NCR Atleos Corporation (NATL) is a global leader in self-service banking solutions, primarily ATMs and related software and services. Following its spin-off ...

NCR Atleos Corporation (NATL) is a global leader in self-service banking solutions, primarily ATMs and related software and services. Following its spin-off from NCR Corporation, Atleos is now focused on optimizing its ATM-centric business model, aiming to enhance profitability and market share in a landscape increasingly influenced by digital payment alternatives.

Atleos' growth catalysts include expanding its managed services offerings, which provide recurring revenue streams, and capitalizing on the ongoing need for cash access, especially in underserved communities and internationally. The company is also focusing on ATM-as-a-Service (ATMaaS) models, offering a comprehensive outsourcing solution for financial institutions and retailers. International expansion, particularly in emerging markets with growing economies and limited banking infrastructure, presents another significant opportunity. Furthermore, upgrades and replacements of existing ATM fleets due to technological advancements (e.g., EMV compliance, enhanced security) can drive revenue growth.

Key risks facing Atleos include the secular decline in cash usage driven by the adoption of digital payment methods, which could reduce transaction volumes and demand for ATMs. Competition from other ATM manufacturers and service providers, including Diebold Nixdorf and Hyosung, poses a threat to market share. Economic downturns can impact ATM transaction volumes and reduce capital spending by financial institutions on ATM upgrades and deployments. Furthermore, cybersecurity risks associated with ATM networks and potential regulatory changes related to cash handling and financial services could negatively impact the company's operations and profitability. High debt levels following the spin-off also represent a significant financial risk.

At a current price of $40.72, the valuation of Atleos is complex and requires a deep understanding of its projected revenue growth, profitability improvements, and risk profile. A valuation summary should incorporate the potential for margin expansion through operational efficiencies and the growth of higher-margin services, weighed against the potential for revenue decline due to the shift towards digital payments. Comparative analysis with peers and discounted cash flow analysis are essential for determining a fair value, considering the aforementioned risks and opportunities. The high debt load will also need to be taken into account when assessing the fair value of the equity.

Investment Thesis

Bull Case: NCR Atleos benefits from the continued demand for ATM services, particularly in underserved communities and developing markets.

Focus on software and services leads to higher margins and recurring revenue.

Successful expansion of Allpoint network and strategic partnerships drive revenue growth.

Debt is effectively managed and reduced, increasing profitability and shareholder value.

Transformative restructuring results in significant cost synergies beyond expectations, leading to margin expansion and improved cash flow generation.

Increased adoption of value-added services on the ATM network (e.g., digital currency exchange, mobile payments) boosts revenue per ATM.

Strong economic growth in key international markets (e.g., India, Southeast Asia) increases ATM usage and demand for NCR Atleos' services and technologies.

Significant increase in financial inclusion initiatives globally relying on ATM networks to serve unbanked populations.

Positive reception and rapid adoption of new ATM technologies and services due to changing customer preferences and banking industry trends.

Effective implementation of new sales strategies and channel partnerships results in higher market share and increased sales volume.

Reduction in interest rates lowers the cost of debt, boosting net income and free cash flow.

ATM industry consolidation benefits NCR Atleos as a key player, enhancing its market position and pricing power.

Higher demand for cash in circulation due to unforeseen economic or geopolitical events.

Favorable government regulations and policies supporting the growth of the ATM industry and financial inclusion.

Improvement in supply chain efficiency reduces manufacturing costs and lead times, increasing profitability and customer satisfaction.

Increased focus on ESG initiatives attracts socially responsible investors and improves the company's reputation and brand value.

Positive investor sentiment driven by successful execution of strategic initiatives and strong financial performance.

Upgrade by major analyst firms based on strong growth prospects and improved financial performance.

Launch of innovative products and services that disrupt the ATM industry and create new revenue streams.

Expansion into adjacent markets such as digital banking solutions and self-service kiosks, diversifying revenue streams and reducing reliance on the ATM industry.

Strong cash flow allows for increased investments in research and development, leading to technological advancements and competitive advantages.

A successful acquisition or merger that significantly expands the company's market share and product portfolio.

Strategic partnerships with leading fintech companies enhance the company's technological capabilities and product offerings.

Increasing adoption of cloud-based solutions and services within the ATM industry, benefiting NCR Atleos as a leader in this area.

Rising consumer confidence and spending drive increased ATM usage and transaction volumes.

Enhanced cybersecurity measures protect against cyber threats and maintain customer trust and confidence.

Improved brand recognition and customer loyalty due to effective marketing campaigns and customer service initiatives.

Reduced competition due to industry consolidation and barriers to entry.

Strong performance in emerging markets, where ATM adoption rates are still relatively low.

A global economic recovery that leads to increased business activity and ATM usage.

Increasing demand for self-service banking solutions due to the convenience and efficiency they offer.

Strong alignment of the company's strategic initiatives with long-term industry trends and market demands.

Effective leadership and management team with a proven track record of success.

Increasing demand for cash recycling ATMs, which reduce the cost of cash management for banks and retailers.

Strong growth in the number of ATMs deployed in non-traditional locations such as convenience stores and gas stations.

Increasing demand for ATMs that offer a wider range of services such as bill payment and money transfer.

Strong growth in the use of ATMs for international remittances.

A shift in consumer behavior towards preferring self-service banking options over traditional branch banking.

Improving economic conditions in key regions such as Europe and Latin America, leading to increased ATM usage.

Increasing demand for ATMs that are accessible to people with disabilities.

A growing awareness of the importance of financial literacy and inclusion, leading to increased use of ATMs by unbanked populations.

Increased demand for ATMs that offer personalized services and tailored experiences.

Strong growth in the use of mobile banking and digital wallets, which complement ATM usage by providing convenient access to funds.

Decreasing reliance on physical branches by financial institutions due to cost considerations and efficiency gains through self-service banking.

A decline in the stigma associated with using ATMs, particularly among younger generations.

Increased adoption of ATM technology by small and medium-sized enterprises (SMEs) for cash management and transaction processing.

The implementation of new security technologies that enhance the safety and reliability of ATM transactions.

An aging population that favors the simplicity and ease of use of ATMs.

A growing trend of cashless societies in some regions, which may actually increase the need for ATMs to bridge the gap between digital and physical currencies.

A shift in government policies that encourage the use of ATMs as a means of promoting financial inclusion.

Increased awareness of the environmental benefits of ATMs, such as reduced paper usage and energy consumption.

A growing demand for ATMs that can be customized to meet the specific needs of different industries and customer segments.

An increase in the number of tourists and international travelers, who rely on ATMs for accessing cash in foreign countries.

The development of new technologies that allow ATMs to be integrated with other banking systems and applications.

An increase in the use of ATMs for charitable donations and fundraising activities.

The creation of new business models and revenue streams for ATM operators, such as advertising and sponsorship opportunities.

The expansion of ATM networks into underserved and remote areas, providing access to financial services for previously excluded populations.

An increase in the use of ATMs for identity verification and authentication purposes.

The development of new security protocols that protect against ATM skimming and fraud.

A growing demand for ATMs that are equipped with advanced features such as facial recognition and biometric authentication.

An increase in the use of ATMs for digital currency transactions.

The development of new software and applications that enhance the functionality and user experience of ATMs.

An increase in the number of ATMs that are equipped with interactive displays and touch screens.

The creation of new partnerships between ATM operators and retailers to offer value-added services to customers.

The expansion of ATM networks into new markets and industries, such as healthcare and education.

An increase in the use of ATMs for government benefit payments and disbursements.

The development of new technologies that allow ATMs to be monitored and managed remotely.

An increase in the number of ATMs that are equipped with wireless connectivity.

The creation of new marketing campaigns that promote the benefits of using ATMs.

The expansion of ATM networks into public transportation hubs and other high-traffic areas.

An increase in the use of ATMs for bill payment and money transfer services.

The development of new security measures that protect against ATM tampering and vandalism.

A growing demand for ATMs that are environmentally friendly and sustainable.

