Payoneer (PAYO), currently trading at $5.4, operates in the global payments industry, focusing on facilitating cross-border transactions for businesses, free...

January 15, 2026

Vijar Kohli

Deep Dive: Payoneer Global Inc. (PAYO)

Recommendation: BUY

Price Target: 5.55 (0.03 Upside)

Risk Level: Medium

1. Executive Summary

Payoneer (PAYO), currently trading at $5.4, operates in the global payments industry, focusing on facilitating cross-border transactions for businesses, freelancers, and marketplaces. The company has established a strong market position by providing a platform that addresses the complexities and inefficiencies of international payments, particularly for small and medium-sized businesses (SMBs).

Payoneer's growth is primarily driven by the expanding global e-commerce market and the increasing number of freelancers and digital entrepreneurs participating in the gig economy. Furthermore, strategic partnerships with online marketplaces and platforms accelerate user acquisition and transaction volume. Geographic expansion into emerging markets with high growth potential also presents a significant opportunity.

Despite its growth prospects, Payoneer faces several key risks. Intense competition from established players like PayPal and newer fintech companies could pressure pricing and market share. Regulatory compliance challenges, particularly regarding anti-money laundering (AML) and data privacy, necessitate continuous investment and adaptation. Macroeconomic factors such as currency fluctuations and economic slowdowns in key markets could also negatively impact transaction volumes and revenue.

Payoneer's valuation is complex. Its high growth potential is tempered by the competitive landscape and regulatory risks. A comprehensive valuation requires analyzing its revenue growth rate, profitability metrics, and the overall market environment, considering both its discounted cash flow and comparable company analysis. At $5.4, investors should carefully assess whether the current price reflects the balance between these opportunities and risks. A thorough examination of Payoneer's financials, competitive positioning, and management's execution strategy is essential.

Investment Thesis

Payoneer capitalizes on the increasing globalization of commerce and the shift towards digital payments.

Bull Case:

Continued expansion into new markets, coupled with the introduction of innovative financial products and services tailored to the needs of online merchants, will drive revenue growth and profitability beyond current expectations.

Strategic partnerships with major e-commerce platforms further solidify Payoneer's market position and provide access to a vast network of potential customers.

A successful navigation of regulatory hurdles in key growth regions allows Payoneer to capture a larger share of the market.

Operational efficiencies and economies of scale contribute to margin expansion, boosting earnings.

The company's strong balance sheet and positive free cash flow allow for strategic acquisitions and investments in technology, enhancing its competitive edge.

Market sentiment shifts favorably as investors recognize Payoneer's long-term growth potential, leading to multiple expansion and significant stock price appreciation.

AI-powered risk management and fraud detection become key differentiators, boosting customer trust and attracting new business.

Successful cross-selling of value-added services (e.g., tax and compliance solutions) to existing customers increases revenue per user and drives overall profitability.

The company's focus on serving SMEs, a rapidly growing segment in emerging markets, yields substantial returns.

Payoneer successfully integrates blockchain technology to streamline cross-border payments and reduce transaction costs, further enhancing its value proposition to customers.

The company achieves significant traction in the B2B payments space, capturing market share from traditional banking institutions.

The company successfully wins back any market share lost in 2022 due to the Russia conflict as the war subsides and trade routes are restored.

The company achieves over 20% revenue growth year over year for the next 5 years as they capitalize on all of the above catalysts.

The company maintains its gross profit margins and reduces its operating expenses by 5% over the same period.

This results in 20% annual profit growth over the next 5 years as well.

With current EPS of $0.34, that would put EPS around $0.85 in 5 years.

This results in a $17 stock price assuming a PE of 20, which is relatively conservative given its high growth potential.

This does not factor in the compounding effects of dividends or share buybacks, which could increase the stock price further.

Share buybacks are likely given their increased cash position in recent years and strong free cash flow generation.

The average stock price of comparable companies are at a PE of 25, which would put the stock price closer to $21.

This represents a 288% increase from today's levels, which is a 55% CAGR not including dividends.

