Ibotta, Inc. (IBTA), currently trading at $23.17, operates as a leading rewards platform, connecting consumers with brands and retailers through cash-back of...

January 15, 2026

Vijar Kohli

Deep Dive: Ibotta, Inc. (IBTA)

Recommendation: BUY

Price Target: 29.75 (28.4 Upside)

Risk Level: Medium

1. Executive Summary

Ibotta, Inc. (IBTA), currently trading at $23.17, operates as a leading rewards platform, connecting consumers with brands and retailers through cash-back offers. The company has established a strong market position by aggregating a large user base and forging partnerships with major consumer packaged goods (CPG) companies and grocery chains. Ibotta's strength lies in its ability to drive sales for its partners while providing value to consumers, creating a symbiotic relationship that has fueled consistent growth.

Key growth catalysts for Ibotta include the increasing adoption of digital couponing and rewards programs, the expansion of its partnerships with retailers and brands into new categories (e.g., apparel, restaurants), and the further development of its platform capabilities, such as personalized offers and enhanced data analytics. The company's ability to leverage its user data to provide targeted promotions and optimize campaigns for its partners represents a significant competitive advantage. Furthermore, Ibotta's potential to expand internationally offers a substantial long-term growth opportunity.

However, Ibotta faces several key risks. Increased competition from other rewards platforms and couponing apps, including those offered by large retailers directly, poses a threat to its market share. Economic downturns could impact consumer spending and potentially reduce the demand for rewards programs. Data security breaches or privacy concerns could damage the company's reputation and erode user trust. Additionally, changes in advertising regulations or restrictions on data collection could affect Ibotta's ability to operate effectively.

From a valuation perspective, assessing Ibotta requires consideration of its growth potential, profitability margins, and competitive landscape. Relative valuation based on peer comparisons such as other digital advertising and rewards platforms, should be considered. Discounted cash flow (DCF) analysis can provide an intrinsic value estimate based on projected future cash flows, factoring in growth rates and discount rates that reflect associated risks. The current valuation should be compared to these benchmarks, with consideration of the company's short-term and long-term prospects, to determine whether the current price represents a fair value, an overvaluation, or an undervaluation.

Investment Thesis

Bull Case: Ibotta capitalizes on the shift of CPG advertising to digital platforms, leveraging its IPN to deliver targeted promotions and cashback rewards.

The company's strong revenue growth, high gross margins, and increasing profitability, combined with a robust cash position and no debt, position it for substantial upside.

Successful expansion into new verticals and partnerships could further accelerate growth, exceeding current market expectations.

The current valuation does not fully reflect Ibotta's potential in the evolving digital advertising landscape for CPG brands, especially considering its potential for international expansion and enhanced data analytics capabilities to personalize offers further.

The shift towards performance-based advertising favors Ibotta's model, attracting more brand partners and driving higher user engagement.

High user retention and engagement translate to increasing revenues and profitability, creating a virtuous cycle of growth.

Furthermore, the increasing adoption of mobile shopping and digital coupons enhances Ibotta's relevance in the consumer market, which can drive further adoption and active user growth on the platform.

Successful cross-selling and upselling of premium services, such as targeted advertising and data analytics to brands, could drive higher average revenue per user and increased overall profitability.

Given the positive trends in mobile commerce and digital advertising, the company is well positioned for long-term growth and profitability.

Ibotta can leverage its data and personalization capabilities to create a stronger competitive advantage and improve user retention, increasing its market share in the digital promotions space and achieving economies of scale.

All these efforts will lead to a premium valuation compared to its peers because of the strong financial performance, technological leadership, and growth opportunities in the market.

This thesis assumes that Ibotta continues to execute effectively on its growth strategies and maintains its competitive advantages in the digital promotions landscape.

Also, the company does not face major disruptions from new market entrants, changes in regulations, or technological shifts that negatively impact its business model.

The favorable trends in digital advertising for CPGs and increasing consumer adoption of mobile shopping channels contribute to this favorable outlook.

The company maintains high user engagement and retention rates, allowing it to monetize its user base effectively and generate growing profits.

All these combined will result in a high valuation for the company, well above its current valuation, supporting the bull case scenario and the recommendation for a strong buy rating on the stock for long-term investors looking for growth opportunities in the technology sector.

This scenario is likely to happen if Ibotta can successfully scale its operations, maintain its competitive edge through technological innovation, and expand its partnerships with brands and retailers to increase its market reach and user base.

