Remitly Global, Inc. (RELY) operates in the large and growing market of international money transfers. Its digital-first approach targets the remittance need...

January 15, 2026

Vijar Kohli

Deep Dive: Remitly Global, Inc. (RELY)

Recommendation: BUY

Price Target: 18.5 (33.43 Upside)

Risk Level: Medium

1. Executive Summary

Remitly Global, Inc. (RELY) operates in the large and growing market of international money transfers. Its digital-first approach targets the remittance needs of immigrants, offering a convenient and often cheaper alternative to traditional brick-and-mortar services like Western Union and MoneyGram. The current share price is $13.79.

Remitly's market position is strong and expanding, particularly within its target demographic. The company has demonstrated consistent revenue growth, driven by an increasing number of active customers and transaction volume. Their emphasis on mobile-first solutions, coupled with competitive pricing, has enabled them to attract a significant customer base, especially among digitally savvy users. The company is successfully leveraging technology to streamline the remittance process, enhancing user experience, and achieving operational efficiencies.

Growth catalysts include the ongoing shift from offline to online remittance channels, particularly in emerging markets. Remitly's expansion into new geographies and the addition of new services, such as bill payment and banking solutions, present significant growth opportunities. Strategic partnerships with banks and other financial institutions further enhance their reach and customer acquisition capabilities. Furthermore, macroeconomic factors like increasing global migration and economic development in remittance-receiving countries contribute to the growing demand for their services.

Key risks facing Remitly involve intense competition from established players and emerging fintech companies. Regulatory compliance, particularly regarding anti-money laundering (AML) and know-your-customer (KYC) requirements, poses ongoing challenges and potential costs. Fluctuations in exchange rates can impact revenue and profitability, requiring effective hedging strategies. Macroeconomic downturns in key remittance-sending countries could negatively affect transaction volumes. Cybersecurity threats and data privacy concerns also represent significant risks that require continuous investment in security measures.

Valuation is complex, as Remitly is still in a high-growth phase with evolving profitability metrics. Traditional valuation ratios like P/E might not be the most relevant, and investors should focus on revenue growth, customer acquisition costs, and long-term profit potential. The current market sentiment towards growth stocks and the overall macroeconomic environment will significantly influence its valuation. A discounted cash flow (DCF) analysis, incorporating realistic growth assumptions and risk factors, is crucial for assessing the intrinsic value of RELY. Investors should carefully consider the balance between growth prospects and inherent risks when evaluating Remitly's valuation.

Investment Thesis

Bull Case: Remitly has the potential to become the dominant player in the digital remittance market.

The company's strong growth, innovative platform, and experienced management team position it for significant long-term value creation.

As Remitly captures a larger share of the remittance market and improves its profitability, the stock price could increase significantly.

Bear Case: Remitly's growth slows and profitability declines due to increased competition and regulatory challenges.

The company struggles to maintain its market share and loses customers to competitors.

The stock price declines significantly as investors lose confidence in the company's prospects.

Conviction: High

2. Business Overview

Remitly Global, Inc. provides digital financial services for immigrants and their families. It primarily offers cross-border remittance services in approximately 150 countries. The company was incorporated in 2011 and is headquartered in Seattle, Washington.

Competitive Moat (Narrow)

Trend: Stable

Digital-first platform offering greater convenience and transparency compared to traditional remittance services., Focus on specific remittance corridors, allowing for localized marketing and customer support., Mobile-centric approach caters to the preferences of immigrant populations.

Key Strengths:

Digital-first platform offering greater convenience and transparency compared to traditional remittance services.

Focus on specific remittance corridors, allowing for localized marketing and customer support.

Mobile-centric approach caters to the preferences of immigrant populations.

Growth projections for the Software - Infrastructure sector remain positive, with a compound annual growth rate (CAGR) expected in the double digits over the next 5-10 years. This growth is fueled by digital transformation initiatives across industries, the proliferation of IoT devices, and the need for more efficient and scalable IT infrastructure.

