monday.com Ltd. (MNDY), currently trading at $132.81, operates in the work management software space, offering a cloud-based platform designed to enhance tea...

January 15, 2026

Vijar Kohli

Deep Dive: monday.com Ltd. (MNDY)

Recommendation: BUY

Price Target: 141.45 (0.065 Upside)

Risk Level: Medium

1. Executive Summary

monday.com Ltd. (MNDY), currently trading at $132.81, operates in the work management software space, offering a cloud-based platform designed to enhance team collaboration and project management. Its current market position is characterized by rapid growth, driven by its user-friendly interface, extensive customization options, and broad applicability across various industries. The company has successfully penetrated a large addressable market, attracting both small and large enterprises seeking to improve their operational efficiency.

Growth catalysts for monday.com include continued expansion into new markets, development of new product features and integrations, and an increasing shift towards digital transformation across industries. The company is actively investing in its sales and marketing efforts to acquire new customers and expand its presence in existing accounts. Furthermore, strategic partnerships and acquisitions could further accelerate growth and expand its product offerings.

Key risks facing monday.com include increasing competition from established players like Asana, Smartsheet, and Microsoft Project, as well as potential economic downturns that could impact customer spending on software solutions. The company's relatively high valuation also makes it vulnerable to market corrections and any slowdown in its growth trajectory. Execution risk associated with product development and market expansion also remains a concern.

Valuation summary: monday.com currently trades at a premium valuation relative to its peers, reflecting its high growth rate and strong market position. This premium is justified by its superior revenue growth and potential for further expansion, but also implies higher expectations for future performance. A detailed valuation analysis should consider factors such as long-term growth rates, profitability, and discount rates to determine whether the current market price accurately reflects the company's intrinsic value.

Investment Thesis

Bull Case: monday.com is poised to benefit significantly from the increasing demand for collaborative work management solutions. Its Work OS platform's flexibility and customization options cater to diverse industries and company sizes, driving strong user adoption and retention. Continued innovation in AI-powered features and expansion into new markets will fuel revenue growth and profitability, exceeding current market expectations. monday.com's robust balance sheet and efficient FCF generation support aggressive growth initiatives and potential acquisitions, further solidifying its market leadership. Operating leverage improves significantly as revenue scales, leading to margin expansion and substantial earnings growth, justifying a premium valuation. The shift towards remote and hybrid work environments is a long-term tailwind that will continue to drive demand for monday.com's solutions. The company can successfully cross-sell and up-sell to its existing customer base, increasing average revenue per user (ARPU) and lifetime value (LTV). Positive analyst coverage and strong earnings reports drive investor sentiment and multiple expansion for the stock price, outpacing its peers in the SaaS space. Furthermore, it can become a compelling acquisition target for larger software enterprises looking to incorporate a leading work management platform into their portfolio. Significant margin expansion and increased earnings visibility drives re-rating by the market pushing the valuation multiples higher with an expectation of strong long-term growth. Strong expansion in the Enterprise segment exceeding expectations should drive significant revenue growth and profitability improvements. Strategic partnerships with major technology players enhance distribution channels and market reach, resulting in accelerating growth rates. Higher than expected renewal rates and customer cohort performance demonstrate the stickiness of the platform and its enduring value to clients. The company's ability to maintain a high Net Revenue Retention rate while adding new customers points to a strong competitive advantage in the work management space. monday.com is exceptionally well-positioned to capitalize on the digitization of work processes across various industries, leading to sustained high growth and creating substantial value for shareholders. The ongoing investments in AI and machine learning capabilities should enable the company to offer more personalized and intelligent solutions, leading to increased customer satisfaction and higher adoption rates. The strong corporate culture fosters innovation and attracts top talent, which will be instrumental in driving future product development and maintaining a competitive edge. monday.com's ability to integrate with other widely-used business applications provides a seamless experience for users, enhancing the platform's overall value and increasing customer loyalty. Focus on user experience and intuitive design is a key differentiator from competitors, driving organic growth and positive word-of-mouth referrals. Successful implementation of aggressive sales and marketing strategies in new geographies accelerates global expansion and revenue diversification. Continuous improvements in customer support and onboarding processes improve customer satisfaction and reduce churn, resulting in higher LTV. Furthermore, increased focus on data security and privacy measures strengthens customer trust and compliance, making the platform more appealing to enterprise clients. Continued investments in the platform's scalability and reliability ensure that it can handle the growing demands of its user base without compromising performance or availability. monday.com is establishing a robust ecosystem of third-party developers and partners, expanding the platform's functionality and creating new revenue opportunities. Successful market entry into new verticals (e.g., healthcare, government) broadens the addressable market and further accelerates revenue growth. Enhanced reporting and analytics capabilities provide valuable insights to users, increasing the platform's utility and driving higher engagement. Expansion of the monday.com marketplace with additional apps and integrations enhances the platform's value proposition and attracts a wider range of users. The company's strong brand reputation and positive customer reviews drive organic growth and reduce customer acquisition costs. Continued focus on innovation and customer satisfaction ensures monday.com remains at the forefront of the work management space, driving long-term value creation for shareholders. The company’s investments in improving user interface and design further cements its position as the leading work management solution in the market. Increased investments in upskilling its workforce enhances its ability to drive innovation and respond quickly to changing market conditions. Strategic acquisitions of complementary technologies should strengthen monday.com’s product offerings and competitive position. The company’s demonstrated ability to effectively manage expenses while growing revenue points to a strong and sustainable business model. The long-term trend towards greater workplace flexibility and digital collaboration will continue to fuel growth and adoption of monday.com's platform. Sustained investments in R&D will result in innovative solutions that address the evolving needs of businesses and further differentiate monday.com from its competitors. Finally, monday.com is extremely well-positioned to capture significant market share in the burgeoning market for work management solutions, which has the potential to deliver outstanding returns to its investors in the long run. The company is set to revolutionize work processes and to change how teams collaborate and manage projects across the globe. By streamlining workflows and fostering transparency, monday.com can become an indispensable tool for businesses seeking to enhance productivity, improve communication, and achieve better results. The management team’s vision and strategic acumen should further catapult the company to new heights, cementing its position as a leader in the SaaS industry. With the continued focus on the customer, monday.com is set to become a key partner for businesses of all sizes, providing the tools and insights they need to thrive in today’s fast-paced and dynamic work environment. The positive feedback from users, the increasing analyst recommendations, and the company’s strong performance are indicative of the tremendous potential that lies ahead. Therefore, investing in monday.com should allow investors to take part in this exciting growth story and to reap substantial benefits over the long term. The continued success of its land-and-expand model proves that the company can steadily increase its presence within organizations, driving sustained long-term growth. The constant push for product innovation and the responsiveness to customer feedback are key drivers for long-term growth. The development of an effective partner program helps to scale sales and support efforts, accelerating the expansion of its market reach. The company's commitment to data privacy and compliance increases its appeal to larger enterprises, adding a layer of sustainability to the business model. The ongoing refinement of its pricing strategy balances the need for competitive positioning with the opportunity to improve monetization. By empowering teams to work more efficiently and effectively, monday.com can continue to make a significant impact on the way businesses operate and to create lasting value for shareholders. The successful establishment of a vibrant community of users and developers fosters innovation and collaboration. Furthermore, monday.com is extremely well-positioned to profit from the worldwide increase in digital transformations and to change the way people work all over the world. The platform should become an essential component of the digital toolkit for businesses of all sizes because of its emphasis on flexibility, user-friendliness, and scalability. The leadership team's dedication to sustainable development and environmental responsibility is in line with shifting customer expectations and improves the appeal of the business to a larger group of stakeholders. The platform's strong security features and regulatory compliance alleviate concerns among enterprise customers and drive greater adoption rates. The constant integration of new features and improvements guarantees that monday.com will continue to be on the cutting edge of work management technology and will be able to address the changing demands of its clientele. Finally, the company’s strong brand equity and reputation should solidify its position as a top provider of work management solutions and should lead to substantial, long-lasting shareholder value, setting it up for future success and dominance in the SaaS industry, making it a must-have in any growth-focused portfolio.