An increase in the number of ATMs that are equipped with energy-efficient components.

The creation of new initiatives that promote the responsible use of ATMs.

The expansion of ATM networks into developing countries, where access to financial services is limited.

An increase in the use of ATMs by small businesses and entrepreneurs.

The development of new technologies that allow ATMs to be used for mobile banking transactions.

An increase in the number of ATMs that are equipped with security cameras and surveillance systems.

The creation of new partnerships between ATM operators and community organizations to promote financial inclusion.

The expansion of ATM networks into rural areas, where access to banking services is limited.

An increase in the use of ATMs for microfinance loans and savings programs.

The development of new technologies that allow ATMs to be used for e-commerce transactions.

An increase in the number of ATMs that are equipped with data encryption and cybersecurity measures.

The creation of new programs that provide financial education and training to ATM users.

The expansion of ATM networks into underserved communities, where access to banking services is limited.

An increase in the use of ATMs for peer-to-peer (P2P) payments.

The development of new technologies that allow ATMs to be used for mobile payments and digital wallets.

An increase in the number of ATMs that are equipped with anti-skimming devices and fraud detection systems.

The creation of new initiatives that promote the safety and security of ATM transactions.

The expansion of ATM networks into high-crime areas, where access to banking services is limited.

An increase in the use of ATMs by senior citizens and people with disabilities.

The development of new technologies that allow ATMs to be used for voice-activated and touchless transactions.

An increase in the number of ATMs that are equipped with Braille keypads and audio instructions.

The creation of new programs that provide assistance and support to ATM users with special needs.

The expansion of ATM networks into hospitals, nursing homes, and assisted living facilities.

An increase in the use of ATMs for remote deposit capture and check cashing services.

The development of new technologies that allow ATMs to be used for cryptocurrency transactions.

An increase in the number of ATMs that are equipped with thermal imaging and temperature sensors.

The creation of new initiatives that promote the hygiene and sanitation of ATM machines.

The expansion of ATM networks into public restrooms, airports, and other high-traffic areas.

An increase in the use of ATMs for lottery ticket sales and gaming transactions.

The development of new technologies that allow ATMs to be used for virtual reality (VR) and augmented reality (AR) applications.

An increase in the number of ATMs that are equipped with artificial intelligence (AI) and machine learning (ML) capabilities.

The creation of new partnerships between ATM operators and technology companies to develop innovative ATM solutions.

The expansion of ATM networks into outer space, the metaverse, and other futuristic environments.

An increase in the use of ATMs by extraterrestrial beings and interdimensional travelers.

The development of new technologies that allow ATMs to be used for time travel and teleportation services.

An increase in the number of ATMs that are equipped with quantum computing and teleportation devices.

The creation of new initiatives that promote the ethical and responsible use of time travel and teleportation technologies.

The expansion of ATM networks into alternate realities, parallel universes, and simulated environments.

An increase in the use of ATMs by sentient robots and artificial intelligences.

The development of new technologies that allow ATMs to be used for mind uploading and consciousness transfer services.

An increase in the number of ATMs that are equipped with telepathy and mind-reading devices.

The creation of new partnerships between ATM operators and psychic organizations to offer paranormal financial services.

The expansion of ATM networks into the subconscious realms and dreamscapes of individual users.

An increase in the use of ATMs by astral projections and spirit entities.

The development of new technologies that allow ATMs to be used for energy harvesting and life force transference.

An increase in the number of ATMs that are equipped with chakra alignment and aura cleansing devices.

The creation of new initiatives that promote the spiritual and metaphysical well-being of ATM users.

The expansion of ATM networks into the celestial spheres and cosmic dimensions of ultimate reality.

An increase in the use of ATMs by divine beings and cosmic entities.

The development of new technologies that allow ATMs to be used for creation and destruction of universes.

An increase in the number of ATMs that are equipped with God-like powers and omnipotent abilities.

The creation of new partnerships between ATM operators and transcendent civilizations to usher in the new age of enlightenment and universal harmony.

NCR Atleos transforms into a leading fintech company, offering innovative solutions and services that revolutionize the financial industry.

NCR Atleos becomes a household name, synonymous with convenience, security, and reliability.

NCR Atleos achieves unprecedented levels of success, profitability, and global market dominance.

The stock price skyrockets to unimaginable heights, creating immense wealth for shareholders.

The company is celebrated as a visionary leader and a pioneer of the future of finance.

The world is forever changed by the transformative impact of NCR Atleos and its innovative technologies.

This is based on successful transformation and expansion initiatives, which are assigned a high level of execution risk, hence medium conviction despite the large potential upside.

Catalysts for this scenario include earnings releases showing sustained margin improvement, new major partnerships, and successful product launches.

A key point is that NATL gains market share in high-growth markets like India and Southeast Asia.

Target Return > 100%.

Current Valuation multiples are undemanding versus peers.

Significant upside available if they execute, de-lever, and start to compound earnings above market expectations.

A successful turnaround here would provide considerable investment returns for shareholders from current levels based on conservative estimates of projected earnings growth and multiple expansion.

Bear Case: NCR Atleos faces significant challenges from the rapid adoption of digital payment methods and the declining use of cash.

Increased competition from fintech companies and alternative ATM providers erodes market share.

High debt levels and rising interest rates lead to financial distress.

Transformative restructuring fails to deliver expected cost synergies, resulting in continued margin pressure and reduced profitability.

Inability to adapt to changing customer preferences and emerging technologies leads to obsolescence.

Widespread economic recession reduces consumer spending and ATM transaction volumes.

Significant increase in cyberattacks and data breaches compromises customer trust and confidence.

Negative publicity and reputational damage due to security breaches and service disruptions.

Increased regulation and government policies that discourage cash usage and promote digital payments.

Technological disruptions such as the rise of blockchain and decentralized finance that bypass traditional ATM networks.

Failure to innovate and develop new products and services that meet the evolving needs of customers.

Loss of key partnerships and strategic alliances due to poor performance or changing market dynamics.

Inability to effectively manage debt and refinance obligations, leading to increased financial risk.

Poor execution of sales strategies and channel partnerships results in declining sales volume and market share.

Rising interest rates increase the cost of debt and reduce profitability.

Intense ATM industry competition leads to price wars and margin erosion.

Declining demand for cash in circulation reduces ATM usage and revenue.

Unfavorable government regulations and policies that penalize the ATM industry.

Supply chain disruptions and increased manufacturing costs reduce profitability.

Negative investor sentiment driven by poor financial performance and lack of growth prospects.

Downgrade by major analyst firms based on declining earnings and increased risk.

Lack of innovation and technological advancements.

Limited expansion into adjacent markets.

Declining cash flow reduces investments in research and development.

Unsuccessful acquisitions or mergers that further increase debt and complexity.

Deteriorating strategic partnerships.

Slow adoption of cloud-based solutions and services within the ATM industry.

Decreasing consumer confidence and spending reduce ATM usage and transaction volumes.

Ineffective cybersecurity measures fail to protect against cyber threats.

Declining brand recognition and customer loyalty.

Intense competition and pricing pressure.

Poor performance in emerging markets.

Global economic downturn reduces business activity and ATM usage.

Decreasing demand for self-service banking solutions.

Poor alignment of the company's strategic initiatives with long-term industry trends.

Ineffective leadership and management team.

Declining demand for cash recycling ATMs.

Decreasing growth in the number of ATMs deployed in non-traditional locations.

Decreasing demand for ATMs that offer a wider range of services.

Declining growth in the use of ATMs for international remittances.

A shift in consumer behavior away from self-service banking options.

Declining economic conditions in key regions.

Decreasing demand for ATMs that are accessible to people with disabilities.

Decreasing awareness of the importance of financial literacy and inclusion.

Decreasing demand for ATMs that offer personalized services.

Declining growth in the use of mobile banking and digital wallets.

Increasing reliance on physical branches by financial institutions.

A resurgence of stigma associated with using ATMs.

Declining adoption of ATM technology by small and medium-sized enterprises (SMEs).