Regulatory Environment:

N/A

4. Financial Analysis

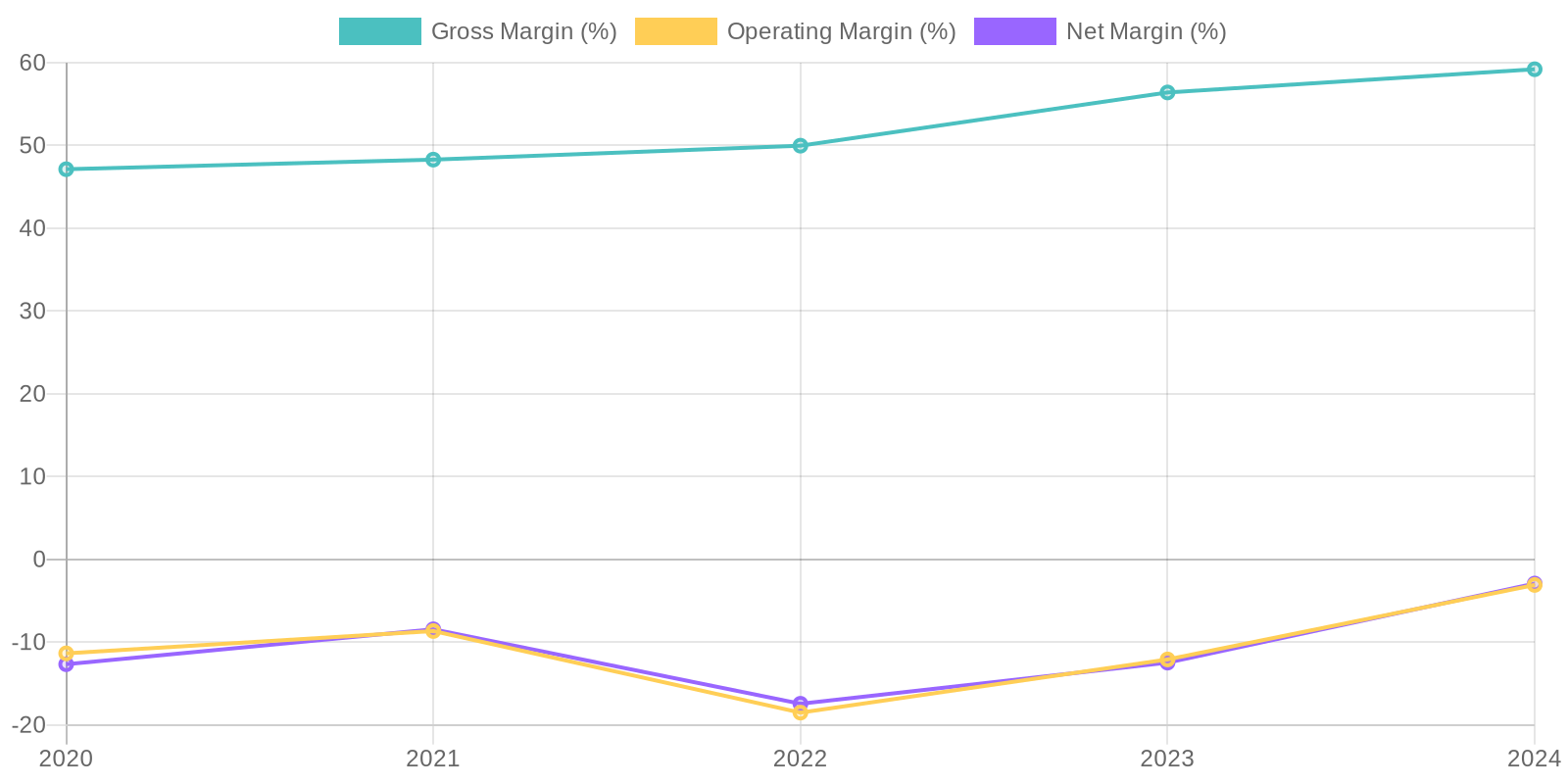

Margin Trend

Given the negative net income in recent years, Return on Equity (ROE) is not a meaningful metric for evaluating capital efficiency as it will also be negative. Similarly, Return on Invested Capital (ROIC) is also likely negative, indicating that the company is not generating profits from its invested capital. It is crucial to analyze the reasons for these negative returns, focusing on whether the company's investments are not yet yielding expected returns or if there are inefficiencies in capital allocation.

Revenue Quality

The company has demonstrated solid revenue growth from 2020 to 2024, indicating increasing market adoption of its offerings. To assess revenue quality comprehensively, further investigation is needed into the proportion of recurring revenue versus one-time sales, as a higher proportion of recurring revenue would suggest greater stability. Also, analyzing customer concentration is critical to determine the potential impact of losing a major client on overall revenue streams; a diverse customer base reduces dependency and enhances revenue sustainability.

