PubMatic (PUBM) is a sell-side platform (SSP) in the digital advertising technology space, connecting online content publishers with advertisers. The company...

January 15, 2026

Vijar Kohli

Deep Dive: PubMatic, Inc. (PUBM)

Recommendation: BUY

Price Target: 10.35 (0.32 Upside)

Risk Level: Medium

1. Executive Summary

PubMatic (PUBM) is a sell-side platform (SSP) in the digital advertising technology space, connecting online content publishers with advertisers. The company's platform allows publishers to manage and monetize their ad inventory in real-time through programmatic advertising. While the stock currently trades at $7.84, reflecting a significant decline from its peak, PubMatic's market position is solid, being a recognized player in a growing sector. They hold relationships with many premium publishers and advertisers, and their focus on independent technology provides a competitive advantage against larger, integrated ad tech companies.

Growth catalysts for PubMatic include the continued expansion of programmatic advertising, particularly in connected TV (CTV) and online video. The increasing adoption of header bidding and the shift towards direct publisher-advertiser relationships also benefit PubMatic. Additionally, their focus on innovation and the development of new ad formats can fuel future growth. Global expansion, especially in emerging markets, represents another avenue for expansion.

Key risks facing PubMatic include intense competition from larger, well-capitalized companies like Google and Magnite. Changes in privacy regulations, such as increased restrictions on data collection, could negatively impact the effectiveness of programmatic advertising. Economic downturns can lead to reduced advertising budgets, impacting PubMatic's revenue. Dependence on key customers and the potential for those customers to move to alternative platforms also poses a risk.

Valuation summary: Given the current price, PUBM's valuation appears potentially undemanding relative to its growth prospects, particularly if the company can successfully capitalize on the CTV opportunity and manage the risks outlined above. However, the uncertainty surrounding the macroeconomic environment and evolving privacy landscape warrants caution. A deeper analysis of the company's financials, competitive positioning, and growth strategy is crucial to determine its intrinsic value and potential for future appreciation. Investors should carefully weigh the potential rewards against the significant risks involved.

Investment Thesis

Bull Case: PubMatic is a leading provider of cloud infrastructure for programmatic advertising, poised to capitalize on the continued shift towards digital and connected TV (CTV) advertising.

Their strong technology platform, growing market share, and healthy financial metrics suggest significant upside potential.

The market is underestimating PubMatic's ability to sustain growth and expand its margins.

Bear Case: PubMatic faces significant risks from a potential slowdown in digital advertising, increasing competition, and technological obsolescence.

If the company fails to adapt to changing market conditions, it could experience a significant decline in revenue and profitability, leading to a substantial loss for investors.

The high reliance on digital advertising makes it vulnerable to economic cycles.

Conviction: High

2. Business Overview

PubMatic, Inc. provides a cloud infrastructure platform that enables real-time programmatic advertising transactions for Internet content creators and advertisers worldwide. The company's solutions include Openwrap, a header bidding solution that provides enterprise-grade management and analytics tools; Openwrap OTT, a header bidding management solution for OTT; Openwrap SDK, a header bidding solution for in-app developers; private marketplace solutions; and media buyer consoles. In addition, it offers Real-Time Bidding (RTB) programmatic technologies, which provides various selling options across screens and ad formats; digital advertising inventory quality solutions to detect and filter out invalid traffic and other nefarious activity; Ad quality solutions targeting the reduction of security issues, quality issues, and performance issues; Identity Hub, an identity solution that allows for the use of any advertiser preferred user identifier in a scaled and privacy-compliant fashion; Audience Encore, an audience data platform; and cross-platform video, a sell side platform, which connects trusted video buyers to premium publishers. The company's platform supports an array of ad formats and digital device types, including mobile app, mobile web, desktop, display, video, over-the-top (OTT), connected television, and media. PubMatic, Inc. was incorporated in 2006 and is based in Redwood City, California.

Competitive Moat (Narrow)

Trend: Stable

Independent SSP focusing exclusively on the sell side, potentially leading to stronger publisher relationships, Technology-driven approach with OpenWrap and other platform solutions

Key Strengths:

Independent SSP focusing exclusively on the sell side, potentially leading to stronger publisher relationships

Technology-driven approach with OpenWrap and other platform solutions

The application software market is expected to continue growing at a healthy rate in the coming years, driven by factors such as increasing digitalization, cloud adoption, the proliferation of mobile devices, and the growing importance of data analytics. Specific growth rates depend on the segment (e.g., SaaS vs. on-premise) and geography, but generally, a CAGR of 5-10% is anticipated over the next 5-7 years.