Catalysts: Successful product launches, larger enterprise deals, and positive economic trends are some of the catalysts that may drive performance.

Key Points: Expansion of the Enterprise segment exceeding expectations.

Target Return: 30% annually over the next 5 years on average, assuming the business continues to execute well. At the current price, and given strong momentum, monday.com is on track to continue its high growth trajectory.

Bear Case: monday.com faces significant challenges from increased competition in the work management software market, leading to slower user growth and pricing pressure. Inability to effectively scale its sales and marketing efforts results in higher customer acquisition costs and reduced profitability. Economic downturns negatively impact IT spending, affecting monday.com's revenue and growth prospects. The company struggles to innovate and differentiate its product offering, losing market share to competitors with more advanced features. Integration issues with other popular business applications hinder adoption and customer satisfaction. Data breaches or security vulnerabilities erode customer trust and result in significant financial and reputational damage. High customer churn due to poor customer support or lack of perceived value impacts recurring revenue and long-term growth. Changes in data privacy regulations increase compliance costs and limit the company's ability to effectively target and acquire new customers. Furthermore, monday.com experiences challenges in managing its operating expenses, leading to lower profitability than expected. The business is unable to effectively upsell or cross-sell its products to existing customers, resulting in lower average revenue per user. Increasing competition in the SaaS market drives up marketing costs. Management team makes poor strategic decisions. The business is unable to adapt quickly to changing customer needs. Economic downturn reduces enterprise IT spending leading to higher churn and lower customer acquisition. Inability to maintain high customer satisfaction due to poor customer service results in lower renewals. Lack of investments in R&D puts monday.com behind competitors and reduces innovation. Failure to expand into new markets and verticals hinders revenue diversification. Difficulties in managing data security and compliance issues reduces trust. Overall, failure to compete effectively in a fast-evolving SaaS market impacts long-term prospects, with the potential for stagnation or decline, leaving the business struggling in a competitive field, with poor execution and resulting in loss of value to shareholders.

