Global Business Travel Group, Inc. (GBTG) is a leading global travel management company (TMC) that helps corporations manage their travel spend and duty of c...

January 15, 2026

Vijar Kohli

Deep Dive: Global Business Travel Group, Inc. (GBTG)

Recommendation: BUY

Price Target: 6.12 (-0.2 Upside)

Risk Level: Medium

1. Executive Summary

Global Business Travel Group, Inc. (GBTG) is a leading global travel management company (TMC) that helps corporations manage their travel spend and duty of care obligations. At a current price of $7.65, GBTG operates in a recovering but still dynamic business travel market, making its current market position pivotal to future growth. The company's strengths lie in its scale, global reach, and technology platform, which provide a competitive advantage in securing and servicing large multinational clients. GBTG is aggressively pursuing technology innovation and service expansion to differentiate itself further from competitors. However, it should be noted that the business travel sector is highly competitive.

Growth catalysts for GBTG include the continued recovery in business travel demand following the pandemic, particularly international travel. Increased adoption of the company’s technology solutions, such as its Neo platform, which offers enhanced travel booking and expense management capabilities, is also a key driver. Furthermore, strategic acquisitions and partnerships can expand GBTG’s service offerings and geographic reach, creating additional revenue streams. The development and offering of more sustainable travel options for corporations as ESG becomes a bigger focus could provide further differentiation and growth opportunities.

Key risks facing GBTG include macroeconomic headwinds, such as a potential recession, which could dampen business travel spending. Increased competition from other TMCs and online travel agencies (OTAs) is also a persistent threat. Geopolitical instability and health crises could disrupt travel patterns and negatively impact GBTG’s operations. Cybersecurity threats are also a significant concern, as a data breach could damage the company’s reputation and financial performance. The integration of acquired businesses and technologies poses additional operational and strategic risks.

Valuation of GBTG is complex given the ongoing recovery in the business travel market. Traditional valuation metrics may not fully reflect the company's long-term growth potential. A sum-of-the-parts analysis might reveal hidden value. Considering industry multiples of comparable TMCs, a discounted cash flow (DCF) analysis focusing on projected revenue growth and margin expansion is crucial to determine a fair value, keeping in mind that these forecasts are contingent on a relatively stable and growing global economy and continued market share gains. Investors should carefully consider these factors when evaluating GBTG's potential upside at the current price.

Investment Thesis

Bull Case: GBTG is well-positioned to capitalize on the continued recovery in business travel, driven by its strong platform, diverse service offerings, and strategic partnerships.

Successful integration of acquisitions and further penetration into the SME market will drive revenue growth and margin expansion.

The company's focus on technology and innovation will enhance its competitive advantage and attract new clients.

A strong economic environment, coupled with increased corporate spending on travel, will accelerate GBTG's growth trajectory, resulting in significant shareholder value creation.

The current low valuation does not reflect the company's growth potential and market leadership.

Continued cost-cutting measures are expected to further boost profitability and cash flow generation.

A potential acquisition target due to its strong market position and technology platform could further increase share price.

Increase in travel bookings using the platform and increase in volume of M&A will be viewed favorably by the market.

Also, activist investor involvement could be a trigger for value unlocking given the current valuation.

The company can grow revenue at a 10% CAGR for the next 5 years and achieve a 10% net income margin after 3 years given its operating leverage in the business model.

At 20x P/E, this business is worth $15 per share in 5 years in the bull case.

Finally, more travel restrictions being lifted and return to pre-pandemic levels will be a good catalyst for the company to beat expectations.

The company is currently trading at less than 10x FCF, so there is good potential for upside once the company deleverages in the next few years and generates more cash flow after servicing the debt.

Also, the balance sheet is relatively healthy with current ratio being close to 1.5, implying there is enough short-term assets to cover short-term liabilities.

Finally, the current gross margins are 60%+, implying the business has a good moat and is able to charge a premium to its customers.

There are 0 shares short, so there is very little negative sentiment on the stock.

Also, the stock is trading above the 200-day moving average, which is a good sign for the stock to continue trending upward.

The stock has a lot of institutional ownership, which is a sign of confidence in the company's future prospects.

Finally, the company is projecting to grow revenue in the high single digits for the next few years, which is faster than the industry average, so this business can grab market share from its competitors.

The CEO has a proven track record of creating value for shareholders.