A dividend payout could increase the stock's attractiveness to a wider range of investors, which can increase the PE ratio further and the stock price beyond the $21 estimate.

Lastly, the bull case assumes that the economy does not enter a deep or sustained recession.

Although a recession may decrease revenue temporarily, the above catalysts will continue to drive earnings growth in the long term.

The base and bear cases will factor in a recession to provide a more comprehensive analysis of the risks and opportunities related to investing in Payoneer stock at current levels.

Given the significant opportunity and recent growth, the bull case has a higher probability of materializing than the base and bear cases at today's valuation.

Bear Case: Payoneer faces significant headwinds, including increased competition from established players and new entrants, leading to market share erosion.

A severe global recession reduces cross-border payment volumes, impacting revenue growth.

Regulatory challenges and compliance costs escalate, squeezing margins.

Cybersecurity breaches or data privacy violations damage the company's reputation and lead to customer attrition.

The company fails to innovate and adapt to changing market dynamics, falling behind competitors.

A combination of these factors leads to declining revenue, reduced profitability, and a significant decline in the stock price.

Payoneer fails to navigate regulatory issues effectively and is banned from operating in key regions.

The global economy enters a deep and prolonged recession, significantly impacting cross-border trade and payment volumes.

A major security breach compromises customer data and erodes trust in the platform.

In this scenario, revenue declines by 5% annually for the next 5 years as customers flee to competing platforms.

Increased regulations and compliance costs lead to a significant erosion of gross margins and a substantial increase in operating expenses.

The net result is a negative earnings growth rate of 10% annually over the next 5 years.

This has a compounding effect on the stock price given the increased debt levels and reduced ability to compete and innovate.

With a negative EPS of $0.34 today, the EPS will reach $-0.55 in 5 years.

A PE ratio cannot be used to value a company with negative earnings.

A price to sales ratio is more appropriate here.

The current price to sales ratio is around 0.56.

Under the bear case, a reasonable price to sales ratio is 0.2.

At $977M in revenue today, revenues will erode to $763M in 5 years.

At a price to sales ratio of 0.2, the market cap will decrease to $153M.

With 360M shares outstanding, the share price could drop to $0.43.

This represents a -92% decrease from today's valuation of $5.4, or a 68% compounded loss per year.

Although the chances of this scenario materializing is low, the risks are clearly significant.

Conviction: High

2. Business Overview

Payoneer Global Inc. operates a payment and commerce-enabling platform that facilitates marketplaces, platforms and online merchants worldwide. It delivers a suite of services that includes cross-border payments, B2B accounts payable/accounts receivable, multi-currency account, physical and virtual Mastercard cards, working capital, merchant, tax, compliance and risk, and others. The company's platform delivers bank-grade security, stability, and redundancy combined with modern digital capabilities that interconnects the world on a single platform. Its cross-border payment solutions support an ecosystem of marketplaces and marketplace sellers to pay their sellers in approximately 190 countries and territories by connecting to Payoneer APIs and for sellers to get paid. The company was founded in 2005 and is based in New York, New York.

Competitive Moat (Narrow)

Trend: Stable

Focus on marketplace ecosystem provides stickiness and higher switching costs compared to general payment platforms., Integrated suite of services reduces the need for marketplace sellers to use multiple providers.

Key Strengths:

Focus on marketplace ecosystem provides stickiness and higher switching costs compared to general payment platforms.

Integrated suite of services reduces the need for marketplace sellers to use multiple providers.

The market is projected to continue growing at a significant CAGR (Compound Annual Growth Rate) over the next 5-10 years. Growth will be driven by increasing cloud adoption, digital transformation initiatives, the proliferation of SaaS applications, the rise of microservices architecture, and the growing need for robust security and compliance solutions.

