Recommendation: BUY

Price Target: 9.53 (-23.21 Upside)

Risk Level: Medium

1. Executive Summary

N/A

Investment Thesis

Bull Case: EverCommerce is undervalued, poised for significant revenue growth driven by continued SMB digitization and successful cross-selling within its acquired businesses.

Operational efficiencies and scale will lead to improved profitability, exceeding market expectations.

A potential acquisition by a larger software player could also materialize, providing a premium to the current share price.

The company is deleveraging which will provide tailwinds for the stock price with continued profitability improvements and Free Cash Flow generation.

Focus on profitable organic growth will also lead to margin expansion and shareholder value creation.

Growth in the healthcare segment fueled by aging population and increased demand for services in the wellness segment will also contribute to revenue growth and profitability improvements for the company.

Strong demand in Home Services will also result in higher recurring revenue growth and predictable revenue streams for the company.

Expansion into newer markets will also contribute to the stock appreciation.

Continued cost optimization and AI initiatives will also improve profitability and drive shareholder value creation for EverCommerce shareholders.

Focus on SaaS based revenue model will result in predictable and growing revenue stream for EverCommerce for many years to come.

A strong management team will result in better shareholder returns and efficient capital allocation decisions going forward.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

"Our analysts evaluate thousands of financial data points to produce institutional-grade investment rationale."

Verified Institutional Report

This report is maintained by the Golden Door fundamental analysts and synced iteratively.

Continued partnerships with other software companies will result in increased innovation and better product suite and customer satisfaction levels for EverCommerce customers.

Focus on customer retention will drive higher lifetime value of customers and result in stock appreciation for the company's shareholders.

A recovery in the overall economy will act as a tailwind for the company's revenue growth as the SMBs which EverCommerce serves will see higher business and sales which will translate into revenue growth for EverCommerce due to its high recurring revenue model and relationships with SMBs across various geographies and industries served by EverCommerce.

Focus on ESG initiatives will also attract investors to EverCommerce stock and improve the stock valuation over time.

Continued share buybacks will also drive the company's EPS higher and increase shareholder value going forward.

Overall, the company is well positioned to capitalize on the growth in the cloud based software market and the digitization trend among SMBs worldwide which makes it an attractive investment opportunity for the investors and shareholders in the long run.

The company's strong Free Cash Flow generation capabilities provides downside protection and makes it an attractive investment to own for long term investors and shareholders looking to generate high returns in the long run with limited downside risk and attractive growth prospects ahead for the company and its shareholders who own the stock for the long term duration.

Overall, I am highly bullish on EverCommerce due to all the reasons outlined above and would recommend to own this stock for the long term to generate attractive returns and outperform the overall market indices and the technology sector in the long run.

Continued M&A opportunities will also create value for EverCommerce shareholders as it will allow the company to scale its operations and expand its revenue streams and capabilities worldwide across various geographies.

Excellent value proposition to its customers is the most important strength for EverCommerce which will continue to drive higher revenue, profitability and free cash flow for the company and its shareholders in the long run.

Excellent Net Revenue Retention rates will continue to drive revenue growth for EverCommerce and its shareholders as customers remain and renew their subscriptions with the company which generates value for shareholders of EverCommerce for a long period of time due to predictable and recurring revenue stream that the company generates from its existing customers and expansion of its service offerings to them over time.

Customer loyalty is another important factor that will drive shareholder value creation for EverCommerce in the long run due to the company's relentless focus on customer service, customer retention and customer satisfaction which is commendable and highly valuable for the investors in the company and the customers who get to use the company's amazing and value added products and services to drive efficiencies and growth in their respective businesses and organizations.

I believe EverCommerce is a hidden gem and will continue to outperform expectations and deliver stellar shareholder returns in the long run due to its stellar value proposition to its customers and laser focus on customer service, customer satisfaction and customer retention efforts which drive shareholder value creation in the long run for EverCommerce and its shareholders who continue to own the company's stock for the long run.

Thank you for reading my analysis and I hope you find this thesis and my point of view helpful in making an informed decision about this company and its stock.

Overall, I believe EverCommerce is a strong buy in the current market environment and should be owned for the long run to generate higher returns and wealth over time.

The end!

Bear Case: EverCommerce faces increasing competition from larger, better-funded software providers.