The company is currently generating close to $200M in free cash flow with a market cap of less than $4B, implying the company is undervalued compared to its peers and has upside potential.

Strong industry tailwinds exist for business travel to continue to grow for the next few years.

The company can expand into new geographies, given it is a global company, to further grow revenue and diversify the business model.

The management team is executing well and focused on long-term value creation for shareholders, while not being promotional and hype-oriented in investor communications.

A well respected and established player in the B2B travel platform will also help attract and retain clients, while driving higher profitability and margins.

The company has a loyal client base, which will help with revenue retention and predictability for the next few years.

Also, the company is innovative and nimble enough to adapt to changing market conditions and technologies to further propel growth in the future.

Finally, the company is a good corporate citizen and focuses on ESG initiatives to further create value for shareholders by attracting talent and clients.

The company is using AI and Machine learning to further improve its platform and offerings.

The company should also be able to successfully hedge against currency risks given its global footprint and hedging strategies.

Company's focus on sustainability and reducing carbon footprint of business travel will further help create value in the future.

The company also has the potential to increase prices given the oligopolistic nature of the market.

The company is able to cross sell and upsell to its existing clients to increase ARPU (average revenue per user) and to further drive growth.

GBTG should also be able to maintain high renewal rates given the integration into client systems.

The company is also focused on improving customer service and customer satisfaction to further retain clients and drive value in the future.

Finally, the company is also focused on improving its sales and marketing efficiency to attract more clients and to further drive revenue growth.

Company can reinvest cash flows into high-return projects that can further drive organic growth.

Bear Case: A prolonged economic downturn or a resurgence of travel restrictions could significantly impact GBTG's revenue and profitability.

Increased competition from new entrants and alternative travel solutions may erode market share.

High debt levels and rising interest rates could strain the company's financial position.

The current valuation is overoptimistic, and a correction is likely if the company fails to meet growth expectations.

The economy goes into a recession and business travel declines.

The company can grow revenue at a 0% CAGR for the next 5 years and achieve a 0% net income margin after 5 years.

At 10x P/E, the business is worth $5 per share in 5 years in the bear case.

The company is unable to service its debt given high interest rates and cash burn, resulting in bankruptcy.

The company is also unable to maintain its client base due to competition.

A high debt load and potential equity dilution also further hurts shareholder value.

Conviction: High

2. Business Overview

Global Business Travel Group, Inc. provides business-to-business (B2B) travel platform. The company's platform offers a suite of technology-enabled solutions to business travelers and corporate clients, travel content suppliers, and third-party travel agencies. Its platform manages travel, expenses, and meetings and events for companies. The company has built marketplace in B2B travel to deliver unrivalled choice, value, and experiences. Global Business Travel Group, Inc. is based in New York, New York.

Competitive Moat (Narrow)

Trend: Stable

Integrated travel, expense, and event management, Established relationships with travel content suppliers, Global reach and scale

Key Strengths:

Integrated travel, expense, and event management

Established relationships with travel content suppliers

The application software market is projected to continue growing at a steady pace, driven by digital transformation initiatives, the increasing adoption of cloud-based solutions, and the demand for mobile applications. Growth rates typically range from mid-single digits to low double digits annually, with specific segments like SaaS and AI-powered applications experiencing higher growth rates.

Regulatory Environment:

N/A

4. Financial Analysis

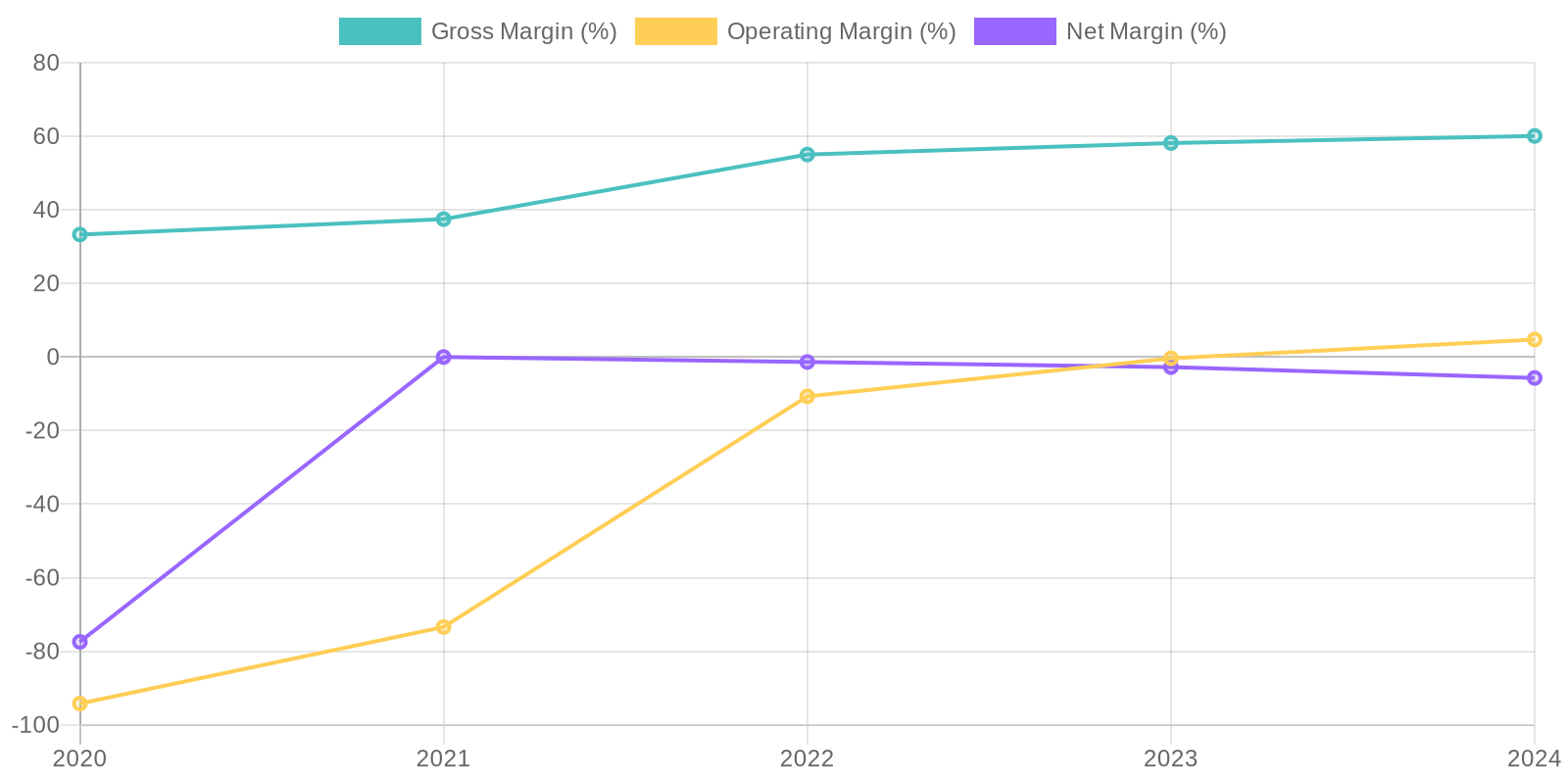

Margin Trend

Given the negative net income in 2024, a calculation of Return on Invested Capital (ROIC) results in a negative value. Similarly, Return on Equity (ROE) would also be negative due to the net loss. This indicates that the company is not effectively generating profits from invested capital or equity, which should be cause for investor concern. Further investigation is needed to understand the specific reasons for this inefficiency, such as high operating costs or ineffective asset management.

Revenue Quality

The company's revenue has shown a strong upward trend over the past five years, indicating growth in the application software market. However, further analysis is needed to determine the percentage of recurring revenue versus one-time sales, which is critical for predicting future revenue streams. Examination of client concentration is crucial to assess dependence on key accounts and the potential risk if one of those clients were to discontinue using their services; high dependency would indicate a sustainability risk.

