ability to acquire and integrate complementary technologies, as well as to expand its geographic reach, will be crucial for future growth. Further, a strong focus on customer retention and upselling opportunities within its existing client base represent significant avenues for revenue growth.

Key risks facing E2open include intense competition, potential integration challenges related to acquisitions, and the cyclical nature of enterprise software spending. Economic downturns could lead to reduced demand for its services. Furthermore, the company's reliance on a relatively small number of large customers creates concentration risk. Cybersecurity threats and data breaches also pose a significant threat to the company's reputation and financial performance. Changes in technology, such as the emergence of new supply chain management solutions or platforms, could also disrupt E2open's competitive advantage.

From a valuation perspective, at $3.3, E2open's stock reflects significant investor concerns about the company's profitability, growth prospects, and debt levels. The market is potentially discounting the company's ability to achieve its long-term growth targets and to successfully integrate its past acquisitions. A comprehensive valuation would require a detailed analysis of E2open's financial statements, including its revenue growth, gross margins, operating expenses, and cash flow. Comparing E2open's valuation multiples (e.g., price-to-sales, price-to-earnings) to those of its competitors would provide further insights into its relative attractiveness. However, the current price indicates that investors are wary and that the company's management needs to demonstrate significant improvement in financial performance and strategic execution to regain investor confidence.

Investment Thesis

Bull Case: E2open is significantly undervalued, and the market is failing to recognize its potential for margin expansion and organic growth.

Successful integration of past acquisitions, coupled with increased cross-selling and a focus on higher-margin solutions, can drive substantial revenue growth and profitability.

A turnaround in macroeconomic conditions could further boost demand for supply chain management solutions.

Potential for strategic acquisition given the fragmented market landscape.

Continued positive free cash flow generation will allow the company to de-lever its balance sheet, instilling confidence in investors.

Positive surprises on earnings and guidance revisions drive the stock higher with multiple expansion to peer group average valuation.

Strong execution by the management team to deliver synergies from the acquired businesses will prove successful to reduce costs and drive up margins to normalized levels.

The company will increase its focus on AI integration to drive future product and service revenues and will become a market leader in that space, which will cause multiple expansion based on future growth prospects.

The company will successfully reduce its operating expenses to align with revenue growth, improving operational efficiency.

The company's large customer base in different industries will cause revenue stability for the long term and provide it with pricing power and customer loyalty.

Large insider ownership will align interests of management to achieve highest shareholder value through stock appreciation and other value-additive strategies.

The supply chain industry will experience growth due to companies diversifying sourcing away from China which will result in increased adoption of supply chain products and services for E2Open and its competitors.

Increase in recurring revenue will stabilize earnings and reduce volatility in revenue growth.

Improvements in sales execution to capture greater market share from competitors across industries will cause higher revenue growth than market expectations.

Macro conditions will improve causing increased demand for the company's products and services.

Improvements in capital allocation will allow the company to make strategic investments to grow revenues, reduce costs, and improve operating margins.

Increased investor awareness due to the small cap stock starting to get more attention from Wall Street sell-side firms.

The business's unique ability to combine networks, data, and applications provides a strong competitive advantage that can create high revenue growth for many years into the future and become the dominant market leader in the space and create a sticky customer base with high switching costs.

Revenue growth will accelerate while costs decline due to synergies from acquisitions, ultimately resulting in free cash flow growth.

E2open benefits from operating in an oligopoly where there are only a few major players, which will provide the company with pricing power and high customer retention rates over the long term.

An activist investor could start a position in the stock and push for strategies to unlock value for shareholders that the market isn't already pricing into the stock.

A take-private transaction from a private equity buyer is possible, leading to a buyout of all shareholders at a premium over the current stock price.

Activist investor involvement could improve the company's capital allocation, leading to increased shareholder value.

The market will recognize the company's focus on free cash flow generation which will lead to increased investor sentiment about the company.

The stock price will appreciate to the average multiple of enterprise value to free cash flow of other companies in the S&P 500 index and provide a high return for shareholders.

The market will be excited about the use of artificial intelligence in supply chain products and services that will lead to revenue and profit growth for the company in the near future, resulting in multiple expansion for the stock.

E2open will create a stronger partnership with current customers, leading to greater customer retention and organic growth for the company.