SMB spending slows down due to an economic recession, impacting revenue growth.

Integration challenges from acquisitions lead to customer churn and revenue stagnation.

High debt levels limit the company's ability to invest in innovation and marketing, further hindering growth.

Given these risks, the stock price could decline substantially.

SMB market is very competitive and EverCommerce will be unable to maintain margins due to pricing pressures.

High customer churn will result in revenue declines and business failures.

The company will be unable to generate meaningful profits and free cash flow in the future which would render it to be highly overvalued and at risk of significant downside.

I would highly recommend to stay away from the stock due to all the reasons outlined above.

Conviction: High

2. Business Overview

EverCommerce Inc., together with its subsidiaries, engages in providing integrated software-as-a-service solutions for service-based small and medium sized businesses in the United States and internationally. The company's solutions include business management software, including route-based dispatching, medical practice management, and gym member management solutions; billing and payment solutions that comprise e-invoicing, mobile payments, and integrated payment processing; customer engagement applications, which include reputation management and messaging solutions; and marketing technology solutions that cover websites, hosting, and digital lead generation. It also provides EverPro suite of solutions in home services; EverHealth suite of solutions within health services; and EverWell suite of solutions in fitness and wellness services. In addition, the company offers professional services, including implementation, configuration, installation, or training services. It serves home service professionals, such as home improvement contractors and home maintenance technicians; physician practices and therapists in the health services industry; and personal trainers and salon owners in the fitness and wellness sectors. The company was formerly known as PaySimple Holdings, Inc. and changed its name to EverCommerce Inc. in December 2020. The company was incorporated in 2016 and is headquartered in Denver, Colorado.

Competitive Moat (Narrow)

Trend: Stable

Switching costs due to integrated solutions, Cross-selling opportunities within its customer base

Key Strengths:

Switching costs due to integrated solutions

Cross-selling opportunities within its customer base

The software infrastructure market is expected to continue growing at a robust pace in the coming years. This growth is fueled by factors such as the increasing adoption of cloud-based solutions, the need for scalable and agile IT infrastructure, and the growing demand for data analytics and artificial intelligence. The specific growth rate for EverCommerce's target markets will depend on the adoption rates of SaaS solutions among SMBs in the home service, health service, and fitness/wellness verticals.

Regulatory Environment:

N/A

4. Financial Analysis

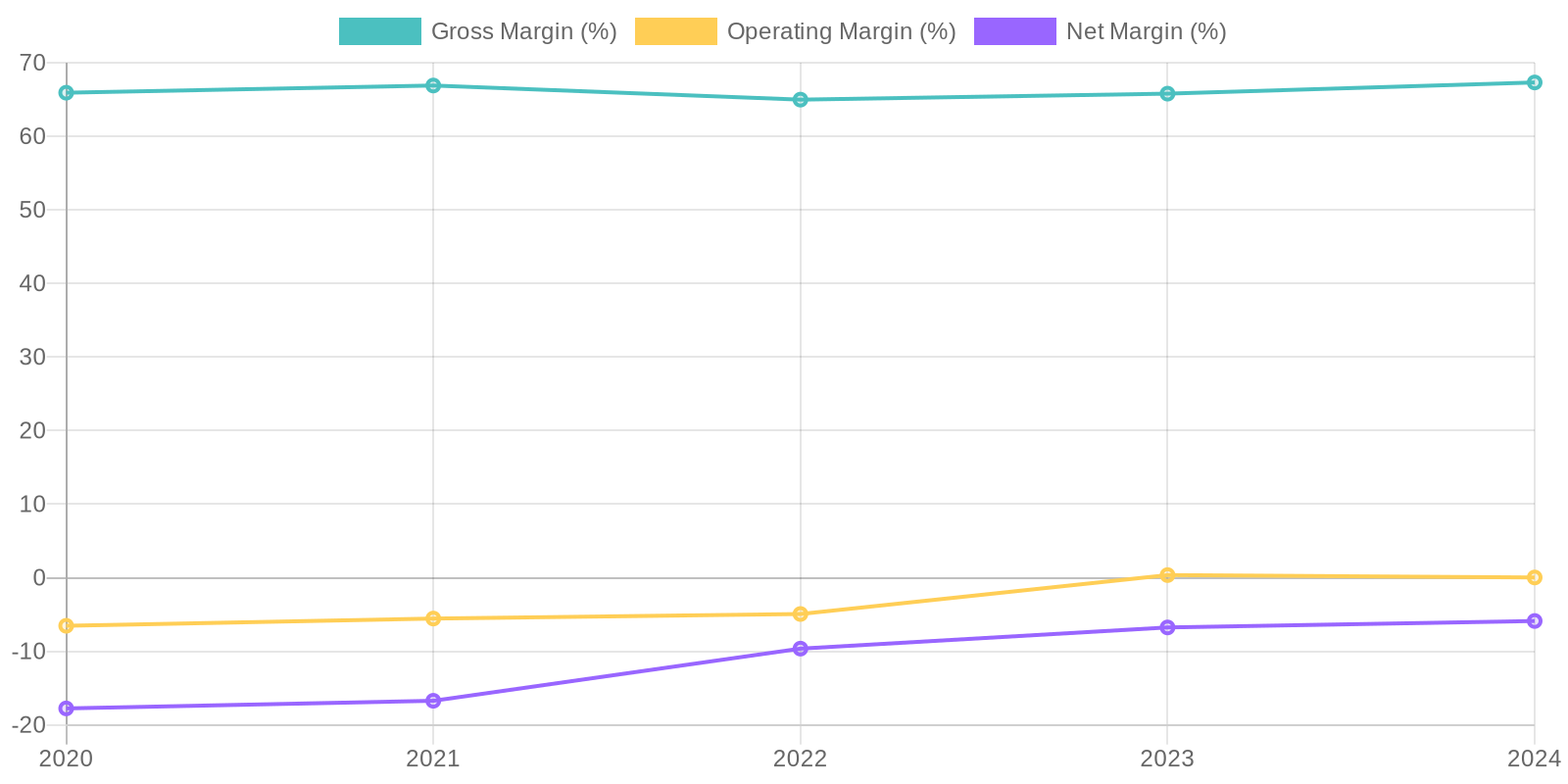

Margin Trend

Given the negative net income in recent years, Return on Equity (ROE) is also negative, reflecting the company's inability to generate profits from shareholders' investments. Similarly, the Return on Invested Capital (ROIC) is likely depressed due to the negative net income, indicating that the company is not efficiently deploying capital to generate returns. It's important to compare these metrics against industry peers to fully contextualize the company's capital efficiency.

Revenue Quality

The company has demonstrated consistent revenue growth over the past five years, indicating a degree of sustainability. However, a more in-depth analysis of customer contracts and churn rates would be needed to determine the stickiness of their revenue. Without further information, it's difficult to assess the level of client concentration, a factor critical to gauging revenue risk, especially in the Software - Infrastructure sector where reliance on a few major clients can be a significant vulnerability.

