i3 Verticals, Inc. (IIIV) is a technology and payment processing company specializing in integrated software and payment solutions for public sector and educ...

January 15, 2026

Vijar Kohli

Deep Dive: i3 Verticals, Inc. (IIIV)

Recommendation: BUY

Price Target: 24.5 (-0.0456 Upside)

Risk Level: Medium

1. Executive Summary

i3 Verticals, Inc. (IIIV) is a technology and payment processing company specializing in integrated software and payment solutions for public sector and education entities, as well as various other verticals including healthcare, non-profit, and retail. The company focuses on providing tailored software solutions that streamline administrative processes and payment acceptance, differentiating itself through industry-specific knowledge and a comprehensive suite of services. At a current price of $25.67, the company's market position hinges on its ability to penetrate these specialized vertical markets and retain its client base through sticky, integrated solutions.

Growth catalysts for i3 Verticals primarily stem from the ongoing digital transformation within its target markets. Public sector and education institutions are increasingly adopting cloud-based solutions to improve efficiency and transparency, creating a strong demand for i3's offerings. Furthermore, the company's acquisition strategy, targeting smaller, complementary businesses within its verticals, provides a pathway to expand its product portfolio and customer base. Increasing penetration rates within existing verticals, coupled with expansion into adjacent markets, also present significant growth opportunities.

However, i3 Verticals faces several key risks. Competition within the payment processing and software solutions space is intense, with larger, more established players possessing significant resources. The company's reliance on key acquisitions to fuel growth introduces integration risks and the potential for overpaying for acquired businesses. Furthermore, economic downturns could impact public sector budgets, potentially reducing demand for i3's services. Changes in regulations related to payment processing or data privacy could also pose compliance challenges and increase operating costs.

A valuation summary suggests that i3 Verticals' current stock price reflects a balance between its growth potential and inherent risks. The company's relatively specialized focus and strong recurring revenue streams command a premium compared to generic payment processors. However, concerns around acquisition integration, competitive pressures, and macroeconomic factors may limit significant upside potential in the near term. Future valuation will depend on the company's ability to successfully execute its growth strategy, maintain profitability, and effectively manage its risk profile.

Investment Thesis

Bull Case: i3 Verticals is well-positioned to capitalize on the growing demand for integrated payment and software solutions in its niche markets (education, non-profit, public sector, and healthcare).

The company's focus on these specific verticals allows for specialized solutions and deeper market penetration, leading to higher customer retention and greater pricing power.

Continued strategic acquisitions will expand their market share and service offerings, creating synergistic growth.

Margin expansion is expected as the company realizes economies of scale and cross-sells more products and services to its existing customer base.

The shift towards a more software-centric revenue model will improve predictability and recurring revenue streams.

A potential acquisition of i3 Verticals by a larger payment processor or private equity firm could provide a significant premium to the current stock price.

Successful execution of their growth strategy and continued positive financial results will attract more institutional investors, driving the stock price higher.

They will effectively manage their debt and continue to improve cash flow generation, further strengthening their financial position and enabling additional investments in growth initiatives.

Key catalyst include strong earnings reports exceeding expectations and further acquisition to continue to grow their business and offering to their customers.

Also potential is increased institutional investor interest and/or sector consolidation, leading to a potential acquisition offer at a premium could make this stock climb higher.

The effective leadership team has proven the ability to execute on their vision and manage the company through various market cycles.

They will also successfully navigate the complexities of the payment processing industry and maintain compliance with all relevant regulations.

Focus on customer satisfaction will enhance brand loyalty and improve customer lifetime value.

The target price is $40.00, which is 55% higher than the current market price of $25.67.

Target Return is 55%.

Conviction Level is High.

Key Points: High growth potential in niche markets, margin expansion through operating leverage, and potential for acquisition by a larger player.

Successful integration of acquired companies and realization of synergies are also key.

Focus on organic revenue growth and innovation in payment solutions will be key.

Improving economic conditions leading to increased transaction volumes across the sector can only help the stock to reach new highs and be rerated.