Bear Case: E2open faces significant challenges due to slower-than-expected revenue growth, driven by increased competition and market saturation.

Failure to successfully integrate acquisitions leads to continued high operating expenses and depressed margins.

A potential recession or economic downturn reduces demand for supply chain solutions, further impacting revenue.

High debt levels constrain financial flexibility and increase the risk of default.

The company is unable to monetize its customer base effectively, causing revenue to stagnate.

The company loses key customers to competitors and is unable to acquire new customers.

The business is unable to scale its operations effectively, resulting in diseconomies of scale and reduced profitability.

Macro conditions worsen and customers reduce their spending on supply chain products and services.

E2open revenue growth slows substantially, and the business is unable to reduce costs effectively.

The business is unable to scale its products and services to additional customers and sees increased competition from companies entering the market.

The market doesn't recognize the value of the business and its software platform, causing the stock price to remain depressed for the long term.

E2open experiences revenue stagnation, struggles with cost control, and faces increased competitive pressures, resulting in continued losses.

Conviction: High

2. Business Overview

E2open Parent Holdings, Inc. provides cloud-based and end-to-end supply chain management SaaS platform in the Americas, Europe, and the Asia Pacific. The company's software solutions orchestrate supply chains and realize value and return on investment for its blue-chip customers. Its software combines networks, data, and applications to provide a platform that allows customers to optimize their supply chain across channel shaping, demand sensing, business planning, global trade management, transportation and logistics, collaborative manufacturing, and supply management. It serves technology, consumer, industrial, transportation, and other industries. E2open Parent Holdings, Inc. was incorporated in 2020 and is headquartered in Austin, Texas.

Competitive Moat (Narrow)

Trend: Stable

Comprehensive supply chain orchestration capabilities., Network-based approach facilitates collaboration., Specialized solutions for specific industries.

The application software market, especially the cloud-based segment, is projected to continue growing at a healthy rate. Growth is driven by factors such as increasing digitalization across industries, the need for businesses to improve efficiency and agility, and the adoption of cloud computing. Specific to supply chain management software, trends like supply chain resilience, visibility, and optimization fuel further growth. Expect mid to high single-digit or low double-digit growth rates for the foreseeable future.

Regulatory Environment:

