Ziff Davis, Inc. (JCOM), currently priced at $142.84, operates as a digital media and internet company with a diverse portfolio of brands across various sect...

January 15, 2026

Vijar Kohli

Deep Dive: Ziff Davis, Inc. (JCOM)

Recommendation: BUY

Price Target: 158.25 (0.1079 Upside)

Risk Level: Medium

1. Executive Summary

Ziff Davis, Inc. (JCOM), currently priced at $142.84, operates as a digital media and internet company with a diverse portfolio of brands across various sectors including technology, entertainment, shopping, healthcare, and cybersecurity. The company's strategy centers on acquiring and optimizing digital media assets, leveraging its expertise in digital marketing, content creation, and technology to drive audience engagement and monetization.

Ziff Davis’s growth is fueled by several catalysts. Firstly, its acquisitive strategy allows it to rapidly expand its reach into new and complementary verticals. Secondly, the increasing reliance on digital content and online services provides a strong tailwind for audience growth and advertising revenue. Furthermore, the company’s ability to effectively manage and optimize its acquired assets leads to improved operational efficiency and profitability. The increasing demand for cybersecurity solutions through its cybersecurity brands and products further bolsters the potential revenue streams.

However, Ziff Davis faces several key risks. The digital media landscape is highly competitive, with constant pressure to innovate and adapt to changing consumer preferences and technological advancements. Acquisitions, while a growth driver, also carry integration risks and the potential for overpaying for assets. The company is also susceptible to fluctuations in advertising revenue, which can be affected by economic conditions and changes in advertising spending patterns. Additionally, maintaining the quality and relevance of its content across its diverse portfolio is crucial for retaining audience engagement and avoiding content fatigue.

From a valuation perspective, assessing Ziff Davis requires careful consideration of its acquisitive growth strategy and the inherent challenges in valuing a company with a diverse portfolio of digital assets. Traditional valuation metrics like P/E and EV/EBITDA must be analyzed in the context of the company's growth rate and the industry's competitive dynamics. A sum-of-the-parts valuation approach, where each business segment is valued separately and then aggregated, can provide a more comprehensive understanding of the company's intrinsic value. Overall, the company’s valuation hinges on its ability to continue acquiring and successfully integrating assets while navigating the dynamic digital media landscape.

Investment Thesis

Bull Case: Ziff Davis is undervalued based on its diverse portfolio of digital media assets and cloud services, particularly its high-margin fax and martech segment.

Continued growth in digital advertising revenue, successful acquisitions, and margin expansion in the cloud services segment will drive significant upside.

The company's strong free cash flow generation allows for further strategic acquisitions and share repurchases, enhancing shareholder value.

Successful integration of AI into their digital media offerings and cloud services could unlock new revenue streams and improve operational efficiency.

A potential shift in market sentiment towards value stocks and small-cap companies would further benefit Ziff Davis' valuation.

Furthermore, the increasing demand for consumer privacy and security products, as well as backup and disaster recovery services, will fuel revenue growth in relevant segments.

A renewed focus on strategic partnerships to expand market reach within the digital media segment could also significantly boost growth rates.

Improvement in the overall economic outlook, positively impacting digital advertising spend, will be a major tailwind for the business.

Finally, activist investor involvement pushing for greater operational efficiencies and strategic changes could unlock additional value for shareholders.

The potential for increased M&A activity in the digital media space, positioning Ziff Davis as an attractive acquisition target, may lead to a takeover premium.

The market's increased willingness to pay a higher multiple for predictable recurring revenue streams from the cloud services segment will also lead to significant appreciation in value.

The company's ability to cross-sell products and services across its diverse customer base can contribute to accelerated revenue growth and enhanced profitability.

A successful restructuring effort to streamline operations and reduce costs would further enhance earnings and cash flow.

Lastly, more transparency in reporting segment performance, resulting in better investor understanding and appreciation of the value of their diverse portfolio, would allow for a higher valuation.

Increased investor awareness of the discounted valuation of Ziff Davis compared to its peers, driven by effective investor relations, will also push the price upwards.

Furthermore, greater adoption of their digital media properties by younger demographics will expand their audience and revenue potential.