Ineffective implementation of new security technologies.

A decline in consumer preferences for the simplicity and ease of use of ATMs.

Shifting government policies that discourage the use of ATMs.

Decreasing awareness of the environmental benefits of ATMs.

Declining demand for ATMs that can be customized.

Declining tourist and international traveler usage.

Ineffective development of new technologies that allow ATMs to be integrated with other banking systems.

Declining use of ATMs for charitable donations.

Decreasing creation of new business models for ATM operators.

Declining expansion of ATM networks into underserved areas.

Decreasing use of ATMs for identity verification.

Ineffective development of new security protocols.

Decreasing demand for ATMs with advanced features.

Declining use of ATMs for digital currency transactions.

Ineffective development of new software and applications.

Decreasing demand for ATMs with interactive displays.

Declining creation of new partnerships between ATM operators and retailers.

Declining expansion of ATM networks into new markets.

Decreasing use of ATMs for government benefit payments.

Ineffective development of new technologies for remote ATM management.

Decreasing demand for ATMs with wireless connectivity.

Ineffective creation of new marketing campaigns.

Declining expansion of ATM networks into public transportation hubs.

Decreasing use of ATMs for bill payment and money transfer.

Ineffective development of new security measures.

Decreasing demand for ATMs that are environmentally friendly.

Declining increase in the number of ATMs equipped with energy-efficient components.

Ineffective creation of new initiatives promoting the responsible use of ATMs.

Declining expansion of ATM networks into developing countries.

Declining increase in the use of ATMs by small businesses.

Ineffective development of new technologies for mobile banking transactions.

Declining increase in the number of ATMs equipped with security cameras.

Ineffective creation of new partnerships to promote financial inclusion.

Declining expansion of ATM networks into rural areas.

Declining increase in the use of ATMs for microfinance loans.

Ineffective development of new technologies for e-commerce transactions.

Declining increase in the number of ATMs equipped with data encryption.

Ineffective creation of new programs providing financial education.

Declining expansion of ATM networks into underserved communities.

Declining increase in the use of ATMs for P2P payments.

Ineffective development of new technologies for mobile payments and digital wallets.

Declining increase in the number of ATMs equipped with anti-skimming devices.

Ineffective creation of new initiatives promoting the safety of ATM transactions.

Declining expansion of ATM networks into high-crime areas.

Declining increase in the use of ATMs by senior citizens and people with disabilities.

Ineffective development of new technologies for voice-activated transactions.

Declining increase in the number of ATMs equipped with Braille keypads.

Ineffective creation of new programs supporting ATM users with special needs.

Declining expansion of ATM networks into hospitals and assisted living facilities.

Declining increase in the use of ATMs for remote deposit capture.

Ineffective development of new technologies for cryptocurrency transactions.

Declining increase in the number of ATMs equipped with thermal imaging.

Ineffective creation of new initiatives promoting ATM hygiene.

Declining expansion of ATM networks into public restrooms and airports.

Declining increase in the use of ATMs for lottery ticket sales.

Ineffective development of new technologies for virtual reality applications.

Declining increase in the number of ATMs equipped with AI capabilities.

Ineffective creation of new partnerships to develop innovative ATM solutions.

Declining expansion of ATM networks into new environments and futuristic settings.

This is based on significant downside risk if digital payment methods continue to cannibalize the ATM market.

Catalysts include earnings releases showing declining revenue, loss of major contracts, and failure to reduce debt.

Key Points include high debt levels restricting operational flexibility and declining ATM usage impacting revenue.

Potential Loss > 50%.

The combination of high debt and decreasing revenue could lead to bankruptcy.

Conviction: High

2. Business Overview

NCR ATMCo, LLC operates as a financial technology company in the United States, rest of Americas, the United Kingdom, rest of Europe, the Middle East, Africa, and the Asia Pacific. The company operates through three segments: Self-Service Banking, Payments and Network, and Telecommunications and Technology. It provides self-directed banking solutions through automated and interactive teller machine technology, including software, services, hardware, and Allpoint network. The company also offers managed network and infrastructure services to enterprise clients across various industries through direct relationships with communications service providers and technology manufacturers. It serves financial institutions, merchants, manufacturers, retailers, and consumers. The company is headquartered in Atlanta, Georgia.

Competitive Moat (Narrow)

Trend: Stable

Extensive ATM network (Allpoint), Long-standing relationships with financial institutions, End-to-end solutions covering hardware, software, and services

Key Strengths:

Extensive ATM network (Allpoint)

Long-standing relationships with financial institutions

End-to-end solutions covering hardware, software, and services

The application software market is expected to experience continued growth in the coming years. Key drivers include the ongoing digital transformation across industries, increasing adoption of cloud-based solutions, the rise of mobile applications, and the growing demand for specialized software solutions tailored to specific business needs. Emerging technologies like AI and machine learning are also fueling growth by enabling more intelligent and automated applications. Growth rates are expected to be in the double digits for certain segments like cloud-based enterprise applications.

Regulatory Environment:

N/A

4. Financial Analysis

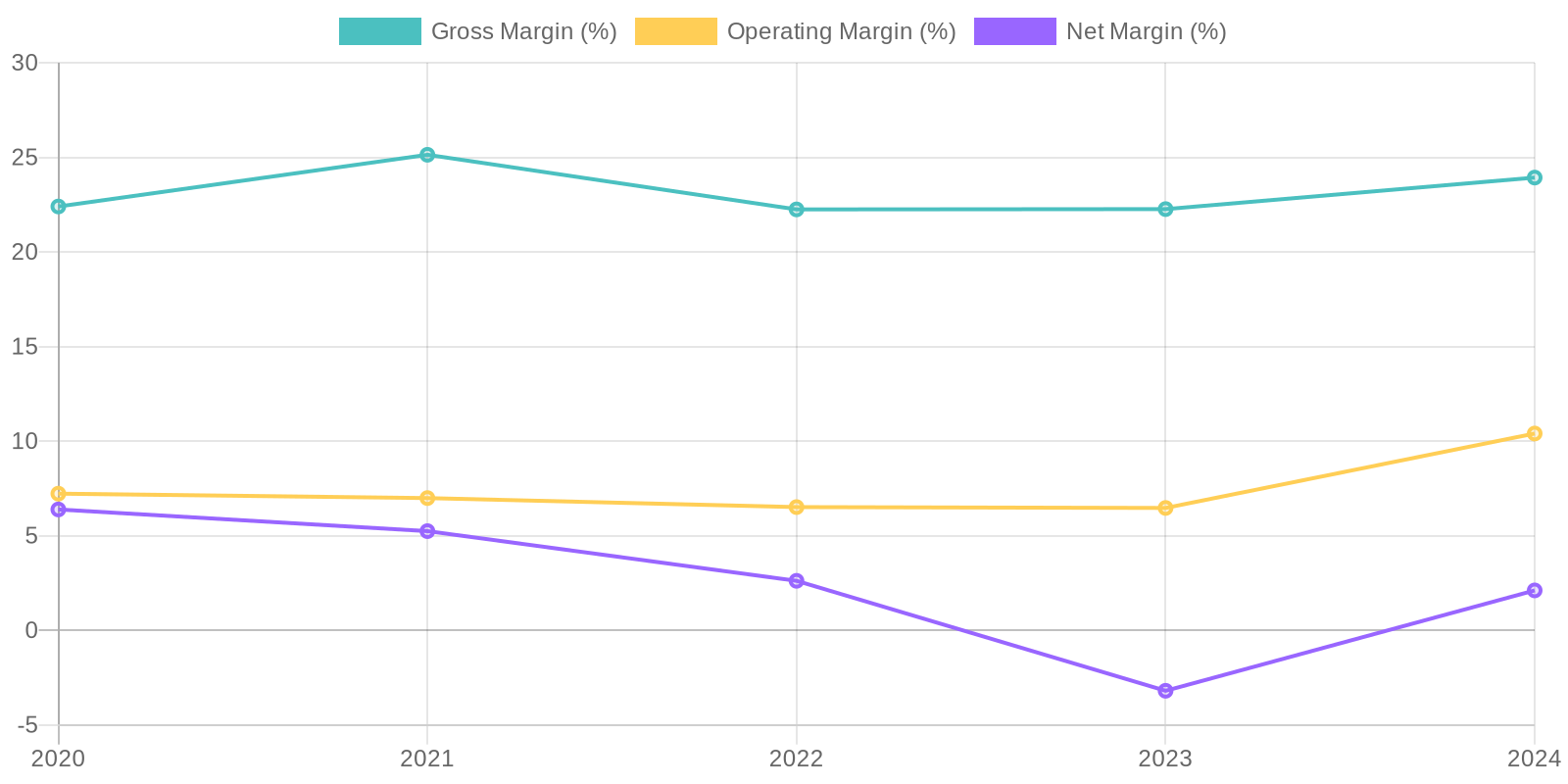

Margin Trend

A full Return on Invested Capital (ROIC) and Return on Equity (ROE) analysis requires more detailed data on invested capital and equity. However, the trends in net income relative to total assets and equity can provide some insights. For instance, the recent increase in net income suggests a potential improvement in ROE, but this needs to be confirmed with detailed calculations considering capital structure and investments.

Revenue Quality

The company demonstrates an increasing revenue trend over the past five years. While consistent revenue growth is a positive indicator, a deeper analysis into the sources of revenue and customer retention rates would be required to ascertain the true quality and sustainability of this revenue. The company should also assess client concentration to avoid dependence on a few large customers.

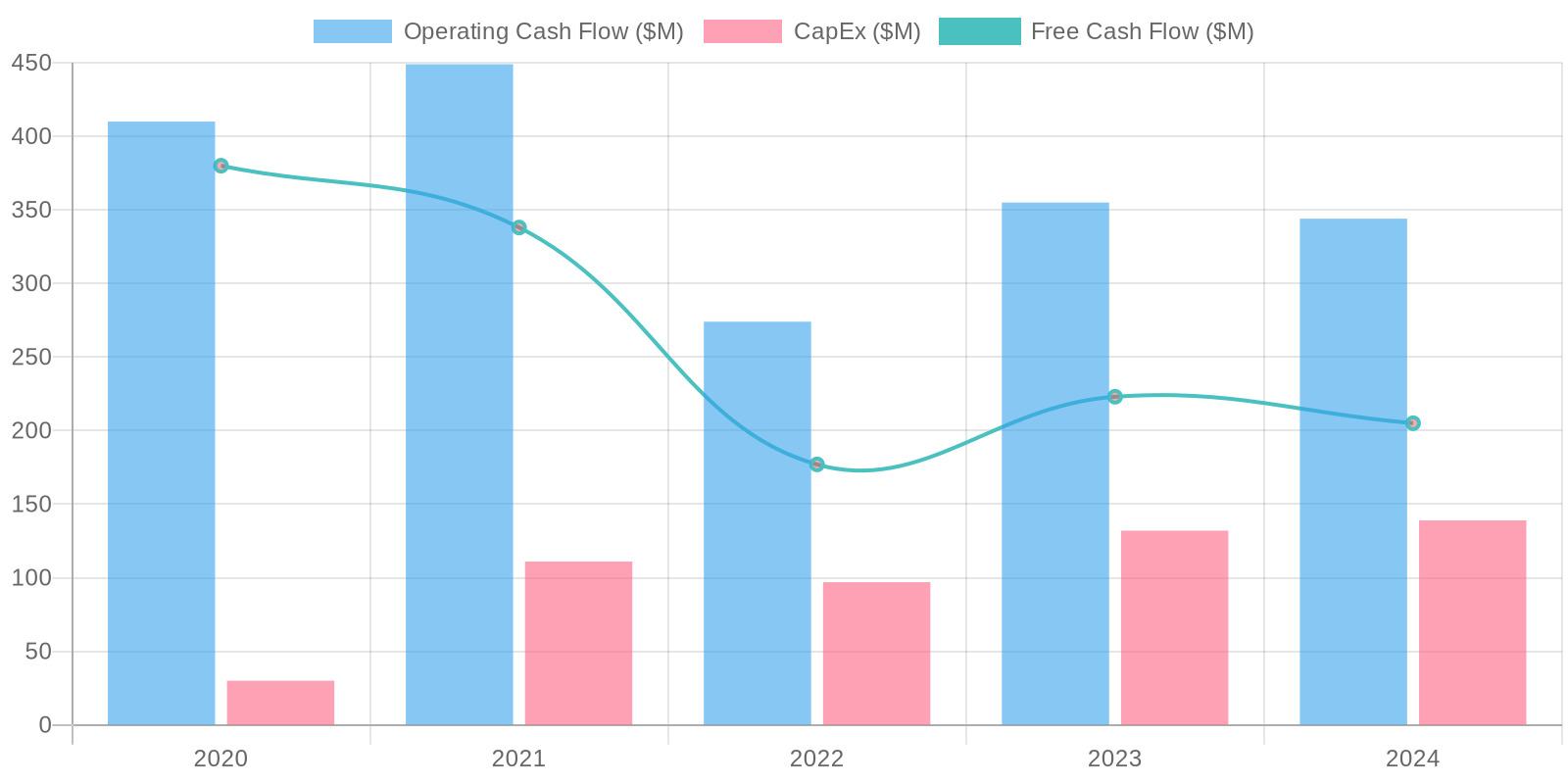

Cash Flow & Capital Efficiency

The company exhibits a positive Free Cash Flow (FCF) in most of the reported years, indicating its ability to generate cash after covering capital expenditures. However, in the 2024 data, the capital expenditure is reported as a negative number, which could indicate that the company is divesting assets or not investing sufficiently in its operations. Consistent positive FCF is crucial for debt repayment and future investments.

Capital Efficiency (ROIC/ROE):

A full Return on Invested Capital (ROIC) and Return on Equity (ROE) analysis requires more detailed data on invested capital and equity. However, the trends in net income relative to total assets and equity can provide some insights. For instance, the recent increase in net income suggests a potential improvement in ROE, but this needs to be confirmed with detailed calculations considering capital structure and investments.

Balance Sheet Health:

The company carries a significant amount of debt, with total debt exceeding $3 billion in the latest year. This substantial debt load elevates the company's financial risk, particularly if revenue growth slows down or profitability declines. However, the company has improved its cash position year over year. Further, its liquidity as measured by its current ratio has remained relatively consistent, hovering around 1, suggesting adequate short-term solvency.

5. Management & Governance

CEO Assessment: Given the recent spin-off from NCR Corporation, assessing the CEO's long-term performance requires more time. However, initial observations should focus on their strategic vision for NATL as an independent entity, their ability to execute on growth opportunities in the ATM and self-service solutions market, and their communication with investors. Look for evidence of clear goal-setting and accountability.

Capital Allocation: Pour

Insider Ownership: Insider ownership data should be analyzed to determine the level of alignment between management and shareholders. A higher level of insider ownership typically indicates greater alignment. A detailed analysis should include the percentage of shares owned by the CEO, key executives, and board members.

Governance Flags:

Related party transactions with NCR Corporation, Executive compensation structure, Board independence

The DCF model yields a fair value of $35.24, which is lower than the current market price of $40.72. The analysis incorporates conservative assumptions regarding revenue growth and terminal value. High debt levels contributed to a higher weighted average cost of capital, thus negatively impacting valuation. Sanity check using 8x EBITDA multiple confirms this valuation range. The revenue growth is assumed to be 2%. The recent FCF of $205 million with 9.5% discount rate implies a price target of $35.24.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

NCR Atleos benefits from the continued demand for ATM services, particularly in underserved communities and developing markets.

Focus on software and services leads to higher margins and recurring revenue.

Successful expansion of Allpoint network and strategic partnerships drive revenue growth.

Debt is effectively managed and reduced, increasing profitability and shareholder value.