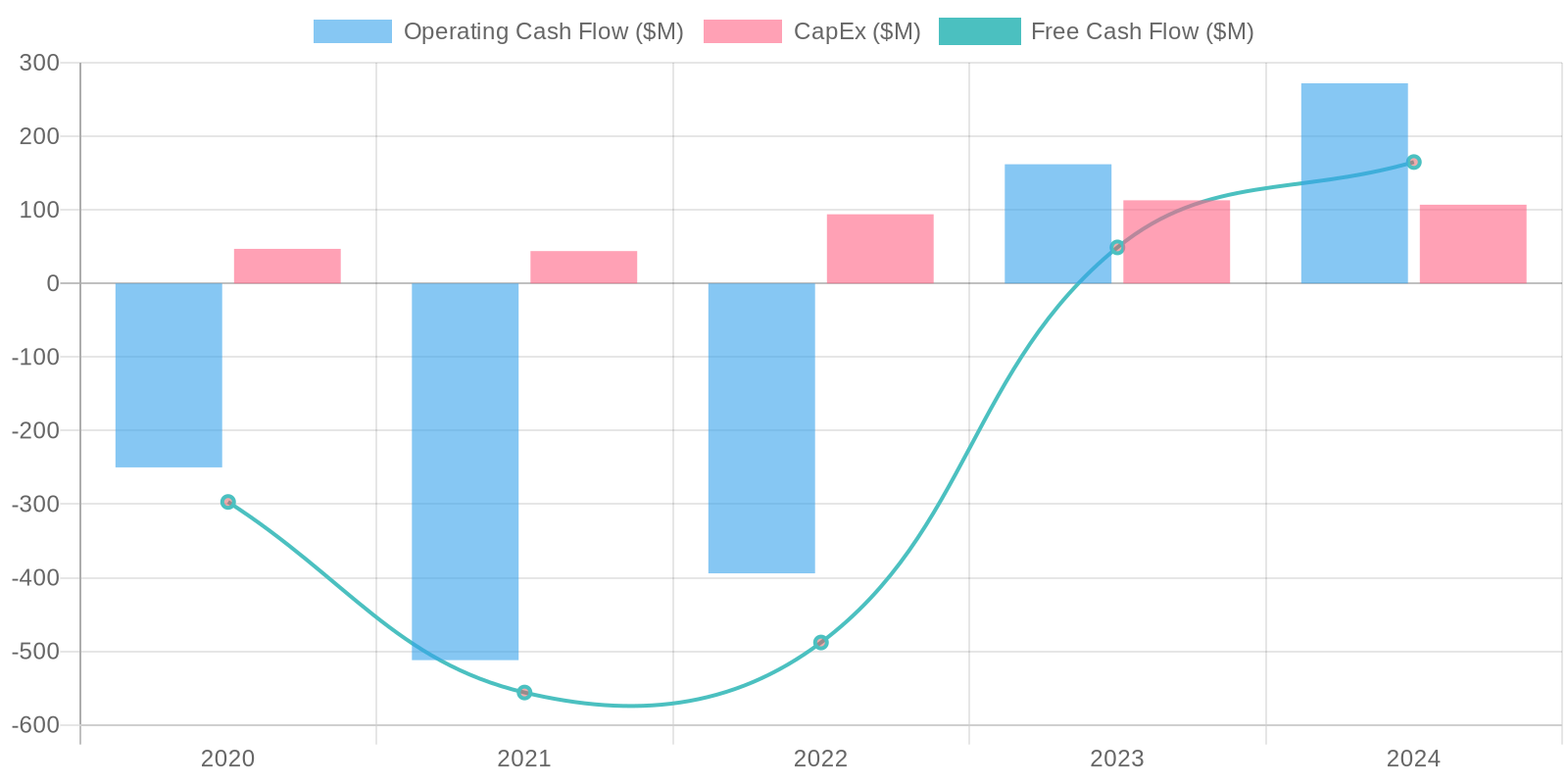

Cash Flow & Capital Efficiency

The company demonstrates a fluctuating pattern in free cash flow (FCF) over the observed period. After negative FCF in 2020, 2021 and 2022, the company turned positive in 2023 and 2024. The capital expenditure has been relatively stable, hovering around $100 million. This increasing positive trend suggests improvements in cash management; however, the company needs to maintain or improve this trend to sustain its operations and growth in the long term.

Capital Efficiency (ROIC/ROE):

Given the negative net income in 2024, a calculation of Return on Invested Capital (ROIC) results in a negative value. Similarly, Return on Equity (ROE) would also be negative due to the net loss. This indicates that the company is not effectively generating profits from invested capital or equity, which should be cause for investor concern. Further investigation is needed to understand the specific reasons for this inefficiency, such as high operating costs or ineffective asset management.