Regulatory Environment:

N/A

4. Financial Analysis

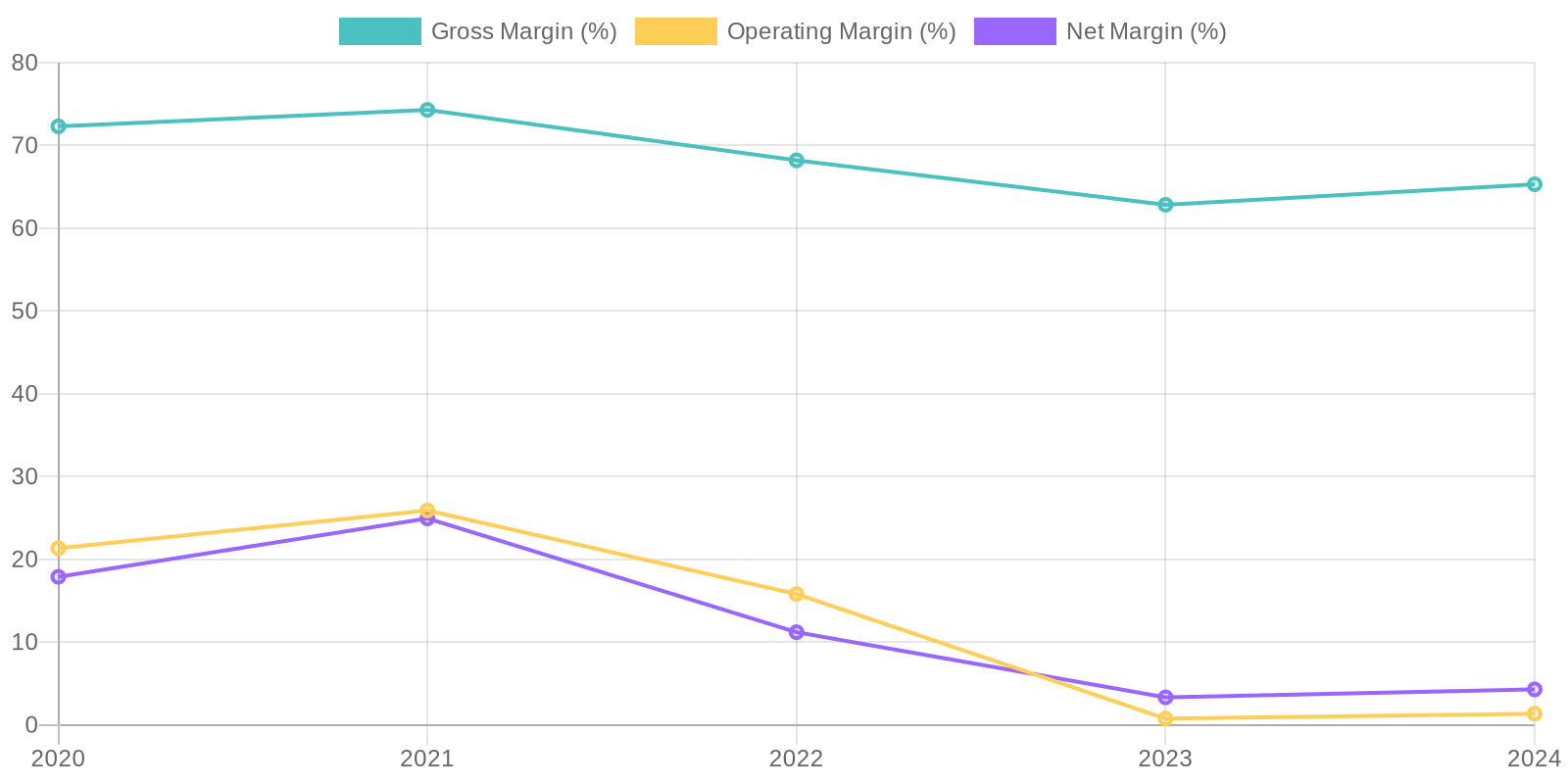

Margin Trend

The company's Return on Invested Capital (ROIC) and Return on Equity (ROE) can be inferred from the provided data. Given the net income and balance sheet figures, ROE has varied significantly over the past five years, directly correlating to net income fluctuations. To calculate ROIC, one would need to determine the invested capital, but generally, the trends in profitability highlight the efficiency with which the company utilizes its capital to generate returns and increase shareholder value.

Revenue Quality

The company's revenue has demonstrated a positive trend over the past five years, increasing from $148.75 million in 2020 to $291.26 million in 2024. This growth suggests a degree of sustainability, but further investigation into client concentration is needed to ensure long-term stability. Analyzing the contract terms and renewal rates with major clients will provide a clearer picture of the recurring nature of their revenue streams and inform on overall revenue dependability.