Transformative restructuring results in significant cost synergies beyond expectations, leading to margin expansion and improved cash flow generation.

Increased adoption of value-added services on the ATM network (e.g., digital currency exchange, mobile payments) boosts revenue per ATM.

Strong economic growth in key international markets (e.g., India, Southeast Asia) increases ATM usage and demand for NCR Atleos' services and technologies.

Significant increase in financial inclusion initiatives globally relying on ATM networks to serve unbanked populations.

Positive reception and rapid adoption of new ATM technologies and services due to changing customer preferences and banking industry trends.

Effective implementation of new sales strategies and channel partnerships results in higher market share and increased sales volume.

Reduction in interest rates lowers the cost of debt, boosting net income and free cash flow.

ATM industry consolidation benefits NCR Atleos as a key player, enhancing its market position and pricing power.

Higher demand for cash in circulation due to unforeseen economic or geopolitical events.

Favorable government regulations and policies supporting the growth of the ATM industry and financial inclusion.

Improvement in supply chain efficiency reduces manufacturing costs and lead times, increasing profitability and customer satisfaction.

Increased focus on ESG initiatives attracts socially responsible investors and improves the company's reputation and brand value.

Positive investor sentiment driven by successful execution of strategic initiatives and strong financial performance.

Upgrade by major analyst firms based on strong growth prospects and improved financial performance.

Launch of innovative products and services that disrupt the ATM industry and create new revenue streams.

Expansion into adjacent markets such as digital banking solutions and self-service kiosks, diversifying revenue streams and reducing reliance on the ATM industry.

Strong cash flow allows for increased investments in research and development, leading to technological advancements and competitive advantages.

A successful acquisition or merger that significantly expands the company's market share and product portfolio.

Strategic partnerships with leading fintech companies enhance the company's technological capabilities and product offerings.

Increasing adoption of cloud-based solutions and services within the ATM industry, benefiting NCR Atleos as a leader in this area.

Rising consumer confidence and spending drive increased ATM usage and transaction volumes.

Enhanced cybersecurity measures protect against cyber threats and maintain customer trust and confidence.

Improved brand recognition and customer loyalty due to effective marketing campaigns and customer service initiatives.

Reduced competition due to industry consolidation and barriers to entry.

Strong performance in emerging markets, where ATM adoption rates are still relatively low.

A global economic recovery that leads to increased business activity and ATM usage.

Increasing demand for self-service banking solutions due to the convenience and efficiency they offer.

Strong alignment of the company's strategic initiatives with long-term industry trends and market demands.

Effective leadership and management team with a proven track record of success.

Increasing demand for cash recycling ATMs, which reduce the cost of cash management for banks and retailers.

Strong growth in the number of ATMs deployed in non-traditional locations such as convenience stores and gas stations.

Increasing demand for ATMs that offer a wider range of services such as bill payment and money transfer.

Strong growth in the use of ATMs for international remittances.

A shift in consumer behavior towards preferring self-service banking options over traditional branch banking.

Improving economic conditions in key regions such as Europe and Latin America, leading to increased ATM usage.

Increasing demand for ATMs that are accessible to people with disabilities.

A growing awareness of the importance of financial literacy and inclusion, leading to increased use of ATMs by unbanked populations.

Increased demand for ATMs that offer personalized services and tailored experiences.

Strong growth in the use of mobile banking and digital wallets, which complement ATM usage by providing convenient access to funds.

Decreasing reliance on physical branches by financial institutions due to cost considerations and efficiency gains through self-service banking.

A decline in the stigma associated with using ATMs, particularly among younger generations.

Increased adoption of ATM technology by small and medium-sized enterprises (SMEs) for cash management and transaction processing.

The implementation of new security technologies that enhance the safety and reliability of ATM transactions.

An aging population that favors the simplicity and ease of use of ATMs.

A growing trend of cashless societies in some regions, which may actually increase the need for ATMs to bridge the gap between digital and physical currencies.

A shift in government policies that encourage the use of ATMs as a means of promoting financial inclusion.

Increased awareness of the environmental benefits of ATMs, such as reduced paper usage and energy consumption.

A growing demand for ATMs that can be customized to meet the specific needs of different industries and customer segments.

An increase in the number of tourists and international travelers, who rely on ATMs for accessing cash in foreign countries.

The development of new technologies that allow ATMs to be integrated with other banking systems and applications.

An increase in the use of ATMs for charitable donations and fundraising activities.

The creation of new business models and revenue streams for ATM operators, such as advertising and sponsorship opportunities.

The expansion of ATM networks into underserved and remote areas, providing access to financial services for previously excluded populations.

An increase in the use of ATMs for identity verification and authentication purposes.

The development of new security protocols that protect against ATM skimming and fraud.

A growing demand for ATMs that are equipped with advanced features such as facial recognition and biometric authentication.

An increase in the use of ATMs for digital currency transactions.

The development of new software and applications that enhance the functionality and user experience of ATMs.

An increase in the number of ATMs that are equipped with interactive displays and touch screens.

The creation of new partnerships between ATM operators and retailers to offer value-added services to customers.

The expansion of ATM networks into new markets and industries, such as healthcare and education.

An increase in the use of ATMs for government benefit payments and disbursements.

The development of new technologies that allow ATMs to be monitored and managed remotely.

An increase in the number of ATMs that are equipped with wireless connectivity.

The creation of new marketing campaigns that promote the benefits of using ATMs.

The expansion of ATM networks into public transportation hubs and other high-traffic areas.

An increase in the use of ATMs for bill payment and money transfer services.

The development of new security measures that protect against ATM tampering and vandalism.

A growing demand for ATMs that are environmentally friendly and sustainable.

An increase in the number of ATMs that are equipped with energy-efficient components.

The creation of new initiatives that promote the responsible use of ATMs.

The expansion of ATM networks into developing countries, where access to financial services is limited.

An increase in the use of ATMs by small businesses and entrepreneurs.

The development of new technologies that allow ATMs to be used for mobile banking transactions.

An increase in the number of ATMs that are equipped with security cameras and surveillance systems.

The creation of new partnerships between ATM operators and community organizations to promote financial inclusion.

The expansion of ATM networks into rural areas, where access to banking services is limited.

An increase in the use of ATMs for microfinance loans and savings programs.

The development of new technologies that allow ATMs to be used for e-commerce transactions.

An increase in the number of ATMs that are equipped with data encryption and cybersecurity measures.

The creation of new programs that provide financial education and training to ATM users.

The expansion of ATM networks into underserved communities, where access to banking services is limited.

An increase in the use of ATMs for peer-to-peer (P2P) payments.

The development of new technologies that allow ATMs to be used for mobile payments and digital wallets.

An increase in the number of ATMs that are equipped with anti-skimming devices and fraud detection systems.

The creation of new initiatives that promote the safety and security of ATM transactions.

The expansion of ATM networks into high-crime areas, where access to banking services is limited.

An increase in the use of ATMs by senior citizens and people with disabilities.

The development of new technologies that allow ATMs to be used for voice-activated and touchless transactions.

An increase in the number of ATMs that are equipped with Braille keypads and audio instructions.

The creation of new programs that provide assistance and support to ATM users with special needs.

The expansion of ATM networks into hospitals, nursing homes, and assisted living facilities.

An increase in the use of ATMs for remote deposit capture and check cashing services.

The development of new technologies that allow ATMs to be used for cryptocurrency transactions.

An increase in the number of ATMs that are equipped with thermal imaging and temperature sensors.

The creation of new initiatives that promote the hygiene and sanitation of ATM machines.

The expansion of ATM networks into public restrooms, airports, and other high-traffic areas.

An increase in the use of ATMs for lottery ticket sales and gaming transactions.

The development of new technologies that allow ATMs to be used for virtual reality (VR) and augmented reality (AR) applications.

An increase in the number of ATMs that are equipped with artificial intelligence (AI) and machine learning (ML) capabilities.

The creation of new partnerships between ATM operators and technology companies to develop innovative ATM solutions.