Risks: Intense competition, economic downturns, and inability to innovate are some risks that may impact the business.

Key Points: Increased competition in the SaaS market drives up marketing costs.

Potential Loss: 50% or more, if execution falters significantly or competition intensifies.

Conviction: High

2. Business Overview

monday.com Ltd., together with its subsidiaries, develops software applications in the United States, Europe, the Middle East, Africa, and internationally. It provides Work OS, a cloud-based visual work operating system that consists of modular building blocks used and assembled to create software applications and work management tools. The company also offers product solutions for marketing, CRM, project management, software development, and other fields; and business development, presale, and customer success services. It serves organizations, educational or government institution, and distinct business unit of an organization. The company was formerly known as DaPulse Labs Ltd. and changed its name to monday.com Ltd. in November 2017. monday.com Ltd. was incorporated in 2012 and is headquartered in Tel Aviv-Yafo, Israel.

Competitive Moat (Narrow)

Trend: Stable

User-friendly interface and customizable platform, Strong brand recognition and marketing, Growing ecosystem of integrations, Flexibility catering to various use cases (marketing, CRM, project management, etc.)

Key Strengths:

User-friendly interface and customizable platform

Strong brand recognition and marketing

Growing ecosystem of integrations

Flexibility catering to various use cases (marketing, CRM, project management, etc.)

The application software market is projected to continue growing at a healthy rate, driven by factors such as increasing cloud adoption, digital transformation initiatives across industries, the growing need for automation, and the increasing demand for specialized software solutions. Mobile applications, AI-powered applications, and low-code/no-code platforms are also expected to fuel growth.

Regulatory Environment:

N/A

4. Financial Analysis

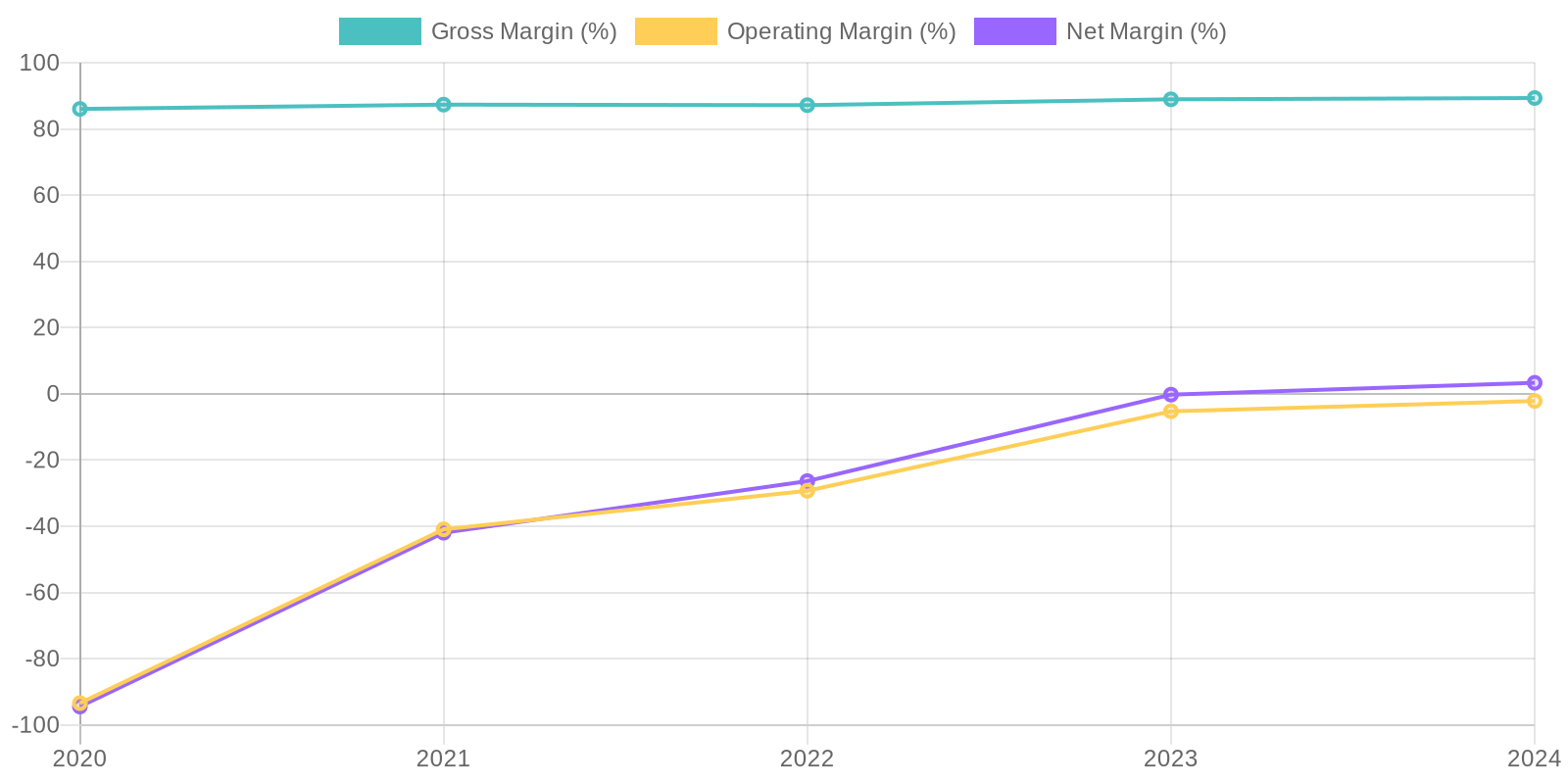

Margin Trend

It's challenging to provide a precise ROIC calculation without knowing the company's invested capital beyond the provided data. However, the trend of improving profitability suggests a potentially increasing ROIC. Similarly, ROE, which considers net income relative to shareholder equity, is showing improvement, as the company transitions from negative to positive net income while shareholder equity remains positive, signaling better utilization of equity for generating profits.

Revenue Quality

The company has shown consistent revenue growth over the past five years, indicating a strengthening market presence. The transition from negative net income to positive net income, suggests the company's revenue growth is becoming more efficient. Further investigation into the proportion of recurring revenue versus one-time sales is needed to fully assess sustainability, as well as analysis of customer concentration to evaluate dependence on key clients.