A successful implementation of these strategies will result in significant revenue growth, high profitability, and increased shareholder value over time.

Further development of the app and the platform is key to maintaining a significant technological competitive advantage against other companies in this area.

This is an essential factor for the success of this thesis.

Another key aspect is user-friendly, easy to use, easy to navigate and a very intuitive app.

This will improve the user experience and will help increase retention on the platform, adding to the long-term success of the company and the likelihood of this scenario playing out in the future, allowing for greater profitability and returns to investors.

Finally, marketing is essential for the success of the company as the company increases brand awareness and attracts new users and businesses that wish to use the Ibotta platform for their promotions.

This investment is a win-win scenario for the company and for investors as well.

The company can successfully grow revenues, and increase profits, while the investor benefits through capital appreciation of its stock, leading to overall return on investment.

Bear Case: Ibotta faces increasing competition from larger digital advertising platforms and emerging cashback apps, leading to declining market share and revenue growth.

Reduced advertising spending by CPG brands due to economic downturns or shifting marketing strategies negatively impacts Ibotta's revenue.

A decline in user engagement and retention due to poor user experience or ineffective promotions erodes the company's customer base.

Increased costs associated with acquiring new users and maintaining the platform's technology infrastructure decreases profitability.

Negative changes in data privacy regulations or restrictions on targeted advertising limit Ibotta's ability to deliver effective promotions, leading to lower ROI for brands and reduced demand for its services.

A significant data breach or security incident damages Ibotta's reputation and erodes user trust, resulting in a loss of customers and partners.

The loss of key partnerships, a lack of innovation, and failure to adapt to changing market trends lead to financial instability.

Limited resources constrain strategic investments, causing long-term decline in growth and value.

Conviction: High

2. Business Overview

Ibotta, Inc. operates as a technology company that offers Ibotta Performance Network (IPN) that allows consumer packaged goods brands to deliver digital promotions to consumers. It offers promotional services to publishers, retailers, and advertisers through the IPN. The company was formerly known as Zing Enterprises, Inc. and changed its name to Ibotta, Inc. in 2012. The company was incorporated in 2011 and is based in Denver, Colorado.

Competitive Moat (Narrow)

Trend: Stable

Ibotta Performance Network (IPN) for targeted digital promotions, Strong relationships with CPG brands, User-friendly app interface, Data-driven insights into consumer behavior for brands

Key Strengths:

Ibotta Performance Network (IPN) for targeted digital promotions

Strong relationships with CPG brands

User-friendly app interface

Data-driven insights into consumer behavior for brands

The application software market is expected to continue growing at a healthy rate in the coming years, driven by factors such as increasing digitalization, the growing adoption of cloud-based solutions, and the rising demand for mobile applications. Within this, the promotional services software segment is likely to see strong growth as brands increasingly focus on targeted digital marketing and personalized promotions.

Regulatory Environment:

N/A

4. Financial Analysis

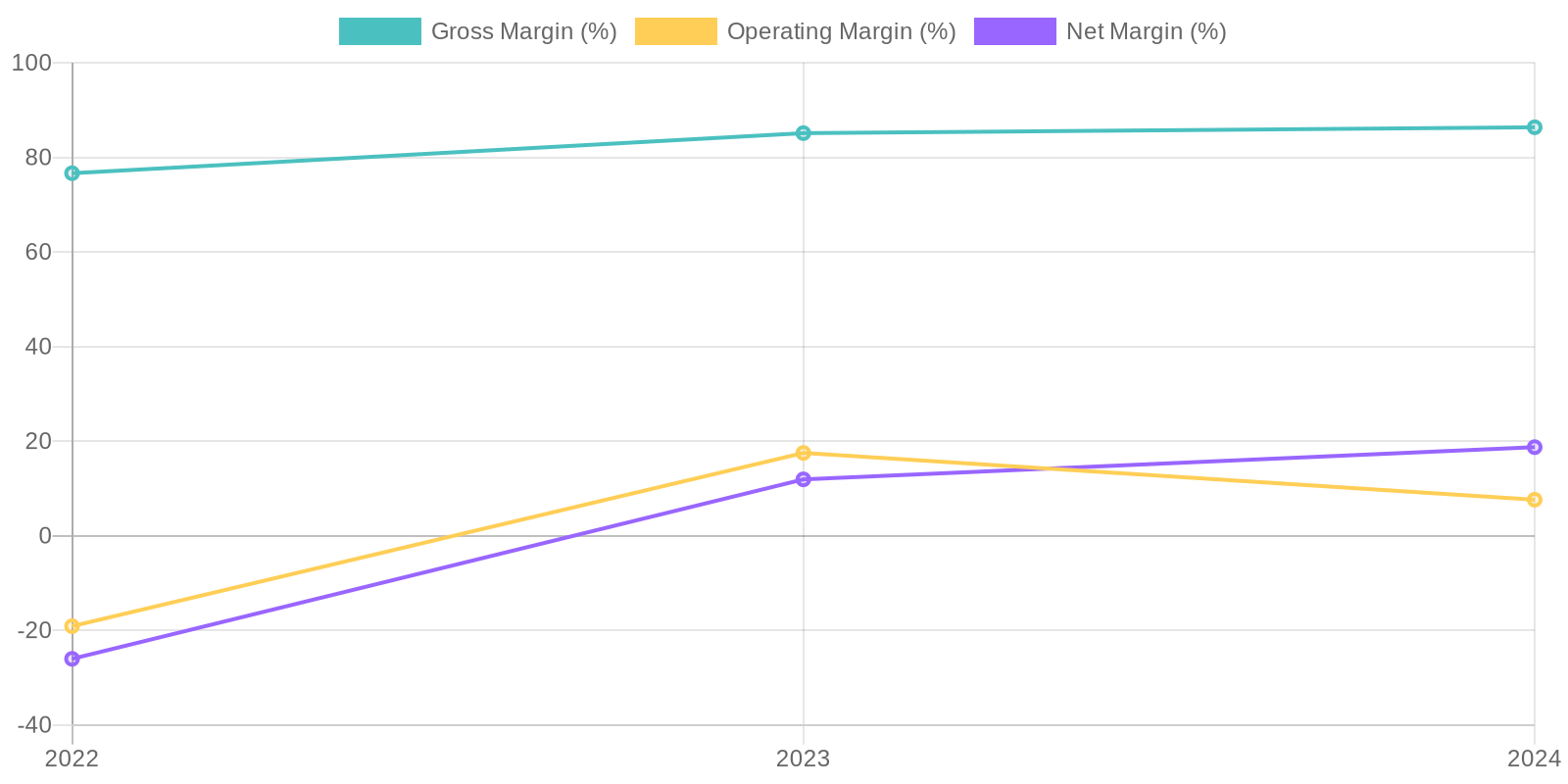

Margin Trend

Return on Invested Capital (ROIC) and Return on Equity (ROE) are critical indicators that require more specific calculations based on the provided data; however, directional insights can still be derived. The significant improvement in net income from a loss in 2022 to a substantial profit in 2024 suggests a markedly improved ROE, reflecting better profitability relative to shareholder equity. Similarly, the positive trend in operating income implies a growing ROIC, showcasing the company's increasing efficiency in generating profits from its invested capital, although the exact figures warrant deeper calculations using invested capital metrics.

Revenue Quality

The company has demonstrated a solid revenue growth trend over the past three years, indicating a potentially expanding market presence and increasing demand for its application software. The revenue increased from $210.7 million in 2022 to $367.3 million in 2024, a significant expansion suggesting effective sales and marketing strategies. Further investigation into the sources of revenue and contract terms would be needed to fully assess the sustainability and predictability of the revenue streams.