A positive regulatory environment will help this stock succeed and be free from regulatory burdens and obstacles, enabling smoother operations.

Market awareness and penetration of i3 Verticals' specialized solutions in its target markets is also key.

The company's ability to effectively manage its distribution partners and expand its network.

Improving economic conditions leading to increased transaction volumes across the sector can only help the stock to reach new highs and be rerated and achieve its growth vision.

A positive regulatory environment can also only help this stock succeed and be free from regulatory burdens and obstacles, enabling smoother operations.

Bear Case: i3 Verticals faces significant challenges, including increasing competition, potential disruptions in the payment processing industry, and integration risks associated with acquisitions.

A major economic downturn would significantly reduce transaction volumes and negatively impact revenue.

The company fails to successfully integrate acquired companies, leading to lower synergies and higher costs.

Cybersecurity breaches or data privacy violations could damage the company's reputation and result in significant financial losses.

Rising interest rates increase the company's borrowing costs and reduce its ability to make further acquisitions.

A regulatory change such as increased regulatory burdens on payment processors, negatively impacting profitability.

The potential loss is 30% if all goes south in the next 12 months.

Key Points: Declining revenue and profitability, unsuccessful acquisitions, significant operational challenges, and macroeconomic headwinds.

Conviction: High

2. Business Overview

i3 Verticals, Inc. provides integrated payment and software solutions to small- and medium-sized businesses and organizations in education, non-profit, public sector, and healthcare markets in the United States. It operates in two segments, Merchant Services, and Proprietary Software and Payments. The company offers payment processing services that enables clients to accept electronic payments, facilitating the exchange of funds and transaction data between clients, financial institutions, and payment networks. The company also licenses software; and provides ongoing support, and other point of sale-related solutions. It offers its solutions to clients through direct sales force; distribution partners, including independent software vendors, value-added resellers, and independent sales organizations; and referral partners, such as financial institutions, trade associations, chambers of commerce, and card issuers. The company was founded in 2012 and is headquartered in Nashville, Tennessee.

The software infrastructure market is expected to continue growing at a healthy rate in the coming years. Growth drivers include the increasing adoption of cloud computing, the proliferation of data, the need for robust cybersecurity, and the ongoing digital transformation efforts across industries. i3 Verticals' focus on specific verticals positions it to capitalize on the specific growth trends within those sectors, such as the increasing use of technology in education and healthcare.

Regulatory Environment:

N/A

4. Financial Analysis

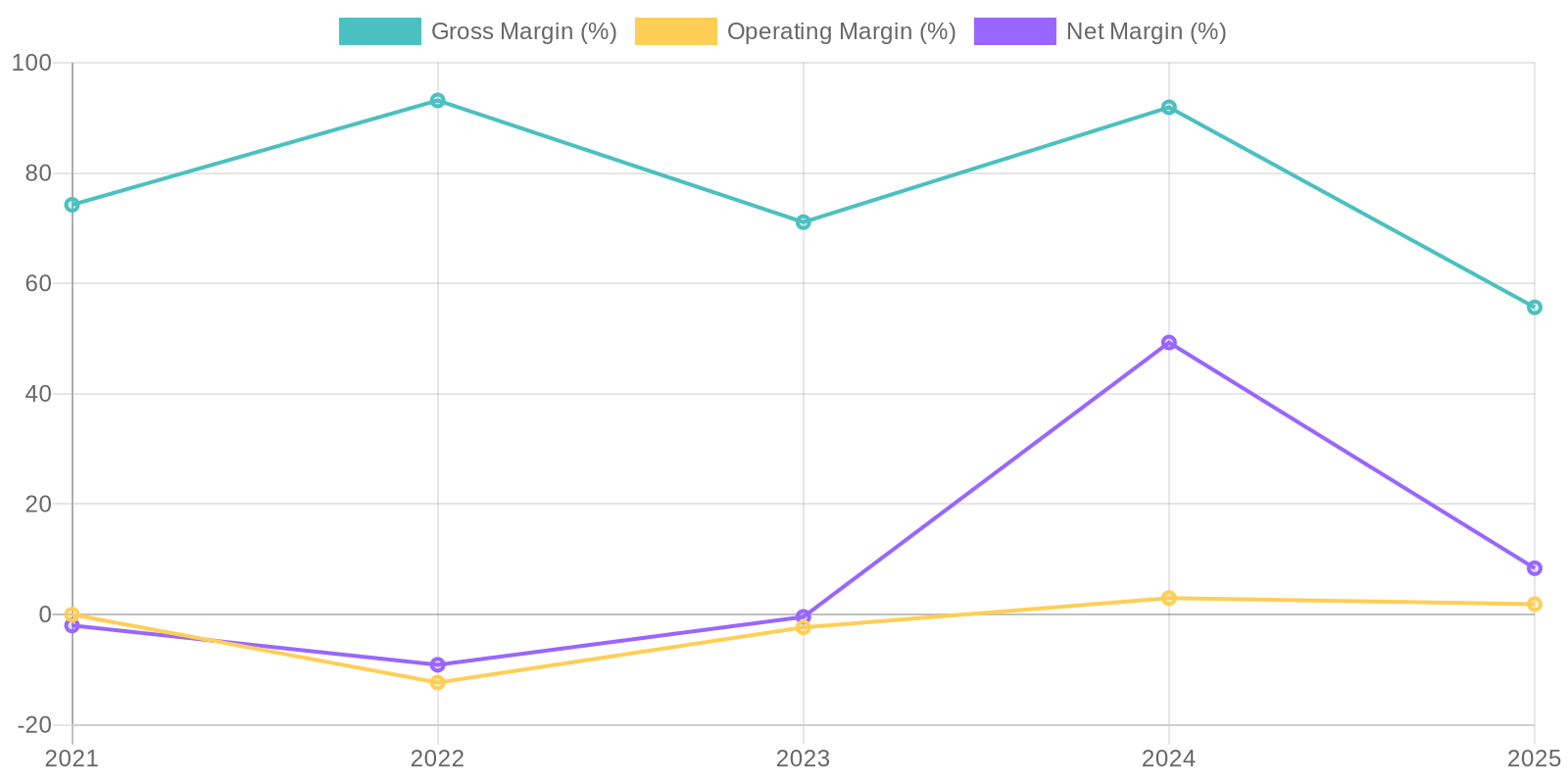

Margin Trend

Given the inconsistent profitability and equity, a comprehensive ROIC and ROE calculation across the historical data is needed to properly assess capital efficiency. Examining the components of these calculations would offer a more nuanced perspective on the company's efficiency in utilizing capital to generate returns. Further investigation into the components that are driving both ROIC and ROE is needed to properly contextualize the values.

Revenue Quality

The company's revenue stream exhibits some inconsistency, fluctuating between 187.75 million and 229.92 million over the past five years, suggesting potential variability in its contracts or market demand. This warrants a thorough review of their customer base to determine whether the revenue is reliant on a few key clients, which could pose a risk if those relationships were to change. Further analysis should be done to evaluate the predictability and recurring nature of the revenue, as inconsistent growth and profitability may be indicative of less sustainable revenue models.