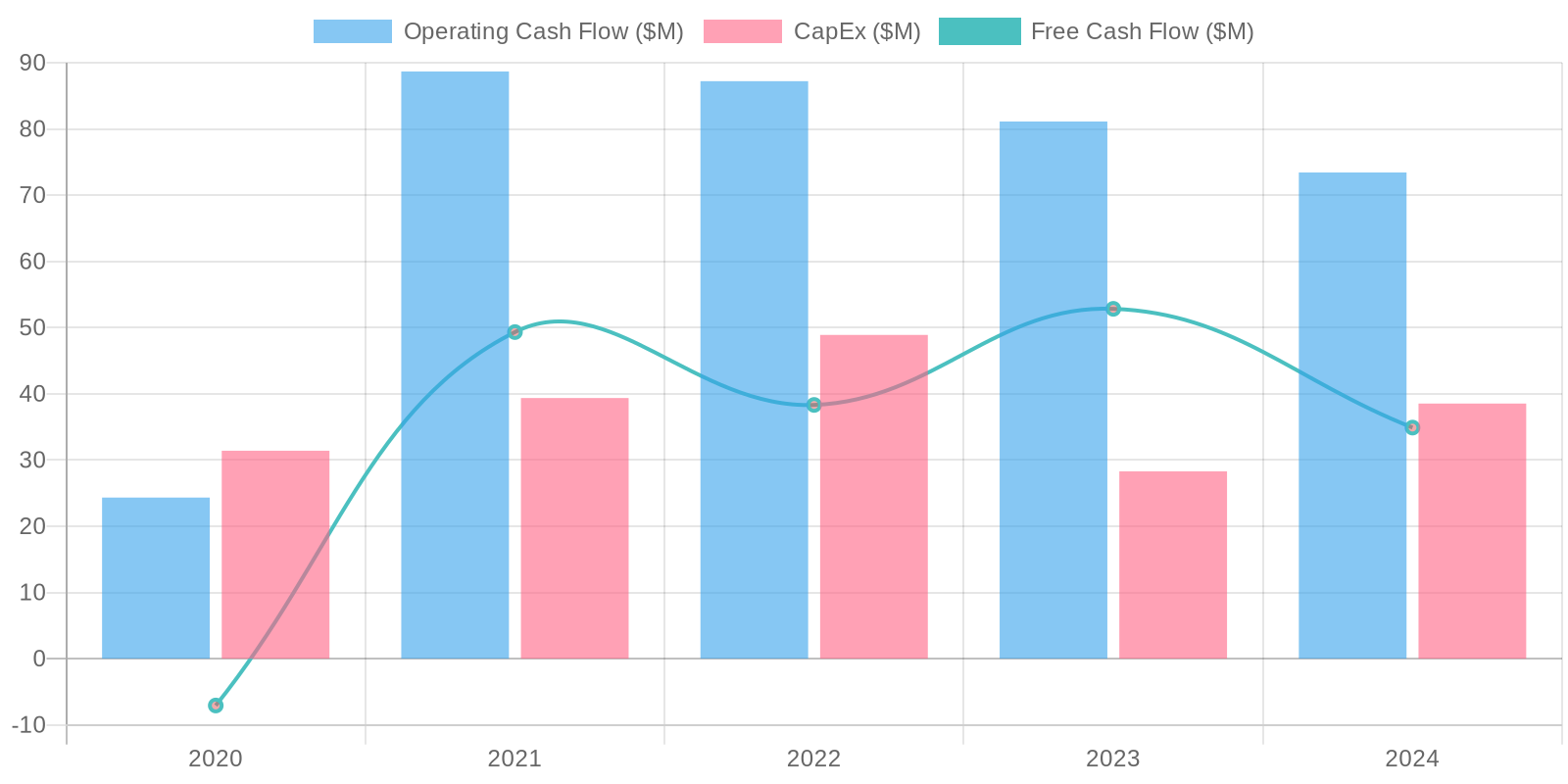

Cash Flow & Capital Efficiency

The company has generally exhibited positive Free Cash Flow (FCF) over the past few years, with a notable exception in 2020. FCF generation is crucial for the company's financial flexibility, supporting investments and debt management. While operating cash flow remains positive, it's important to understand the drivers behind changes in working capital and how they impact the overall cash position and future projects.

Capital Efficiency (ROIC/ROE):

The company's Return on Invested Capital (ROIC) and Return on Equity (ROE) can be inferred from the provided data. Given the net income and balance sheet figures, ROE has varied significantly over the past five years, directly correlating to net income fluctuations. To calculate ROIC, one would need to determine the invested capital, but generally, the trends in profitability highlight the efficiency with which the company utilizes its capital to generate returns and increase shareholder value.