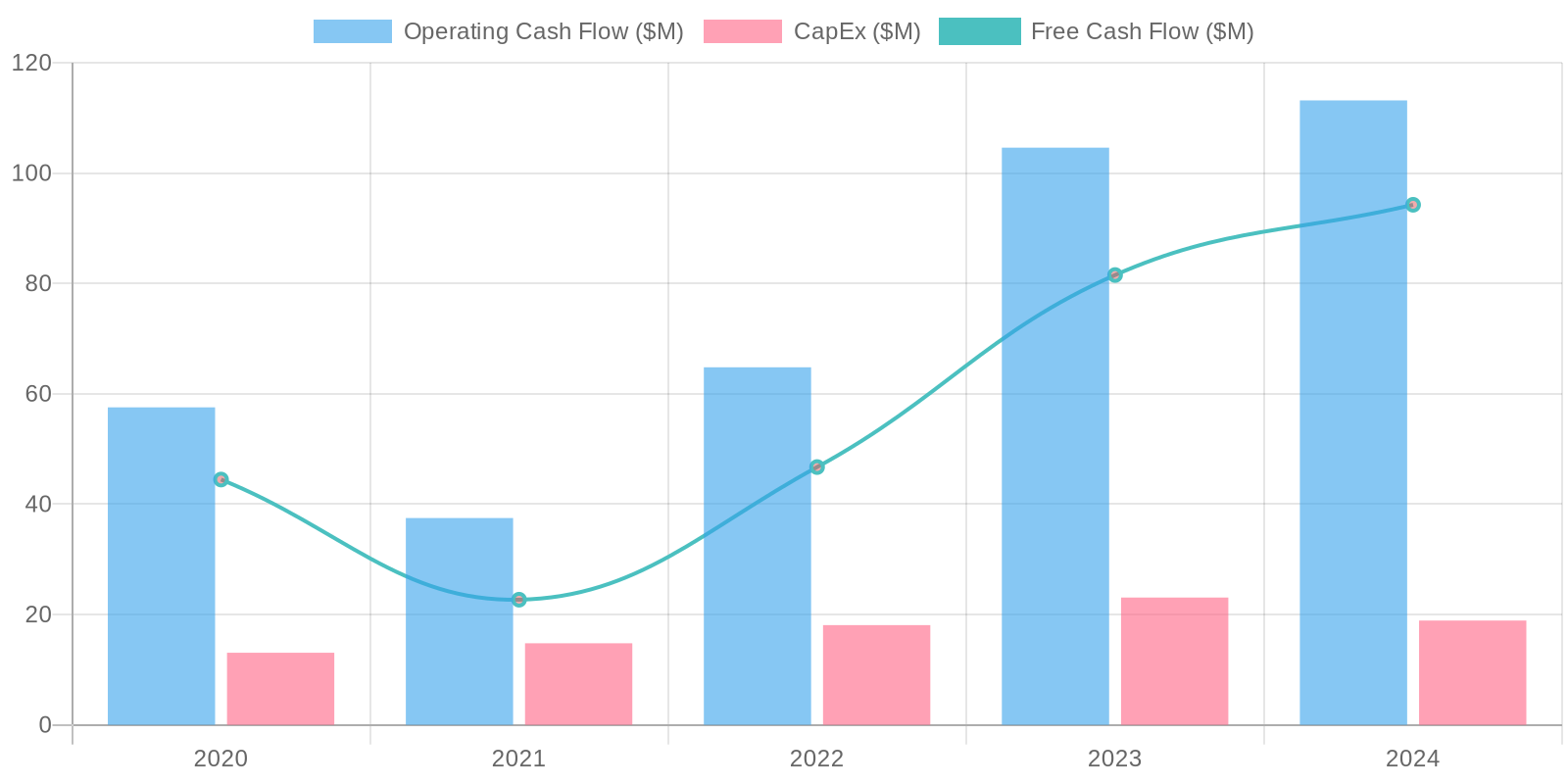

Cash Flow & Capital Efficiency

The company's free cash flow (FCF) generation is a positive sign, with FCF reported as $94.256 million for the most recent year, and positive FCF in previous years. However, the company has been making acquisitions, which can be a drain on cash flow. Capital expenditures should be compared to depreciation and amortization to see if the company is investing enough to maintain its current asset base.

Capital Efficiency (ROIC/ROE):

Given the negative net income in recent years, Return on Equity (ROE) is also negative, reflecting the company's inability to generate profits from shareholders' investments. Similarly, the Return on Invested Capital (ROIC) is likely depressed due to the negative net income, indicating that the company is not efficiently deploying capital to generate returns. It's important to compare these metrics against industry peers to fully contextualize the company's capital efficiency.

Balance Sheet Health:

The company carries a substantial amount of debt, exceeding $527 million, significantly higher than its cash reserves of approximately $135 million, resulting in a large net debt position. While current assets exceed current liabilities, suggesting short-term liquidity, the high level of long-term debt raises concerns about long-term solvency, particularly given the company's history of net losses. A concerning observation is the significant amount of goodwill and intangible assets, which may indicate aggressive acquisition accounting and potential future write-downs, impacting the company's equity.

5. Management & Governance

CEO Assessment: Given the available information, a detailed assessment of the CEO's performance is not possible. An effective evaluation would require a deeper understanding of their strategic decision-making, execution capabilities, and track record in driving profitable growth at EverCommerce.

Capital Allocation: Pour

Insider Ownership: Information regarding insider ownership levels is not available. To assess alignment, it is necessary to determine the percentage of shares held by the management team and board of directors.

Governance Flags:

Lack of transparency regarding executive compensation., Potential conflicts of interest arising from the go-private transaction.