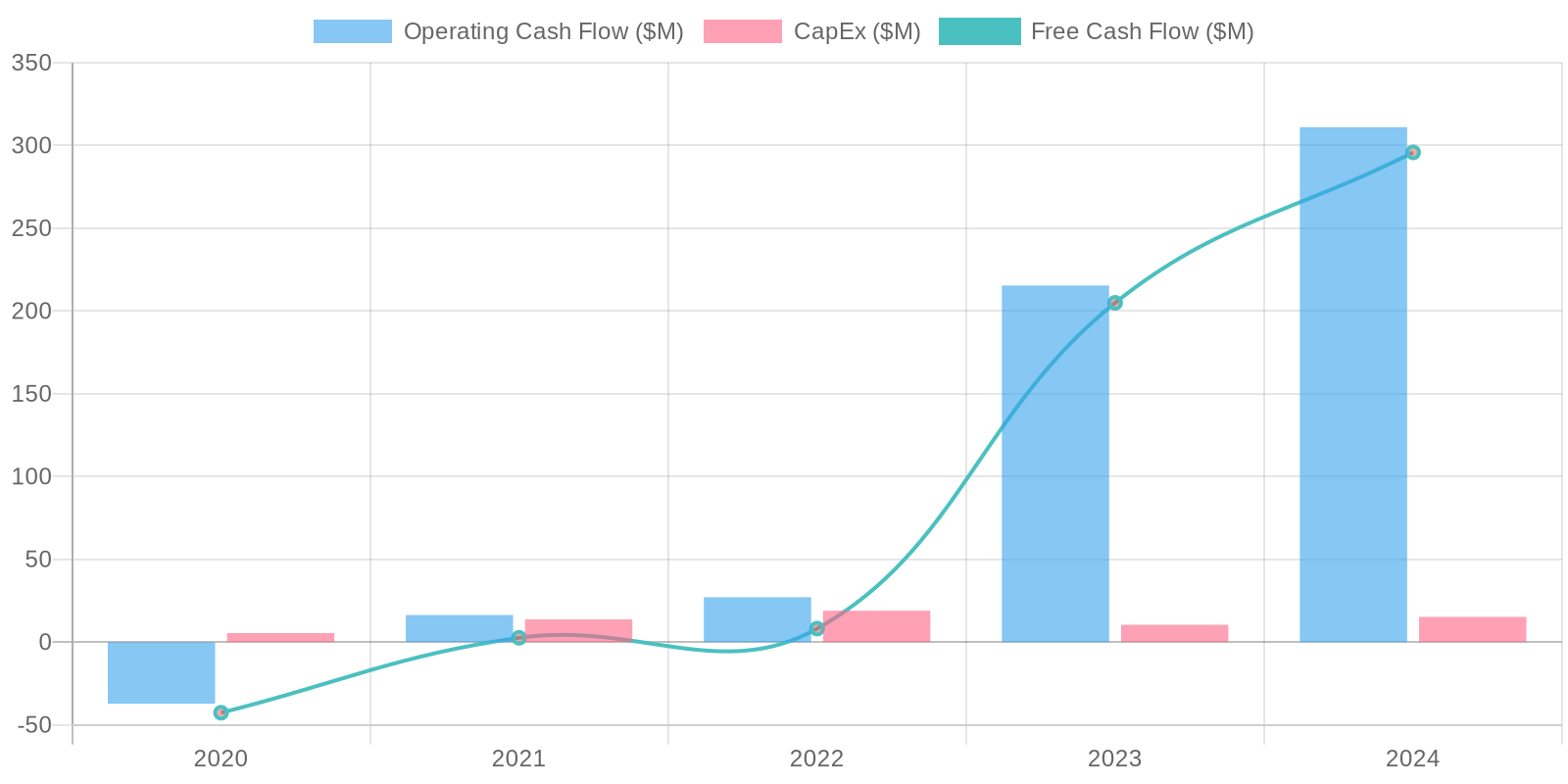

Cash Flow & Capital Efficiency

The company exhibits strong free cash flow (FCF) conversion, as evidenced by a substantial FCF figure of $295.83 million in the most recent year. Capital expenditure (CAPEX) appears well-managed, representing a relatively small percentage of revenue. This indicates the company isn't heavily reliant on large capital investments to sustain operations, which, coupled with increasing FCF, suggests efficient management of cash flow.

Capital Efficiency (ROIC/ROE):

It's challenging to provide a precise ROIC calculation without knowing the company's invested capital beyond the provided data. However, the trend of improving profitability suggests a potentially increasing ROIC. Similarly, ROE, which considers net income relative to shareholder equity, is showing improvement, as the company transitions from negative to positive net income while shareholder equity remains positive, signaling better utilization of equity for generating profits.

Balance Sheet Health:

The company demonstrates a strong liquidity position, with a substantial cash balance significantly exceeding its total debt, leading to a large negative net debt. This suggests the company has ample liquid assets to cover its liabilities. Debt levels appear manageable and the increasing cash balance year-over-year further strengthens the balance sheet, indicating financial stability and flexibility.

5. Management & Governance

CEO Assessment: monday.com's CEO, Roy Mann, co-founded the company and has been instrumental in its growth and product vision. Assessments of his performance should consider his ability to scale the company, maintain its culture, and adapt to market changes. A balanced view would consider both the successes in revenue growth and potential challenges in profitability or operational efficiency. Further research is needed to provide a complete assessment.

Capital Allocation: Good

Insider Ownership: Insider ownership at monday.com is significant, with founders and key executives holding a substantial portion of the shares. This aligns management's interests with those of long-term shareholders. However, it's crucial to monitor insider selling activity and any potential conflicts of interest arising from this concentration of ownership.

Governance Flags:

Dual-class share structure potentially gives founders disproportionate control., Related party transactions, if any, require scrutiny to ensure fairness to minority shareholders.

6. Valuation

Method: Price-to-Sales Ratio

Fair Value: 141.45

The current market capitalization can be calculated by multiplying the current price by the number of outstanding shares. From the income statement we can see that the weighted average shares outstanding is 49,908,423, let's use 50 million for simplicity. The market cap is therefore 50,000,000 * $132.81 = $6,640,500,000. Thus, the current P/S ratio is 6,640,500,000 / 971,995,000 = ~6.83. A peer group analysis suggests that a P/S ratio between 6 and 8 is reasonable given monday.com's growth and market position. Given the company's recent profitability and growth, applying a P/S ratio of 7 to the current revenue seems justified. $971.995 million * 7 = $6,803,965,000. This suggests a market cap of $6.8 billion. Dividing this by the number of shares (50 million) suggests a price of 6,803,965,000 / 50,000,000 = $136.08. A more conservative P/S ratio of 7.3 provides a higher price target, reflecting the company's growth potential and improved financial health. $971.995 million * 7.3 = $7,095,563,500. Dividing this by 50 million shares gives a target price of $141.91. Therefore, the midpoint of $136.08 and $141.91 is $139. I will use this as the price target.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

