Repay Holdings Corporation (RPAY), currently trading at $3.6, operates as a vertically integrated payment solutions provider. The company focuses on niche ma...

January 15, 2026

Vijar Kohli

Deep Dive: Repay Holdings Corporation (RPAY)

Recommendation: BUY

Price Target: 4.12 (0.14 Upside)

Risk Level: Medium

1. Executive Summary

Repay Holdings Corporation (RPAY), currently trading at $3.6, operates as a vertically integrated payment solutions provider. The company focuses on niche markets like accounts payable, consumer finance, healthcare, and automotive, offering a suite of services including payment processing, virtual cards, and integrated payment technology. Repay distinguishes itself through its specialized focus, integration capabilities, and commitment to customer service within these targeted verticals. While the company has faced headwinds, its focus on growing within less cyclical industries provides a somewhat more durable base compared to firms with a broader customer base.

Key growth catalysts for Repay include continued penetration within its existing verticals, expansion into new adjacent markets, strategic acquisitions, and leveraging its integrated payment platform to drive increased transaction volume. The shift towards electronic payments, particularly within the verticals Repay serves, provides a long-term tailwind. Successfully integrating acquired companies and realizing synergies are crucial for maintaining growth momentum. Furthermore, the continued development and deployment of new payment solutions tailored to specific industry needs will be vital for attracting and retaining customers.

Several risks need to be considered. First, competition within the payment processing industry is intense, with established players and emerging fintech companies vying for market share. The economic sensitivity of some of Repay's verticals, such as consumer finance, could impact transaction volume during economic downturns. Integration risks associated with acquisitions pose a challenge, and failure to successfully integrate acquired businesses could negatively impact financial performance. Furthermore, data security breaches and compliance issues related to payment processing could lead to reputational damage and financial losses. Changes in regulations impacting payment processing could also affect Repay's business model.

At the current share price of $3.6, Repay's valuation appears potentially discounted relative to its historical multiples and growth prospects, though any investment decision depends on a deeper analysis of its financial health, recent performance, and future outlook. Investors should consider the company's profitability, cash flow generation, and balance sheet strength. A discounted cash flow analysis, relative valuation metrics (such as price-to-earnings, price-to-sales, and EV/EBITDA), and peer group comparisons are essential for determining a fair value. The depressed share price likely reflects some investor concern about recent results and broader market sentiment, potentially offering an opportunity for value investors if the company can execute its growth strategy successfully and address its key risks. It should be noted that valuation metrics need to be considered in light of the overall economic climate and outlook for payment processors.

Investment Thesis

Bull Case: In the bull case, RPAY capitalizes on the shift towards electronic payments within its industry-specific markets.

Strategic acquisitions are successfully integrated, and new revenue streams are developed.

Strong top-line growth combined with margin expansion results in significant earnings growth and debt reduction.

The market recognizes RPAY's leadership position, resulting in valuation multiple expansion.

Bear Case: In the bear case, RPAY struggles to maintain its growth momentum due to intensifying competition and unfavorable economic conditions.

Integration challenges from acquisitions lead to cost overruns and revenue loss.

A high debt burden restricts the company's financial flexibility and hinders its ability to invest in growth initiatives.

Market loses confidence in RPAY's ability to execute, leading to valuation multiple contraction.

Conviction: High

2. Business Overview

Repay Holdings Corporation provides integrated payment processing solutions to industry-oriented markets. The company's payment processing solutions enable consumers and businesses to make payments using electronic payment methods. It also offers a range of solutions relating to electronic payment methods, including credit and debit processing, virtual credit card processing, automated clearing house (ACH) processing, enhanced ACH processing, and instant funding that are processed through its proprietary payment channels, such as Web-based, mobile application, text-to-pay, interactive voice response, and point of sale. In addition, the company provides payment processing solutions to customers primarily operating in the personal loans, automotive loans, receivables management, and business-to-business verticals. It sells its products through direct sales representatives and software integration partners. The company was founded in 2006 and is headquartered in Atlanta, Georgia.

Competitive Moat (Narrow)

Trend: Stable

Specialized solutions for specific verticals, Integrated platform across multiple payment channels

Key Strengths:

Specialized solutions for specific verticals

Integrated platform across multiple payment channels

Growth projections are positive, driven by cloud adoption, digital transformation initiatives, and the increasing complexity of IT environments. Expect continued expansion in areas like cloud-native technologies, cybersecurity, and automation.

