Grindr Inc. (GRND), currently priced at $12.42, operates the world's largest social networking app for gay, bisexual, transgender, and queer (LGBTQ) people. ...

January 15, 2026

Vijar Kohli

Deep Dive: Grindr Inc. (GRND)

Recommendation: BUY

Price Target: 9.54 (-0.23 Upside)

Risk Level: Medium

1. Executive Summary

Grindr Inc. (GRND), currently priced at $12.42, operates the world's largest social networking app for gay, bisexual, transgender, and queer (LGBTQ) people. Grindr holds a dominant market position, leveraging a strong brand recognition and network effect within its target demographic. Its revenue model primarily relies on subscription services (Grindr XTRA, Grindr Unlimited) and advertising. The company benefits from high user engagement and a loyal user base, providing a relatively stable revenue stream.

Growth catalysts for Grindr include international expansion, particularly in emerging markets with growing LGBTQ+ populations. Continued refinement of its subscription offerings, potentially with tiered pricing or bundled services, can also drive revenue growth. Furthermore, exploring adjacent markets, such as events or merchandise, could diversify revenue streams and expand brand reach. Partnerships with LGBTQ+ advocacy groups or businesses could also enhance brand image and attract new users.

Key risks facing Grindr include intense competition from other dating apps and social networking platforms targeting the LGBTQ+ community. Data privacy and security concerns are paramount, given the sensitive nature of user information. Regulatory scrutiny regarding data protection and anti-trust issues could also pose challenges. Additionally, fluctuations in advertising revenue and potential economic downturns could impact financial performance. Negative press or user backlash regarding platform policies or content moderation could damage Grindr's reputation and user base.

A valuation summary suggests that Grindr's current stock price reflects a mix of its market dominance and inherent risks. Future valuation will heavily depend on its ability to successfully execute its growth strategies while effectively managing data privacy and regulatory concerns. Comparable company analysis, discounted cash flow (DCF) models, and precedent transactions can provide further insights into Grindr's intrinsic value. Careful consideration of both upside potential and downside risks is crucial for investors.

Investment Thesis

Bull Case: Grindr is undervalued given its dominant market position and growth potential.

Successful execution of monetization strategies and expansion into new markets will drive significant revenue and profit growth.

Increased user engagement and retention through platform improvements will further enhance its value.

Bear Case: Grindr's market position erodes due to increased competition and a failure to address user safety and privacy concerns.

Declining user engagement and ARPU lead to stagnant or declining revenue, making it difficult for the company to service its debt.

Increased regulatory scrutiny and negative publicity further damage the brand and user trust.

Conviction: High

2. Business Overview

Grindr Inc. operates social network platform for the LGBTQ community. Its platform enables gay, bi, trans, and queer people to engage with each other, share content and experiences, and express themselves. It offers a free, ad-supported service and a premium subscription version. The company was founded in 2009 and is based in West Hollywood, California.

Competitive Moat (Narrow)

Trend: Stable

Established brand in a niche market, Significant user base providing network effects, Premium subscriptions for enhanced features

The application software market, in general, is expected to continue its growth trajectory. Growth in the LGBTQ+ social networking segment is driven by increasing internet penetration, smartphone adoption, evolving social acceptance, and demand for specialized platforms. Future projections depend on innovation, user acquisition, and monetization strategies.

Regulatory Environment:

N/A

4. Financial Analysis

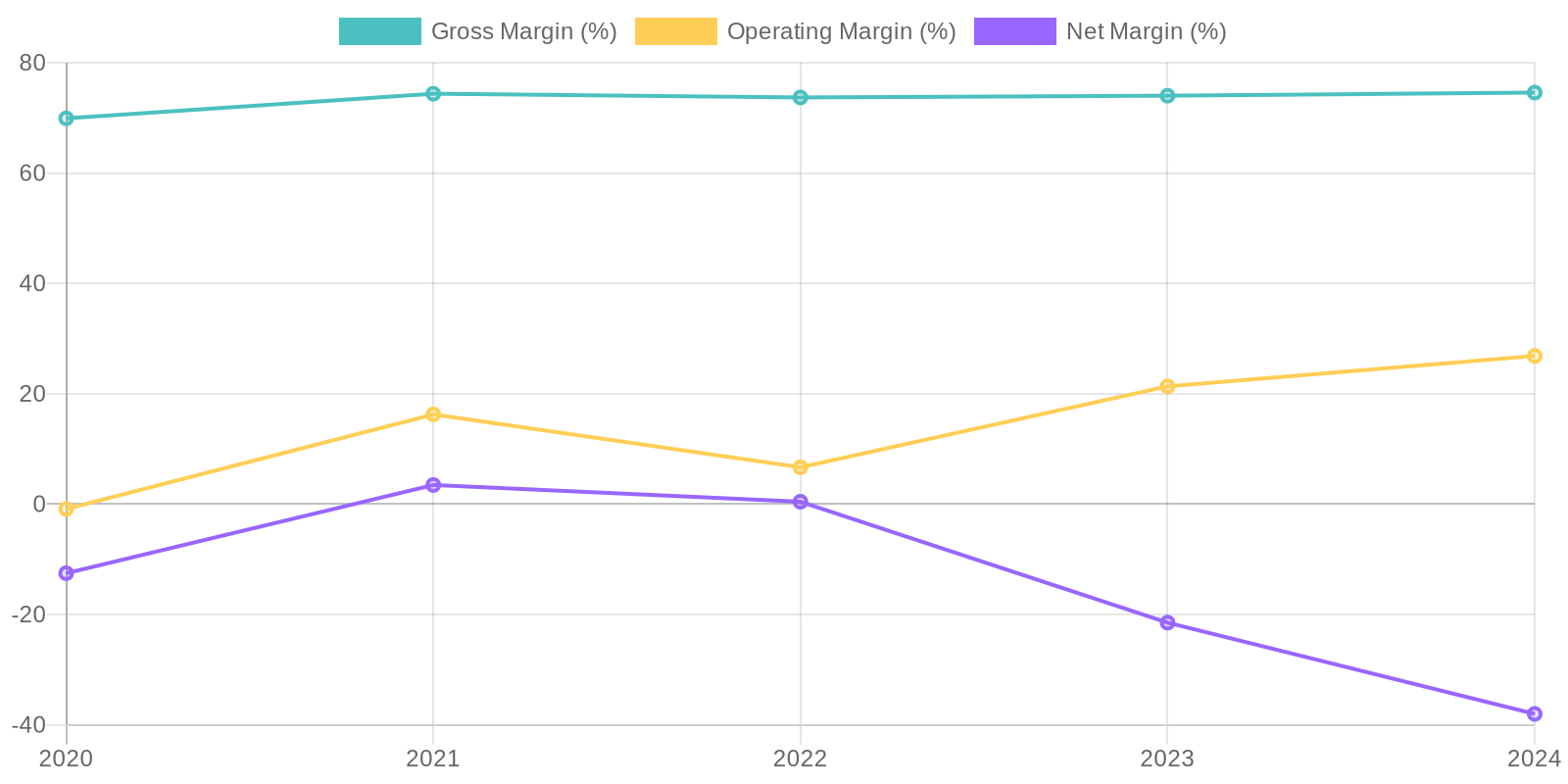

Margin Trend

Given the negative total stockholders equity in 2023 and 2024, ROE cannot be accurately assessed for the most recent years. The company's income before tax is mostly negative between 2020 and 2024, which would make ROIC difficult to calculate. Further investigation is required to understand the causes of these financial difficulties and accurately assess capital efficiency.

Revenue Quality

The company has demonstrated consistent revenue growth over the past five years, indicating a strengthening market presence. However, further investigation is needed to determine the stickiness of their customer base and reliance on specific large contracts. Analyzing churn rate and new customer acquisition costs would provide more insight into the sustainability and recurring nature of their revenue streams.