Expansion into new geographic markets, replicating their success in existing regions, will also contribute to above-average growth rates.

The market's recognition of Ziff Davis as a leading player in the digital media and cloud services space will improve investor confidence and attract a higher valuation.

Finally, a strategic divestiture of non-core assets to focus on high-growth areas will improve capital allocation and boost shareholder returns.

Successful execution in their key segments and growth initiatives will pave the way for strong financial performance and substantial share price appreciation.

The company's ability to outperform market expectations consistently, building credibility and trust among investors, will also drive positive momentum.

A potential spin-off of high-growth divisions, allowing for better valuation and investor focus, could result in a significant value unlock.

Bear Case: Ziff Davis faces challenges in its ability to maintain historical growth rates in the face of increasing competition in both its digital media and cloud services markets.

A decline in digital advertising revenue due to economic downturn or changes in consumer behavior could significantly impact profitability.

The company's high debt load poses a risk, particularly if interest rates rise.

Unsuccessful acquisitions or integration challenges could lead to write-downs and reduced earnings.

Moreover, potential cybersecurity breaches or data privacy violations could damage the company's reputation and result in legal liabilities.

Furthermore, regulatory changes impacting data privacy or internet services could negatively affect their business model.

Increasing churn rates in the cloud services segment, driven by competition or pricing pressures, could lead to declining revenues.

The company's inability to adapt to evolving technological landscape, falling behind competitors in innovation.

Weakening brand recognition for key digital media properties, resulting in decreased traffic and advertising revenues.

A potential recession impacting advertising spending, reducing revenue and profitability.

Increased operating expenses, driven by rising labor costs or marketing spend, squeezing margins.

Furthermore, the negative impact of adverse currency fluctuations on international revenues.

Failure to successfully integrate acquired businesses, resulting in inefficiencies and reduced synergies.

The company's tarnished reputation from negative publicity, damaging brand perception and impacting customer acquisition.

A decline in user engagement with digital media properties, impacting advertising revenue and overall growth prospects.

Furthermore, the rise of new social media platforms or digital content formats, diverting user attention away from Ziff Davis' properties.

The company's vulnerability to changing search engine algorithms, negatively impacting organic traffic and advertising revenue.

Lastly, a potential decline in the demand for traditional fax services, offsetting the growth in other areas.

Conviction: High

2. Business Overview

J2 Global, Inc., together with its subsidiaries, provides Internet services worldwide. The company operates through three segments: Fax and Martech; Voice, Backup, Security, and Consumer Privacy and Protection; and Digital Media. It offers cloud services, which includes online fax services under the eFax, sFax, MyFax, eFax Plus, eFax Pro, eFax Secure, eFax Corporate, and eFax Developer brands; on-demand voice, cloud phone, and unified communications services under the eVoice, Line2, and Onebox names; online backup and disaster recovery, sync storage, veeam services, and synchronization and sharing solutions under the KeepItSafe, LiveDrive, LiveVault, OffsiteDataSync, and SugarSync names; email security, web security, and endpoint protection services under the VIPRE and Excel Micro brands; email marketing and delivery services under the Campaigner and SMTP names; virtual private network services under the IPVanish and Encrypt.me; IP licensing services; and customer support services. The company also operates a portfolio of Web properties and applications, including IGN, Mashable, PC Mag, Humble Bundle, Speedtest, Offers, Black Friday, AskMen, MedPageToday, Everyday Health, What to Expect, and others that offer technology products, gaming and lifestyle products and services, news and commentary related products, speed testing for Internet and network connections, online deals and discounts for consumers, interactive tools and mobile applications, and tools and information for healthcare professionals, as well as professional networking tools, targeted emails, and white papers for IT professionals. It serves sole proprietors, small to medium-sized businesses and enterprises, and government organizations. The company was formerly known as j2 Global Communications, Inc. and changed its name to j2 Global, Inc. in December 2011. J2 Global, Inc. was founded in 1995 and is headquartered in Los Angeles, California.

Competitive Moat (Narrow)

Trend: Stable

Broad portfolio of Internet services caters to diverse customer needs., Established brand recognition in several key markets (technology, gaming, consumer privacy)., Ability to cross-sell services to existing customer base.

