Jamf Holding Corp. (JAMF), currently trading at $13.02, occupies a leading position in the Apple device management (MDM) market. The company provides a compr...

January 15, 2026

Vijar Kohli

Deep Dive: Jamf Holding Corp. (JAMF)

Recommendation: BUY

Price Target: 13.5 (0.0369 Upside)

Risk Level: Medium

1. Executive Summary

Jamf Holding Corp. (JAMF), currently trading at $13.02, occupies a leading position in the Apple device management (MDM) market. The company provides a comprehensive suite of software solutions that enable organizations to effectively manage and secure Apple devices, including iPhones, iPads, and Macs. Its strong brand recognition, specialized focus on the Apple ecosystem, and large customer base provide a significant competitive advantage.

Growth catalysts for Jamf include the continued proliferation of Apple devices in enterprise and education settings, cross-selling and upselling opportunities within its existing customer base, and expansion into adjacent markets such as endpoint security and identity management. The increasing complexity of IT environments and the growing demand for enhanced security solutions are also expected to drive demand for Jamf's offerings. Furthermore, strategic partnerships with Apple and other technology providers could fuel additional growth.

Key risks facing Jamf include intense competition from larger players in the MDM market, such as Microsoft and VMware, as well as emerging niche competitors. Economic downturns could reduce IT spending and negatively impact Jamf's revenue. The company's reliance on the Apple ecosystem also exposes it to potential risks associated with changes in Apple's product strategy or software updates. Data security breaches or service disruptions could damage Jamf's reputation and erode customer trust.

Valuation is complex given the current macro environment. Based on available information, a discounted cash flow (DCF) analysis and comparable company analysis suggest a range of fair values. However, given the current market volatility and uncertainty surrounding future growth rates, accurately estimating intrinsic value is challenging. The current market price reflects a degree of investor skepticism regarding Jamf's ability to sustain its historical growth trajectory and effectively compete in the evolving MDM landscape. Further monitoring of company performance, industry trends, and macroeconomic factors is crucial to assess its long-term investment potential.

Investment Thesis

Bull Case: Jamf is significantly undervalued due to temporary macroeconomic headwinds and concerns about profitability.

As Apple's ecosystem continues to penetrate enterprise and education, Jamf's leading platform for managing and securing these devices will experience accelerated growth.

Margin expansion through operating leverage and successful cross-selling will drive significant earnings growth, leading to substantial stock appreciation.

Bear Case: Jamf fails to effectively compete against larger players like Microsoft, resulting in market share loss and decelerating revenue growth.

Continued operating losses erode investor confidence, and the company's high debt burden limits its ability to invest in growth initiatives.

This leads to a significant decline in the stock price.

Conviction: High

2. Business Overview

Jamf Holding Corp. offers a cloud software platform for Apple infrastructure and security platform worldwide. Its products include Jamf Pro, an Apple ecosystem management software solution for IT environments; Jamf Now, a pay-as-you-go Apple device management software solution for small-to-medium-sized businesses; Jamf School, a software solution for educators; Jamf Data Policy, a solution to enforce acceptable usage policies to eliminate shadow IT and block risky content and manage data consumption with real-time analytics and granular reporting; and Jamf Connect that streamlines Mac authentication and identity management; and Jamf Private Access, a ZTNA solution that replaces legacy conditional access and VPN technology. The company also offers Jamf Protect, which provides protection of Mac-targeted malware and creates customized telemetry and detections that give enterprise security teams visibility into their Macs; Jamf Threat Defense, a solution to protect workers from malicious attackers; and Jamf Nation, an online community of IT and security professionals focusing on Apple in the enterprise. It sells its SaaS solutions through a subscription model, direct sales force, and online, as well as indirectly through channel partners, including Apple. The company was founded in 2002 and is headquartered in Minneapolis, Minnesota.