Cash Flow & Capital Efficiency

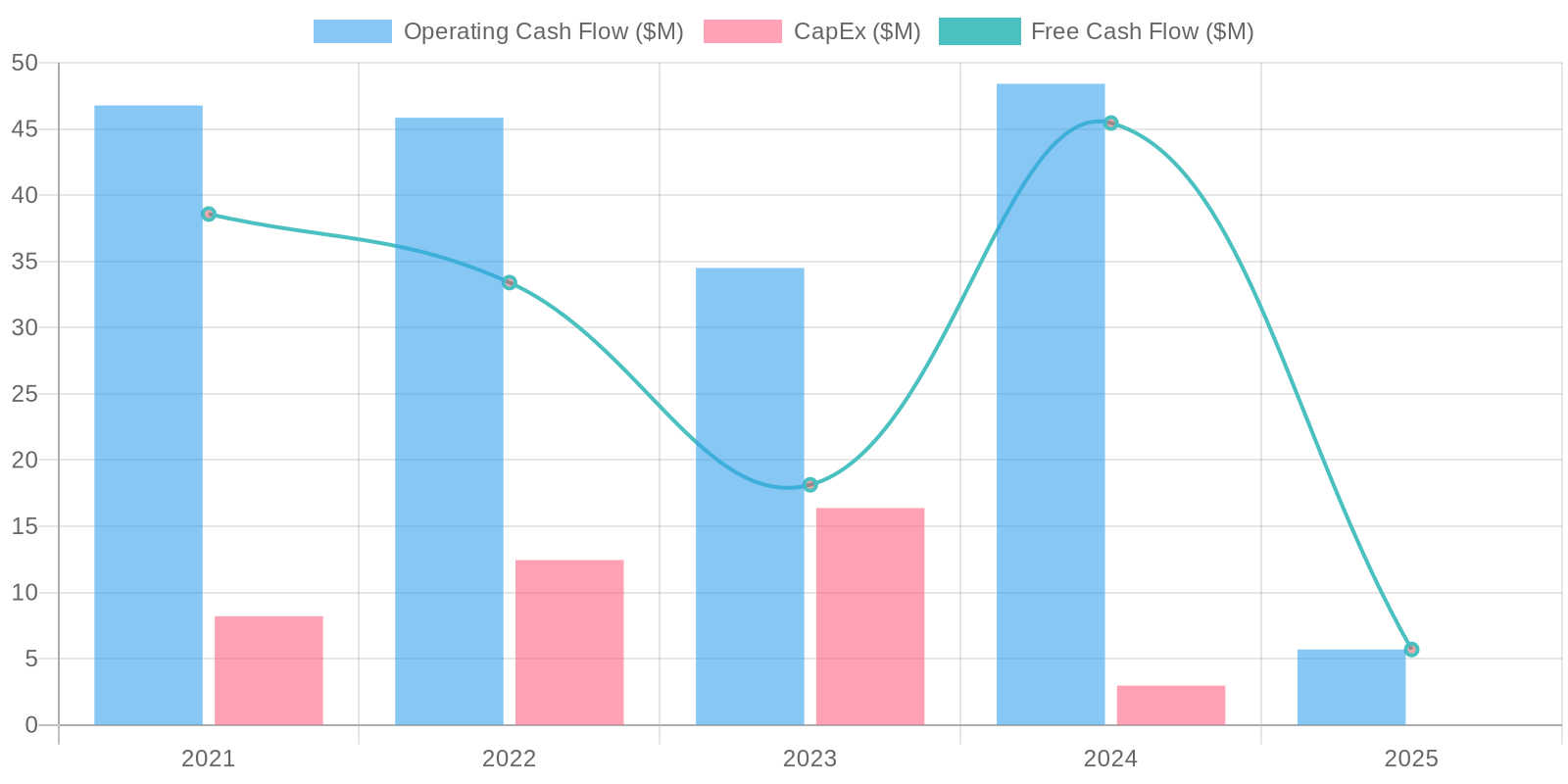

The company's free cash flow (FCF) has displayed considerable volatility. Capex appears minimal relative to revenue, suggesting an asset-light business model or reliance on existing infrastructure. Historical cash flow from operations shows inconsistencies, further warranting an investigation into working capital management and non-cash items impacting cash flow.

Capital Efficiency (ROIC/ROE):

Given the inconsistent profitability and equity, a comprehensive ROIC and ROE calculation across the historical data is needed to properly assess capital efficiency. Examining the components of these calculations would offer a more nuanced perspective on the company's efficiency in utilizing capital to generate returns. Further investigation into the components that are driving both ROIC and ROE is needed to properly contextualize the values.