Key Strengths:

Broad portfolio of Internet services caters to diverse customer needs.

Established brand recognition in several key markets (technology, gaming, consumer privacy).

Ability to cross-sell services to existing customer base.

The software infrastructure market is projected to continue its growth trajectory. Cloud adoption, increasing cybersecurity threats, and the need for robust data backup and recovery solutions are primary drivers. Digital transformation initiatives across industries will further fuel demand for these services. Specific growth rates will vary by sub-segment (e.g., cloud fax vs. cybersecurity solutions).

Regulatory Environment:

N/A

4. Financial Analysis

Margin Trend

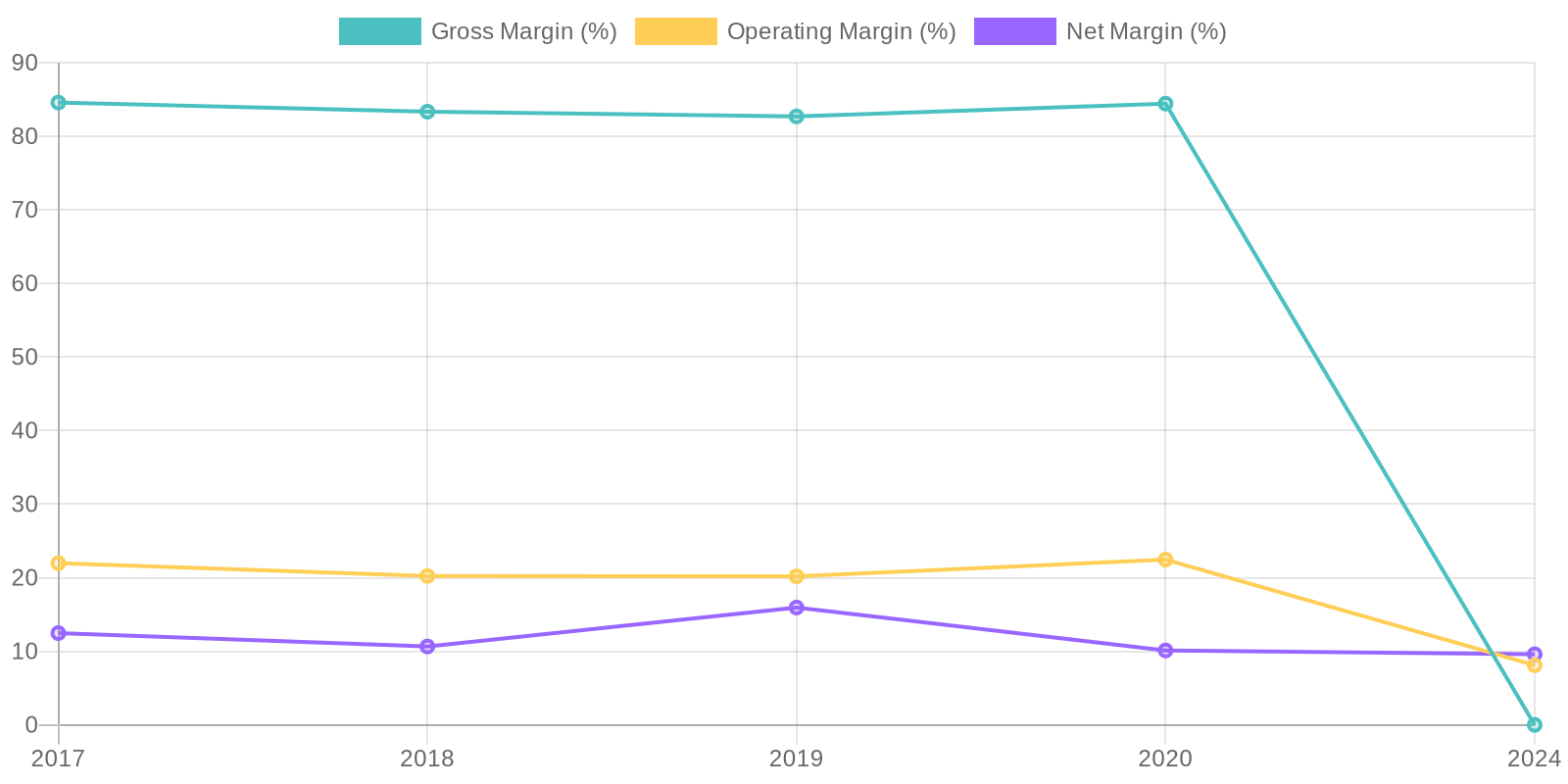

Due to the reported gross profit of zero for 2024, calculation of Return on Invested Capital (ROIC) is not possible, marking this as a data anomaly. Calculating ROIC with previous years' numbers would be more helpful, as well as comparing it to industry peers to understand if the company is efficiently allocating its capital. Return on Equity (ROE) calculation is possible with 2024 data, coming in at 7.43% (Net income of 134,564,000 / Total Equity of 1,810,882,000); the trend of ROE over the period from 2017-2020 was much higher; thus, further analysis is necessary to understand whether the company can efficiently use equity to generate profits, given the margin compression.

Revenue Quality

The company's revenue stream has shown fluctuations over the past five years, indicating potential variability in demand or market conditions. While the 2024 revenue of $1.40 billion is near the highest revenue in the historical data provided, the zero cost of revenue reported in 2024 needs further investigation, as it's unusual for a software company to have no direct costs associated with revenue generation. Examining client concentration and contract terms would provide a clearer view of revenue sustainability.