Competitive Moat (Narrow)

Trend: Stable

Deep Apple ecosystem expertise, Strong brand recognition in its niche, Active and valuable online community

The market is expected to continue growing at a healthy pace due to the increasing demand for managing and securing Apple devices in various organizations. Growth is fueled by trends like BYOD (Bring Your Own Device) policies, remote work, and the increasing sophistication of cyber threats targeting macOS and iOS devices. The shift towards subscription-based SaaS models also drives recurring revenue and overall market expansion. Again, consulting industry reports will provide specific CAGR (Compound Annual Growth Rate) projections.

Regulatory Environment:

N/A

4. Financial Analysis

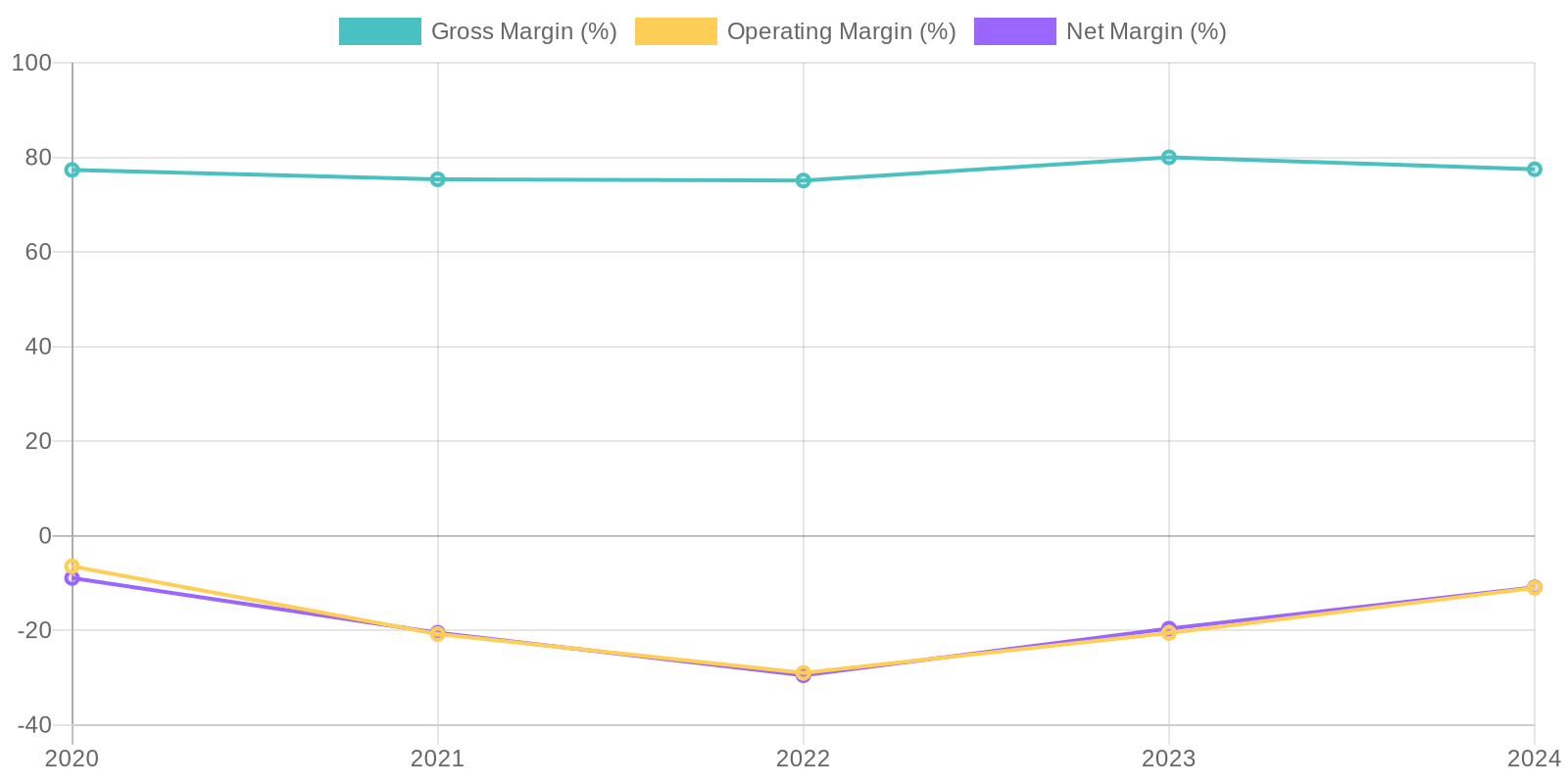

Margin Trend

Given the consistent negative net income, Return on Invested Capital (ROIC) and Return on Equity (ROE) are negative, reflecting an inefficient use of capital. Specifically, the company isn't generating profits from its investments and equity. This could stem from a combination of factors, including substantial investments in growth initiatives, acquisitions, or operational inefficiencies. The negative profitability needs to be addressed to improve capital efficiency.

Revenue Quality

Jamf's revenue has demonstrated consistent growth over the past five years, indicating a potentially strong market position in its sector. However, the quality of this revenue needs further scrutiny regarding its recurring nature, as consistent revenue growth does not automatically imply high revenue quality. Client concentration should also be evaluated to determine the potential impact of losing a major client, and sustainability should be assessed by looking at factors such as customer churn and competitive pressures.