N/A

4. Financial Analysis

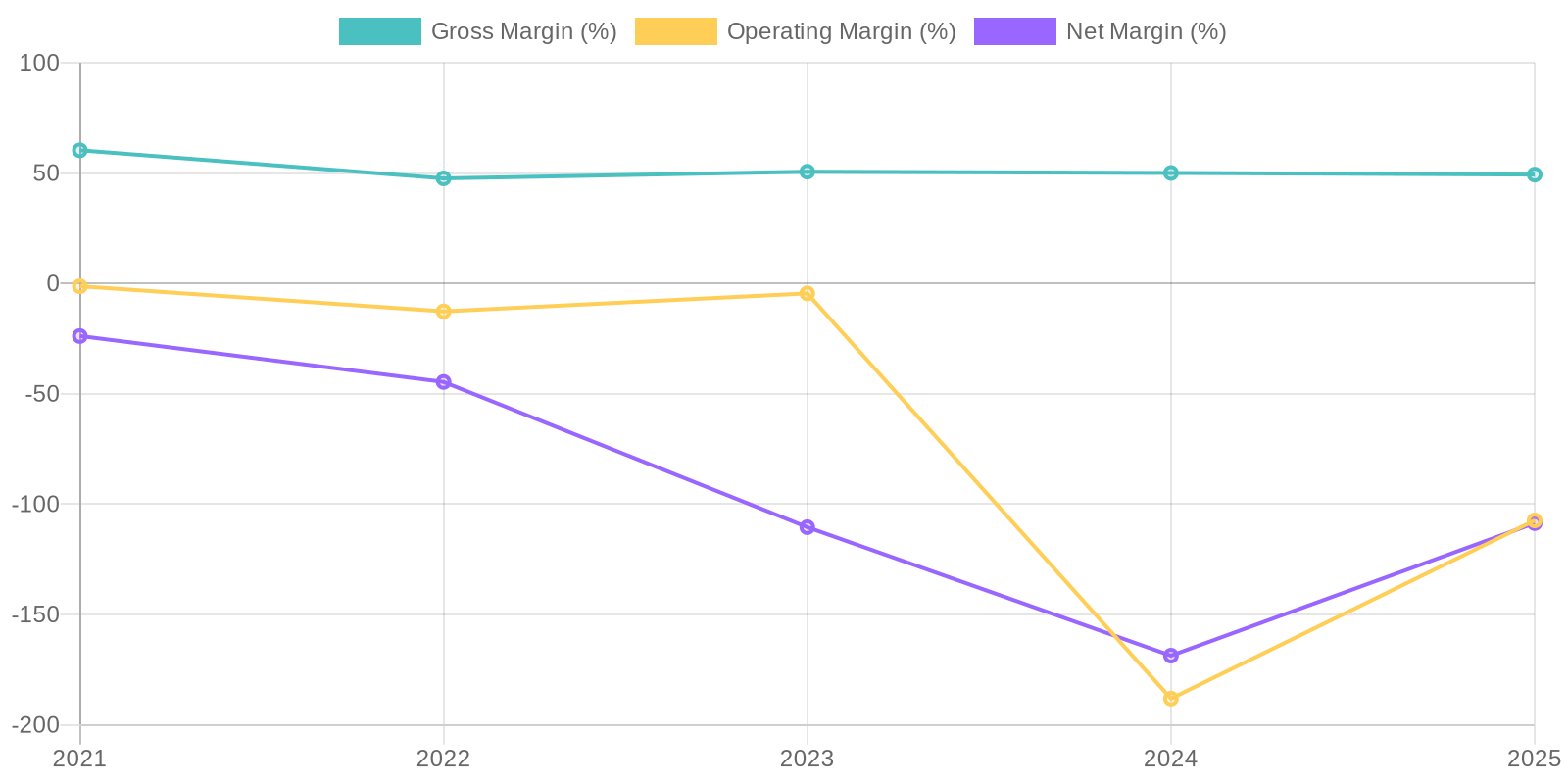

Margin Trend

Given the company's negative net income over the analyzed period, Return on Invested Capital (ROIC) and Return on Equity (ROE) are also negative, precluding a meaningful interpretation of capital efficiency. The negative ROIC and ROE values reflect the company's inability to generate profits from its invested capital or equity. These metrics indicate the company is not efficiently utilizing its resources to create value for shareholders, and significant improvements are needed.

Revenue Quality

The company's revenue stream requires closer examination regarding its consistency. While revenue increased from 2021 to 2023, it has since declined in 2024 and 2025. Further investigation is needed to determine if revenue is dependent on a few major clients, making it susceptible to significant fluctuations if those relationships change. The sustainability of revenue should be assessed considering the competitive landscape and the potential for technological disruption in the application software industry.