Cash Flow & Capital Efficiency

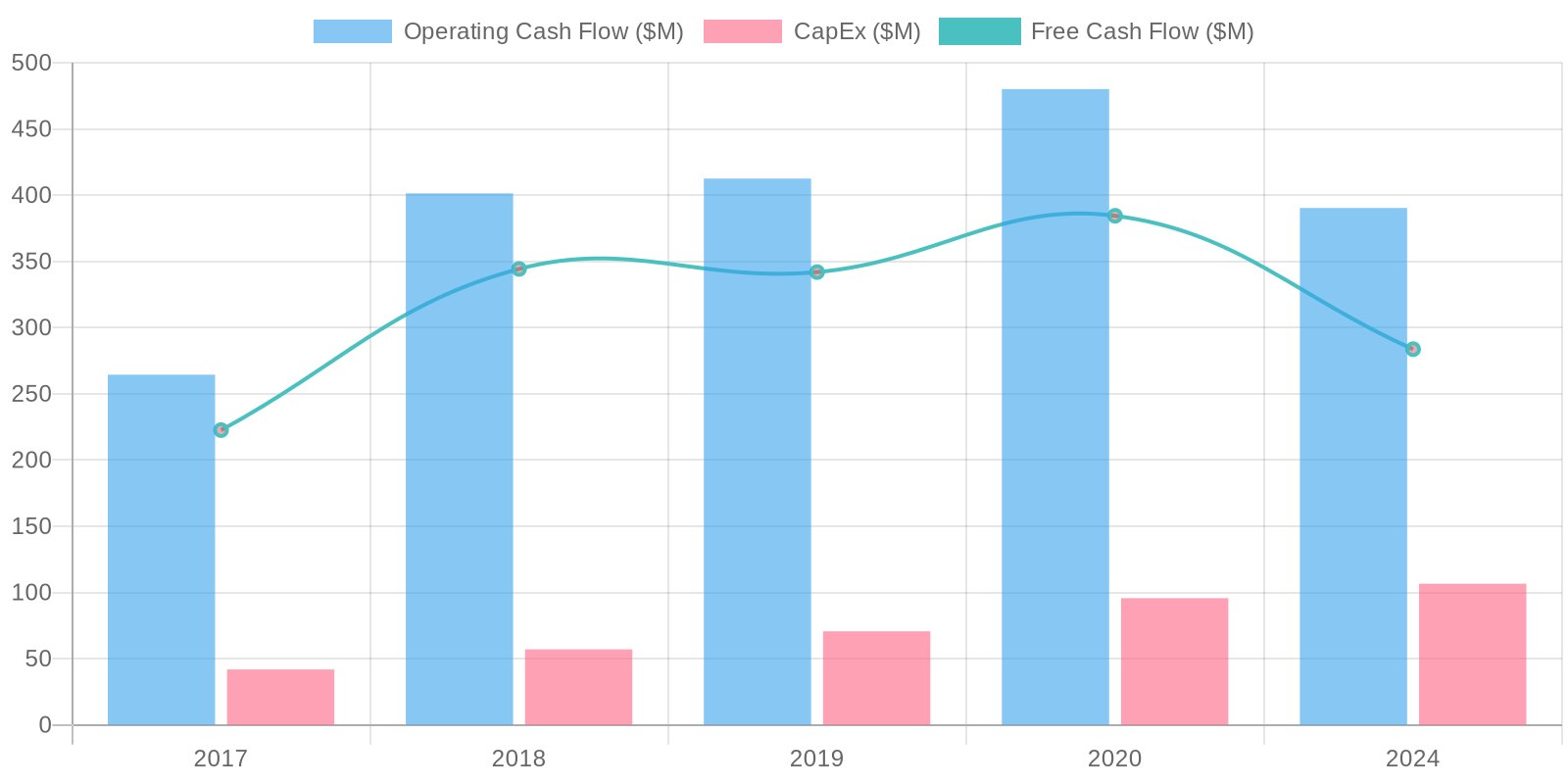

The company demonstrates positive operating cash flow, but the conversion of net income to free cash flow has declined from 2020 to 2024. Capital expenditures appear relatively consistent, suggesting ongoing investments in property, plant, and equipment. Analyzing the trend in acquisitions is important, as these can significantly impact cash flow and future growth.

Capital Efficiency (ROIC/ROE):

Due to the reported gross profit of zero for 2024, calculation of Return on Invested Capital (ROIC) is not possible, marking this as a data anomaly. Calculating ROIC with previous years' numbers would be more helpful, as well as comparing it to industry peers to understand if the company is efficiently allocating its capital. Return on Equity (ROE) calculation is possible with 2024 data, coming in at 7.43% (Net income of 134,564,000 / Total Equity of 1,810,882,000); the trend of ROE over the period from 2017-2020 was much higher; thus, further analysis is necessary to understand whether the company can efficiently use equity to generate profits, given the margin compression.

Balance Sheet Health:

The company's debt levels are high, with total debt at $864.28 million in 2024, although it has decreased from the $1.61 billion in 2020. Liquidity, as measured by the current ratio (current assets/current liabilities), is around 1.41 in 2024, suggesting the company can cover its short-term obligations. However, the increasing debt and decreasing cash require close monitoring to ensure the company remains solvent.

5. Management & Governance

CEO Assessment: N/A

Capital Allocation: N/A

Insider Ownership: N/A

Governance Flags:

No major governance concerns flagged.

