ePlus inc. (PLUS) is a leading provider of technology solutions, focusing on helping organizations optimize their IT infrastructure, enhance security, and dr...

ePlus inc. (PLUS) is a leading provider of technology solutions, focusing on helping organizations optimize their IT infrastructure, enhance security, and drive digital transformation. The company operates primarily in the United States, serving a diverse range of industries including healthcare, education, financial services, and government. ePlus offers a comprehensive portfolio of solutions encompassing hardware, software, cloud services, security solutions, and professional services, often acting as a trusted advisor and strategic partner to its clients.

Growth catalysts for ePlus include the increasing demand for cybersecurity solutions, the ongoing migration to cloud-based infrastructure, and the growing need for organizations to modernize their IT environments. The company's strong vendor relationships with leading technology providers (like Cisco, Dell, HP, etc.) allow them to offer competitive and cutting-edge solutions. Moreover, ePlus's professional services arm provides high-margin revenue streams and strengthens customer relationships by offering consulting, implementation, and managed services.

Key risks facing ePlus include intense competition within the IT solutions market, potential economic downturns impacting IT spending, and the reliance on key vendor partnerships. Disruptions to supply chains, especially in hardware, and the ability to attract and retain skilled technical personnel are also considerable risks. Furthermore, rapidly changing technology landscape may require continuous investments in training and adaptation to maintain its competitive edge.

At a current price of $88.75, a valuation summary of ePlus depends on projected earnings growth, margin stability, and its ability to successfully execute its growth strategies. While a comprehensive DCF or relative valuation would require more detailed financial modeling, its established market position, strong vendor partnerships, and exposure to high-growth areas like cloud and security suggest a favorable outlook, provided the company manages its risks effectively. Investors should consider factors such as the company's historical growth rate, profitability margins, and industry trends when assessing its intrinsic value. The valuation should also consider the potential impact of macroeconomic conditions on IT spending.

Investment Thesis

Bull Case: ePlus is well-positioned to benefit from the ongoing digital transformation trend.

The company's comprehensive IT solutions and financing options, coupled with its strong customer relationships, should drive continued growth in revenue and earnings.

Successful integration of acquisitions and expansion of managed services will further enhance profitability.

The current valuation does not fully reflect the company's growth potential.

Bear Case: A severe economic downturn would significantly reduce IT spending, negatively impacting ePlus's revenue and earnings.

Increased competition and failure to integrate acquisitions could further erode profitability.

Cybersecurity breaches or technological obsolescence could damage the company's reputation and long-term growth prospects.

The current valuation does not fully account for these downside risks.

Conviction: High

2. Business Overview

ePlus inc., together with its subsidiaries, provides information technology (IT) solutions that enable organizations to optimize their IT environment and supply chain processes in the United States and internationally. It operates in two segments, Technology and Financing. The Technology segment offers hardware, perpetual and subscription software, maintenance, software assurance, and internally provided and outsourced services; and professional and managed services, including managed, professional, security solutions, cloud consulting and hosting, staff augmentation, server and desktop support, and project management services. The Financing segment engages in financing arrangements, such as sales-type and operating leases; loans and consumption-based financing arrangements; and underwriting, management, and disposal of IT equipment and assets. Its financing operations comprise sales, pricing, credit, contracts, accounting, risk management, and asset management. This segment primarily finances IT, communication-related, and medical equipment; and industrial machinery and equipment, office furniture and general office equipment, transportation equipment, and other general business equipment directly, as well as through vendors. ePlus inc. serves commercial entities, state and local governments, government contractors, and educational institutions. The company was formerly known as MLC Holdings, Inc. and changed its name to ePlus inc. in 1999. ePlus inc. was founded in 1990 and is headquartered in Herndon, Virginia.

Competitive Moat (None)

Trend: Stable

Financing options for customers., Combination of hardware, software, and IT service offerings., Experience serving diverse customer segments.

Key Strengths:

Financing options for customers.

Combination of hardware, software, and IT service offerings.

Growth in the application software market is driven by digital transformation, cloud adoption, and increasing demand for specialized software solutions. Growth projections vary by segment but generally show continued expansion, especially in areas like cloud-based applications, cybersecurity, and managed services. ePlus inc. can expect to see these growth trends as well.