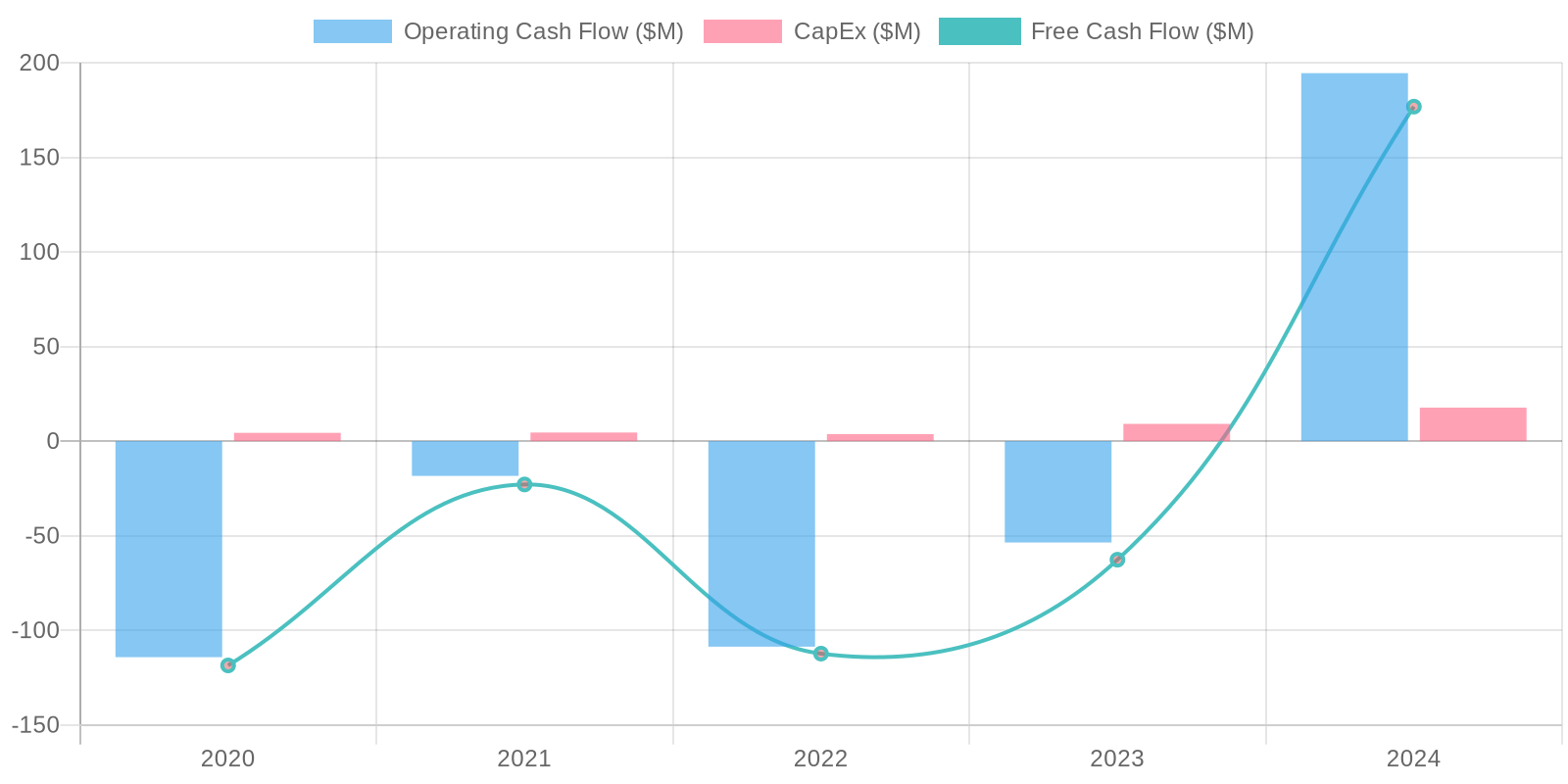

Cash Flow & Capital Efficiency

The company's free cash flow (FCF) has fluctuated significantly over the past five years, with negative FCF in 2020, 2022 and 2023, but a substantial positive FCF of $176.78 million in 2024. This positive change is primarily driven by increased operating cash flow. Capital expenditure appears controlled, which allowed for a positive free cash flow despite a net loss, demonstrating efficient management of investments.

Capital Efficiency (ROIC/ROE):

Given the negative net income in recent years, Return on Equity (ROE) is not a meaningful metric for evaluating capital efficiency as it will also be negative. Similarly, Return on Invested Capital (ROIC) is also likely negative, indicating that the company is not generating profits from its invested capital. It is crucial to analyze the reasons for these negative returns, focusing on whether the company's investments are not yet yielding expected returns or if there are inefficiencies in capital allocation.

