Deep Dive: Porch Group, Inc. (PRCH)

Recommendation: HOLD Price Target: 5.5 (-39.5 Upside) Risk Level: Medium

1. Executive Summary

Porch Group, Inc. (PRCH) operates a vertical software platform for the home services industry. It connects homeowners with home service professionals, offering tools and services to manage projects, generate leads, and streamline operations. Porch's current market position is characterized by its focus on both the professional and consumer sides of the home services marketplace, attempting to create a comprehensive ecosystem. The company has expanded through acquisitions to broaden its service offerings and geographic reach, now including insurance and other value-added services. At a price of $9.09, the market is likely factoring in considerable risk and uncertainty about Porch's path to profitability.

Growth catalysts for Porch include continued penetration of the home services market, expansion of its insurance offerings, and cross-selling opportunities within its existing customer base. The increasing demand for home improvement and maintenance services, driven by factors like aging housing stock and changing consumer preferences, provides a favorable backdrop. Furthermore, Porch's investments in technology and data analytics could enhance its ability to match homeowners with qualified professionals, improving the user experience and driving repeat business. Successful integration of acquired companies and realizing synergies from these acquisitions are also key to future growth.

Key risks facing Porch include intense competition in the home services and insurance industries, potential economic slowdowns impacting consumer spending on home improvement, and challenges in integrating acquired companies. The company's relatively short operating history as a public company and its history of net losses raise concerns about its financial sustainability. Maintaining a high level of customer satisfaction is crucial, as negative reviews can significantly impact its reputation and ability to attract new users. Execution risk related to its growth strategy and potential regulatory changes in the insurance sector are also significant concerns.

From a valuation perspective, Porch's current market capitalization reflects the market's skepticism about its ability to achieve profitability and sustained growth. A valuation summary should consider both revenue multiples and discounted cash flow analysis. While top-line growth may be attractive, the company's bottom-line performance needs substantial improvement to justify a higher valuation. The market's current price suggests investors are heavily discounting future prospects due to concerns about execution, profitability, and competitive pressures. Therefore, any investment decision should carefully weigh the potential for growth against the significant risks.

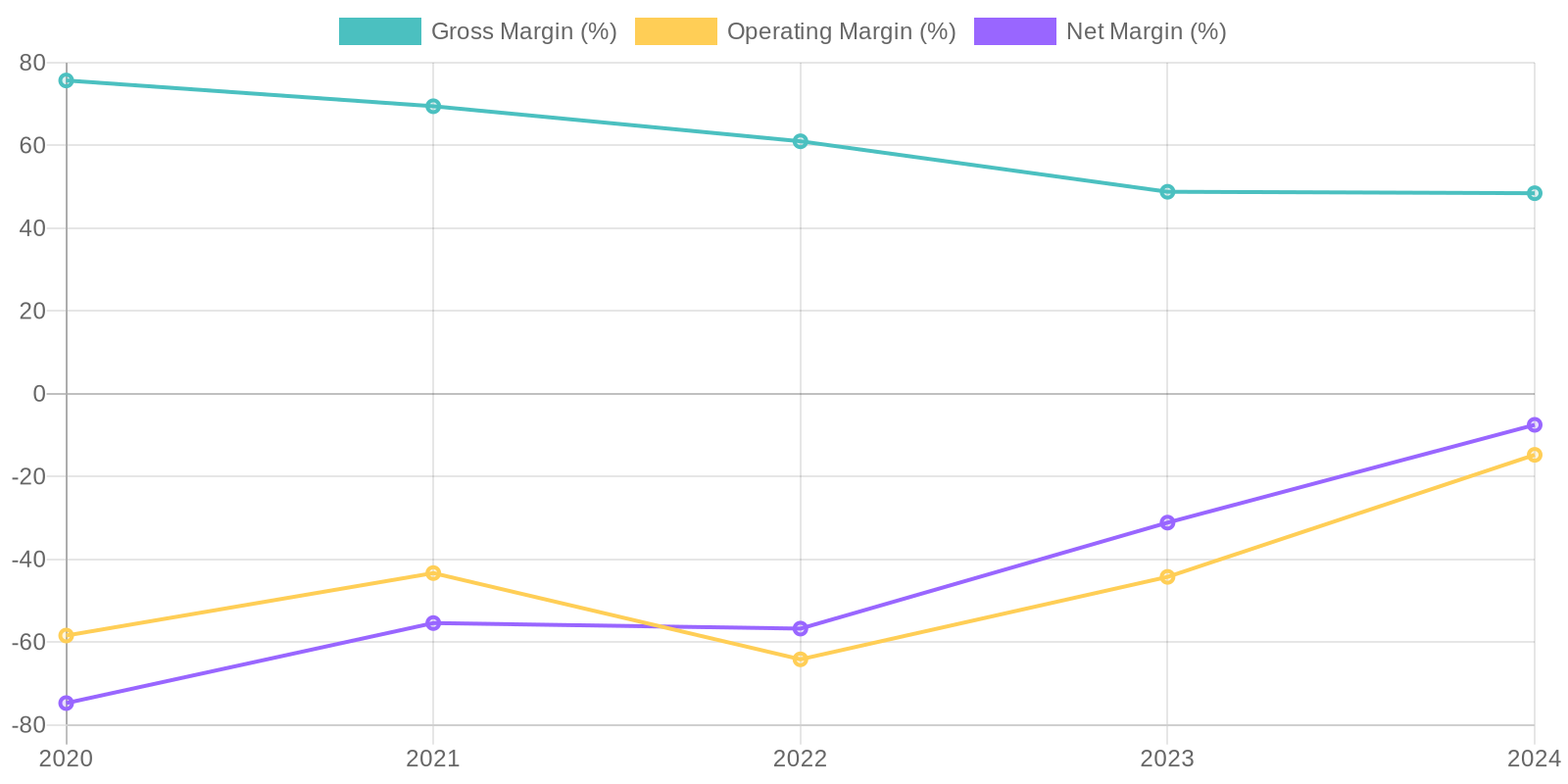

Given the company's negative net income for all reported periods, Return on Equity (ROE) is also negative, indicating inefficiency in generating profit from shareholder equity. Similarly, Return on Invested Capital (ROIC) would also be negative, reflecting the company's struggles in generating returns from its invested capital. The negative profitability makes it difficult to assess how efficiently the company is using its capital.