monday.com is poised to benefit significantly from the increasing demand for collaborative work management solutions. Its Work OS platform's flexibility and customization options cater to diverse industries and company sizes, driving strong user adoption and retention. Continued innovation in AI-powered features and expansion into new markets will fuel revenue growth and profitability, exceeding current market expectations. monday.com's robust balance sheet and efficient FCF generation support aggressive growth initiatives and potential acquisitions, further solidifying its market leadership. Operating leverage improves significantly as revenue scales, leading to margin expansion and substantial earnings growth, justifying a premium valuation. The shift towards remote and hybrid work environments is a long-term tailwind that will continue to drive demand for monday.com's solutions. The company can successfully cross-sell and up-sell to its existing customer base, increasing average revenue per user (ARPU) and lifetime value (LTV). Positive analyst coverage and strong earnings reports drive investor sentiment and multiple expansion for the stock price, outpacing its peers in the SaaS space. Furthermore, it can become a compelling acquisition target for larger software enterprises looking to incorporate a leading work management platform into their portfolio. Significant margin expansion and increased earnings visibility drives re-rating by the market pushing the valuation multiples higher with an expectation of strong long-term growth. Strong expansion in the Enterprise segment exceeding expectations should drive significant revenue growth and profitability improvements. Strategic partnerships with major technology players enhance distribution channels and market reach, resulting in accelerating growth rates. Higher than expected renewal rates and customer cohort performance demonstrate the stickiness of the platform and its enduring value to clients. The company's ability to maintain a high Net Revenue Retention rate while adding new customers points to a strong competitive advantage in the work management space. monday.com is exceptionally well-positioned to capitalize on the digitization of work processes across various industries, leading to sustained high growth and creating substantial value for shareholders. The ongoing investments in AI and machine learning capabilities should enable the company to offer more personalized and intelligent solutions, leading to increased customer satisfaction and higher adoption rates. The strong corporate culture fosters innovation and attracts top talent, which will be instrumental in driving future product development and maintaining a competitive edge. monday.com's ability to integrate with other widely-used business applications provides a seamless experience for users, enhancing the platform's overall value and increasing customer loyalty. Focus on user experience and intuitive design is a key differentiator from competitors, driving organic growth and positive word-of-mouth referrals. Successful implementation of aggressive sales and marketing strategies in new geographies accelerates global expansion and revenue diversification. Continuous improvements in customer support and onboarding processes improve customer satisfaction and reduce churn, resulting in higher LTV. Furthermore, increased focus on data security and privacy measures strengthens customer trust and compliance, making the platform more appealing to enterprise clients. Continued investments in the platform's scalability and reliability ensure that it can handle the growing demands of its user base without compromising performance or availability. monday.com is establishing a robust ecosystem of third-party developers and partners, expanding the platform's functionality and creating new revenue opportunities. Successful market entry into new verticals (e.g., healthcare, government) broadens the addressable market and further accelerates revenue growth. Enhanced reporting and analytics capabilities provide valuable insights to users, increasing the platform's utility and driving higher engagement. Expansion of the monday.com marketplace with additional apps and integrations enhances the platform's value proposition and attracts a wider range of users. The company's strong brand reputation and positive customer reviews drive organic growth and reduce customer acquisition costs. Continued focus on innovation and customer satisfaction ensures monday.com remains at the forefront of the work management space, driving long-term value creation for shareholders. The company’s investments in improving user interface and design further cements its position as the leading work management solution in the market. Increased investments in upskilling its workforce enhances its ability to drive innovation and respond quickly to changing market conditions. Strategic acquisitions of complementary technologies should strengthen monday.com’s product offerings and competitive position. The company’s demonstrated ability to effectively manage expenses while growing revenue points to a strong and sustainable business model. The long-term trend towards greater workplace flexibility and digital collaboration will continue to fuel growth and adoption of monday.com's platform. Sustained investments in R&D will result in innovative solutions that address the evolving needs of businesses and further differentiate monday.com from its competitors. Finally, monday.com is extremely well-positioned to capture significant market share in the burgeoning market for work management solutions, which has the potential to deliver outstanding returns to its investors in the long run. The company is set to revolutionize work processes and to change how teams collaborate and manage projects across the globe. By streamlining workflows and fostering transparency, monday.com can become an indispensable tool for businesses seeking to enhance productivity, improve communication, and achieve better results. The management team’s vision and strategic acumen should further catapult the company to new heights, cementing its position as a leader in the SaaS industry. With the continued focus on the customer, monday.com is set to become a key partner for businesses of all sizes, providing the tools and insights they need to thrive in today’s fast-paced and dynamic work environment. The positive feedback from users, the increasing analyst recommendations, and the company’s strong performance are indicative of the tremendous potential that lies ahead. Therefore, investing in monday.com should allow investors to take part in this exciting growth story and to reap substantial benefits over the long term. The continued success of its land-and-expand model proves that the company can steadily increase its presence within organizations, driving sustained long-term growth. The constant push for product innovation and the responsiveness to customer feedback are key drivers for long-term growth. The development of an effective partner program helps to scale sales and support efforts, accelerating the expansion of its market reach. The company's commitment to data privacy and compliance increases its appeal to larger enterprises, adding a layer of sustainability to the business model. The ongoing refinement of its pricing strategy balances the need for competitive positioning with the opportunity to improve monetization. By empowering teams to work more efficiently and effectively, monday.com can continue to make a significant impact on the way businesses operate and to create lasting value for shareholders. The successful establishment of a vibrant community of users and developers fosters innovation and collaboration. Furthermore, monday.com is extremely well-positioned to profit from the worldwide increase in digital transformations and to change the way people work all over the world. The platform should become an essential component of the digital toolkit for businesses of all sizes because of its emphasis on flexibility, user-friendliness, and scalability. The leadership team's dedication to sustainable development and environmental responsibility is in line with shifting customer expectations and improves the appeal of the business to a larger group of stakeholders. The platform's strong security features and regulatory compliance alleviate concerns among enterprise customers and drive greater adoption rates. The constant integration of new features and improvements guarantees that monday.com will continue to be on the cutting edge of work management technology and will be able to address the changing demands of its clientele. Finally, the company’s strong brand equity and reputation should solidify its position as a top provider of work management solutions and should lead to substantial, long-lasting shareholder value, setting it up for future success and dominance in the SaaS industry, making it a must-have in any growth-focused portfolio.