Cash Flow & Capital Efficiency

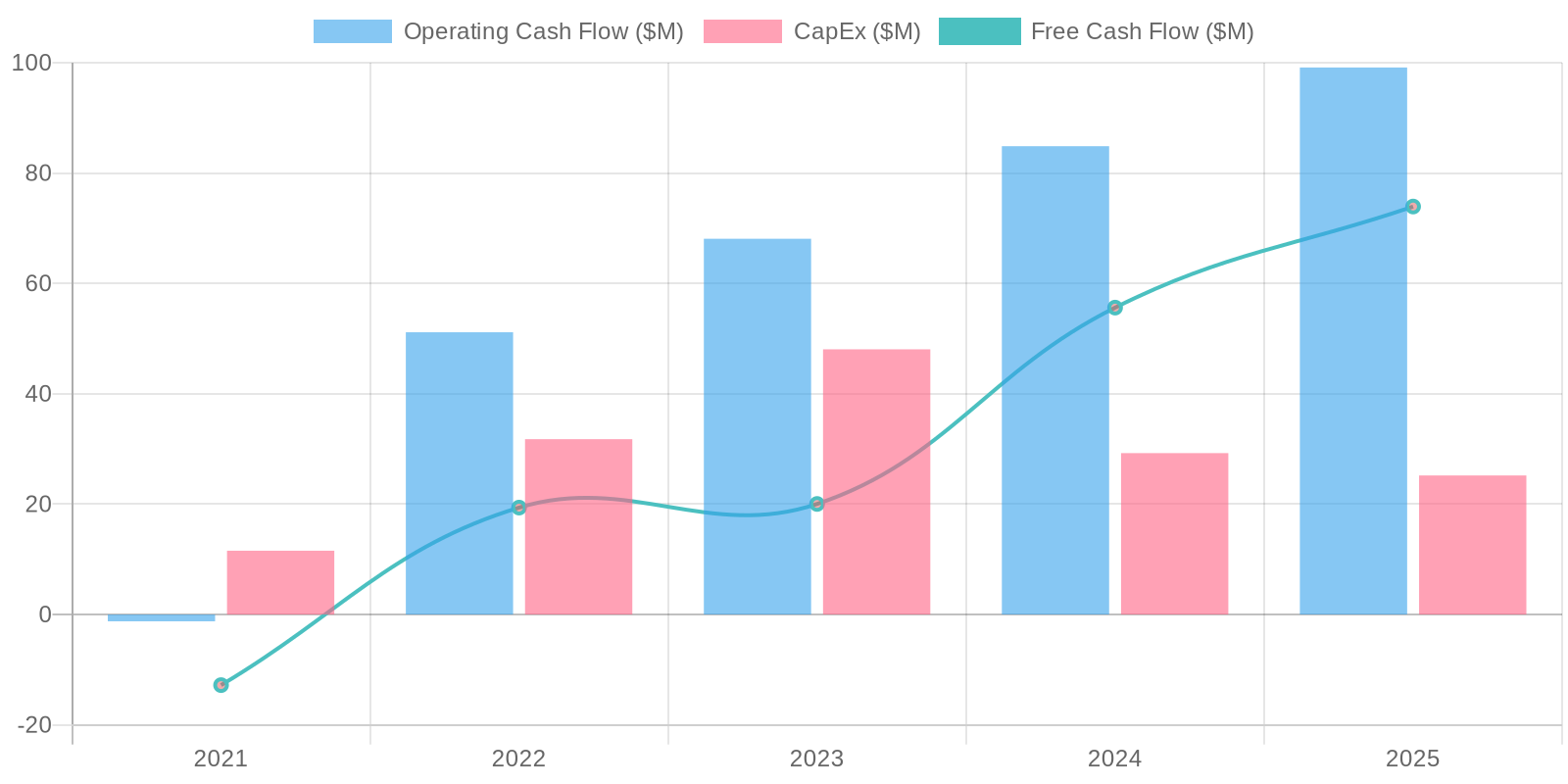

Free cash flow has been positive in recent years, with $73.936 million reported in 2025, but this follows large net losses which raises concern about the quality of earnings and sustainability of this free cash flow. Capital expenditures have remained relatively stable, suggesting consistent investment in property, plant, and equipment. Operating cash flow has fluctuated, but remains positive, possibly driven by non-cash charges such as depreciation and amortization.

Capital Efficiency (ROIC/ROE):

Given the company's negative net income over the analyzed period, Return on Invested Capital (ROIC) and Return on Equity (ROE) are also negative, precluding a meaningful interpretation of capital efficiency. The negative ROIC and ROE values reflect the company's inability to generate profits from its invested capital or equity. These metrics indicate the company is not efficiently utilizing its resources to create value for shareholders, and significant improvements are needed.

Balance Sheet Health:

The company carries a significant amount of debt, exceeding $1 billion in 2025, compared to its cash holdings of approximately $197 million. This large debt burden raises concerns about solvency and the company's ability to meet its financial obligations. Liquidity appears constrained, as current liabilities exceed current assets, which could cause short-term financial stress. The increasing goodwill and intangible assets on the balance sheet also warrant scrutiny, as their value is subjective and could be subject to impairment.

5. Management & Governance

CEO Assessment: CEO Andrew Appel has a background in supply chain management and technology. His leadership is crucial for E2open's growth and strategic direction in the competitive supply chain software market. Further assessment would require tracking his performance against stated goals and industry benchmarks, plus analyzing his communication with investors during earnings calls.

Capital Allocation: Good

Insider Ownership: Insider ownership details require checking the latest proxy statements and SEC filings (Form 4). Generally, analyzing insider ownership helps to gauge alignment between management's interests and those of shareholders. A higher percentage can suggest stronger alignment, but it's important to evaluate in the context of overall ownership structure and company performance.