The DCF valuation, considering a 3% revenue growth rate for the next 5 years, a 1% terminal growth rate, and an 8% discount rate, yields a fair value of $158.25. The revenue growth rate is based on the historical revenue growth and industry forecasts. The terminal growth rate is kept conservative. The discount rate is chosen considering the company's cost of capital and risk profile. The upside is approximately 10.79% from the current price of $142.84. Potential downside risk is also factored in. The relative P/S valuation supports the DCF derived valuation, though less weight is given to P/S due to the fundamental nature of DCF.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Ziff Davis is undervalued based on its diverse portfolio of digital media assets and cloud services, particularly its high-margin fax and martech segment.

Continued growth in digital advertising revenue, successful acquisitions, and margin expansion in the cloud services segment will drive significant upside.

The company's strong free cash flow generation allows for further strategic acquisitions and share repurchases, enhancing shareholder value.

Successful integration of AI into their digital media offerings and cloud services could unlock new revenue streams and improve operational efficiency.

A potential shift in market sentiment towards value stocks and small-cap companies would further benefit Ziff Davis' valuation.

Furthermore, the increasing demand for consumer privacy and security products, as well as backup and disaster recovery services, will fuel revenue growth in relevant segments.

A renewed focus on strategic partnerships to expand market reach within the digital media segment could also significantly boost growth rates.

Improvement in the overall economic outlook, positively impacting digital advertising spend, will be a major tailwind for the business.