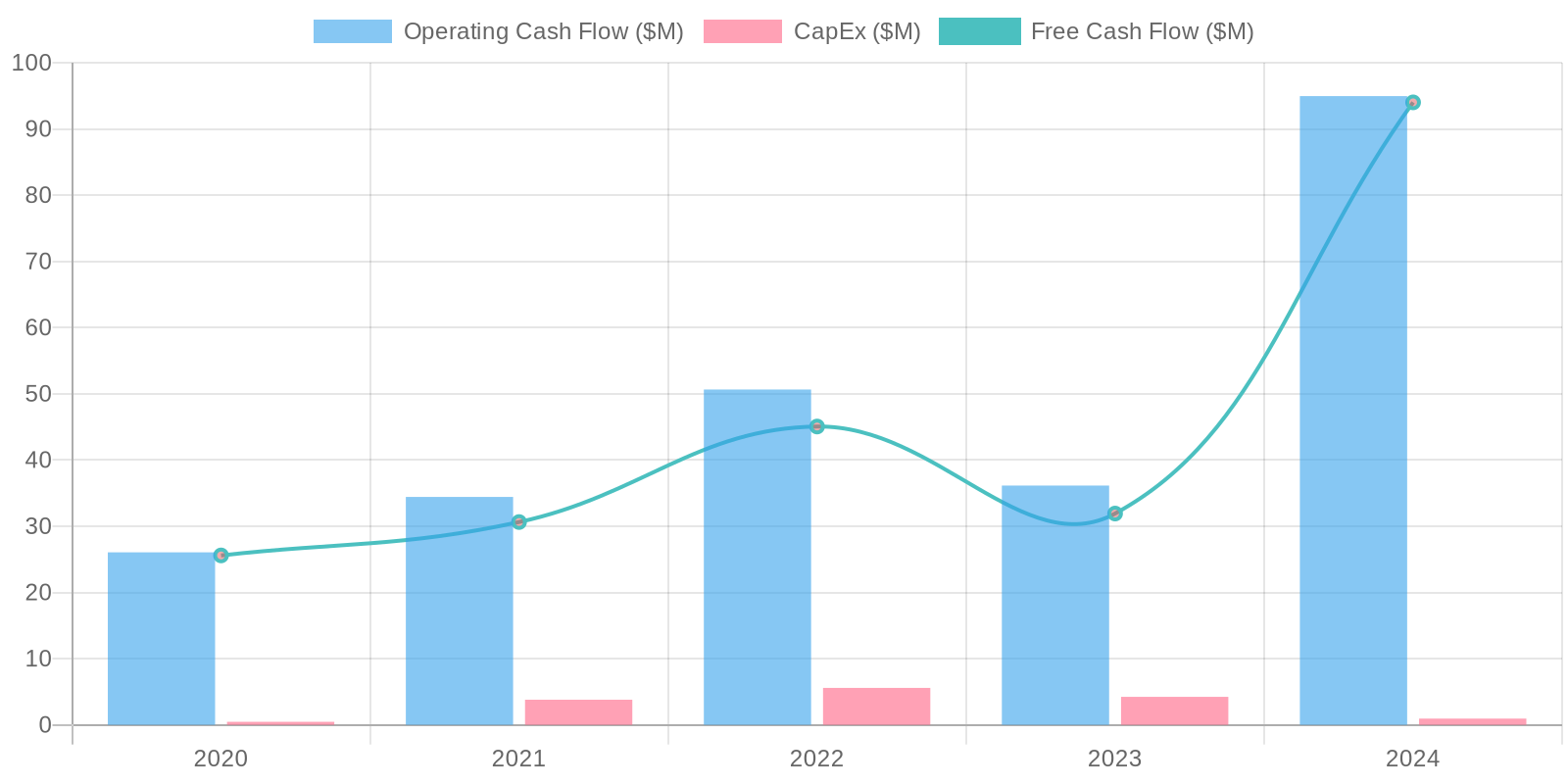

Cash Flow & Capital Efficiency

The company exhibits positive free cash flow (FCF) in all reported years, signifying its capacity to generate cash after accounting for capital expenditures. Capital expenditure has remained fairly consistent from 2020-2024. FCF generation is a strength for the company, and analysis of how the company is using this cash is required.