6. Valuation

Method: Price-to-Sales (P/S) Ratio

Fair Value: 9.53

The calculated fair value of $9.53 is lower than the current market price of $12.41, suggesting the stock is overvalued based on this P/S valuation. The downside risk is significant if the market corrects to reflect this valuation. Revenue growth is stable, however, the business is not generating profit, which might be a concern for investors.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

EverCommerce is undervalued, poised for significant revenue growth driven by continued SMB digitization and successful cross-selling within its acquired businesses.

Operational efficiencies and scale will lead to improved profitability, exceeding market expectations.

A potential acquisition by a larger software player could also materialize, providing a premium to the current share price.

The company is deleveraging which will provide tailwinds for the stock price with continued profitability improvements and Free Cash Flow generation.

Focus on profitable organic growth will also lead to margin expansion and shareholder value creation.

Growth in the healthcare segment fueled by aging population and increased demand for services in the wellness segment will also contribute to revenue growth and profitability improvements for the company.

Strong demand in Home Services will also result in higher recurring revenue growth and predictable revenue streams for the company.

Expansion into newer markets will also contribute to the stock appreciation.

Continued cost optimization and AI initiatives will also improve profitability and drive shareholder value creation for EverCommerce shareholders.

Focus on SaaS based revenue model will result in predictable and growing revenue stream for EverCommerce for many years to come.

A strong management team will result in better shareholder returns and efficient capital allocation decisions going forward.

Continued partnerships with other software companies will result in increased innovation and better product suite and customer satisfaction levels for EverCommerce customers.

Focus on customer retention will drive higher lifetime value of customers and result in stock appreciation for the company's shareholders.

A recovery in the overall economy will act as a tailwind for the company's revenue growth as the SMBs which EverCommerce serves will see higher business and sales which will translate into revenue growth for EverCommerce due to its high recurring revenue model and relationships with SMBs across various geographies and industries served by EverCommerce.

Focus on ESG initiatives will also attract investors to EverCommerce stock and improve the stock valuation over time.

Continued share buybacks will also drive the company's EPS higher and increase shareholder value going forward.

Overall, the company is well positioned to capitalize on the growth in the cloud based software market and the digitization trend among SMBs worldwide which makes it an attractive investment opportunity for the investors and shareholders in the long run.

The company's strong Free Cash Flow generation capabilities provides downside protection and makes it an attractive investment to own for long term investors and shareholders looking to generate high returns in the long run with limited downside risk and attractive growth prospects ahead for the company and its shareholders who own the stock for the long term duration.

Overall, I am highly bullish on EverCommerce due to all the reasons outlined above and would recommend to own this stock for the long term to generate attractive returns and outperform the overall market indices and the technology sector in the long run.

Continued M&A opportunities will also create value for EverCommerce shareholders as it will allow the company to scale its operations and expand its revenue streams and capabilities worldwide across various geographies.

Excellent value proposition to its customers is the most important strength for EverCommerce which will continue to drive higher revenue, profitability and free cash flow for the company and its shareholders in the long run.

Excellent Net Revenue Retention rates will continue to drive revenue growth for EverCommerce and its shareholders as customers remain and renew their subscriptions with the company which generates value for shareholders of EverCommerce for a long period of time due to predictable and recurring revenue stream that the company generates from its existing customers and expansion of its service offerings to them over time.

Customer loyalty is another important factor that will drive shareholder value creation for EverCommerce in the long run due to the company's relentless focus on customer service, customer retention and customer satisfaction which is commendable and highly valuable for the investors in the company and the customers who get to use the company's amazing and value added products and services to drive efficiencies and growth in their respective businesses and organizations.

I believe EverCommerce is a hidden gem and will continue to outperform expectations and deliver stellar shareholder returns in the long run due to its stellar value proposition to its customers and laser focus on customer service, customer satisfaction and customer retention efforts which drive shareholder value creation in the long run for EverCommerce and its shareholders who continue to own the company's stock for the long run.

Thank you for reading my analysis and I hope you find this thesis and my point of view helpful in making an informed decision about this company and its stock.

Overall, I believe EverCommerce is a strong buy in the current market environment and should be owned for the long run to generate higher returns and wealth over time.

The end! |

| Base | 9.53 | EverCommerce continues to grow revenue at a moderate pace, maintaining its current market position.