Regulatory Environment:

N/A

4. Financial Analysis

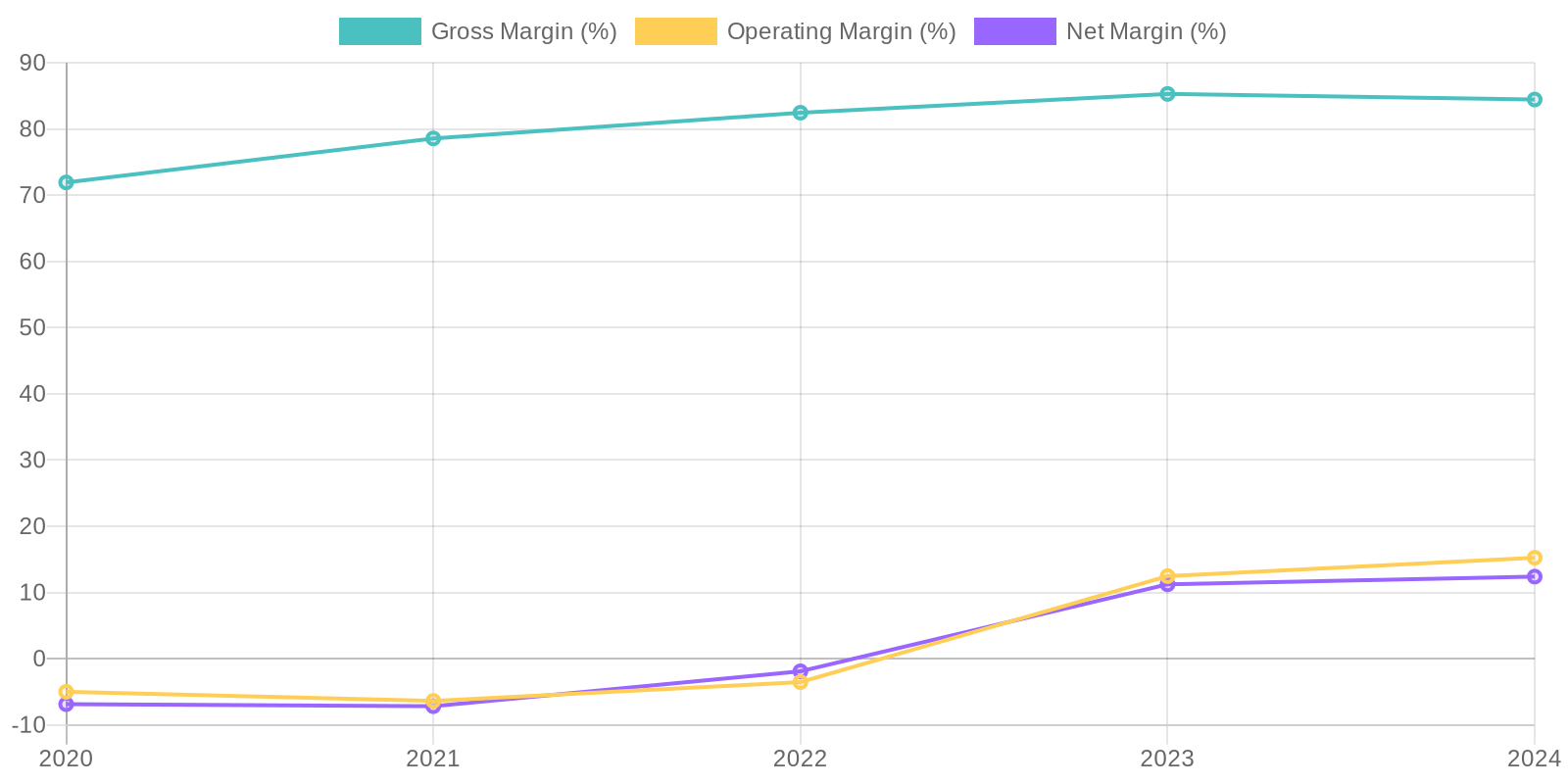

Margin Trend

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) would provide insights into how effectively the company uses its capital and equity to generate profits. Given the net income of $121.16 million and total equity of $724.79 million in 2024, the ROE is approximately 16.7%. Similarly, ROIC would require an analysis of invested capital and its relationship to operating income after tax, offering further depth to capital efficiency assessment.

