InterDigital (IDCC) is a leading research and development company specializing in wireless and video technologies. Its primary business model revolves around...

January 15, 2026

Vijar Kohli

Deep Dive: InterDigital, Inc. (IDCC)

Recommendation: HOLD

Price Target: 325.5 (0.0485 Upside)

Risk Level: Medium

1. Executive Summary

InterDigital (IDCC) is a leading research and development company specializing in wireless and video technologies. Its primary business model revolves around licensing its extensive portfolio of patents, essential for cellular standards (like 5G) and video codecs, to device manufacturers. The company benefits from the increasing global adoption of these technologies, resulting in recurring royalty revenues. InterDigital holds a strong market position due to its early and sustained investment in fundamental research, giving it a robust patent portfolio that is difficult for competitors to replicate. Its stock currently trades at $310.43.

Growth catalysts for InterDigital are primarily centered around the continued rollout and expansion of 5G networks and the increasing demand for advanced video compression technologies. New licensing agreements with major device manufacturers, particularly in emerging markets, can significantly boost revenues. Furthermore, successful outcomes in patent enforcement actions and litigations will contribute positively to financial performance. The company's ongoing research into future technologies, such as 6G and AI-driven video compression, positions it to capitalize on future industry trends.

Key risks facing InterDigital include potential challenges to its patent validity, particularly from large, well-resourced technology companies. Unfavorable rulings in patent litigation can negatively impact its revenue stream. The cyclical nature of the wireless technology industry and the potential for technological disruptions (e.g., the emergence of alternative, non-patented technologies) also pose risks. Economic downturns could reduce consumer demand for devices using InterDigital's licensed technologies, impacting royalty revenues. Additionally, dependence on a small number of major licensees creates concentration risk.

Valuation Summary: InterDigital's valuation is heavily reliant on its ability to generate future royalty revenues from its patent portfolio. While a precise valuation requires detailed financial modeling, including discounted cash flow analysis of projected royalty streams, several factors suggest that the current price of $310.43 reflects a premium based on anticipated 5G revenue growth and potential future technologies. Key metrics to watch include licensing agreement renewals, litigation outcomes, and the company's success in securing new licensees. Changes in these factors can significantly impact market perception and, consequently, the company's stock price.

Investment Thesis

Bull Case: N/A

Bear Case: N/A

Conviction: High

2. Business Overview

InterDigital, Inc., together with its subsidiaries, designs and develops technologies that enable and enhance wireless communications in the United States, China, South Korea, Japan, Taiwan, and Europe. It provides technology solutions for use in digital cellular and wireless products and networks, including 2G, 3G, 4G, 5G, and IEEE 802-related products and networks. The company develops cellular technologies, such as technologies related to CDMA, TDMA, OFDM/OFDMA, and MIMO for use in 2G, 3G, 4G, and 5G wireless networks, as well as mobile terminal devices; and 3GPP technology portfolio in 5G NR, beyond 5G (B5G), extended reality over wireless, and cellular Internet of Things (IoT) areas, as well as technologies for automobiles, wearables, smart homes, drones, and other connected consumer electronic products. It also provides video coding and transmission technologies; and engages in the research and development of artificial intelligence. The company's patented technologies are used in various products that include cellular phones, tablets, notebook computers, and wireless personal digital assistants; wireless infrastructure equipment, which comprise base stations; components, dongles, and modules for wireless devices; and IoT devices and software platforms. As of December 31, 2021, it had a portfolio of approximately 27,500 patents and patent applications related to wireless communications, video coding, display technology, and other areas. InterDigital, Inc. was incorporated in 1972 and is headquartered in Wilmington, Delaware.

Competitive Moat (Narrow)

Trend: Stable

Proprietary technology portfolio., Expertise in wireless communications., Strong brand recognition within the industry.

The application software market is projected to continue growing at a healthy rate in the coming years, driven by digital transformation initiatives, increasing adoption of cloud-based solutions, the proliferation of mobile devices, and the growing importance of data analytics and AI. Growth rates vary by segment, with AI and IoT-related applications expected to experience the highest growth.