Regulatory Environment:

N/A

4. Financial Analysis

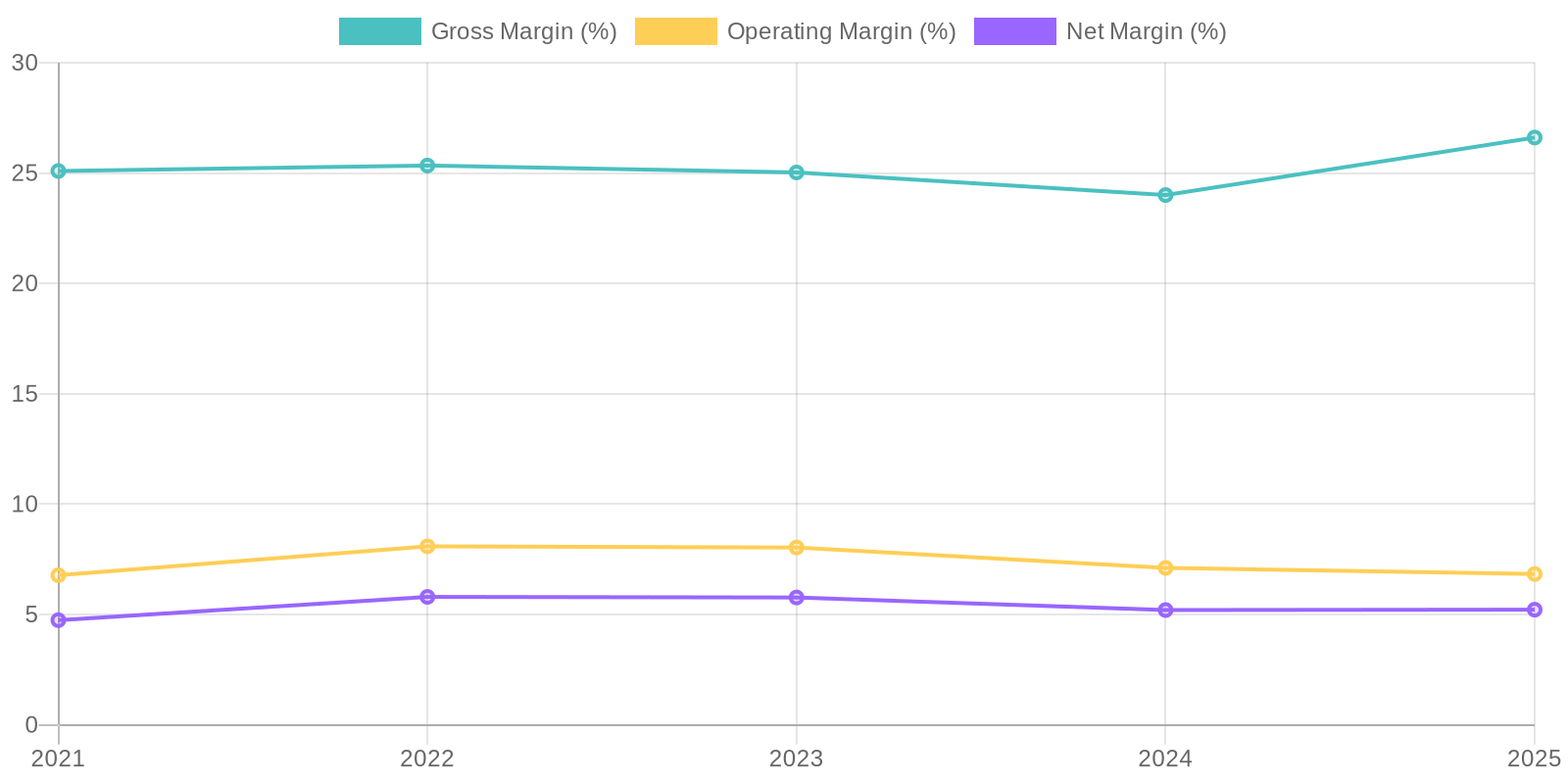

Margin Trend

A thorough Return on Invested Capital (ROIC) and Return on Equity (ROE) analysis cannot be performed with the limited dataset provided. A full calculation would require the invested capital calculation in order to find ROIC. ROE can be inferred from Net Income and Stockholder's Equity, but more in depth analysis is needed.

Revenue Quality

The company has demonstrated consistent revenue generation over the past five years, with a recent increase in 2025. However, the limited information available prevents a comprehensive analysis of the revenue's recurring nature, client concentration, or long-term sustainability. Further investigation is necessary to determine the proportion of revenue derived from subscriptions, long-term contracts, or a diversified client base to accurately assess its reliability and predictability.