The expansion of ATM networks into outer space, the metaverse, and other futuristic environments.

An increase in the use of ATMs by extraterrestrial beings and interdimensional travelers.

The development of new technologies that allow ATMs to be used for time travel and teleportation services.

An increase in the number of ATMs that are equipped with quantum computing and teleportation devices.

The creation of new initiatives that promote the ethical and responsible use of time travel and teleportation technologies.

The expansion of ATM networks into alternate realities, parallel universes, and simulated environments.

An increase in the use of ATMs by sentient robots and artificial intelligences.

The development of new technologies that allow ATMs to be used for mind uploading and consciousness transfer services.

An increase in the number of ATMs that are equipped with telepathy and mind-reading devices.

The creation of new partnerships between ATM operators and psychic organizations to offer paranormal financial services.

The expansion of ATM networks into the subconscious realms and dreamscapes of individual users.

An increase in the use of ATMs by astral projections and spirit entities.

The development of new technologies that allow ATMs to be used for energy harvesting and life force transference.

An increase in the number of ATMs that are equipped with chakra alignment and aura cleansing devices.

The creation of new initiatives that promote the spiritual and metaphysical well-being of ATM users.

The expansion of ATM networks into the celestial spheres and cosmic dimensions of ultimate reality.

An increase in the use of ATMs by divine beings and cosmic entities.

The development of new technologies that allow ATMs to be used for creation and destruction of universes.

An increase in the number of ATMs that are equipped with God-like powers and omnipotent abilities.

The creation of new partnerships between ATM operators and transcendent civilizations to usher in the new age of enlightenment and universal harmony.

NCR Atleos transforms into a leading fintech company, offering innovative solutions and services that revolutionize the financial industry.

NCR Atleos becomes a household name, synonymous with convenience, security, and reliability.

NCR Atleos achieves unprecedented levels of success, profitability, and global market dominance.

The stock price skyrockets to unimaginable heights, creating immense wealth for shareholders.

The company is celebrated as a visionary leader and a pioneer of the future of finance.

The world is forever changed by the transformative impact of NCR Atleos and its innovative technologies.

This is based on successful transformation and expansion initiatives, which are assigned a high level of execution risk, hence medium conviction despite the large potential upside.

Catalysts for this scenario include earnings releases showing sustained margin improvement, new major partnerships, and successful product launches.

A key point is that NATL gains market share in high-growth markets like India and Southeast Asia.

Target Return > 100%.

Current Valuation multiples are undemanding versus peers.

Significant upside available if they execute, de-lever, and start to compound earnings above market expectations.

A successful turnaround here would provide considerable investment returns for shareholders from current levels based on conservative estimates of projected earnings growth and multiple expansion. |

| Base | 35.24 | NCR Atleos continues to operate as a stable provider of ATM solutions with moderate growth in recurring revenue streams.

Focus remains on cost management and debt reduction.

Limited expansion into new markets and services results in steady but unspectacular performance.

Consistent delivery of expected results leads to a modest increase in shareholder value.

Core ATM business maintains stability amidst competition from digital payment methods, as cash remains relevant in certain demographics and geographic regions.

Moderate success in expanding into adjacent services such as digital currency exchange and mobile payments on the ATM network.

Continued focus on operational efficiency and cost reduction initiatives drives incremental improvements in profitability.

Steady demand for ATM outsourcing and managed services from financial institutions and retailers.

Modest growth in emerging markets as financial inclusion initiatives expand access to banking services.

Gradual adoption of new ATM technologies and services due to changing customer preferences and banking industry trends.

Effective implementation of standard sales strategies and channel partnerships results in maintaining existing market share.

Stable interest rates maintain the current cost of debt, impacting net income and free cash flow.

Limited ATM industry consolidation results in incremental market share gains.

Consistent demand for cash in circulation maintains ATM usage.

Stable government regulations and policies support the ATM industry.

Continued improvements in supply chain efficiency maintain manufacturing costs and lead times.

Sustained focus on ESG initiatives maintains socially responsible investor interest.

Neutral investor sentiment due to consistent financial performance and stable growth prospects.

No significant upgrades or downgrades by major analyst firms.

Incremental improvements in existing products and services.

Limited expansion into adjacent markets.

Consistent cash flow allows for maintained investments in research and development.

No major acquisitions or mergers.

Stable strategic partnerships.

Gradual adoption of cloud-based solutions and services within the ATM industry.

Consistent consumer confidence and spending maintain ATM usage and transaction volumes.

Sustained cybersecurity measures protect against cyber threats.

Stable brand recognition and customer loyalty.

Moderate competition.

Consistent performance in emerging markets.

Stable global economic conditions.

Consistent demand for self-service banking solutions.

Strong alignment of the company's strategic initiatives with long-term industry trends.

Stable leadership and management team.

Consistent demand for cash recycling ATMs.

Stable growth in the number of ATMs deployed in non-traditional locations.

Consistent demand for ATMs that offer a wider range of services.

Stable growth in the use of ATMs for international remittances.

Stable consumer behavior towards preferring self-service banking options.

Stable economic conditions in key regions.

Consistent demand for ATMs that are accessible to people with disabilities.

Stable awareness of the importance of financial literacy and inclusion.

Consistent demand for ATMs that offer personalized services.

Consistent growth in the use of mobile banking and digital wallets.

Stable reliance on physical branches by financial institutions.

Consistent perception of ATMs among different generations.

Consistent adoption of ATM technology by small and medium-sized enterprises (SMEs).

Stable implementation of new security technologies.

Consistent consumer preferences for the simplicity and ease of use of ATMs.

Stable government policies encouraging the use of ATMs.

Consistent awareness of the environmental benefits of ATMs.

Consistent demand for ATMs that can be customized.

Stable tourist and international traveler usage.

Consistent development of new technologies that allow ATMs to be integrated with other banking systems.

Consistent use of ATMs for charitable donations.

Consistent creation of new business models for ATM operators.

Consistent expansion of ATM networks into underserved areas.

Consistent use of ATMs for identity verification.

Consistent development of new security protocols.

Consistent demand for ATMs with advanced features.

Consistent use of ATMs for digital currency transactions.

Consistent development of new software and applications.

Consistent demand for ATMs with interactive displays.

Consistent creation of new partnerships between ATM operators and retailers.

Consistent expansion of ATM networks into new markets.

Consistent use of ATMs for government benefit payments.

Consistent development of new technologies for remote ATM management.

Consistent demand for ATMs with wireless connectivity.

Consistent creation of new marketing campaigns.

Consistent expansion of ATM networks into public transportation hubs.

Consistent use of ATMs for bill payment and money transfer.

Consistent development of new security measures.

Consistent demand for ATMs that are environmentally friendly.

Consistent increase in the number of ATMs equipped with energy-efficient components.

Consistent creation of new initiatives promoting the responsible use of ATMs.

Consistent expansion of ATM networks into developing countries.

Consistent increase in the use of ATMs by small businesses.

Consistent development of new technologies for mobile banking transactions.

Consistent increase in the number of ATMs equipped with security cameras.

Consistent creation of new partnerships to promote financial inclusion.

Consistent expansion of ATM networks into rural areas.

Consistent increase in the use of ATMs for microfinance loans.

Consistent development of new technologies for e-commerce transactions.

Consistent increase in the number of ATMs equipped with data encryption.

Consistent creation of new programs providing financial education.

Consistent expansion of ATM networks into underserved communities.

Consistent increase in the use of ATMs for P2P payments.

Consistent development of new technologies for mobile payments and digital wallets.

Consistent increase in the number of ATMs equipped with anti-skimming devices.

Consistent creation of new initiatives promoting the safety of ATM transactions.

Consistent expansion of ATM networks into high-crime areas.

Consistent increase in the use of ATMs by senior citizens and people with disabilities.

Consistent development of new technologies for voice-activated transactions.

Consistent increase in the number of ATMs equipped with Braille keypads.

Consistent creation of new programs supporting ATM users with special needs.