Regulatory Environment:

N/A

4. Financial Analysis

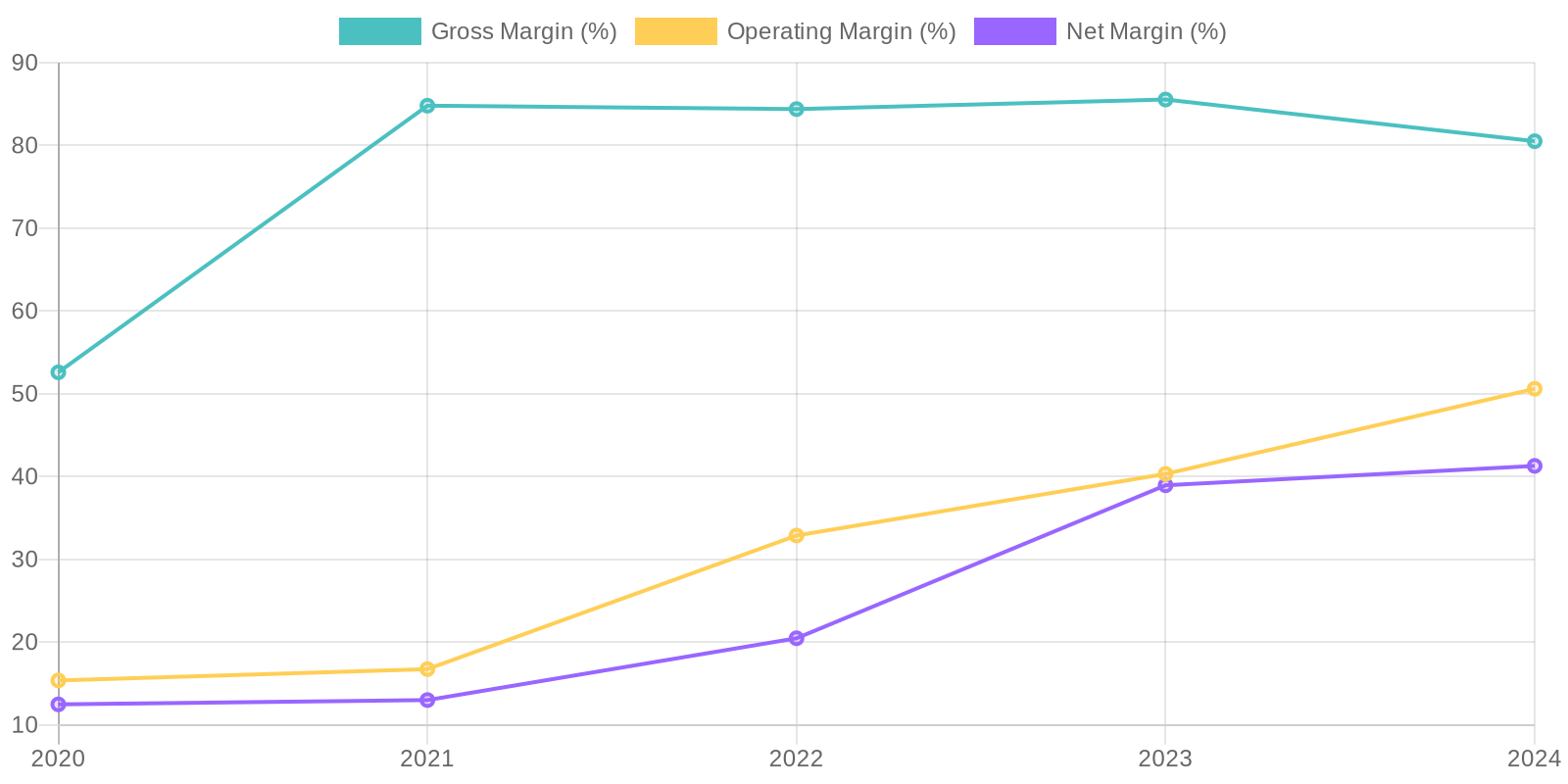

Margin Trend

Calculating Return on Invested Capital (ROIC) requires additional details regarding invested capital. The company's Return on Equity (ROE) can be roughly estimated, using Net Income and Total Equity. Given the rise in Net Income and Equity, ROE may show improvement in 2024. Trends in ROIC and ROE should be examined to ensure capital is being allocated efficiently and effectively to generate shareholder value.