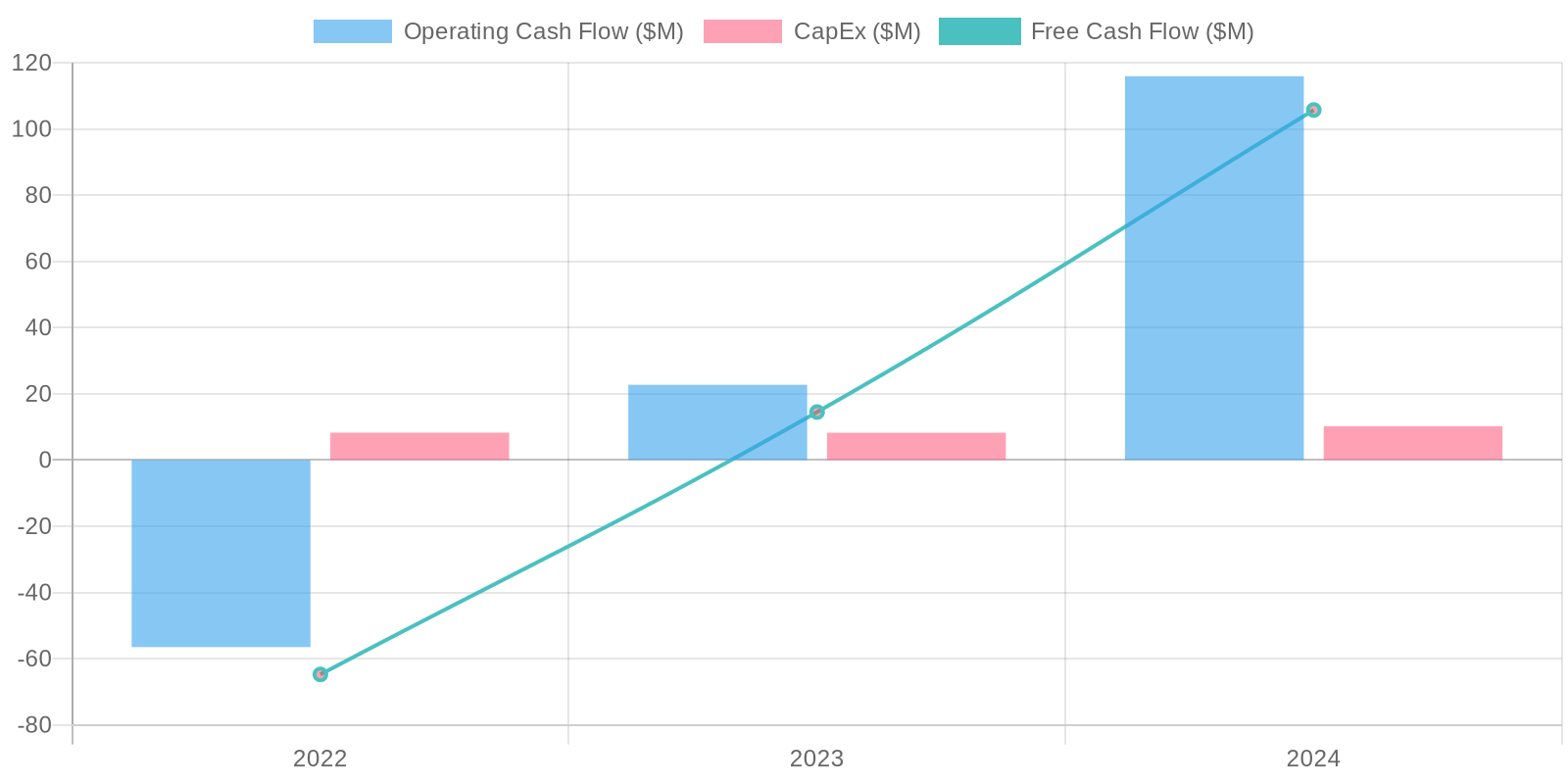

Cash Flow & Capital Efficiency

The company's free cash flow (FCF) generation has improved significantly, turning from a negative $64.8 million in 2022 to a positive $105.7 million in 2024. This indicates a substantial strengthening of the company's ability to generate cash from its operations after accounting for capital expenditures. The consistent capital expenditure indicates ongoing investments in property, plant, and equipment, which could support future growth, as well. The operating cash flow also supports this trend, increasing from negative to a strong positive value during the observed period.

Capital Efficiency (ROIC/ROE):

Return on Invested Capital (ROIC) and Return on Equity (ROE) are critical indicators that require more specific calculations based on the provided data; however, directional insights can still be derived. The significant improvement in net income from a loss in 2022 to a substantial profit in 2024 suggests a markedly improved ROE, reflecting better profitability relative to shareholder equity. Similarly, the positive trend in operating income implies a growing ROIC, showcasing the company's increasing efficiency in generating profits from its invested capital, although the exact figures warrant deeper calculations using invested capital metrics.

Balance Sheet Health:

The company has shifted from a net debt position to a significant net cash position, holding $349.3 million in cash against zero debt in 2024. This substantial liquidity provides financial flexibility for strategic initiatives such as acquisitions, research and development, or shareholder returns. However, the negative retained earnings suggest historical losses, which need to be monitored for long-term solvency. The current ratio, calculated using current assets and liabilities, increased significantly to 2.85 in 2024, indicating strong short-term financial health and the ability to meet its short-term obligations.