Balance Sheet Health:

The company maintains a relatively strong balance sheet, characterized by substantial cash reserves and moderate debt levels. The current ratio, calculated from current assets and current liabilities, has been above 1 for the reported years, indicating sufficient liquidity to meet short-term obligations. While the company holds debt, the net debt position is negative due to the large cash balance, implying a healthy solvency profile and the capacity to manage liabilities effectively, though the significant increase in accounts payable during the latest year should be investigated.

5. Management & Governance

CEO Assessment: Assessing the CEO's performance requires a deep dive into PubMatic's strategic decisions, execution against stated goals, and overall impact on shareholder value. Recent performance metrics, innovation pipeline management, and communication strategies would be key factors in this assessment. Without specific data points, a comprehensive evaluation is challenging. I need more information.

Capital Allocation: Good

Insider Ownership: Insider ownership data is crucial for evaluating alignment between management and shareholders. A significant level of insider ownership often indicates that management's interests are aligned with creating long-term shareholder value. Publicly available data on insider ownership percentages should be analyzed to determine the level of alignment.

Governance Flags:

Potential conflicts of interest should be monitored, particularly regarding related-party transactions., Board composition and independence should be assessed to ensure effective oversight of management., Executive compensation structure should be aligned with long-term shareholder value creation.

The DCF model suggests a fair value of $10.35 per share. This is based on a conservative estimate of revenue growth, a reasonable FCF margin, and a WACC derived from industry averages and the company's capital structure. The revenue growth is decelerating, consistent with the company size and industry trends. The relative valuation using P/S ratios of peers yields a similar result, confirming the DCF valuation's reasonableness. The upside is significant but within a plausible range for a growing software company. The downside reflects the sensitivity of the valuation to the growth rate and discount rate assumptions.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

PubMatic is a leading provider of cloud infrastructure for programmatic advertising, poised to capitalize on the continued shift towards digital and connected TV (CTV) advertising.

Their strong technology platform, growing market share, and healthy financial metrics suggest significant upside potential.

The market is underestimating PubMatic's ability to sustain growth and expand its margins. |

| Base | 10.35 | PubMatic is a solid company with a sustainable business model in the programmatic advertising space.

While growth may be slower than in the past, the company should continue to generate profits and cash flow.

At the current valuation, the stock offers a reasonable return with moderate risk. |

| Bear | Low | PubMatic faces significant risks from a potential slowdown in digital advertising, increasing competition, and technological obsolescence.

If the company fails to adapt to changing market conditions, it could experience a significant decline in revenue and profitability, leading to a substantial loss for investors.

The high reliance on digital advertising makes it vulnerable to economic cycles. |

7. Risks

PubMatic faces risks related to competition, technological change, and reliance on relationships with publishers and advertisers. Slowing revenue growth and volatility in net income also present concerns. The company's high accounts receivable balance could indicate potential issues with revenue recognition and collections.

Red Flags:

The significant increase in accounts payable in the most recent year (2024) warrants further investigation.

Fluctuations in operating and net income margins may indicate instability or aggressive accounting practices.

8. Conclusion

PubMatic is a solid company with a sustainable business model in the programmatic advertising space.

While growth may be slower than in the past, the company should continue to generate profits and cash flow.

At the current valuation, the stock offers a reasonable return with moderate risk.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

The company's Return on Invested Capital (ROIC) and Return on Equity (ROE) can be inferred from the provided data. Given the net income and balance sheet figures, ROE has varied significantly over the past five years, directly correlating to net income fluctuations. To calculate ROIC, one would need to determine the invested capital, but generally, the trends in profitability highlight the efficiency with which the company utilizes its capital to generate returns and increase shareholder value.

The company's Return on Invested Capital (ROIC) and Return on Equity (ROE) can be inferred from the provided data. Given the net income and balance sheet figures, ROE has varied significantly over the past five years, directly correlating to net income fluctuations. To calculate ROIC, one would need to determine the invested capital, but generally, the trends in profitability highlight the efficiency with which the company utilizes its capital to generate returns and increase shareholder value. The company has generally exhibited positive Free Cash Flow (FCF) over the past few years, with a notable exception in 2020. FCF generation is crucial for the company's financial flexibility, supporting investments and debt management. While operating cash flow remains positive, it's important to understand the drivers behind changes in working capital and how they impact the overall cash position and future projects.

The company has generally exhibited positive Free Cash Flow (FCF) over the past few years, with a notable exception in 2020. FCF generation is crucial for the company's financial flexibility, supporting investments and debt management. While operating cash flow remains positive, it's important to understand the drivers behind changes in working capital and how they impact the overall cash position and future projects.