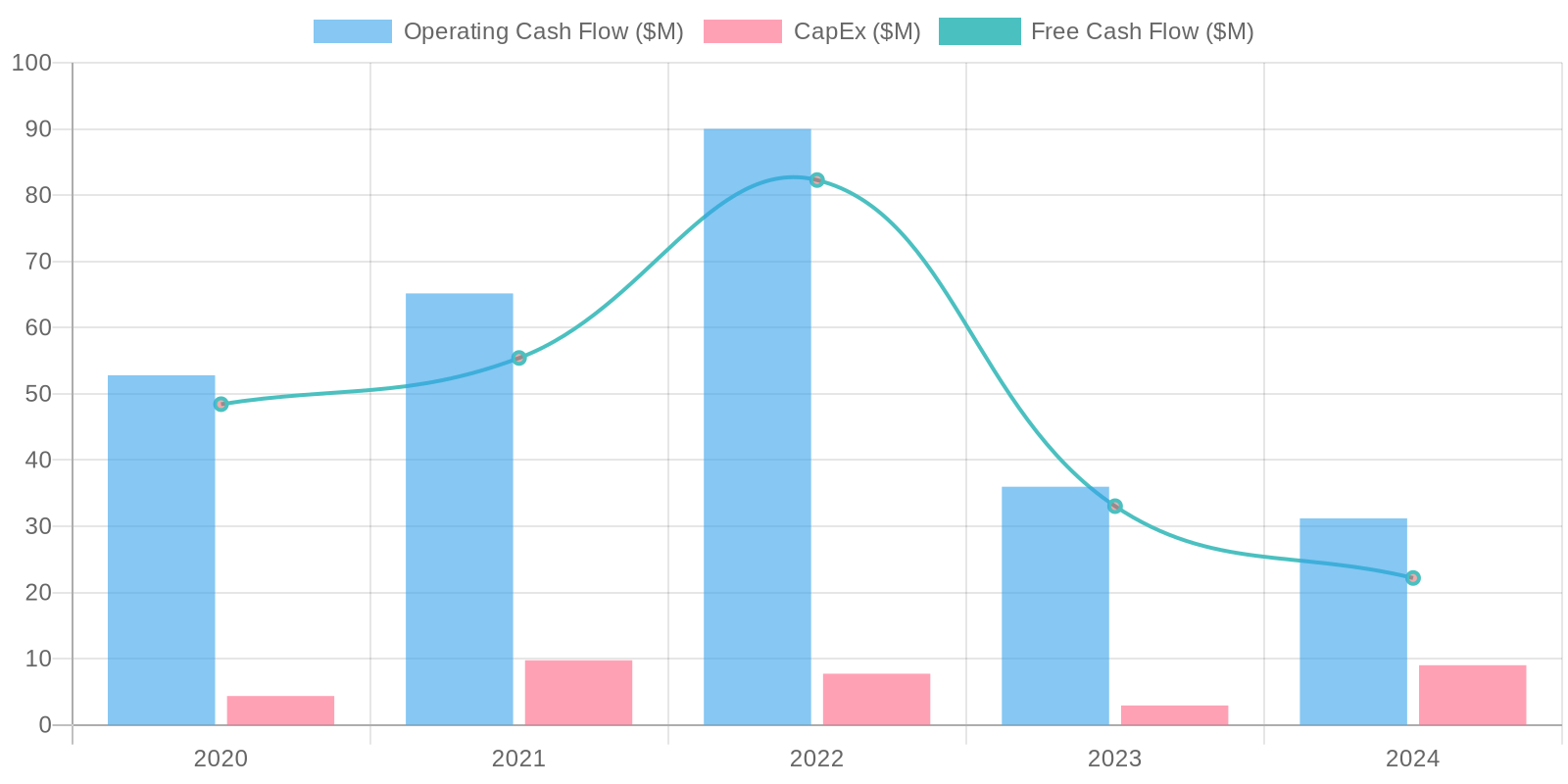

Cash Flow & Capital Efficiency

Jamf has exhibited fluctuating cash flow from operations, showing both positive and negative values. The company's free cash flow (FCF) has generally been positive in recent years, suggesting an ability to generate cash after capital expenditures. However, it is crucial to analyze how these cash flows are being utilized, particularly in light of the company's history of acquisitions and share repurchases. Any major swings in these categories would need further investigation.

Capital Efficiency (ROIC/ROE):

Given the consistent negative net income, Return on Invested Capital (ROIC) and Return on Equity (ROE) are negative, reflecting an inefficient use of capital. Specifically, the company isn't generating profits from its investments and equity. This could stem from a combination of factors, including substantial investments in growth initiatives, acquisitions, or operational inefficiencies. The negative profitability needs to be addressed to improve capital efficiency.

Balance Sheet Health:

Jamf's balance sheet reveals a substantial amount of debt, which, when compared to its cash reserves, results in a net debt position. While the company maintains a current ratio above one, indicating sufficient liquidity to cover short-term obligations, the high debt levels could pose a risk, especially given the company's history of negative net income. Furthermore, a significant portion of assets are tied up in goodwill and intangible assets, which may be subject to impairment if the company's performance does not improve.

5. Management & Governance

CEO Assessment: As of late 2023 and early 2024, Jamf is led by CEO Dean Hager. Assessments of his leadership generally focus on his ability to drive growth in the enterprise market while maintaining Jamf's strong position in the education sector. Key areas for evaluation include execution on strategic acquisitions (like Wandera), ability to navigate the complexities of a subscription-based model in a competitive market, and maintaining a strong company culture during periods of rapid growth and expansion.

Capital Allocation: Good

Insider Ownership: Insider ownership, encompassing executive officers and board members, is a relevant factor. Evaluate the percentage of shares held by insiders relative to the overall market capitalization. Significant insider ownership can align management's interests with those of shareholders, incentivizing long-term value creation. Conversely, very low insider ownership might raise concerns about the degree to which management is truly invested in the company's success. It needs to be checked whether insiders are buying or selling shares, as this can provide signals about management's confidence in Jamf's future prospects. Also if there were any insider trading scandals.

Governance Flags:

Related party transactions could be a potential concern., Executive compensation structure, should be aligned with long-term shareholder value creation, and not incentivize excessive risk-taking., Board Independence, the proportion of independent directors on the board and the presence of key committees (audit, compensation, nominating/governance) can all have an impact.