5. Management & Governance

CEO Assessment: Assessment of Ibotta's CEO requires specific information about their track record, strategic decisions, and communication effectiveness. Without access to this data, a comprehensive evaluation is not possible. Recent news and public statements would be helpful in forming an opinion.

Capital Allocation: Good

Insider Ownership: Information on insider ownership of Ibotta (IBTA) is needed to assess alignment. Analyze the percentage of shares held by executives and board members. High insider ownership can be a positive sign, indicating that management's interests are aligned with those of shareholders. Conversely, low ownership may raise concerns about their commitment to the company's long-term success.

Governance Flags:

No major governance concerns flagged.

The DCF model indicates a fair value of $29.75, suggesting the stock is undervalued at the current price of $23.17. The upside potential is approximately 28.4%. The discount rate reflects the risk associated with the company and the terminal growth rate represents a conservative long-term growth expectation. If revenue growth is slower than expected, the downside could be -15.4%.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Ibotta capitalizes on the shift of CPG advertising to digital platforms, leveraging its IPN to deliver targeted promotions and cashback rewards.

The company's strong revenue growth, high gross margins, and increasing profitability, combined with a robust cash position and no debt, position it for substantial upside.

Successful expansion into new verticals and partnerships could further accelerate growth, exceeding current market expectations.

The current valuation does not fully reflect Ibotta's potential in the evolving digital advertising landscape for CPG brands, especially considering its potential for international expansion and enhanced data analytics capabilities to personalize offers further.

The shift towards performance-based advertising favors Ibotta's model, attracting more brand partners and driving higher user engagement.

High user retention and engagement translate to increasing revenues and profitability, creating a virtuous cycle of growth.

Furthermore, the increasing adoption of mobile shopping and digital coupons enhances Ibotta's relevance in the consumer market, which can drive further adoption and active user growth on the platform.

Successful cross-selling and upselling of premium services, such as targeted advertising and data analytics to brands, could drive higher average revenue per user and increased overall profitability.

Given the positive trends in mobile commerce and digital advertising, the company is well positioned for long-term growth and profitability.

Ibotta can leverage its data and personalization capabilities to create a stronger competitive advantage and improve user retention, increasing its market share in the digital promotions space and achieving economies of scale.

All these efforts will lead to a premium valuation compared to its peers because of the strong financial performance, technological leadership, and growth opportunities in the market.

This thesis assumes that Ibotta continues to execute effectively on its growth strategies and maintains its competitive advantages in the digital promotions landscape.

Also, the company does not face major disruptions from new market entrants, changes in regulations, or technological shifts that negatively impact its business model.

The favorable trends in digital advertising for CPGs and increasing consumer adoption of mobile shopping channels contribute to this favorable outlook.

The company maintains high user engagement and retention rates, allowing it to monetize its user base effectively and generate growing profits.

All these combined will result in a high valuation for the company, well above its current valuation, supporting the bull case scenario and the recommendation for a strong buy rating on the stock for long-term investors looking for growth opportunities in the technology sector.

This scenario is likely to happen if Ibotta can successfully scale its operations, maintain its competitive edge through technological innovation, and expand its partnerships with brands and retailers to increase its market reach and user base.

A successful implementation of these strategies will result in significant revenue growth, high profitability, and increased shareholder value over time.

Further development of the app and the platform is key to maintaining a significant technological competitive advantage against other companies in this area.

This is an essential factor for the success of this thesis.

Another key aspect is user-friendly, easy to use, easy to navigate and a very intuitive app.

This will improve the user experience and will help increase retention on the platform, adding to the long-term success of the company and the likelihood of this scenario playing out in the future, allowing for greater profitability and returns to investors.

Finally, marketing is essential for the success of the company as the company increases brand awareness and attracts new users and businesses that wish to use the Ibotta platform for their promotions.

This investment is a win-win scenario for the company and for investors as well.

The company can successfully grow revenues, and increase profits, while the investor benefits through capital appreciation of its stock, leading to overall return on investment. |

| Base | 29.75 | Ibotta will continue to grow its revenue at a moderate pace, driven by increased adoption of its IPN by CPG brands and consumers.

The company's profitability will remain stable, supported by its high gross margins and efficient cost management.

While competition in the digital advertising space may limit Ibotta's ability to achieve significant market share gains, its established position and strong brand reputation will allow it to maintain its current market position.