Revenue Quality

The company has demonstrated consistent revenue growth over the past five years, indicating a potentially strong market position and effective sales strategies. The significant increase in revenue from 2023 to 2024 suggests successful expansion or increased market demand for their software applications, though a deeper analysis of the source of this growth is warranted to ensure its sustainability. Further investigation is needed to determine the portion of revenue derived from recurring subscriptions versus one-time licenses, as a higher proportion of recurring revenue generally indicates more predictable and stable future income.

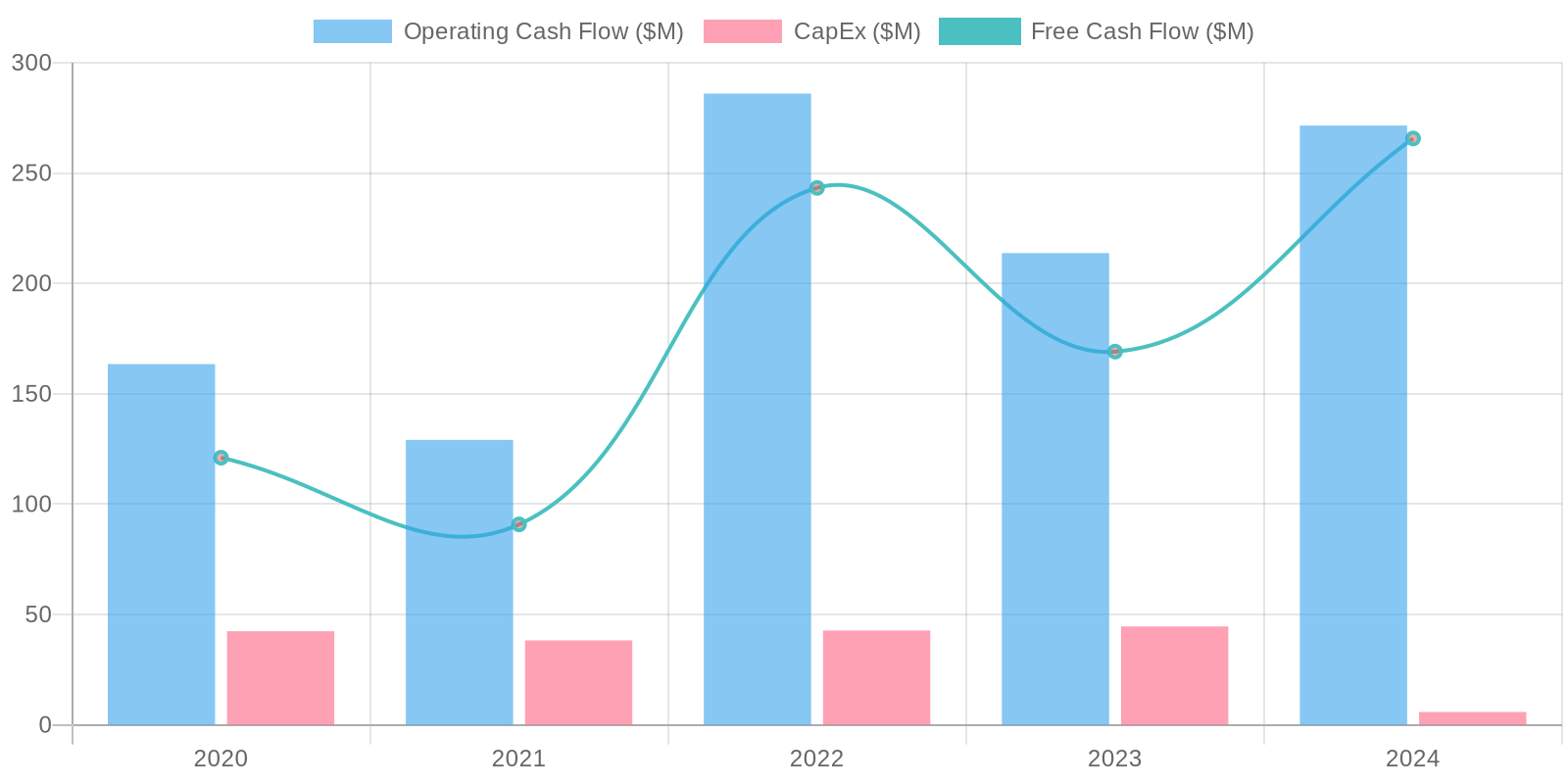

Cash Flow & Capital Efficiency

The company has consistently generated positive Free Cash Flow (FCF) over the past five years, demonstrating its ability to convert revenue into cash. The substantial increase in FCF in 2024 is particularly noteworthy, reflecting strong operational performance. A forensic review would dig deeper into the nature of capital expenditures to assess if they are being used effectively to generate growth.