The DCF model projects future free cash flows based on the assumptions outlined. Revenue growth gradually decreases over the next 5 years to reflect a mature growth phase, and a perpetual growth rate of 2.5% is applied to calculate the terminal value. The discount rate (WACC) of 10% is used to discount the future cash flows to their present value. The present value of the projected free cash flows, plus the present value of the terminal value, results in an enterprise value. Net Debt is subtracted from the enterprise value to calculate the Equity Value. The Equity Value is then divided by the current shares outstanding to derive a fair value per share of $13.50. This represents a slight upside of 3.69% from the current market price, meaning JAMF is fairly valued with these assumptions. However, since the assumptions are sensitive to changes in economic outlook and company performance, it's important to acknowledge a potential downside risk. Given the volatility of growth stocks, a downside range of 20% is possible.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Jamf is significantly undervalued due to temporary macroeconomic headwinds and concerns about profitability.

As Apple's ecosystem continues to penetrate enterprise and education, Jamf's leading platform for managing and securing these devices will experience accelerated growth.

Margin expansion through operating leverage and successful cross-selling will drive significant earnings growth, leading to substantial stock appreciation. |

| Base | 13.5 | Jamf will continue to be the dominant player in Apple device management, experiencing solid revenue growth and gradual margin expansion.

The market will recognize the intrinsic value of its platform, leading to a moderate increase in its share price. |

| Bear | Low | Jamf fails to effectively compete against larger players like Microsoft, resulting in market share loss and decelerating revenue growth.

Continued operating losses erode investor confidence, and the company's high debt burden limits its ability to invest in growth initiatives.

This leads to a significant decline in the stock price. |

7. Risks

Jamf's consistent revenue growth is offset by persistent net losses, a high debt burden, and significant reliance on goodwill and intangible assets. Dependence on the Apple ecosystem presents a concentrated risk. These factors, combined with substantial stock-based compensation expense, raise concerns about long-term financial sustainability.

Red Flags:

Consistent negative net income despite revenue growth.

High levels of debt relative to cash reserves.

Significant portion of assets in goodwill and intangibles.

Fluctuations in cash flow from operations.

8. Conclusion

Jamf will continue to be the dominant player in Apple device management, experiencing solid revenue growth and gradual margin expansion.

The market will recognize the intrinsic value of its platform, leading to a moderate increase in its share price.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Given the consistent negative net income, Return on Invested Capital (ROIC) and Return on Equity (ROE) are negative, reflecting an inefficient use of capital. Specifically, the company isn't generating profits from its investments and equity. This could stem from a combination of factors, including substantial investments in growth initiatives, acquisitions, or operational inefficiencies. The negative profitability needs to be addressed to improve capital efficiency.

Given the consistent negative net income, Return on Invested Capital (ROIC) and Return on Equity (ROE) are negative, reflecting an inefficient use of capital. Specifically, the company isn't generating profits from its investments and equity. This could stem from a combination of factors, including substantial investments in growth initiatives, acquisitions, or operational inefficiencies. The negative profitability needs to be addressed to improve capital efficiency. Jamf has exhibited fluctuating cash flow from operations, showing both positive and negative values. The company's free cash flow (FCF) has generally been positive in recent years, suggesting an ability to generate cash after capital expenditures. However, it is crucial to analyze how these cash flows are being utilized, particularly in light of the company's history of acquisitions and share repurchases. Any major swings in these categories would need further investigation.

Jamf has exhibited fluctuating cash flow from operations, showing both positive and negative values. The company's free cash flow (FCF) has generally been positive in recent years, suggesting an ability to generate cash after capital expenditures. However, it is crucial to analyze how these cash flows are being utilized, particularly in light of the company's history of acquisitions and share repurchases. Any major swings in these categories would need further investigation.