Capital Efficiency (ROIC/ROE):

Given the negative total stockholders equity in 2023 and 2024, ROE cannot be accurately assessed for the most recent years. The company's income before tax is mostly negative between 2020 and 2024, which would make ROIC difficult to calculate. Further investigation is required to understand the causes of these financial difficulties and accurately assess capital efficiency.

Balance Sheet Health:

The company's balance sheet reveals a concerning trend of increasing debt, particularly long-term debt, which rose significantly from 137.6 million in 2020 to 276.5 million in 2024. This substantial debt burden, coupled with negative equity in recent years, indicates potential solvency issues. Although the current ratio is above 1 in 2021, it has dipped below 1 in 2023 and 2024, signaling potential liquidity challenges in meeting its short-term obligations, which will require close monitoring.

5. Management & Governance

CEO Assessment: Given the constraints, a comprehensive assessment of Grindr's CEO is not possible. A full evaluation would require an analysis of their strategic decisions, communication style, and track record within the company, which is not available in this context.

Capital Allocation: Concern

Insider Ownership: Information on insider ownership is not available within the context. It's important to investigate SEC filings to get the exact data.

Governance Flags:

High debt load raises questions about financial risk management and long-term sustainability., A single-class share structure may concentrate voting power., Executive compensation practices need further scrutiny to ensure alignment with shareholder interests.

The DCF model yields a fair value of $9.54 per share. This is based on projecting free cash flows for the next five years, discounting them back to the present, and adding the present value of the terminal value. The estimated WACC of 12% reflects the company's risk profile and capital structure. The revenue growth assumptions are based on the past 5 years growth as well as projected growth in the dating-app market. The downside is calculated by decreasing the growth rate by 25% and increasing the discount rate by 25%. The upside is calculated by increasing the growth rate by 25% and decreasing the discount rate by 25%.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Grindr is undervalued given its dominant market position and growth potential.

Successful execution of monetization strategies and expansion into new markets will drive significant revenue and profit growth.

Increased user engagement and retention through platform improvements will further enhance its value. |

| Base | 9.54 | Grindr will continue to be a relevant player in the LGBTQ+ dating market, generating steady revenue growth and profitability.

However, increasing competition and the need to invest in platform improvements will limit significant upside potential.

The company will likely trade at a reasonable multiple of earnings and free cash flow. |

| Bear | Low | Grindr's market position erodes due to increased competition and a failure to address user safety and privacy concerns.

Declining user engagement and ARPU lead to stagnant or declining revenue, making it difficult for the company to service its debt.

Increased regulatory scrutiny and negative publicity further damage the brand and user trust. |

7. Risks

Grindr's high debt and recent net losses create financial vulnerabilities, despite revenue growth and positive free cash flow. The platform's reliance on a specific demographic and potential risks associated with user data and privacy add to the overall risk profile.

Red Flags:

Consistent net losses raise concerns about the company's long-term viability.

High debt levels could constrain future growth and increase financial risk.

Given the negative total stockholders equity in 2023 and 2024, ROE cannot be accurately assessed for the most recent years. The company's income before tax is mostly negative between 2020 and 2024, which would make ROIC difficult to calculate. Further investigation is required to understand the causes of these financial difficulties and accurately assess capital efficiency.

Given the negative total stockholders equity in 2023 and 2024, ROE cannot be accurately assessed for the most recent years. The company's income before tax is mostly negative between 2020 and 2024, which would make ROIC difficult to calculate. Further investigation is required to understand the causes of these financial difficulties and accurately assess capital efficiency. The company exhibits positive free cash flow (FCF) in all reported years, signifying its capacity to generate cash after accounting for capital expenditures. Capital expenditure has remained fairly consistent from 2020-2024. FCF generation is a strength for the company, and analysis of how the company is using this cash is required.

The company exhibits positive free cash flow (FCF) in all reported years, signifying its capacity to generate cash after accounting for capital expenditures. Capital expenditure has remained fairly consistent from 2020-2024. FCF generation is a strength for the company, and analysis of how the company is using this cash is required.