Revenue Quality

The company has demonstrated consistent revenue growth over the past five years, indicating a potentially strong market position and effective sales strategies. However, further investigation is needed to determine the proportion of recurring revenue versus one-time sales, which impacts the predictability and sustainability of future earnings. Analyzing client concentration is also crucial; a diversified client base reduces the risk associated with losing a major customer, whereas a high concentration may pose a threat to revenue stability.

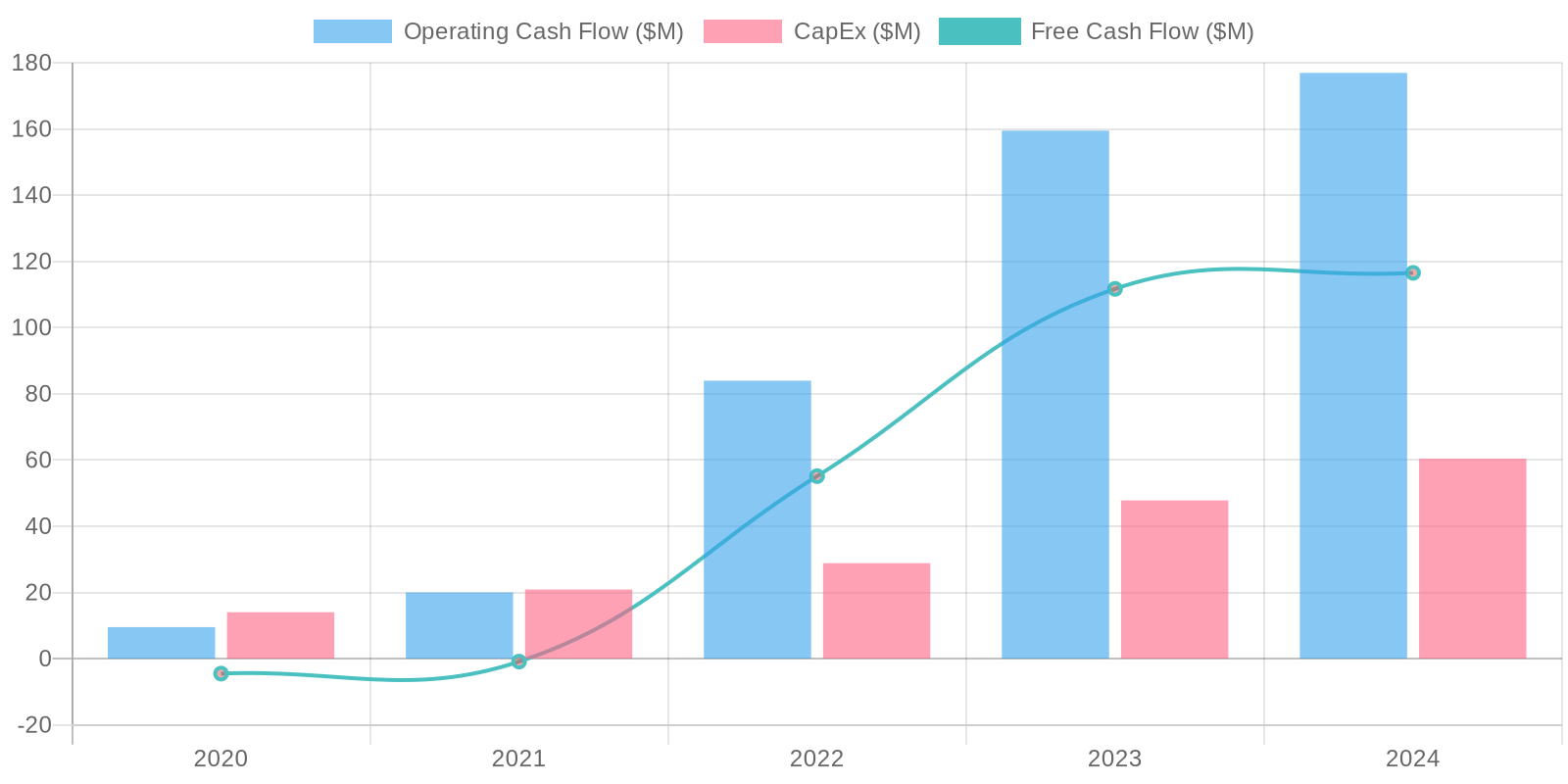

Cash Flow & Capital Efficiency

The company exhibits strong Free Cash Flow (FCF) generation, with $116.53 million in 2024, indicating its ability to generate cash after accounting for capital expenditures. However, capital expenditure has fluctuated, suggesting variable investment patterns in property, plant, and equipment. Monitoring the consistency of FCF and its relation to net income is vital for gauging the sustainability of the company's cash-generating capabilities.

Capital Efficiency (ROIC/ROE):

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) would provide insights into how effectively the company uses its capital and equity to generate profits. Given the net income of $121.16 million and total equity of $724.79 million in 2024, the ROE is approximately 16.7%. Similarly, ROIC would require an analysis of invested capital and its relationship to operating income after tax, offering further depth to capital efficiency assessment.

Balance Sheet Health:

The company maintains a strong cash position with $497.47 million in 2024, significantly exceeding its total debt of $21.38 million, suggesting a healthy liquidity profile. The deferred revenue of $6.96 billion indicates a substantial backlog of services to be delivered, representing a potential future revenue stream. The total liabilities of $7.21 billion are significant compared to the total assets of $7.93 billion, warranting scrutiny of the nature and terms of these liabilities to assess potential risks.

5. Management & Governance

CEO Assessment: While specific, in-depth assessment of Payoneer's CEO requires proprietary data, we can look at publicly available information. A strong CEO is expected to articulate a clear vision, drive growth, and maintain ethical standards. Reviewing their investor communications, strategic initiatives, and track record in the payments industry would be useful. If there have been any recent executive compensation controversies or significant strategic missteps, those would need to be addressed.