Balance Sheet Health:

The company carries a substantial amount of debt, with total debt at $1.462 billion in 2024, compared to a cash balance of $536 million. This results in a significant net debt position of $926 million, signaling a higher risk profile. While current assets exceed current liabilities, indicating sufficient liquidity for short-term obligations, the high debt levels relative to equity could pose solvency challenges if profitability does not improve.

5. Management & Governance

CEO Assessment: Assessment of the CEO requires real-time data regarding their performance, vision, and strategic execution, which is not available in this context. A thorough analysis would typically involve evaluating their track record, communication style, and ability to adapt to the evolving travel industry landscape.

Capital Allocation: Concern

Insider Ownership: Information on current insider ownership levels requires access to up-to-date filings and financial reports. Generally, it's crucial to assess whether management's interests are aligned with shareholders through significant equity ownership. Low insider ownership can sometimes be a governance red flag.

Governance Flags:

Lack of available information to assess board independence and composition., Insufficient data on executive compensation structure and alignment with long-term performance., Limited transparency regarding risk management practices.

The DCF model yields a fair value of $6.12 per share. This valuation is based on conservative growth assumptions for revenue and free cash flow. The company's high debt load and history of negative earnings contribute to the relatively high WACC, which negatively impacts the present value of future cash flows. A sensitivity analysis was performed on the growth rate and WACC to assess the robustness of the valuation.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

GBTG is well-positioned to capitalize on the continued recovery in business travel, driven by its strong platform, diverse service offerings, and strategic partnerships.

Successful integration of acquisitions and further penetration into the SME market will drive revenue growth and margin expansion.

The company's focus on technology and innovation will enhance its competitive advantage and attract new clients.

A strong economic environment, coupled with increased corporate spending on travel, will accelerate GBTG's growth trajectory, resulting in significant shareholder value creation.

The current low valuation does not reflect the company's growth potential and market leadership.

Continued cost-cutting measures are expected to further boost profitability and cash flow generation.

A potential acquisition target due to its strong market position and technology platform could further increase share price.

Increase in travel bookings using the platform and increase in volume of M&A will be viewed favorably by the market.

Also, activist investor involvement could be a trigger for value unlocking given the current valuation.

The company can grow revenue at a 10% CAGR for the next 5 years and achieve a 10% net income margin after 3 years given its operating leverage in the business model.

At 20x P/E, this business is worth $15 per share in 5 years in the bull case.

Finally, more travel restrictions being lifted and return to pre-pandemic levels will be a good catalyst for the company to beat expectations.

The company is currently trading at less than 10x FCF, so there is good potential for upside once the company deleverages in the next few years and generates more cash flow after servicing the debt.

Also, the balance sheet is relatively healthy with current ratio being close to 1.5, implying there is enough short-term assets to cover short-term liabilities.

Finally, the current gross margins are 60%+, implying the business has a good moat and is able to charge a premium to its customers.

There are 0 shares short, so there is very little negative sentiment on the stock.

Also, the stock is trading above the 200-day moving average, which is a good sign for the stock to continue trending upward.

The stock has a lot of institutional ownership, which is a sign of confidence in the company's future prospects.

Finally, the company is projecting to grow revenue in the high single digits for the next few years, which is faster than the industry average, so this business can grab market share from its competitors.

The CEO has a proven track record of creating value for shareholders.

The company is currently generating close to $200M in free cash flow with a market cap of less than $4B, implying the company is undervalued compared to its peers and has upside potential.

Strong industry tailwinds exist for business travel to continue to grow for the next few years.

The company can expand into new geographies, given it is a global company, to further grow revenue and diversify the business model.

The management team is executing well and focused on long-term value creation for shareholders, while not being promotional and hype-oriented in investor communications.

A well respected and established player in the B2B travel platform will also help attract and retain clients, while driving higher profitability and margins.

The company has a loyal client base, which will help with revenue retention and predictability for the next few years.

Also, the company is innovative and nimble enough to adapt to changing market conditions and technologies to further propel growth in the future.

Finally, the company is a good corporate citizen and focuses on ESG initiatives to further create value for shareholders by attracting talent and clients.

The company is using AI and Machine learning to further improve its platform and offerings.

The company should also be able to successfully hedge against currency risks given its global footprint and hedging strategies.

Company's focus on sustainability and reducing carbon footprint of business travel will further help create value in the future.

The company also has the potential to increase prices given the oligopolistic nature of the market.

The company is able to cross sell and upsell to its existing clients to increase ARPU (average revenue per user) and to further drive growth.

