Recommendation: BUY

Price Target: 25.3 (-0.2 Upside)

Risk Level: Medium

1. Executive Summary

N/A

Investment Thesis

Bull Case: Figma is poised to become the dominant design platform for the future.

Its collaborative, cloud-based approach offers significant advantages over traditional design tools.

As the company continues to innovate and expand its product offerings, it will attract more users and generate significant revenue growth.

With improvements in operating leverage, Figma will achieve profitability and deliver substantial returns to investors.

Bear Case: Figma's growth may stall due to increased competition and a failure to monetize new product offerings.

The company may struggle to attract and retain top talent, hindering innovation.

Security breaches or data leaks could damage Figma's reputation and lead to user attrition.

If Figma is unable to achieve profitability, its stock price will decline significantly.

Conviction: High

2. Business Overview

Figma, Inc. develops a browser-based tool for designing user interfaces that helps design and development teams build various products. The company offers Figma Design, a collaborative design tool for teams that explore ideas and gather feedback, build realistic prototypes, and streamline product development with design systems; Dev Mode to inspect designs and translate them into code without changing the design file; FigJam to define ideas, align on decisions, and move work forwardall in one place; and Figma Slides, a presentation tool built for designers and their teams. It also provides Figma Draw to create expressive designs with illustration tools; Figma Buzz that publishes brand templates to create social media assets, display ads, one-pagers, and others; Figma Sites to design, prototype, and publish; and Figma Make, an AI tool to design and prompt way to a functional prototype. The company was incorporated in 2012 and is headquartered in San Francisco, California.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

The market for application software, particularly in the UI/UX design space, is projected to continue growing at a robust rate. Factors driving this growth include the increasing importance of user-centric design, the adoption of digital transformation initiatives, and the rise of remote and distributed teams that require collaborative tools like Figma. Emerging technologies such as AI (as evidenced by Figma Make) will likely contribute to the expansion of the market.

Regulatory Environment:

N/A

4. Financial Analysis

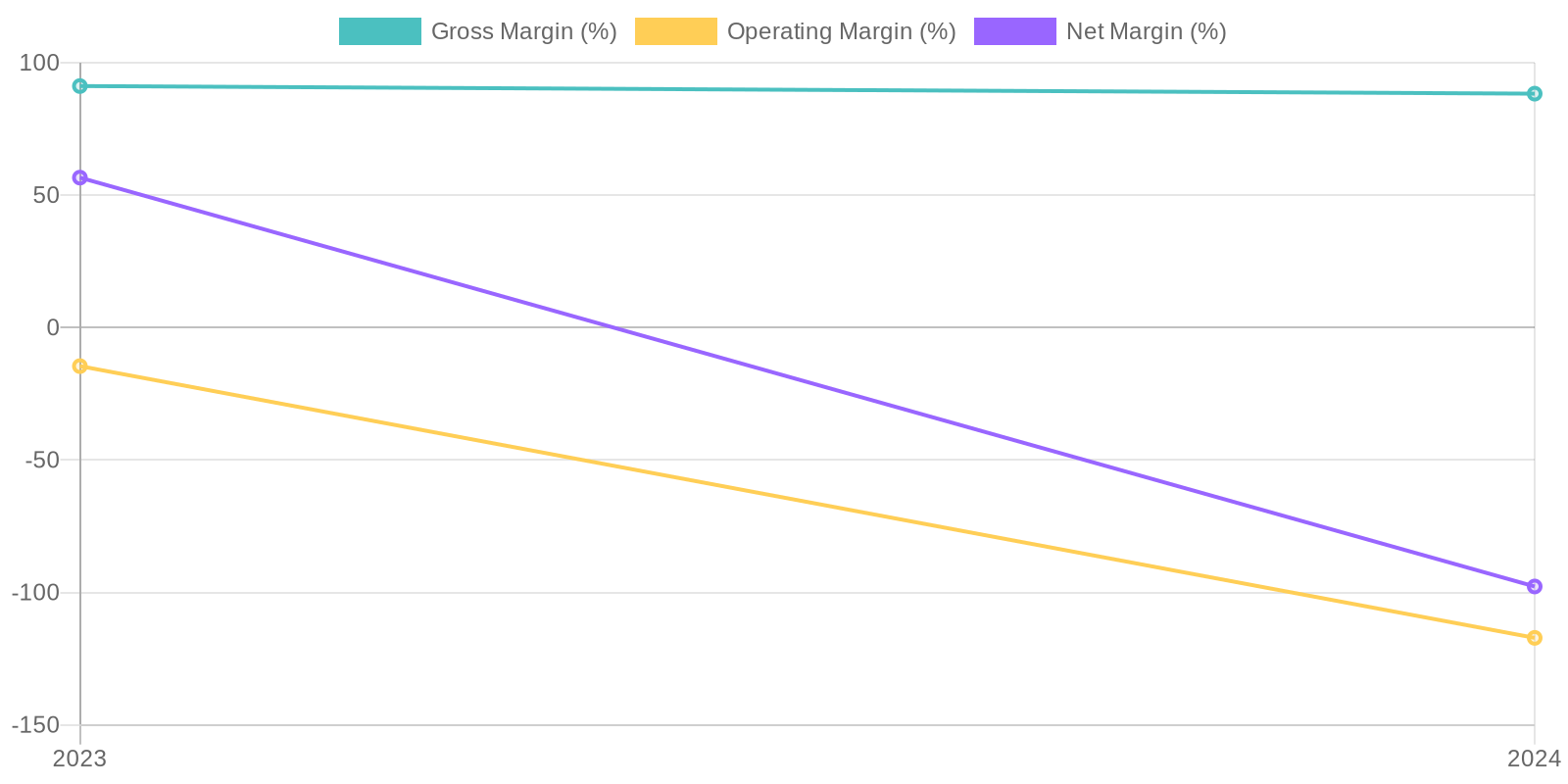

Margin Trend

Given the net loss of $732.12 million in 2024, Return on Invested Capital (ROIC) and Return on Equity (ROE) are negative, indicating inefficient capital allocation and poor returns for shareholders. It is crucial to examine the reasons behind the significant expenses increase to understand whether they are investments for future growth or signs of operational inefficiency. A positive ROE and ROIC were achieved in 2023 due to positive net income, but this trend has reversed.

Revenue Quality

The company experienced a significant increase in revenue from 2023 to 2024, growing from $504.87 million to $749.01 million. However, given the industry and the limited historical data, it's difficult to determine the recurring nature and sustainability of this revenue without further information on contract terms and customer retention rates. Further investigation is needed to ascertain whether this growth is sustainable or a result of one-time events.