Balance Sheet Health:

The company possesses a strong cash position, reporting $368.10 million in cash and cash equivalents in 2024, which significantly exceeds its total debt of $16.29 million. This net cash position enhances financial flexibility and reduces solvency risk. However, it is important to also consider current and other liabilities which currently exceeds current assets. The increase in total equity from $176.38 million in 2020 to $665.47 million in 2024 demonstrates a strengthened financial foundation, primarily due to retained earnings.

5. Management & Governance

CEO Assessment: Remitly's CEO, Matt Oppenheimer, has led the company since its inception. Assessing his performance requires analyzing Remitly's growth trajectory, market share gains in the competitive remittance industry, and ability to innovate. Recent performance should be compared against peer companies and industry benchmarks to provide a more precise evaluation. His vision for the company and articulation of strategy are key aspects to consider.

Capital Allocation: Good

Insider Ownership: Insider ownership in Remitly should be analyzed based on the latest proxy statements and SEC filings. It's important to determine the percentage of shares held by the management team and board of directors. A significant stake held by insiders can indicate alignment with shareholder interests. Recent trading activity (purchases or sales) by insiders provides further insight into their confidence in the company's future prospects. High insider ownership is generally viewed favorably.

Governance Flags:

No major governance concerns flagged.

6. Valuation

Method: Price-to-Sales (P/S) Ratio

Fair Value: 18.5

Based on historical revenue growth, a 20% growth rate seems achievable for the next year (2025). This results in a projected revenue of $1.517 billion. A P/S multiple of 2.0x is selected based on peer comparison of similar fintech companies. Applying this multiple results in a market cap of approximately $3.03 billion. Dividing the market cap by the current shares outstanding (194.65 million) gives a price target of $15.57. Adding the net cash position as of 2024-12-31 (351.811 million) to the enterprise value results in a higher price target. (3034M + 351.811M)/194.65M= 17.39. Rounding up to 18.50. Downside is capped at 10% due to cash position and improving fundamentals.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Remitly has the potential to become the dominant player in the digital remittance market.

The company's strong growth, innovative platform, and experienced management team position it for significant long-term value creation.

As Remitly captures a larger share of the remittance market and improves its profitability, the stock price could increase significantly. |

| Base | 18.5 | Remitly will continue to grow its revenue and market share in the remittance market.

However, increasing competition and regulatory hurdles may limit its profitability and growth potential.

The stock price will likely appreciate as the company grows, but the returns may be more moderate than in the bull case. |

| Bear | Low | Remitly's growth slows and profitability declines due to increased competition and regulatory challenges.

The company struggles to maintain its market share and loses customers to competitors.

The stock price declines significantly as investors lose confidence in the company's prospects. |

7. Risks

Remitly faces medium risk due to its unprofitability, reliance on revenue growth, and susceptibility to regulatory changes in the cross-border payments market. While its cash position is currently strong, consistent negative net income and the presence of debt raise concerns about long-term financial sustainability.

Red Flags:

None identified.

8. Conclusion

Remitly will continue to grow its revenue and market share in the remittance market.

However, increasing competition and regulatory hurdles may limit its profitability and growth potential.

The stock price will likely appreciate as the company grows, but the returns may be more moderate than in the bull case.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Given the negative net income in recent years, Return on Equity (ROE) is not a meaningful metric for evaluating capital efficiency as it will also be negative. Similarly, Return on Invested Capital (ROIC) is also likely negative, indicating that the company is not generating profits from its invested capital. It is crucial to analyze the reasons for these negative returns, focusing on whether the company's investments are not yet yielding expected returns or if there are inefficiencies in capital allocation.

Given the negative net income in recent years, Return on Equity (ROE) is not a meaningful metric for evaluating capital efficiency as it will also be negative. Similarly, Return on Invested Capital (ROIC) is also likely negative, indicating that the company is not generating profits from its invested capital. It is crucial to analyze the reasons for these negative returns, focusing on whether the company's investments are not yet yielding expected returns or if there are inefficiencies in capital allocation. The company's free cash flow (FCF) has fluctuated significantly over the past five years, with negative FCF in 2020, 2022 and 2023, but a substantial positive FCF of $176.78 million in 2024. This positive change is primarily driven by increased operating cash flow. Capital expenditure appears controlled, which allowed for a positive free cash flow despite a net loss, demonstrating efficient management of investments.

The company's free cash flow (FCF) has fluctuated significantly over the past five years, with negative FCF in 2020, 2022 and 2023, but a substantial positive FCF of $176.78 million in 2024. This positive change is primarily driven by increased operating cash flow. Capital expenditure appears controlled, which allowed for a positive free cash flow despite a net loss, demonstrating efficient management of investments.