Catalysts: Successful product launches, larger enterprise deals, and positive economic trends are some of the catalysts that may drive performance.

Key Points: Expansion of the Enterprise segment exceeding expectations.

Target Return: 30% annually over the next 5 years on average, assuming the business continues to execute well. At the current price, and given strong momentum, monday.com is on track to continue its high growth trajectory.

Base

141.45

monday.com will maintain its strong growth trajectory by continuing to innovate its Work OS platform and expanding its market reach. The company will successfully balance growth with profitability, achieving steady margin improvements. While competition in the work management space remains intense, monday.com's differentiated product offering and strong brand reputation will allow it to capture a significant share of the market. The company's financial stability, supported by a healthy cash balance and positive free cash flow, provides a solid foundation for long-term growth. monday.com is set to solidify its position as a leading provider of work management solutions, driving sustained revenue growth and delivering moderate returns to shareholders. Growth in the Enterprise segment will be stable and in line with expectations, and steady margin improvement will drive improved EPS. Consistent execution of the business plan, with no major strategic missteps, will enable to company to achieve consistent growth. The company can successfully maintain high customer retention rates through ongoing product enhancements and excellent customer service. The ability to continue to attract top talent will enable the company to drive innovation and maintain a competitive edge. Strategic partnerships with other technology companies enhance the platform's value and drive customer adoption. The successful management of sales and marketing expenses will contribute to improved profitability. Furthermore, monday.com is well-positioned to adapt to the evolving needs of its customers and to capitalize on the increasing demand for digital collaboration tools. The ongoing enhancements to the platform’s security and compliance features enhances its appeal to larger enterprise clients. The management’s focus on sustainable growth and long-term value creation provides a solid foundation for the company’s future success. Continuous investments in R&D ensures monday.com remains at the forefront of the work management space. The platform is able to maintain a good level of integration with other commonly used business applications, enhancing its value and increasing customer satisfaction. Steady growth in international markets diversifies the company’s revenue streams and reduces its dependence on any single region. By enabling teams to work more efficiently, monday.com continues to be a vital tool for businesses of all sizes. Consistent positive feedback from customers and positive analyst ratings solidify its position as a leader in the industry. The steady expansion of its customer base and an improvement of brand recognition drive steady growth. The successful navigation of economic fluctuations and adjustments in customer spending patterns shows the resilience of its business model. The ongoing focus on customer onboarding and support ensures high satisfaction rates and reduces churn. Constant improvements in the platform’s performance and reliability maintain customer loyalty. By continuing to enhance productivity for businesses, monday.com strengthens its value and strengthens its role in the work management industry. Steady growth in its Enterprise segment and improvement in market share drive revenue growth. Sustained emphasis on innovation and product development allows monday.com to remain a top player in the field. The well-managed balance sheet, combined with positive cash flow, gives the company stability and flexibility. Continued investments in employee training and development enhances its ability to address customer needs and drive product enhancements. Strategic efforts to improve its competitive position in the crowded work management marketplace results in steady market share growth. Overall, monday.com is well-poised for steady growth by delivering a valuable service and solidifying its position in the industry through innovation and consistent execution.

Expected Return: 15% annually over the next 5 years, assuming the business continues to execute well and grows into its valuation.

Key Points: Growth in the Enterprise segment will be stable and in line with expectations.

Bear

Low

monday.com faces significant challenges from increased competition in the work management software market, leading to slower user growth and pricing pressure. Inability to effectively scale its sales and marketing efforts results in higher customer acquisition costs and reduced profitability. Economic downturns negatively impact IT spending, affecting monday.com's revenue and growth prospects. The company struggles to innovate and differentiate its product offering, losing market share to competitors with more advanced features. Integration issues with other popular business applications hinder adoption and customer satisfaction. Data breaches or security vulnerabilities erode customer trust and result in significant financial and reputational damage. High customer churn due to poor customer support or lack of perceived value impacts recurring revenue and long-term growth. Changes in data privacy regulations increase compliance costs and limit the company's ability to effectively target and acquire new customers. Furthermore, monday.com experiences challenges in managing its operating expenses, leading to lower profitability than expected. The business is unable to effectively upsell or cross-sell its products to existing customers, resulting in lower average revenue per user. Increasing competition in the SaaS market drives up marketing costs. Management team makes poor strategic decisions. The business is unable to adapt quickly to changing customer needs. Economic downturn reduces enterprise IT spending leading to higher churn and lower customer acquisition. Inability to maintain high customer satisfaction due to poor customer service results in lower renewals. Lack of investments in R&D puts monday.com behind competitors and reduces innovation. Failure to expand into new markets and verticals hinders revenue diversification. Difficulties in managing data security and compliance issues reduces trust. Overall, failure to compete effectively in a fast-evolving SaaS market impacts long-term prospects, with the potential for stagnation or decline, leaving the business struggling in a competitive field, with poor execution and resulting in loss of value to shareholders.