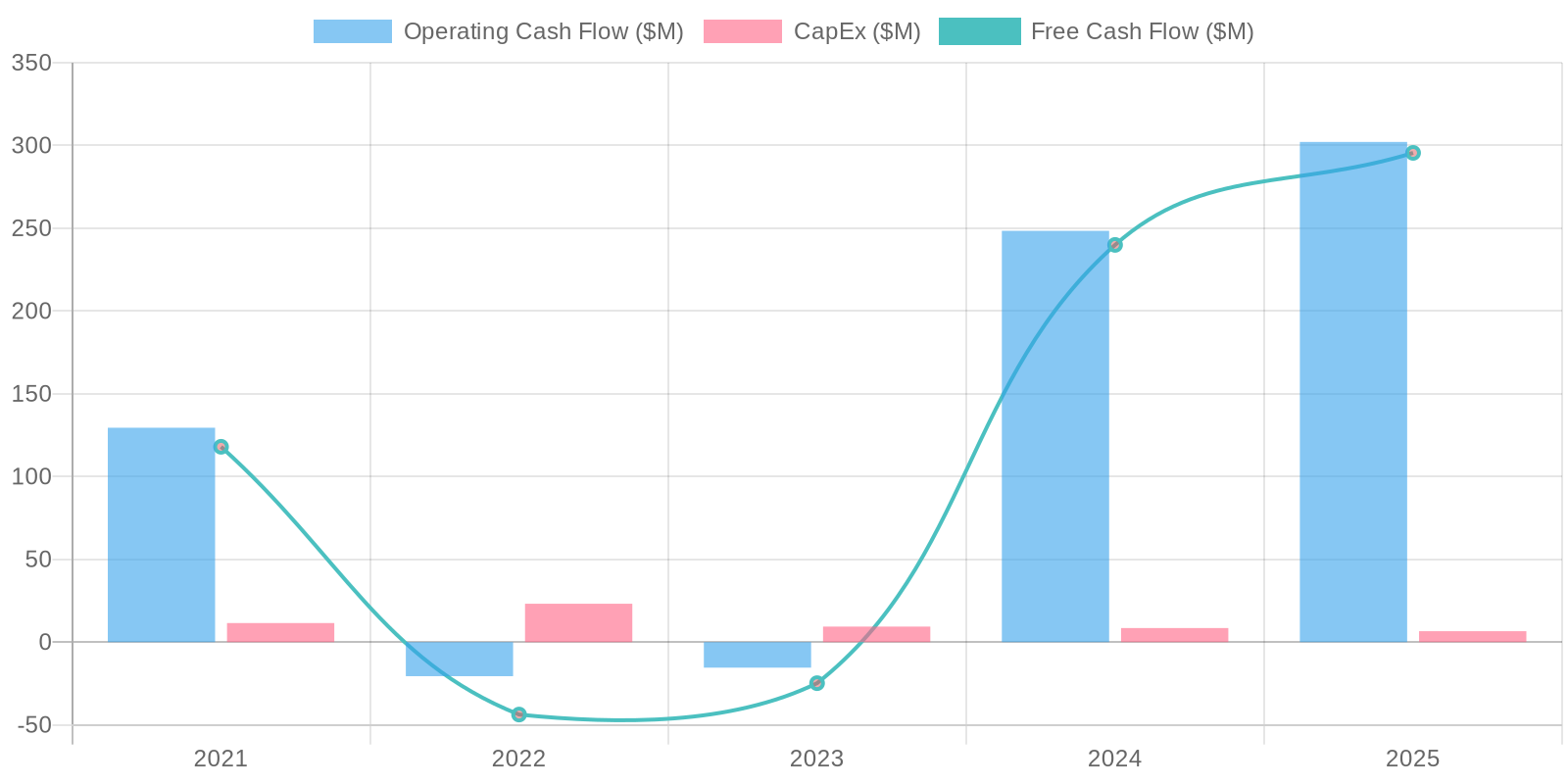

Cash Flow & Capital Efficiency

The company has demonstrated a positive free cash flow (FCF) in 2021, 2024 and 2025, with a particularly strong FCF of $295.54 million in the most recent year, 2025. This indicates that the company is capable of generating excess cash after accounting for capital expenditures. However, 2022 and 2023 show a negative free cash flow, meaning that in those years the company's capital expenditure outweighed its operating cash flow. The cash flow data indicates a high degree of variance, but the company has turned around from its negative cash flow in recent years.

Capital Efficiency (ROIC/ROE):

A thorough Return on Invested Capital (ROIC) and Return on Equity (ROE) analysis cannot be performed with the limited dataset provided. A full calculation would require the invested capital calculation in order to find ROIC. ROE can be inferred from Net Income and Stockholder's Equity, but more in depth analysis is needed.