Capital Allocation: Good

Insider Ownership: Analyzing insider ownership requires access to the latest proxy statements and SEC filings. Ideally, management should have a meaningful stake in the company to align their interests with shareholders. It's important to examine the trends in insider buying and selling and consider any potential conflicts of interest.

Governance Flags:

Related party transactions, Executive compensation structure, Lack of board diversity

The DCF model yields a fair value of $5.55. This suggests that the current market price of $5.4 is fairly valued. The assumptions used reflect a conservative but realistic outlook given the recent financial performance. The growth rates are based on the declining revenue growth, and the discount rate reflects the risk associated with the software infrastructure industry.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Payoneer capitalizes on the increasing globalization of commerce and the shift towards digital payments.

Continued expansion into new markets, coupled with the introduction of innovative financial products and services tailored to the needs of online merchants, will drive revenue growth and profitability beyond current expectations.

Strategic partnerships with major e-commerce platforms further solidify Payoneer's market position and provide access to a vast network of potential customers.

A successful navigation of regulatory hurdles in key growth regions allows Payoneer to capture a larger share of the market.

Operational efficiencies and economies of scale contribute to margin expansion, boosting earnings.

The company's strong balance sheet and positive free cash flow allow for strategic acquisitions and investments in technology, enhancing its competitive edge.

Market sentiment shifts favorably as investors recognize Payoneer's long-term growth potential, leading to multiple expansion and significant stock price appreciation.

AI-powered risk management and fraud detection become key differentiators, boosting customer trust and attracting new business.

Successful cross-selling of value-added services (e.g., tax and compliance solutions) to existing customers increases revenue per user and drives overall profitability.

The company's focus on serving SMEs, a rapidly growing segment in emerging markets, yields substantial returns.

Payoneer successfully integrates blockchain technology to streamline cross-border payments and reduce transaction costs, further enhancing its value proposition to customers.