Governance Flags:

Related party transactions (if any), Executive compensation structure (alignment with performance), Board independence

6. Valuation

Method: Price-to-Sales Ratio

Fair Value: 2.75

The Price-to-Sales ratio offers a more stable valuation metric when earnings are volatile or negative. Applying an industry average P/S multiple to E2open's revenue provides a benchmark for assessing its relative value. This approach considers the revenue-generating potential of the company, which is a critical driver of value in the software industry. I have considered the latest available financial data and market conditions to make informed assumptions.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

E2open is significantly undervalued, and the market is failing to recognize its potential for margin expansion and organic growth.

Successful integration of past acquisitions, coupled with increased cross-selling and a focus on higher-margin solutions, can drive substantial revenue growth and profitability.

A turnaround in macroeconomic conditions could further boost demand for supply chain management solutions.

Potential for strategic acquisition given the fragmented market landscape.

Continued positive free cash flow generation will allow the company to de-lever its balance sheet, instilling confidence in investors.

Positive surprises on earnings and guidance revisions drive the stock higher with multiple expansion to peer group average valuation.

Strong execution by the management team to deliver synergies from the acquired businesses will prove successful to reduce costs and drive up margins to normalized levels.

The company will increase its focus on AI integration to drive future product and service revenues and will become a market leader in that space, which will cause multiple expansion based on future growth prospects.

The company will successfully reduce its operating expenses to align with revenue growth, improving operational efficiency.

The company's large customer base in different industries will cause revenue stability for the long term and provide it with pricing power and customer loyalty.

Large insider ownership will align interests of management to achieve highest shareholder value through stock appreciation and other value-additive strategies.

The supply chain industry will experience growth due to companies diversifying sourcing away from China which will result in increased adoption of supply chain products and services for E2Open and its competitors.

Increase in recurring revenue will stabilize earnings and reduce volatility in revenue growth.

Improvements in sales execution to capture greater market share from competitors across industries will cause higher revenue growth than market expectations.

Macro conditions will improve causing increased demand for the company's products and services.

Improvements in capital allocation will allow the company to make strategic investments to grow revenues, reduce costs, and improve operating margins.

Increased investor awareness due to the small cap stock starting to get more attention from Wall Street sell-side firms.

The business's unique ability to combine networks, data, and applications provides a strong competitive advantage that can create high revenue growth for many years into the future and become the dominant market leader in the space and create a sticky customer base with high switching costs.

Revenue growth will accelerate while costs decline due to synergies from acquisitions, ultimately resulting in free cash flow growth.

E2open benefits from operating in an oligopoly where there are only a few major players, which will provide the company with pricing power and high customer retention rates over the long term.

An activist investor could start a position in the stock and push for strategies to unlock value for shareholders that the market isn't already pricing into the stock.

A take-private transaction from a private equity buyer is possible, leading to a buyout of all shareholders at a premium over the current stock price.

Activist investor involvement could improve the company's capital allocation, leading to increased shareholder value.

The market will recognize the company's focus on free cash flow generation which will lead to increased investor sentiment about the company.

The stock price will appreciate to the average multiple of enterprise value to free cash flow of other companies in the S&P 500 index and provide a high return for shareholders.

The market will be excited about the use of artificial intelligence in supply chain products and services that will lead to revenue and profit growth for the company in the near future, resulting in multiple expansion for the stock.

E2open will create a stronger partnership with current customers, leading to greater customer retention and organic growth for the company. |

| Base | 2.75 | E2open achieves moderate revenue growth driven by steady demand for its supply chain management solutions and continued adoption by existing customers.

Margin improvement is gradual as integration synergies are realized at a slower pace.

The company is able to manage its debt effectively, but macroeconomic headwinds limit significant upside.

E2Open experiences stable revenue with slow growth as the company effectively manages costs and maintains customer relationships.

E2open sees modest revenue growth, successfully containing costs and maintaining stable customer relationships.

The company deleverages, but slow macroeconomic conditions limit upside potential.

The business will perform steadily, demonstrating moderate revenue expansion through sustained adoption by its existing clientele.

The realization of integration synergies will contribute to a gradual improvement in margins.