Finally, activist investor involvement pushing for greater operational efficiencies and strategic changes could unlock additional value for shareholders.

The potential for increased M&A activity in the digital media space, positioning Ziff Davis as an attractive acquisition target, may lead to a takeover premium.

The market's increased willingness to pay a higher multiple for predictable recurring revenue streams from the cloud services segment will also lead to significant appreciation in value.

The company's ability to cross-sell products and services across its diverse customer base can contribute to accelerated revenue growth and enhanced profitability.

A successful restructuring effort to streamline operations and reduce costs would further enhance earnings and cash flow.

Lastly, more transparency in reporting segment performance, resulting in better investor understanding and appreciation of the value of their diverse portfolio, would allow for a higher valuation.

Increased investor awareness of the discounted valuation of Ziff Davis compared to its peers, driven by effective investor relations, will also push the price upwards.

Furthermore, greater adoption of their digital media properties by younger demographics will expand their audience and revenue potential.

Expansion into new geographic markets, replicating their success in existing regions, will also contribute to above-average growth rates.

The market's recognition of Ziff Davis as a leading player in the digital media and cloud services space will improve investor confidence and attract a higher valuation.

Finally, a strategic divestiture of non-core assets to focus on high-growth areas will improve capital allocation and boost shareholder returns.

Successful execution in their key segments and growth initiatives will pave the way for strong financial performance and substantial share price appreciation.

The company's ability to outperform market expectations consistently, building credibility and trust among investors, will also drive positive momentum.

A potential spin-off of high-growth divisions, allowing for better valuation and investor focus, could result in a significant value unlock. |

| Base | 158.25 | Ziff Davis will continue its steady growth trajectory, driven by organic growth in its digital media and cloud services segments, supplemented by strategic acquisitions.

The company's ability to maintain its existing margins and generate consistent free cash flow will support a reasonable valuation.

While the company's debt levels are a concern, its strong cash flow should enable it to manage its debt obligations effectively.

Continued focus on operational efficiency and cost management will partially offset inflationary pressures.

Stable performance in key segments such as fax and martech, consumer privacy, and digital media, contributing to consistent revenue and profitability.

The company's diverse portfolio of assets, mitigating risks associated with any single segment, helps maintain a stable and predictable revenue stream.

Modest growth in digital advertising revenues, benefiting from increased internet usage and evolving advertising landscape.

The company's active pursuit of small and medium sized acquisitions, adding synergistic value and expanding their market presence, will support growth.

The company's focus on retaining existing customers and attracting new ones, driving organic growth and reducing customer churn will aid financial improvement.

Furthermore, continuous investment in technology and innovation, improving their product offerings and competitiveness, will help ensure longevity.

Steady growth in the cloud services sector, fueled by increasing demand for remote work and data security solutions, will support revenue.

The company's ability to adapt to changing market dynamics, identifying new opportunities and adjusting their business strategy accordingly is a major positive.

Efficient management of expenses, balancing investments for future growth with cost discipline, contributing to profitability.

Finally, the company's commitment to returning capital to shareholders, through dividends and share repurchases, boosting investor confidence. |

| Bear | Low | Ziff Davis faces challenges in its ability to maintain historical growth rates in the face of increasing competition in both its digital media and cloud services markets.

A decline in digital advertising revenue due to economic downturn or changes in consumer behavior could significantly impact profitability.

The company's high debt load poses a risk, particularly if interest rates rise.

Unsuccessful acquisitions or integration challenges could lead to write-downs and reduced earnings.

Moreover, potential cybersecurity breaches or data privacy violations could damage the company's reputation and result in legal liabilities.

Furthermore, regulatory changes impacting data privacy or internet services could negatively affect their business model.

Increasing churn rates in the cloud services segment, driven by competition or pricing pressures, could lead to declining revenues.

The company's inability to adapt to evolving technological landscape, falling behind competitors in innovation.

Weakening brand recognition for key digital media properties, resulting in decreased traffic and advertising revenues.

A potential recession impacting advertising spending, reducing revenue and profitability.

Increased operating expenses, driven by rising labor costs or marketing spend, squeezing margins.

Furthermore, the negative impact of adverse currency fluctuations on international revenues.