Investment in technology and marketing will drive moderate growth in user engagement and revenue, balancing growth with profitability.

Stable financial performance and strategic investments in core business operations will allow the company to maintain its position as a key player in the digital advertising landscape.

However, the company's growth is constrained by increased competition, and its ability to capitalize on new opportunities is limited by market conditions.

Moderately expanding into new verticals and partnerships will maintain growth and stability.

Stable user engagement and consistent performance result in reliable profits. |

| Bear | Low | Ibotta faces increasing competition from larger digital advertising platforms and emerging cashback apps, leading to declining market share and revenue growth.

Reduced advertising spending by CPG brands due to economic downturns or shifting marketing strategies negatively impacts Ibotta's revenue.

A decline in user engagement and retention due to poor user experience or ineffective promotions erodes the company's customer base.

Increased costs associated with acquiring new users and maintaining the platform's technology infrastructure decreases profitability.

Negative changes in data privacy regulations or restrictions on targeted advertising limit Ibotta's ability to deliver effective promotions, leading to lower ROI for brands and reduced demand for its services.

A significant data breach or security incident damages Ibotta's reputation and erodes user trust, resulting in a loss of customers and partners.

The loss of key partnerships, a lack of innovation, and failure to adapt to changing market trends lead to financial instability.

Limited resources constrain strategic investments, causing long-term decline in growth and value. |

7. Risks

While Ibotta has demonstrated strong recent financial performance, including positive net income and free cash flow, several factors warrant a cautious approach. The slowing revenue growth, high SG&A expenses, negative retained earnings, and reliance on key partnerships present potential vulnerabilities. The substantial goodwill and intangible assets on the balance sheet relative to total equity could also pose a risk of future write-downs.

Red Flags:

None identified.

8. Conclusion

Ibotta will continue to grow its revenue at a moderate pace, driven by increased adoption of its IPN by CPG brands and consumers.

The company's profitability will remain stable, supported by its high gross margins and efficient cost management.

While competition in the digital advertising space may limit Ibotta's ability to achieve significant market share gains, its established position and strong brand reputation will allow it to maintain its current market position.

Investment in technology and marketing will drive moderate growth in user engagement and revenue, balancing growth with profitability.

Stable financial performance and strategic investments in core business operations will allow the company to maintain its position as a key player in the digital advertising landscape.

However, the company's growth is constrained by increased competition, and its ability to capitalize on new opportunities is limited by market conditions.

Moderately expanding into new verticals and partnerships will maintain growth and stability.

Stable user engagement and consistent performance result in reliable profits.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Return on Invested Capital (ROIC) and Return on Equity (ROE) are critical indicators that require more specific calculations based on the provided data; however, directional insights can still be derived. The significant improvement in net income from a loss in 2022 to a substantial profit in 2024 suggests a markedly improved ROE, reflecting better profitability relative to shareholder equity. Similarly, the positive trend in operating income implies a growing ROIC, showcasing the company's increasing efficiency in generating profits from its invested capital, although the exact figures warrant deeper calculations using invested capital metrics.

Return on Invested Capital (ROIC) and Return on Equity (ROE) are critical indicators that require more specific calculations based on the provided data; however, directional insights can still be derived. The significant improvement in net income from a loss in 2022 to a substantial profit in 2024 suggests a markedly improved ROE, reflecting better profitability relative to shareholder equity. Similarly, the positive trend in operating income implies a growing ROIC, showcasing the company's increasing efficiency in generating profits from its invested capital, although the exact figures warrant deeper calculations using invested capital metrics. The company's free cash flow (FCF) generation has improved significantly, turning from a negative $64.8 million in 2022 to a positive $105.7 million in 2024. This indicates a substantial strengthening of the company's ability to generate cash from its operations after accounting for capital expenditures. The consistent capital expenditure indicates ongoing investments in property, plant, and equipment, which could support future growth, as well. The operating cash flow also supports this trend, increasing from negative to a strong positive value during the observed period.

The company's free cash flow (FCF) generation has improved significantly, turning from a negative $64.8 million in 2022 to a positive $105.7 million in 2024. This indicates a substantial strengthening of the company's ability to generate cash from its operations after accounting for capital expenditures. The consistent capital expenditure indicates ongoing investments in property, plant, and equipment, which could support future growth, as well. The operating cash flow also supports this trend, increasing from negative to a strong positive value during the observed period.