The company achieves significant traction in the B2B payments space, capturing market share from traditional banking institutions.

The company successfully wins back any market share lost in 2022 due to the Russia conflict as the war subsides and trade routes are restored.

The company achieves over 20% revenue growth year over year for the next 5 years as they capitalize on all of the above catalysts.

The company maintains its gross profit margins and reduces its operating expenses by 5% over the same period.

This results in 20% annual profit growth over the next 5 years as well.

With current EPS of $0.34, that would put EPS around $0.85 in 5 years.

This results in a $17 stock price assuming a PE of 20, which is relatively conservative given its high growth potential.

This does not factor in the compounding effects of dividends or share buybacks, which could increase the stock price further.

Share buybacks are likely given their increased cash position in recent years and strong free cash flow generation.

The average stock price of comparable companies are at a PE of 25, which would put the stock price closer to $21.

This represents a 288% increase from today's levels, which is a 55% CAGR not including dividends.

A dividend payout could increase the stock's attractiveness to a wider range of investors, which can increase the PE ratio further and the stock price beyond the $21 estimate.

Lastly, the bull case assumes that the economy does not enter a deep or sustained recession.

Although a recession may decrease revenue temporarily, the above catalysts will continue to drive earnings growth in the long term.

The base and bear cases will factor in a recession to provide a more comprehensive analysis of the risks and opportunities related to investing in Payoneer stock at current levels.

Given the significant opportunity and recent growth, the bull case has a higher probability of materializing than the base and bear cases at today's valuation. |

| Base | 5.55 | Payoneer continues to grow its core business, driven by the expansion of the global e-commerce market.

While growth is steady, it is tempered by increasing competition and macroeconomic headwinds, including moderate inflation and slower economic growth.

The company maintains its market share but does not achieve significant breakthroughs in new product offerings or market penetration.

Regulatory challenges and compliance costs remain manageable.

Operational efficiencies lead to modest margin improvement.

The company's valuation reflects its steady growth profile, with moderate stock price appreciation in line with earnings growth.

A mild recession occurs that reduces revenues by 5% temporarily, but growth recovers quickly the following year.

The company trades at a fair valuation to its peers, with a modest increase in its PE ratio as growth resumes.

The company benefits from the eventual normalization of trade routes and reduction of geopolitical tensions.

This growth results in a 15% annual revenue growth rate over the next 5 years.

However, inflationary pressures and increased competition erodes the company's gross margins and operating expenses.

This results in an overall 10% increase in net income over the next 5 years.

Using the same approach as the bull case, the stock price would increase from $5.4 to $9.

With EPS of $0.34 today, EPS would reach $0.55 in 5 years assuming a 10% compounded rate of return on net income.

At a PE ratio of 16, the target price is $8.80, representing a 63% appreciation from the current price.

This is a conservative case that accounts for moderate growth and potential economic downturns.

Although this return is not as lucrative as the bull case, it still exceeds average market returns in the long run.

However, the return may not be worth the risks and capital if the bear case materializes. |

| Bear | Low | Payoneer faces significant headwinds, including increased competition from established players and new entrants, leading to market share erosion.

A severe global recession reduces cross-border payment volumes, impacting revenue growth.

Regulatory challenges and compliance costs escalate, squeezing margins.

Cybersecurity breaches or data privacy violations damage the company's reputation and lead to customer attrition.

The company fails to innovate and adapt to changing market dynamics, falling behind competitors.

A combination of these factors leads to declining revenue, reduced profitability, and a significant decline in the stock price.

Payoneer fails to navigate regulatory issues effectively and is banned from operating in key regions.

The global economy enters a deep and prolonged recession, significantly impacting cross-border trade and payment volumes.

A major security breach compromises customer data and erodes trust in the platform.

In this scenario, revenue declines by 5% annually for the next 5 years as customers flee to competing platforms.

Increased regulations and compliance costs lead to a significant erosion of gross margins and a substantial increase in operating expenses.

The net result is a negative earnings growth rate of 10% annually over the next 5 years.