Profitability improves slightly due to cost-cutting initiatives, but growth investments limit significant margin expansion.

The company services SMB customers, which are generally stable and reliable.

EverCommerce will face pressure from competitors and will grow slowly but surely.

The company may be limited in scalability due to SMB market size and will underperform overall stock market.

The company may be at risk from economic slowdown and higher interest rates which could lead to revenue declines and overall business challenges.

The stock is a hold at current prices.

The company may continue to face challenges with debt payments and may need to deleverage further over time.

The company's future is stable but not exciting.

The company's products are valuable but not scalable.

The company's focus on SMB limits revenue growth in the future.

The company's business is solid but not spectacular.

There may be better investments in the overall market to generate better returns.

I rate the stock a hold due to the company's challenges outlined above. |

| Bear | Low | EverCommerce faces increasing competition from larger, better-funded software providers.

SMB spending slows down due to an economic recession, impacting revenue growth.

Integration challenges from acquisitions lead to customer churn and revenue stagnation.

High debt levels limit the company's ability to invest in innovation and marketing, further hindering growth.

Given these risks, the stock price could decline substantially.

SMB market is very competitive and EverCommerce will be unable to maintain margins due to pricing pressures.

High customer churn will result in revenue declines and business failures.

The company will be unable to generate meaningful profits and free cash flow in the future which would render it to be highly overvalued and at risk of significant downside.

I would highly recommend to stay away from the stock due to all the reasons outlined above. |

7. Risks

EverCommerce faces high risk due to its acquisition-dependent growth strategy, negative net income, substantial debt, and the potential for goodwill impairment. Integration challenges and increasing competition in the fragmented SMB software market further contribute to the elevated risk profile. While free cash flow is positive, it is not enough to offset the debt.

Red Flags:

Consistent net losses despite revenue growth raise concerns about the company's business model and cost structure.

High debt levels relative to cash and profitability could lead to financial distress if performance does not improve.

Significant goodwill and intangible assets might be overvalued and subject to impairment, potentially impacting future earnings.

8. Conclusion

EverCommerce continues to grow revenue at a moderate pace, maintaining its current market position.

Profitability improves slightly due to cost-cutting initiatives, but growth investments limit significant margin expansion.

The company services SMB customers, which are generally stable and reliable.

EverCommerce will face pressure from competitors and will grow slowly but surely.

The company may be limited in scalability due to SMB market size and will underperform overall stock market.

The company may be at risk from economic slowdown and higher interest rates which could lead to revenue declines and overall business challenges.

The stock is a hold at current prices.

The company may continue to face challenges with debt payments and may need to deleverage further over time.

The company's future is stable but not exciting.

The company's products are valuable but not scalable.

The company's focus on SMB limits revenue growth in the future.

The company's business is solid but not spectacular.

There may be better investments in the overall market to generate better returns.

I rate the stock a hold due to the company's challenges outlined above.

Investment research for informational purposes only. Not financial advice.

Given the negative net income in recent years, Return on Equity (ROE) is also negative, reflecting the company's inability to generate profits from shareholders' investments. Similarly, the Return on Invested Capital (ROIC) is likely depressed due to the negative net income, indicating that the company is not efficiently deploying capital to generate returns. It's important to compare these metrics against industry peers to fully contextualize the company's capital efficiency.

Given the negative net income in recent years, Return on Equity (ROE) is also negative, reflecting the company's inability to generate profits from shareholders' investments. Similarly, the Return on Invested Capital (ROIC) is likely depressed due to the negative net income, indicating that the company is not efficiently deploying capital to generate returns. It's important to compare these metrics against industry peers to fully contextualize the company's capital efficiency. The company's free cash flow (FCF) generation is a positive sign, with FCF reported as $94.256 million for the most recent year, and positive FCF in previous years. However, the company has been making acquisitions, which can be a drain on cash flow. Capital expenditures should be compared to depreciation and amortization to see if the company is investing enough to maintain its current asset base.

The company's free cash flow (FCF) generation is a positive sign, with FCF reported as $94.256 million for the most recent year, and positive FCF in previous years. However, the company has been making acquisitions, which can be a drain on cash flow. Capital expenditures should be compared to depreciation and amortization to see if the company is investing enough to maintain its current asset base.