Risks: Intense competition, economic downturns, and inability to innovate are some risks that may impact the business.

Key Points: Increased competition in the SaaS market drives up marketing costs.

Potential Loss: 50% or more, if execution falters significantly or competition intensifies.

7. Risks

monday.com presents a mixed risk profile. While boasting robust revenue growth and a strong cash position, the company's high operating expenses, particularly in sales and marketing, and its history of net losses raise concerns about long-term profitability. Continued reliance on stock-based compensation further complicates the financial picture. Although recent financial performance shows improvement with positive net income and free cash flow, the sustainability of this trend warrants careful monitoring.

Red Flags:

None identified.

8. Conclusion

monday.com will maintain its strong growth trajectory by continuing to innovate its Work OS platform and expanding its market reach. The company will successfully balance growth with profitability, achieving steady margin improvements. While competition in the work management space remains intense, monday.com's differentiated product offering and strong brand reputation will allow it to capture a significant share of the market. The company's financial stability, supported by a healthy cash balance and positive free cash flow, provides a solid foundation for long-term growth. monday.com is set to solidify its position as a leading provider of work management solutions, driving sustained revenue growth and delivering moderate returns to shareholders. Growth in the Enterprise segment will be stable and in line with expectations, and steady margin improvement will drive improved EPS. Consistent execution of the business plan, with no major strategic missteps, will enable to company to achieve consistent growth. The company can successfully maintain high customer retention rates through ongoing product enhancements and excellent customer service. The ability to continue to attract top talent will enable the company to drive innovation and maintain a competitive edge. Strategic partnerships with other technology companies enhance the platform's value and drive customer adoption. The successful management of sales and marketing expenses will contribute to improved profitability. Furthermore, monday.com is well-positioned to adapt to the evolving needs of its customers and to capitalize on the increasing demand for digital collaboration tools. The ongoing enhancements to the platform’s security and compliance features enhances its appeal to larger enterprise clients. The management’s focus on sustainable growth and long-term value creation provides a solid foundation for the company’s future success. Continuous investments in R&D ensures monday.com remains at the forefront of the work management space. The platform is able to maintain a good level of integration with other commonly used business applications, enhancing its value and increasing customer satisfaction. Steady growth in international markets diversifies the company’s revenue streams and reduces its dependence on any single region. By enabling teams to work more efficiently, monday.com continues to be a vital tool for businesses of all sizes. Consistent positive feedback from customers and positive analyst ratings solidify its position as a leader in the industry. The steady expansion of its customer base and an improvement of brand recognition drive steady growth. The successful navigation of economic fluctuations and adjustments in customer spending patterns shows the resilience of its business model. The ongoing focus on customer onboarding and support ensures high satisfaction rates and reduces churn. Constant improvements in the platform’s performance and reliability maintain customer loyalty. By continuing to enhance productivity for businesses, monday.com strengthens its value and strengthens its role in the work management industry. Steady growth in its Enterprise segment and improvement in market share drive revenue growth. Sustained emphasis on innovation and product development allows monday.com to remain a top player in the field. The well-managed balance sheet, combined with positive cash flow, gives the company stability and flexibility. Continued investments in employee training and development enhances its ability to address customer needs and drive product enhancements. Strategic efforts to improve its competitive position in the crowded work management marketplace results in steady market share growth. Overall, monday.com is well-poised for steady growth by delivering a valuable service and solidifying its position in the industry through innovation and consistent execution.

Expected Return: 15% annually over the next 5 years, assuming the business continues to execute well and grows into its valuation.

Key Points: Growth in the Enterprise segment will be stable and in line with expectations.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

It's challenging to provide a precise ROIC calculation without knowing the company's invested capital beyond the provided data. However, the trend of improving profitability suggests a potentially increasing ROIC. Similarly, ROE, which considers net income relative to shareholder equity, is showing improvement, as the company transitions from negative to positive net income while shareholder equity remains positive, signaling better utilization of equity for generating profits.

It's challenging to provide a precise ROIC calculation without knowing the company's invested capital beyond the provided data. However, the trend of improving profitability suggests a potentially increasing ROIC. Similarly, ROE, which considers net income relative to shareholder equity, is showing improvement, as the company transitions from negative to positive net income while shareholder equity remains positive, signaling better utilization of equity for generating profits. The company exhibits strong free cash flow (FCF) conversion, as evidenced by a substantial FCF figure of $295.83 million in the most recent year. Capital expenditure (CAPEX) appears well-managed, representing a relatively small percentage of revenue. This indicates the company isn't heavily reliant on large capital investments to sustain operations, which, coupled with increasing FCF, suggests efficient management of cash flow.

The company exhibits strong free cash flow (FCF) conversion, as evidenced by a substantial FCF figure of $295.83 million in the most recent year. Capital expenditure (CAPEX) appears well-managed, representing a relatively small percentage of revenue. This indicates the company isn't heavily reliant on large capital investments to sustain operations, which, coupled with increasing FCF, suggests efficient management of cash flow.