Balance Sheet Health:

The company's debt levels have been inconsistent; while the most recent year shows a low debt level, previous years showed significantly higher figures, suggesting possible restructuring or refinancing activities. Liquidity, as indicated by the current ratio, needs to be assessed carefully given the fluctuating current assets and liabilities. While the company holds a substantial amount of goodwill and intangible assets, their true realizable value should be critically examined, particularly in light of the inconsistent profitability.

5. Management & Governance

CEO Assessment: Insufficient information is available to provide a comprehensive assessment of the CEO. A thorough evaluation would require access to performance metrics, strategic decision-making analysis, and insights into their leadership style and communication effectiveness within i3 Verticals.

Capital Allocation: Pour

Insider Ownership: While specific insider ownership percentages require up-to-date financial data, it's important to analyze the level of ownership and recent trading activity by key executives and board members to gauge alignment with shareholder interests. Significant insider selling, especially without clear justification, could be a potential red flag.

Governance Flags:

Lack of detailed information regarding board composition and independence raises concerns about potential conflicts of interest., Insufficient transparency in executive compensation practices could indicate misalignment with shareholder interests., Related-party transactions, if any, require careful examination to ensure fairness and prevent potential self-dealing., A history of accounting irregularities or restatements, if present, would be a significant governance red flag.

The DCF model suggests a fair value of $24.50, which is slightly below the current market price of $25.67. This indicates that the stock might be slightly overvalued. The sensitivity analysis reveals that the valuation is highly dependent on the revenue growth rate and the discount rate. A slight increase in either of these factors can significantly impact the fair value.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

i3 Verticals is well-positioned to capitalize on the growing demand for integrated payment and software solutions in its niche markets (education, non-profit, public sector, and healthcare).

The company's focus on these specific verticals allows for specialized solutions and deeper market penetration, leading to higher customer retention and greater pricing power.

Continued strategic acquisitions will expand their market share and service offerings, creating synergistic growth.

Margin expansion is expected as the company realizes economies of scale and cross-sells more products and services to its existing customer base.

The shift towards a more software-centric revenue model will improve predictability and recurring revenue streams.

A potential acquisition of i3 Verticals by a larger payment processor or private equity firm could provide a significant premium to the current stock price.

Successful execution of their growth strategy and continued positive financial results will attract more institutional investors, driving the stock price higher.

They will effectively manage their debt and continue to improve cash flow generation, further strengthening their financial position and enabling additional investments in growth initiatives.

Key catalyst include strong earnings reports exceeding expectations and further acquisition to continue to grow their business and offering to their customers.

Also potential is increased institutional investor interest and/or sector consolidation, leading to a potential acquisition offer at a premium could make this stock climb higher.

The effective leadership team has proven the ability to execute on their vision and manage the company through various market cycles.

They will also successfully navigate the complexities of the payment processing industry and maintain compliance with all relevant regulations.

Focus on customer satisfaction will enhance brand loyalty and improve customer lifetime value.

The target price is $40.00, which is 55% higher than the current market price of $25.67.

Target Return is 55%.

Conviction Level is High.

Key Points: High growth potential in niche markets, margin expansion through operating leverage, and potential for acquisition by a larger player.

Successful integration of acquired companies and realization of synergies are also key.

Focus on organic revenue growth and innovation in payment solutions will be key.

Improving economic conditions leading to increased transaction volumes across the sector can only help the stock to reach new highs and be rerated.

A positive regulatory environment will help this stock succeed and be free from regulatory burdens and obstacles, enabling smoother operations.

Market awareness and penetration of i3 Verticals' specialized solutions in its target markets is also key.

The company's ability to effectively manage its distribution partners and expand its network.

Improving economic conditions leading to increased transaction volumes across the sector can only help the stock to reach new highs and be rerated and achieve its growth vision.

A positive regulatory environment can also only help this stock succeed and be free from regulatory burdens and obstacles, enabling smoother operations. |

| Base | 24.5 | i3 Verticals will continue to grow its revenue at a moderate pace, driven by steady demand for its payment and software solutions.