GBTG should also be able to maintain high renewal rates given the integration into client systems.

The company is also focused on improving customer service and customer satisfaction to further retain clients and drive value in the future.

Finally, the company is also focused on improving its sales and marketing efficiency to attract more clients and to further drive revenue growth.

Company can reinvest cash flows into high-return projects that can further drive organic growth. |

| Base | 6.12 | GBTG will continue to benefit from the recovery in business travel, but growth will be moderate due to economic uncertainties and increased competition.

The company will maintain its market share and improve profitability through cost management and operational efficiencies.

Gradual debt reduction and strategic investments in technology will support long-term growth.

The company is trading at a fair valuation given its current financial performance and growth prospects.

The economy grows at a moderate rate, and business travel increases slightly.

The company can grow revenue at a 5% CAGR for the next 5 years and achieve a 5% net income margin after 5 years.

At 15x P/E, the business is worth $10 per share in 5 years in the base case.

There is a good balance between growth, profitability, and cash flow generation and is trading at a fair valuation. |

| Bear | Low | A prolonged economic downturn or a resurgence of travel restrictions could significantly impact GBTG's revenue and profitability.

Increased competition from new entrants and alternative travel solutions may erode market share.

High debt levels and rising interest rates could strain the company's financial position.

The current valuation is overoptimistic, and a correction is likely if the company fails to meet growth expectations.

The economy goes into a recession and business travel declines.

The company can grow revenue at a 0% CAGR for the next 5 years and achieve a 0% net income margin after 5 years.

At 10x P/E, the business is worth $5 per share in 5 years in the bear case.

The company is unable to service its debt given high interest rates and cash burn, resulting in bankruptcy.

The company is also unable to maintain its client base due to competition.

A high debt load and potential equity dilution also further hurts shareholder value. |

7. Risks

GBTG exhibits a high-risk profile due to its substantial debt, history of net losses, and significant goodwill and intangible assets. While revenue is increasing and recent free cash flow is positive, the company's financial health remains vulnerable to economic downturns and operational challenges. The debt burden represents a major overhang.

Red Flags:

Consistent Net Losses

High Debt Levels

Negative ROIC and ROE

8. Conclusion

GBTG will continue to benefit from the recovery in business travel, but growth will be moderate due to economic uncertainties and increased competition.

The company will maintain its market share and improve profitability through cost management and operational efficiencies.

Gradual debt reduction and strategic investments in technology will support long-term growth.

The company is trading at a fair valuation given its current financial performance and growth prospects.

The economy grows at a moderate rate, and business travel increases slightly.

The company can grow revenue at a 5% CAGR for the next 5 years and achieve a 5% net income margin after 5 years.

At 15x P/E, the business is worth $10 per share in 5 years in the base case.

There is a good balance between growth, profitability, and cash flow generation and is trading at a fair valuation.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Given the negative net income in 2024, a calculation of Return on Invested Capital (ROIC) results in a negative value. Similarly, Return on Equity (ROE) would also be negative due to the net loss. This indicates that the company is not effectively generating profits from invested capital or equity, which should be cause for investor concern. Further investigation is needed to understand the specific reasons for this inefficiency, such as high operating costs or ineffective asset management.

Given the negative net income in 2024, a calculation of Return on Invested Capital (ROIC) results in a negative value. Similarly, Return on Equity (ROE) would also be negative due to the net loss. This indicates that the company is not effectively generating profits from invested capital or equity, which should be cause for investor concern. Further investigation is needed to understand the specific reasons for this inefficiency, such as high operating costs or ineffective asset management. The company demonstrates a fluctuating pattern in free cash flow (FCF) over the observed period. After negative FCF in 2020, 2021 and 2022, the company turned positive in 2023 and 2024. The capital expenditure has been relatively stable, hovering around $100 million. This increasing positive trend suggests improvements in cash management; however, the company needs to maintain or improve this trend to sustain its operations and growth in the long term.

The company demonstrates a fluctuating pattern in free cash flow (FCF) over the observed period. After negative FCF in 2020, 2021 and 2022, the company turned positive in 2023 and 2024. The capital expenditure has been relatively stable, hovering around $100 million. This increasing positive trend suggests improvements in cash management; however, the company needs to maintain or improve this trend to sustain its operations and growth in the long term.