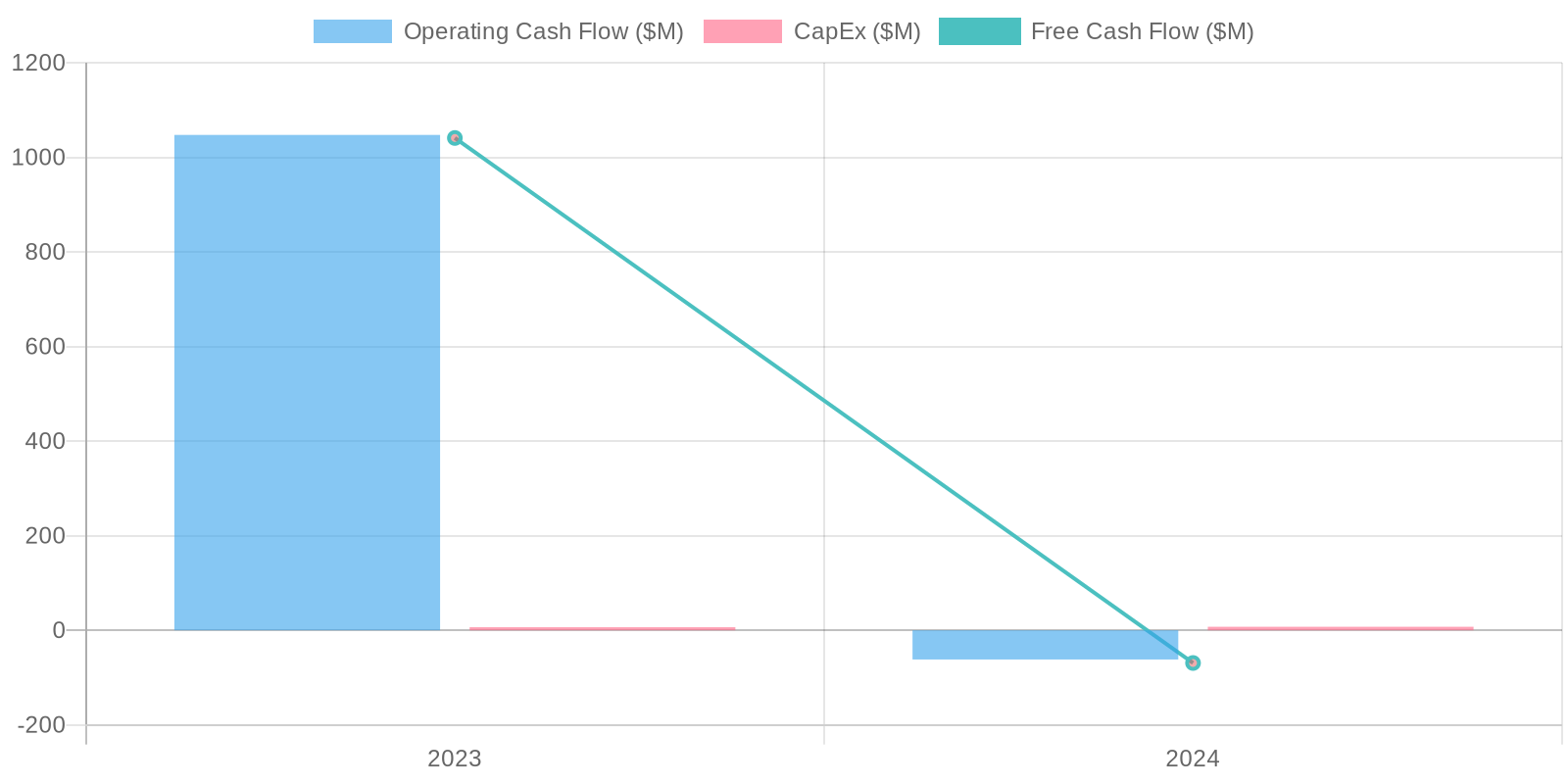

Cash Flow & Capital Efficiency

The company's free cash flow (FCF) is negative $69.14 million in 2024, a significant drop from the positive $1,040.88 million in 2023. This negative FCF is concerning, suggesting the company is not generating enough cash from operations to cover its capital expenditures. The company's operating cash flow went from positive $1,047.33 million in 2023 to negative $61.72 million in 2024, further suggesting a declining operational efficiency.

Capital Efficiency (ROIC/ROE):

Given the net loss of $732.12 million in 2024, Return on Invested Capital (ROIC) and Return on Equity (ROE) are negative, indicating inefficient capital allocation and poor returns for shareholders. It is crucial to examine the reasons behind the significant expenses increase to understand whether they are investments for future growth or signs of operational inefficiency. A positive ROE and ROIC were achieved in 2023 due to positive net income, but this trend has reversed.

Balance Sheet Health:

The company's cash position decreased significantly from $1,274.11 million in 2023 to $490.59 million in 2024. While the company holds a considerable amount of cash and short-term investments ($1,457.84 million), the negative free cash flow and net loss raise concerns about its long-term liquidity. Total debt remained relatively low at $28.77 million in 2024, indicating that the company's financial struggles are not primarily due to high leverage, but are stemming from a decline in earnings.

5. Management & Governance

CEO Assessment: Dylan Field is the CEO and co-founder of Figma. Assessments often highlight his vision for collaborative design and his ability to build a strong company culture. While a definitive 'assessment' requires deep insight, his leadership has guided Figma's rapid growth and user adoption.

Capital Allocation: Good

Insider Ownership: As a private company until recently, insider ownership at Figma was likely significant, concentrated among founders, early employees, and venture capital investors. Specific details are not publicly available. The Adobe acquisition would have significantly altered ownership for many, converting equity into Adobe stock or cash.