Failure to successfully integrate acquired businesses, resulting in inefficiencies and reduced synergies.

The company's tarnished reputation from negative publicity, damaging brand perception and impacting customer acquisition.

A decline in user engagement with digital media properties, impacting advertising revenue and overall growth prospects.

Furthermore, the rise of new social media platforms or digital content formats, diverting user attention away from Ziff Davis' properties.

The company's vulnerability to changing search engine algorithms, negatively impacting organic traffic and advertising revenue.

Lastly, a potential decline in the demand for traditional fax services, offsetting the growth in other areas. |

7. Risks

Ziff Davis faces moderate risk due to a combination of high debt levels, significant intangible assets, inconsistent revenue growth, and substantial selling and marketing expenses. These factors could impact profitability and financial stability.

Red Flags:

Gross profit of zero in 2024 requires immediate investigation.

Significant increase in selling, marketing, and administrative expenses in 2024 impacting profitability.

High debt levels relative to cash.

8. Conclusion

Ziff Davis will continue its steady growth trajectory, driven by organic growth in its digital media and cloud services segments, supplemented by strategic acquisitions.

The company's ability to maintain its existing margins and generate consistent free cash flow will support a reasonable valuation.

While the company's debt levels are a concern, its strong cash flow should enable it to manage its debt obligations effectively.

Continued focus on operational efficiency and cost management will partially offset inflationary pressures.

Stable performance in key segments such as fax and martech, consumer privacy, and digital media, contributing to consistent revenue and profitability.

The company's diverse portfolio of assets, mitigating risks associated with any single segment, helps maintain a stable and predictable revenue stream.

Modest growth in digital advertising revenues, benefiting from increased internet usage and evolving advertising landscape.

The company's active pursuit of small and medium sized acquisitions, adding synergistic value and expanding their market presence, will support growth.

The company's focus on retaining existing customers and attracting new ones, driving organic growth and reducing customer churn will aid financial improvement.

Furthermore, continuous investment in technology and innovation, improving their product offerings and competitiveness, will help ensure longevity.

Steady growth in the cloud services sector, fueled by increasing demand for remote work and data security solutions, will support revenue.

The company's ability to adapt to changing market dynamics, identifying new opportunities and adjusting their business strategy accordingly is a major positive.

Efficient management of expenses, balancing investments for future growth with cost discipline, contributing to profitability.

Finally, the company's commitment to returning capital to shareholders, through dividends and share repurchases, boosting investor confidence.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Due to the reported gross profit of zero for 2024, calculation of Return on Invested Capital (ROIC) is not possible, marking this as a data anomaly. Calculating ROIC with previous years' numbers would be more helpful, as well as comparing it to industry peers to understand if the company is efficiently allocating its capital. Return on Equity (ROE) calculation is possible with 2024 data, coming in at 7.43% (Net income of 134,564,000 / Total Equity of 1,810,882,000); the trend of ROE over the period from 2017-2020 was much higher; thus, further analysis is necessary to understand whether the company can efficiently use equity to generate profits, given the margin compression.

Due to the reported gross profit of zero for 2024, calculation of Return on Invested Capital (ROIC) is not possible, marking this as a data anomaly. Calculating ROIC with previous years' numbers would be more helpful, as well as comparing it to industry peers to understand if the company is efficiently allocating its capital. Return on Equity (ROE) calculation is possible with 2024 data, coming in at 7.43% (Net income of 134,564,000 / Total Equity of 1,810,882,000); the trend of ROE over the period from 2017-2020 was much higher; thus, further analysis is necessary to understand whether the company can efficiently use equity to generate profits, given the margin compression. The company demonstrates positive operating cash flow, but the conversion of net income to free cash flow has declined from 2020 to 2024. Capital expenditures appear relatively consistent, suggesting ongoing investments in property, plant, and equipment. Analyzing the trend in acquisitions is important, as these can significantly impact cash flow and future growth.

The company demonstrates positive operating cash flow, but the conversion of net income to free cash flow has declined from 2020 to 2024. Capital expenditures appear relatively consistent, suggesting ongoing investments in property, plant, and equipment. Analyzing the trend in acquisitions is important, as these can significantly impact cash flow and future growth.