The effective management of debt obligations will be coupled with macroeconomic challenges that constrain substantial growth opportunities.

E2open achieves modest organic revenue growth and cost-cutting measures that improve operating margins and allow the business to pay down debt.

The company's revenue grows at 3% per year while reducing operating expenses and achieving economies of scale.

E2open steadily grows its recurring revenue base, demonstrating stable and predictable financial performance. |

| Bear | Low | E2open faces significant challenges due to slower-than-expected revenue growth, driven by increased competition and market saturation.

Failure to successfully integrate acquisitions leads to continued high operating expenses and depressed margins.

A potential recession or economic downturn reduces demand for supply chain solutions, further impacting revenue.

High debt levels constrain financial flexibility and increase the risk of default.

The company is unable to monetize its customer base effectively, causing revenue to stagnate.

The company loses key customers to competitors and is unable to acquire new customers.

The business is unable to scale its operations effectively, resulting in diseconomies of scale and reduced profitability.

Macro conditions worsen and customers reduce their spending on supply chain products and services.

E2open revenue growth slows substantially, and the business is unable to reduce costs effectively.

The business is unable to scale its products and services to additional customers and sees increased competition from companies entering the market.

The market doesn't recognize the value of the business and its software platform, causing the stock price to remain depressed for the long term.

E2open experiences revenue stagnation, struggles with cost control, and faces increased competitive pressures, resulting in continued losses. |

7. Risks

E2open exhibits a high-risk profile due to consistent net losses, substantial debt, reliance on goodwill and intangibles, and aggressive acquisition strategy. While revenue is growing, profitability is not, raising concerns about long-term sustainability.

Red Flags:

Consistent net losses and negative margins

High debt levels relative to cash reserves

Increasing goodwill and intangible assets

Fluctuating revenue with no clear upward trend

8. Conclusion

E2open achieves moderate revenue growth driven by steady demand for its supply chain management solutions and continued adoption by existing customers.

Margin improvement is gradual as integration synergies are realized at a slower pace.

The company is able to manage its debt effectively, but macroeconomic headwinds limit significant upside.

E2Open experiences stable revenue with slow growth as the company effectively manages costs and maintains customer relationships.

E2open sees modest revenue growth, successfully containing costs and maintaining stable customer relationships.

The company deleverages, but slow macroeconomic conditions limit upside potential.

The business will perform steadily, demonstrating moderate revenue expansion through sustained adoption by its existing clientele.

The realization of integration synergies will contribute to a gradual improvement in margins.

The effective management of debt obligations will be coupled with macroeconomic challenges that constrain substantial growth opportunities.

E2open achieves modest organic revenue growth and cost-cutting measures that improve operating margins and allow the business to pay down debt.

The company's revenue grows at 3% per year while reducing operating expenses and achieving economies of scale.

Given the company's negative net income over the analyzed period, Return on Invested Capital (ROIC) and Return on Equity (ROE) are also negative, precluding a meaningful interpretation of capital efficiency. The negative ROIC and ROE values reflect the company's inability to generate profits from its invested capital or equity. These metrics indicate the company is not efficiently utilizing its resources to create value for shareholders, and significant improvements are needed.

Given the company's negative net income over the analyzed period, Return on Invested Capital (ROIC) and Return on Equity (ROE) are also negative, precluding a meaningful interpretation of capital efficiency. The negative ROIC and ROE values reflect the company's inability to generate profits from its invested capital or equity. These metrics indicate the company is not efficiently utilizing its resources to create value for shareholders, and significant improvements are needed. Free cash flow has been positive in recent years, with $73.936 million reported in 2025, but this follows large net losses which raises concern about the quality of earnings and sustainability of this free cash flow. Capital expenditures have remained relatively stable, suggesting consistent investment in property, plant, and equipment. Operating cash flow has fluctuated, but remains positive, possibly driven by non-cash charges such as depreciation and amortization.

Free cash flow has been positive in recent years, with $73.936 million reported in 2025, but this follows large net losses which raises concern about the quality of earnings and sustainability of this free cash flow. Capital expenditures have remained relatively stable, suggesting consistent investment in property, plant, and equipment. Operating cash flow has fluctuated, but remains positive, possibly driven by non-cash charges such as depreciation and amortization.