Governance Flags:

No major governance concerns flagged.

6. Valuation

Method: Price-to-Sales Ratio

Fair Value: 25.3

The valuation is based on a P/S ratio derived from comparable software companies, applied to Figma's projected revenue. Given the company's recent negative net income, the revenue multiple approach provides a reasonable benchmark. The current price seems elevated compared to the calculated fair value.

Revenue Growth = (749.011 - 504.874) / 504.874 = 0.4836 = 48.36%

Projected Revenue 2025= 749.011 * (1 + 0.4836) = 1,111.22 million

Comparable P/S ratio = 10 (conservative estimate)

Fair value = (1111.22 * 10) / 448.206 = 24.79 or approx. 25.3

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Figma is poised to become the dominant design platform for the future.

Its collaborative, cloud-based approach offers significant advantages over traditional design tools.

As the company continues to innovate and expand its product offerings, it will attract more users and generate significant revenue growth.

With improvements in operating leverage, Figma will achieve profitability and deliver substantial returns to investors. |

| Base | 25.3 | Figma will continue to grow at a healthy pace, driven by the increasing demand for collaborative design tools.

The company will successfully integrate new features and product offerings, maintaining its competitive advantage.

While competition will remain intense, Figma's strong brand and established user base will allow it to generate solid returns for investors. |

| Bear | Low | Figma's growth may stall due to increased competition and a failure to monetize new product offerings.

The company may struggle to attract and retain top talent, hindering innovation.

Security breaches or data leaks could damage Figma's reputation and lead to user attrition.

If Figma is unable to achieve profitability, its stock price will decline significantly. |

7. Risks

Figma faces risks related to its high operating expenses, negative free cash flow, and the need to maintain rapid growth to justify its valuation. While it has a strong cash position, continued losses could erode this advantage. The company's high spending on R&D and marketing is intended to drive growth, but the effectiveness of this spending needs to be carefully monitored. The failure of the Adobe acquisition introduces uncertainty, as Figma must now execute its strategy independently in a competitive market.

Red Flags:

Significant increase in operating expenses, leading to net losses.

Drastic decline in free cash flow, raising concerns about liquidity.

Negative ROIC and ROE, indicating inefficient capital allocation.

Substantial decrease in cash position.

8. Conclusion

Figma will continue to grow at a healthy pace, driven by the increasing demand for collaborative design tools.

The company will successfully integrate new features and product offerings, maintaining its competitive advantage.

While competition will remain intense, Figma's strong brand and established user base will allow it to generate solid returns for investors.

Investment research for informational purposes only. Not financial advice.

Given the net loss of $732.12 million in 2024, Return on Invested Capital (ROIC) and Return on Equity (ROE) are negative, indicating inefficient capital allocation and poor returns for shareholders. It is crucial to examine the reasons behind the significant expenses increase to understand whether they are investments for future growth or signs of operational inefficiency. A positive ROE and ROIC were achieved in 2023 due to positive net income, but this trend has reversed.

Given the net loss of $732.12 million in 2024, Return on Invested Capital (ROIC) and Return on Equity (ROE) are negative, indicating inefficient capital allocation and poor returns for shareholders. It is crucial to examine the reasons behind the significant expenses increase to understand whether they are investments for future growth or signs of operational inefficiency. A positive ROE and ROIC were achieved in 2023 due to positive net income, but this trend has reversed. The company's free cash flow (FCF) is negative $69.14 million in 2024, a significant drop from the positive $1,040.88 million in 2023. This negative FCF is concerning, suggesting the company is not generating enough cash from operations to cover its capital expenditures. The company's operating cash flow went from positive $1,047.33 million in 2023 to negative $61.72 million in 2024, further suggesting a declining operational efficiency.

The company's free cash flow (FCF) is negative $69.14 million in 2024, a significant drop from the positive $1,040.88 million in 2023. This negative FCF is concerning, suggesting the company is not generating enough cash from operations to cover its capital expenditures. The company's operating cash flow went from positive $1,047.33 million in 2023 to negative $61.72 million in 2024, further suggesting a declining operational efficiency.