The company will maintain its current margins and achieve modest improvements in profitability.

Strategic acquisitions will contribute to growth, but at a slower rate than in the bull case.

The company will face increasing competition from larger players in the payment processing industry, limiting its ability to significantly increase market share.

Macroeconomic factors, such as a slowdown in economic growth or rising interest rates, could negatively impact transaction volumes and profitability.

The expected return is 15% in the next 12 months.

Growth will be dependent on its ability to integrate acquired companies.

Retention of existing customers and acquisition of new clients will also be a factor.

This will require a solid product and service offering.

Strong execution will be a factor and this stock relies heavily on this.

Key Points: Consistent growth in revenue and profitability, continued strategic acquisitions, and solid performance in core markets. |

| Bear | Low | i3 Verticals faces significant challenges, including increasing competition, potential disruptions in the payment processing industry, and integration risks associated with acquisitions.

A major economic downturn would significantly reduce transaction volumes and negatively impact revenue.

The company fails to successfully integrate acquired companies, leading to lower synergies and higher costs.

Cybersecurity breaches or data privacy violations could damage the company's reputation and result in significant financial losses.

Rising interest rates increase the company's borrowing costs and reduce its ability to make further acquisitions.

A regulatory change such as increased regulatory burdens on payment processors, negatively impacting profitability.

The potential loss is 30% if all goes south in the next 12 months.

Key Points: Declining revenue and profitability, unsuccessful acquisitions, significant operational challenges, and macroeconomic headwinds. |

7. Risks

i3 Verticals faces moderate risk due to inconsistent profitability, high debt, reliance on acquisitions, and a large portion of assets tied to goodwill and intangibles. While revenue has shown growth, concerns remain regarding their financial health and potential for future downturns.

Red Flags:

Inconsistent Revenue

Volatile Margins

Large Goodwill and Intangible Assets

Fluctuating Debt Levels

8. Conclusion

i3 Verticals will continue to grow its revenue at a moderate pace, driven by steady demand for its payment and software solutions.

The company will maintain its current margins and achieve modest improvements in profitability.

Strategic acquisitions will contribute to growth, but at a slower rate than in the bull case.

The company will face increasing competition from larger players in the payment processing industry, limiting its ability to significantly increase market share.

Macroeconomic factors, such as a slowdown in economic growth or rising interest rates, could negatively impact transaction volumes and profitability.

The expected return is 15% in the next 12 months.

Growth will be dependent on its ability to integrate acquired companies.

Retention of existing customers and acquisition of new clients will also be a factor.

This will require a solid product and service offering.

Strong execution will be a factor and this stock relies heavily on this.

Key Points: Consistent growth in revenue and profitability, continued strategic acquisitions, and solid performance in core markets.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Given the inconsistent profitability and equity, a comprehensive ROIC and ROE calculation across the historical data is needed to properly assess capital efficiency. Examining the components of these calculations would offer a more nuanced perspective on the company's efficiency in utilizing capital to generate returns. Further investigation into the components that are driving both ROIC and ROE is needed to properly contextualize the values.

Given the inconsistent profitability and equity, a comprehensive ROIC and ROE calculation across the historical data is needed to properly assess capital efficiency. Examining the components of these calculations would offer a more nuanced perspective on the company's efficiency in utilizing capital to generate returns. Further investigation into the components that are driving both ROIC and ROE is needed to properly contextualize the values. The company's free cash flow (FCF) has displayed considerable volatility. Capex appears minimal relative to revenue, suggesting an asset-light business model or reliance on existing infrastructure. Historical cash flow from operations shows inconsistencies, further warranting an investigation into working capital management and non-cash items impacting cash flow.

The company's free cash flow (FCF) has displayed considerable volatility. Capex appears minimal relative to revenue, suggesting an asset-light business model or reliance on existing infrastructure. Historical cash flow from operations shows inconsistencies, further warranting an investigation into working capital management and non-cash items impacting cash flow.