This has a compounding effect on the stock price given the increased debt levels and reduced ability to compete and innovate.

With a negative EPS of $0.34 today, the EPS will reach $-0.55 in 5 years.

A PE ratio cannot be used to value a company with negative earnings.

A price to sales ratio is more appropriate here.

The current price to sales ratio is around 0.56.

Under the bear case, a reasonable price to sales ratio is 0.2.

At $977M in revenue today, revenues will erode to $763M in 5 years.

At a price to sales ratio of 0.2, the market cap will decrease to $153M.

With 360M shares outstanding, the share price could drop to $0.43.

This represents a -92% decrease from today's valuation of $5.4, or a 68% compounded loss per year.

Although the chances of this scenario materializing is low, the risks are clearly significant. |

7. Risks

Payoneer's growth is appealing, but the nature of its assets and liabilities, competitive landscape, and potential regulatory hurdles pose significant risks. While currently profitable and generating free cash flow, a deeper dive into balance sheet specifics and customer concentration is warranted. Further, while not currently over-leveraged, they do hold substantial deferred revenue.

Red Flags:

None identified.

8. Conclusion

Payoneer continues to grow its core business, driven by the expansion of the global e-commerce market.

While growth is steady, it is tempered by increasing competition and macroeconomic headwinds, including moderate inflation and slower economic growth.

The company maintains its market share but does not achieve significant breakthroughs in new product offerings or market penetration.

Regulatory challenges and compliance costs remain manageable.

Operational efficiencies lead to modest margin improvement.

The company's valuation reflects its steady growth profile, with moderate stock price appreciation in line with earnings growth.

A mild recession occurs that reduces revenues by 5% temporarily, but growth recovers quickly the following year.

The company trades at a fair valuation to its peers, with a modest increase in its PE ratio as growth resumes.

The company benefits from the eventual normalization of trade routes and reduction of geopolitical tensions.

This growth results in a 15% annual revenue growth rate over the next 5 years.

However, inflationary pressures and increased competition erodes the company's gross margins and operating expenses.

This results in an overall 10% increase in net income over the next 5 years.

Using the same approach as the bull case, the stock price would increase from $5.4 to $9.

With EPS of $0.34 today, EPS would reach $0.55 in 5 years assuming a 10% compounded rate of return on net income.

At a PE ratio of 16, the target price is $8.80, representing a 63% appreciation from the current price.

This is a conservative case that accounts for moderate growth and potential economic downturns.

Although this return is not as lucrative as the bull case, it still exceeds average market returns in the long run.

However, the return may not be worth the risks and capital if the bear case materializes.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) would provide insights into how effectively the company uses its capital and equity to generate profits. Given the net income of $121.16 million and total equity of $724.79 million in 2024, the ROE is approximately 16.7%. Similarly, ROIC would require an analysis of invested capital and its relationship to operating income after tax, offering further depth to capital efficiency assessment.

Calculating Return on Invested Capital (ROIC) and Return on Equity (ROE) would provide insights into how effectively the company uses its capital and equity to generate profits. Given the net income of $121.16 million and total equity of $724.79 million in 2024, the ROE is approximately 16.7%. Similarly, ROIC would require an analysis of invested capital and its relationship to operating income after tax, offering further depth to capital efficiency assessment. The company exhibits strong Free Cash Flow (FCF) generation, with $116.53 million in 2024, indicating its ability to generate cash after accounting for capital expenditures. However, capital expenditure has fluctuated, suggesting variable investment patterns in property, plant, and equipment. Monitoring the consistency of FCF and its relation to net income is vital for gauging the sustainability of the company's cash-generating capabilities.

The company exhibits strong Free Cash Flow (FCF) generation, with $116.53 million in 2024, indicating its ability to generate cash after accounting for capital expenditures. However, capital expenditure has fluctuated, suggesting variable investment patterns in property, plant, and equipment. Monitoring the consistency of FCF and its relation to net income is vital for gauging the sustainability of the company's cash-generating capabilities.