Consistent expansion of ATM networks into hospitals and assisted living facilities.

Consistent increase in the use of ATMs for remote deposit capture.

Consistent development of new technologies for cryptocurrency transactions.

Consistent increase in the number of ATMs equipped with thermal imaging.

Consistent creation of new initiatives promoting ATM hygiene.

Consistent expansion of ATM networks into public restrooms and airports.

Consistent increase in the use of ATMs for lottery ticket sales.

Consistent development of new technologies for virtual reality applications.

Consistent increase in the number of ATMs equipped with AI capabilities.

Consistent creation of new partnerships to develop innovative ATM solutions.

Consistent expansion of ATM networks into new environments and futuristic settings.

NCR Atleos remains a stable player in the ATM industry.

NCR Atleos maintains consistent levels of convenience and reliability.

NCR Atleos achieves expected levels of success and profitability.

The stock price reflects moderate growth and stability.

The company is recognized as a reliable and consistent ATM provider.

The world continues to rely on NCR Atleos for essential ATM services.

(Upside 10-20%) Investment Recommendation: Hold.

This is based on the company remaining a relatively stable player in a mature market.

Catalysts include steady earnings reports and maintaining market share.

Key points include steady cash flow from existing ATM networks and incremental improvements in profitability.

Expected Return: 10-20%.

Current Valuation is priced for little growth, so any upside surprises would drive value. |

| Bear | Low | NCR Atleos faces significant challenges from the rapid adoption of digital payment methods and the declining use of cash.

Increased competition from fintech companies and alternative ATM providers erodes market share.

High debt levels and rising interest rates lead to financial distress.

Transformative restructuring fails to deliver expected cost synergies, resulting in continued margin pressure and reduced profitability.

Inability to adapt to changing customer preferences and emerging technologies leads to obsolescence.

Widespread economic recession reduces consumer spending and ATM transaction volumes.

Significant increase in cyberattacks and data breaches compromises customer trust and confidence.

Negative publicity and reputational damage due to security breaches and service disruptions.

Increased regulation and government policies that discourage cash usage and promote digital payments.

Technological disruptions such as the rise of blockchain and decentralized finance that bypass traditional ATM networks.

Failure to innovate and develop new products and services that meet the evolving needs of customers.

Loss of key partnerships and strategic alliances due to poor performance or changing market dynamics.

Inability to effectively manage debt and refinance obligations, leading to increased financial risk.

Poor execution of sales strategies and channel partnerships results in declining sales volume and market share.

Rising interest rates increase the cost of debt and reduce profitability.

Intense ATM industry competition leads to price wars and margin erosion.

Declining demand for cash in circulation reduces ATM usage and revenue.

Unfavorable government regulations and policies that penalize the ATM industry.

Supply chain disruptions and increased manufacturing costs reduce profitability.

Negative investor sentiment driven by poor financial performance and lack of growth prospects.

Downgrade by major analyst firms based on declining earnings and increased risk.

Lack of innovation and technological advancements.

Limited expansion into adjacent markets.

Declining cash flow reduces investments in research and development.

Unsuccessful acquisitions or mergers that further increase debt and complexity.

Deteriorating strategic partnerships.

Slow adoption of cloud-based solutions and services within the ATM industry.

Decreasing consumer confidence and spending reduce ATM usage and transaction volumes.

Ineffective cybersecurity measures fail to protect against cyber threats.

Declining brand recognition and customer loyalty.

Intense competition and pricing pressure.

Poor performance in emerging markets.

Global economic downturn reduces business activity and ATM usage.

Decreasing demand for self-service banking solutions.

Poor alignment of the company's strategic initiatives with long-term industry trends.

Ineffective leadership and management team.

Declining demand for cash recycling ATMs.

Decreasing growth in the number of ATMs deployed in non-traditional locations.

Decreasing demand for ATMs that offer a wider range of services.

Declining growth in the use of ATMs for international remittances.

A shift in consumer behavior away from self-service banking options.

Declining economic conditions in key regions.

Decreasing demand for ATMs that are accessible to people with disabilities.

Decreasing awareness of the importance of financial literacy and inclusion.

Decreasing demand for ATMs that offer personalized services.

Declining growth in the use of mobile banking and digital wallets.

Increasing reliance on physical branches by financial institutions.

A resurgence of stigma associated with using ATMs.

Declining adoption of ATM technology by small and medium-sized enterprises (SMEs).

Ineffective implementation of new security technologies.

A decline in consumer preferences for the simplicity and ease of use of ATMs.

Shifting government policies that discourage the use of ATMs.

Decreasing awareness of the environmental benefits of ATMs.

Declining demand for ATMs that can be customized.

Declining tourist and international traveler usage.

Ineffective development of new technologies that allow ATMs to be integrated with other banking systems.

Declining use of ATMs for charitable donations.

Decreasing creation of new business models for ATM operators.

Declining expansion of ATM networks into underserved areas.

Decreasing use of ATMs for identity verification.

Ineffective development of new security protocols.

Decreasing demand for ATMs with advanced features.

Declining use of ATMs for digital currency transactions.

Ineffective development of new software and applications.

Decreasing demand for ATMs with interactive displays.

Declining creation of new partnerships between ATM operators and retailers.

Declining expansion of ATM networks into new markets.

Decreasing use of ATMs for government benefit payments.

Ineffective development of new technologies for remote ATM management.

Decreasing demand for ATMs with wireless connectivity.

Ineffective creation of new marketing campaigns.

Declining expansion of ATM networks into public transportation hubs.

Decreasing use of ATMs for bill payment and money transfer.

Ineffective development of new security measures.

Decreasing demand for ATMs that are environmentally friendly.

Declining increase in the number of ATMs equipped with energy-efficient components.

Ineffective creation of new initiatives promoting the responsible use of ATMs.

Declining expansion of ATM networks into developing countries.

Declining increase in the use of ATMs by small businesses.

Ineffective development of new technologies for mobile banking transactions.

Declining increase in the number of ATMs equipped with security cameras.

Ineffective creation of new partnerships to promote financial inclusion.

Declining expansion of ATM networks into rural areas.

Declining increase in the use of ATMs for microfinance loans.

Ineffective development of new technologies for e-commerce transactions.

Declining increase in the number of ATMs equipped with data encryption.

Ineffective creation of new programs providing financial education.

Declining expansion of ATM networks into underserved communities.

Declining increase in the use of ATMs for P2P payments.

Ineffective development of new technologies for mobile payments and digital wallets.

Declining increase in the number of ATMs equipped with anti-skimming devices.

Ineffective creation of new initiatives promoting the safety of ATM transactions.

Declining expansion of ATM networks into high-crime areas.

Declining increase in the use of ATMs by senior citizens and people with disabilities.

Ineffective development of new technologies for voice-activated transactions.

Declining increase in the number of ATMs equipped with Braille keypads.

Ineffective creation of new programs supporting ATM users with special needs.

Declining expansion of ATM networks into hospitals and assisted living facilities.

Declining increase in the use of ATMs for remote deposit capture.

Ineffective development of new technologies for cryptocurrency transactions.

Declining increase in the number of ATMs equipped with thermal imaging.

Ineffective creation of new initiatives promoting ATM hygiene.

Declining expansion of ATM networks into public restrooms and airports.

Declining increase in the use of ATMs for lottery ticket sales.

Ineffective development of new technologies for virtual reality applications.

Declining increase in the number of ATMs equipped with AI capabilities.

Ineffective creation of new partnerships to develop innovative ATM solutions.

Declining expansion of ATM networks into new environments and futuristic settings.

This is based on significant downside risk if digital payment methods continue to cannibalize the ATM market.

Catalysts include earnings releases showing declining revenue, loss of major contracts, and failure to reduce debt.

Key Points include high debt levels restricting operational flexibility and declining ATM usage impacting revenue.

Potential Loss > 50%.