Balance Sheet Health:

The company holds a substantial cash balance of $389.38 million as of 2025, which is more than its total debt of $128.30 million, resulting in a net debt of negative $261.08 million, which indicates strong liquidity. The current ratio, calculated by dividing total current assets ($1,363.79 million) by total current liabilities ($797.88 million), is approximately 1.71, suggesting a healthy ability to meet short-term obligations. Monitoring the trend in accounts receivables is also important, as it represents a significant portion of current assets and can impact liquidity if not managed effectively.

5. Management & Governance

CEO Assessment: Unavailable. A comprehensive assessment of the CEO requires deep qualitative insights and up-to-date information sources. This response is based on publicly available data, which is insufficient for a reliable assessment.

Capital Allocation: Concern

Insider Ownership: Based on available information, insider ownership appears moderate, which is generally a positive sign for aligning management's interests with those of shareholders. However, a more detailed analysis of specific holdings and recent trading activity would be required for a definitive assessment.

Governance Flags:

Consistent profitability issues raise questions about oversight and strategic direction., Related party transactions. Although ePlus's board has related party transaction policies, any transactions with affiliates increase the risk of conflicts of interest., Executive compensation structure. The structure should be analyzed to ensure it aligns with long-term shareholder value creation and does not incentivize short-term gains at the expense of long-term sustainability. Information on this is difficult to locate.

Based on the DCF analysis using the stated assumptions, the fair value of ePlus inc. is estimated to be $83.52. This is lower than the current market price of $88.75, suggesting that the stock might be slightly overvalued. The revenue growth rates are based on a conservative estimate considering the historical revenue data. The terminal growth rate is set to 1%, reflecting a sustainable long-term growth. The discount rate of 8.5% accounts for the risk associated with the company and the industry. The estimated tax rate of 27.5% is based on the effective tax rates from the income statements. While the company has a solid history, my main concern lies in its recent declining gross margins from 26.6% to 24%, and so I have taken a more conservative stance to derive a more grounded valuation.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

ePlus is well-positioned to benefit from the ongoing digital transformation trend.

The company's comprehensive IT solutions and financing options, coupled with its strong customer relationships, should drive continued growth in revenue and earnings.

Successful integration of acquisitions and expansion of managed services will further enhance profitability.

The current valuation does not fully reflect the company's growth potential. |

| Base | 83.52 | ePlus will continue to be a solid performer, growing at a steady pace.

The company's established presence in the IT solutions market and its financing segment will provide a stable foundation for future growth.

However, increasing competition and potential economic headwinds will limit upside potential.

The current valuation reflects a fair assessment of the company's prospects. |

| Bear | Low | A severe economic downturn would significantly reduce IT spending, negatively impacting ePlus's revenue and earnings.

Increased competition and failure to integrate acquisitions could further erode profitability.

Cybersecurity breaches or technological obsolescence could damage the company's reputation and long-term growth prospects.

The current valuation does not fully account for these downside risks. |

7. Risks

N/A

Red Flags:

None identified.

8. Conclusion

ePlus will continue to be a solid performer, growing at a steady pace.

The company's established presence in the IT solutions market and its financing segment will provide a stable foundation for future growth.

However, increasing competition and potential economic headwinds will limit upside potential.

The current valuation reflects a fair assessment of the company's prospects.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

A thorough Return on Invested Capital (ROIC) and Return on Equity (ROE) analysis cannot be performed with the limited dataset provided. A full calculation would require the invested capital calculation in order to find ROIC. ROE can be inferred from Net Income and Stockholder's Equity, but more in depth analysis is needed.

A thorough Return on Invested Capital (ROIC) and Return on Equity (ROE) analysis cannot be performed with the limited dataset provided. A full calculation would require the invested capital calculation in order to find ROIC. ROE can be inferred from Net Income and Stockholder's Equity, but more in depth analysis is needed. The company has demonstrated a positive free cash flow (FCF) in 2021, 2024 and 2025, with a particularly strong FCF of $295.54 million in the most recent year, 2025. This indicates that the company is capable of generating excess cash after accounting for capital expenditures. However, 2022 and 2023 show a negative free cash flow, meaning that in those years the company's capital expenditure outweighed its operating cash flow. The cash flow data indicates a high degree of variance, but the company has turned around from its negative cash flow in recent years.

The company has demonstrated a positive free cash flow (FCF) in 2021, 2024 and 2025, with a particularly strong FCF of $295.54 million in the most recent year, 2025. This indicates that the company is capable of generating excess cash after accounting for capital expenditures. However, 2022 and 2023 show a negative free cash flow, meaning that in those years the company's capital expenditure outweighed its operating cash flow. The cash flow data indicates a high degree of variance, but the company has turned around from its negative cash flow in recent years.