Capital Efficiency (ROIC/ROE):

Calculating Return on Invested Capital (ROIC) requires additional details regarding invested capital. The company's Return on Equity (ROE) can be roughly estimated, using Net Income and Total Equity. Given the rise in Net Income and Equity, ROE may show improvement in 2024. Trends in ROIC and ROE should be examined to ensure capital is being allocated efficiently and effectively to generate shareholder value.

Balance Sheet Health:

The company maintains a solid balance sheet with substantial cash and short-term investments. While the company has a significant debt load, the net debt position is negative, implying they have more cash than debt. This provides financial flexibility to pursue growth opportunities or weather economic downturns. The current ratio, calculated by dividing total current assets by total current liabilities, is above 1.0, signifying the company's short-term obligations can be covered by its current assets.

5. Management & Governance

CEO Assessment: Assessment of InterDigital's CEO requires a review of their strategic decisions, execution track record, and communication with shareholders. Recent performance and forward-looking guidance should be analyzed. This assessment necessitates access to up-to-date financial reports, investor calls, and industry analysis not available at this time.

Capital Allocation: Good

Insider Ownership: Information regarding insider ownership as a percentage of total shares outstanding and the trend (increasing, decreasing, or stable) is needed to properly analyze insider alignment. This information can typically be found in the company's proxy statements and financial reports.

Governance Flags:

Lack of detailed information on board independence and committee structure.

The DCF model uses the company's free cash flow to project future cash flows and discounts them back to present value. A revenue growth rate of 15% is assumed for the first year, followed by a gradual decline to 5% over the next four years, and a terminal growth rate of 2%. An 8% discount rate is used to calculate the present value of future cash flows, and the current net debt is accounted for. The result of these calculations is a fair value of $325.50.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

N/A

Base

325.5

N/A

Bear

Low

N/A

7. Risks

InterDigital faces moderate risks due to its reliance on patent licensing, potential challenges in enforcing its patents, and revenue concentration. While the company's financial health appears generally stable with positive free cash flow, its debt and revenue volatility are areas of concern.

Red Flags:

The significant increase in revenue from 2023 to 2024 warrants a deeper investigation to confirm its source and sustainability, especially considering the limited information on client concentration.

The large 'otherTotalStockholdersEquity' negative balance requires clarification, as it significantly impacts the overall equity position and could indicate aggressive accounting practices or hidden liabilities.

The fluctuations in 'changeInWorkingCapital' from year to year should be investigated further. Large swings may point to mismanaged accounts receivables or payables.

8. Conclusion

N/A

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Calculating Return on Invested Capital (ROIC) requires additional details regarding invested capital. The company's Return on Equity (ROE) can be roughly estimated, using Net Income and Total Equity. Given the rise in Net Income and Equity, ROE may show improvement in 2024. Trends in ROIC and ROE should be examined to ensure capital is being allocated efficiently and effectively to generate shareholder value.

Calculating Return on Invested Capital (ROIC) requires additional details regarding invested capital. The company's Return on Equity (ROE) can be roughly estimated, using Net Income and Total Equity. Given the rise in Net Income and Equity, ROE may show improvement in 2024. Trends in ROIC and ROE should be examined to ensure capital is being allocated efficiently and effectively to generate shareholder value. The company has consistently generated positive Free Cash Flow (FCF) over the past five years, demonstrating its ability to convert revenue into cash. The substantial increase in FCF in 2024 is particularly noteworthy, reflecting strong operational performance. A forensic review would dig deeper into the nature of capital expenditures to assess if they are being used effectively to generate growth.

The company has consistently generated positive Free Cash Flow (FCF) over the past five years, demonstrating its ability to convert revenue into cash. The substantial increase in FCF in 2024 is particularly noteworthy, reflecting strong operational performance. A forensic review would dig deeper into the nature of capital expenditures to assess if they are being used effectively to generate growth.