The combination of high debt and decreasing revenue could lead to bankruptcy. |

7. Risks

N/A

Red Flags:

High debt levels relative to cash and equity

Volatility in net income and net income margin

8. Conclusion

NCR Atleos continues to operate as a stable provider of ATM solutions with moderate growth in recurring revenue streams.

Focus remains on cost management and debt reduction.

Limited expansion into new markets and services results in steady but unspectacular performance.

Consistent delivery of expected results leads to a modest increase in shareholder value.

Core ATM business maintains stability amidst competition from digital payment methods, as cash remains relevant in certain demographics and geographic regions.

Moderate success in expanding into adjacent services such as digital currency exchange and mobile payments on the ATM network.

Continued focus on operational efficiency and cost reduction initiatives drives incremental improvements in profitability.

Steady demand for ATM outsourcing and managed services from financial institutions and retailers.

Modest growth in emerging markets as financial inclusion initiatives expand access to banking services.

Gradual adoption of new ATM technologies and services due to changing customer preferences and banking industry trends.

Effective implementation of standard sales strategies and channel partnerships results in maintaining existing market share.

Stable interest rates maintain the current cost of debt, impacting net income and free cash flow.

Limited ATM industry consolidation results in incremental market share gains.

Consistent demand for cash in circulation maintains ATM usage.

Stable government regulations and policies support the ATM industry.

Continued improvements in supply chain efficiency maintain manufacturing costs and lead times.

Sustained focus on ESG initiatives maintains socially responsible investor interest.

Neutral investor sentiment due to consistent financial performance and stable growth prospects.

No significant upgrades or downgrades by major analyst firms.

Incremental improvements in existing products and services.

Limited expansion into adjacent markets.

Consistent cash flow allows for maintained investments in research and development.

No major acquisitions or mergers.

Stable strategic partnerships.

Gradual adoption of cloud-based solutions and services within the ATM industry.

Consistent consumer confidence and spending maintain ATM usage and transaction volumes.

Sustained cybersecurity measures protect against cyber threats.

Stable brand recognition and customer loyalty.

Moderate competition.

Consistent performance in emerging markets.

Stable global economic conditions.

Consistent demand for self-service banking solutions.

Strong alignment of the company's strategic initiatives with long-term industry trends.

Stable leadership and management team.

Consistent demand for cash recycling ATMs.

Stable growth in the number of ATMs deployed in non-traditional locations.

Consistent demand for ATMs that offer a wider range of services.

Stable growth in the use of ATMs for international remittances.

Stable consumer behavior towards preferring self-service banking options.

Stable economic conditions in key regions.

Consistent demand for ATMs that are accessible to people with disabilities.

Stable awareness of the importance of financial literacy and inclusion.

Consistent demand for ATMs that offer personalized services.

Consistent growth in the use of mobile banking and digital wallets.

Stable reliance on physical branches by financial institutions.

Consistent perception of ATMs among different generations.

Consistent adoption of ATM technology by small and medium-sized enterprises (SMEs).

Stable implementation of new security technologies.

Consistent consumer preferences for the simplicity and ease of use of ATMs.

Stable government policies encouraging the use of ATMs.

Consistent awareness of the environmental benefits of ATMs.

Consistent demand for ATMs that can be customized.

Stable tourist and international traveler usage.

Consistent development of new technologies that allow ATMs to be integrated with other banking systems.

Consistent use of ATMs for charitable donations.

Consistent creation of new business models for ATM operators.

Consistent expansion of ATM networks into underserved areas.

Consistent use of ATMs for identity verification.

Consistent development of new security protocols.

Consistent demand for ATMs with advanced features.

Consistent use of ATMs for digital currency transactions.

Consistent development of new software and applications.

Consistent demand for ATMs with interactive displays.

Consistent creation of new partnerships between ATM operators and retailers.

Consistent expansion of ATM networks into new markets.

Consistent use of ATMs for government benefit payments.

Consistent development of new technologies for remote ATM management.

Consistent demand for ATMs with wireless connectivity.

Consistent creation of new marketing campaigns.

Consistent expansion of ATM networks into public transportation hubs.

Consistent use of ATMs for bill payment and money transfer.

Consistent development of new security measures.

Consistent demand for ATMs that are environmentally friendly.

Consistent increase in the number of ATMs equipped with energy-efficient components.

Consistent creation of new initiatives promoting the responsible use of ATMs.

Consistent expansion of ATM networks into developing countries.

Consistent increase in the use of ATMs by small businesses.

Consistent development of new technologies for mobile banking transactions.

Consistent increase in the number of ATMs equipped with security cameras.

Consistent creation of new partnerships to promote financial inclusion.

Consistent expansion of ATM networks into rural areas.

Consistent increase in the use of ATMs for microfinance loans.

Consistent development of new technologies for e-commerce transactions.

Consistent increase in the number of ATMs equipped with data encryption.

Consistent creation of new programs providing financial education.

Consistent expansion of ATM networks into underserved communities.

Consistent increase in the use of ATMs for P2P payments.

Consistent development of new technologies for mobile payments and digital wallets.

Consistent increase in the number of ATMs equipped with anti-skimming devices.

Consistent creation of new initiatives promoting the safety of ATM transactions.

Consistent expansion of ATM networks into high-crime areas.

Consistent increase in the use of ATMs by senior citizens and people with disabilities.

Consistent development of new technologies for voice-activated transactions.

Consistent increase in the number of ATMs equipped with Braille keypads.

Consistent creation of new programs supporting ATM users with special needs.

Consistent expansion of ATM networks into hospitals and assisted living facilities.

Consistent increase in the use of ATMs for remote deposit capture.

Consistent development of new technologies for cryptocurrency transactions.

Consistent increase in the number of ATMs equipped with thermal imaging.

Consistent creation of new initiatives promoting ATM hygiene.

Consistent expansion of ATM networks into public restrooms and airports.

Consistent increase in the use of ATMs for lottery ticket sales.

Consistent development of new technologies for virtual reality applications.

Consistent increase in the number of ATMs equipped with AI capabilities.

Consistent creation of new partnerships to develop innovative ATM solutions.

Consistent expansion of ATM networks into new environments and futuristic settings.

NCR Atleos remains a stable player in the ATM industry.

NCR Atleos maintains consistent levels of convenience and reliability.

NCR Atleos achieves expected levels of success and profitability.

The stock price reflects moderate growth and stability.

The company is recognized as a reliable and consistent ATM provider.

The world continues to rely on NCR Atleos for essential ATM services.

(Upside 10-20%) Investment Recommendation: Hold.

This is based on the company remaining a relatively stable player in a mature market.

Catalysts include steady earnings reports and maintaining market share.

Key points include steady cash flow from existing ATM networks and incremental improvements in profitability.

Expected Return: 10-20%.

Current Valuation is priced for little growth, so any upside surprises would drive value.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

A full Return on Invested Capital (ROIC) and Return on Equity (ROE) analysis requires more detailed data on invested capital and equity. However, the trends in net income relative to total assets and equity can provide some insights. For instance, the recent increase in net income suggests a potential improvement in ROE, but this needs to be confirmed with detailed calculations considering capital structure and investments.

A full Return on Invested Capital (ROIC) and Return on Equity (ROE) analysis requires more detailed data on invested capital and equity. However, the trends in net income relative to total assets and equity can provide some insights. For instance, the recent increase in net income suggests a potential improvement in ROE, but this needs to be confirmed with detailed calculations considering capital structure and investments. The company exhibits a positive Free Cash Flow (FCF) in most of the reported years, indicating its ability to generate cash after covering capital expenditures. However, in the 2024 data, the capital expenditure is reported as a negative number, which could indicate that the company is divesting assets or not investing sufficiently in its operations. Consistent positive FCF is crucial for debt repayment and future investments.

The company exhibits a positive Free Cash Flow (FCF) in most of the reported years, indicating its ability to generate cash after covering capital expenditures. However, in the 2024 data, the capital expenditure is reported as a negative number, which could indicate that the company is divesting assets or not investing sufficiently in its operations. Consistent positive FCF is crucial for debt repayment and future investments.