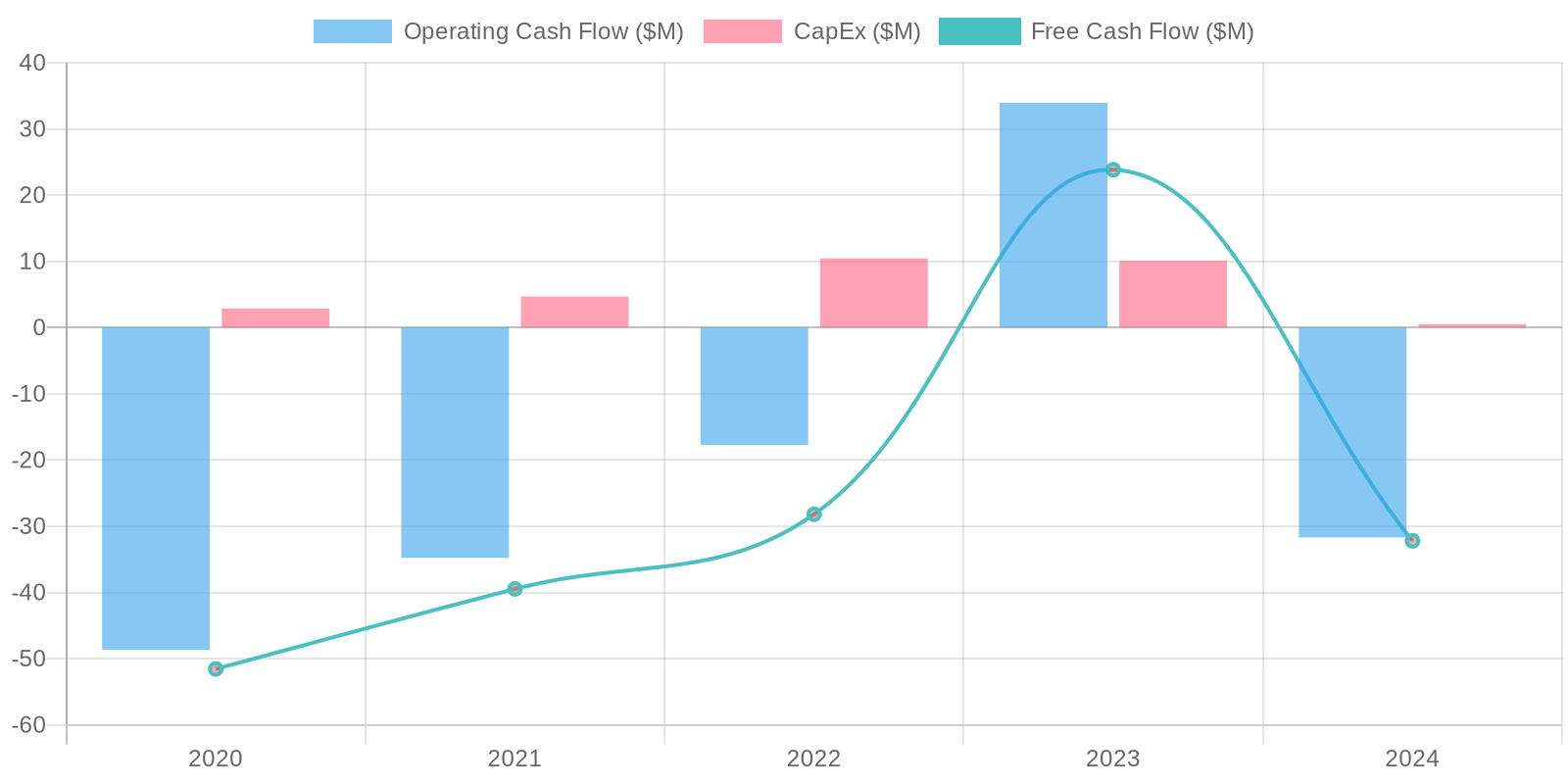

Given the company's negative net income for all reported periods, Return on Equity (ROE) is also negative, indicating inefficiency in generating profit from shareholder equity. Similarly, Return on Invested Capital (ROIC) would also be negative, reflecting the company's struggles in generating returns from its invested capital. The negative profitability makes it difficult to assess how efficiently the company is using its capital. The company's free cash flow (FCF) is negative in 2024, indicating that it is burning cash, not generating it, after accounting for capital expenditures. While FCF was positive in 2023, the overall trend reflects the need for external financing. The company's investments in property, plant, and equipment are relatively low, suggesting a limited capital expenditure strategy.

The company's free cash flow (FCF) is negative in 2024, indicating that it is burning cash, not generating it, after accounting for capital expenditures. While FCF was positive in 2023, the overall trend reflects the need for external financing. The company's investments in property, plant, and equipment are relatively low, suggesting a limited capital expenditure strategy.