Regulatory Environment:

N/A

4. Financial Analysis

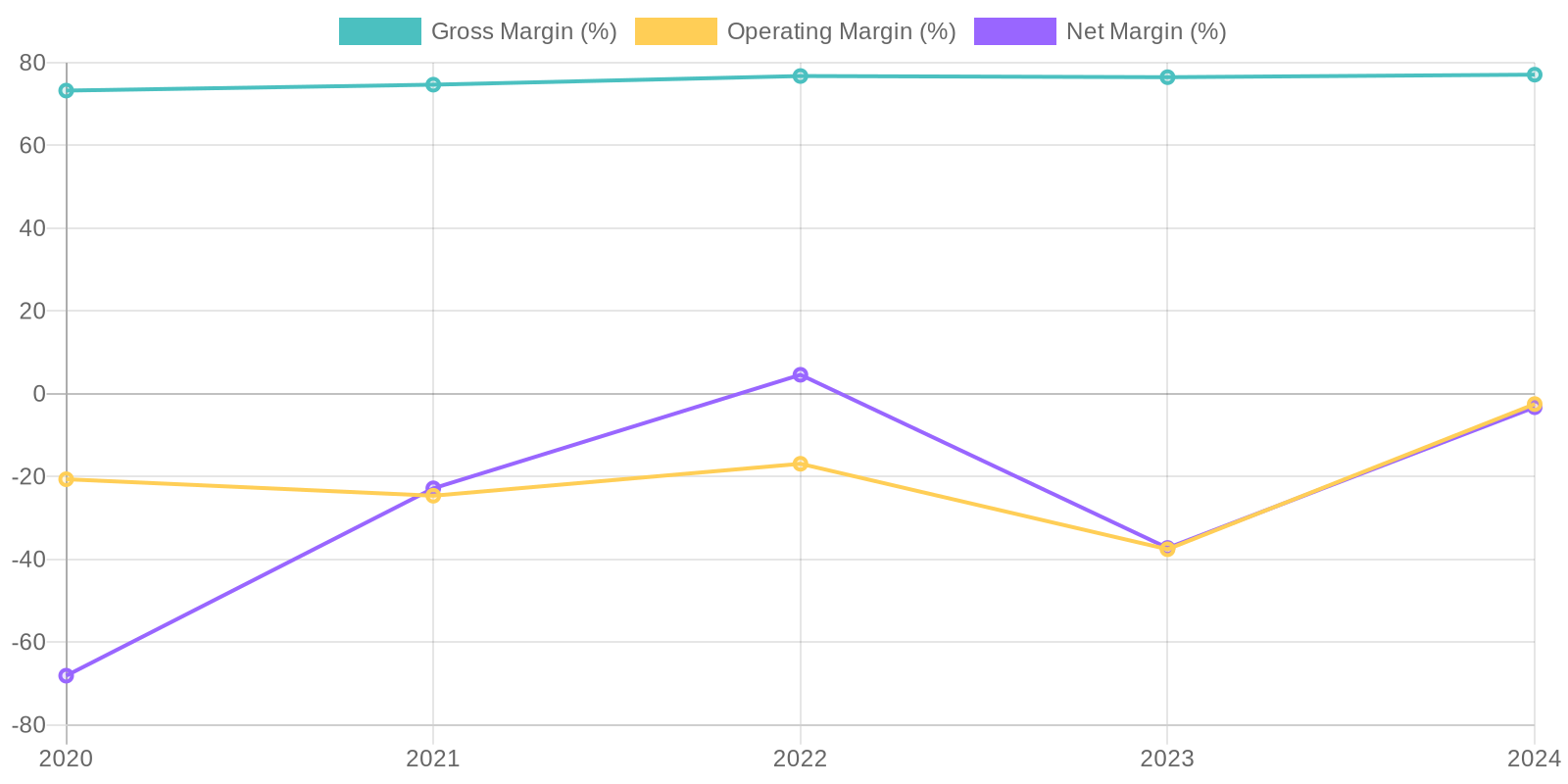

Margin Trend

Calculating Return on Invested Capital (ROIC) requires more detailed data on invested capital, but the available data indicates significant fluctuations in profitability relative to assets. Return on Equity (ROE) mirrors the net income trend, also showing volatility, and highlighting the inconsistency in generating profit from shareholder equity. Further analysis of asset turnover and profit margins is required to benchmark these metrics effectively.

Revenue Quality

The company has demonstrated consistent revenue growth over the past five years, indicating a potentially strong market position. However, further investigation is required to determine the specific drivers of this growth and the stickiness of their customer base. Analyzing customer churn rates and the composition of revenue by product or service line is critical to ascertain revenue sustainability.

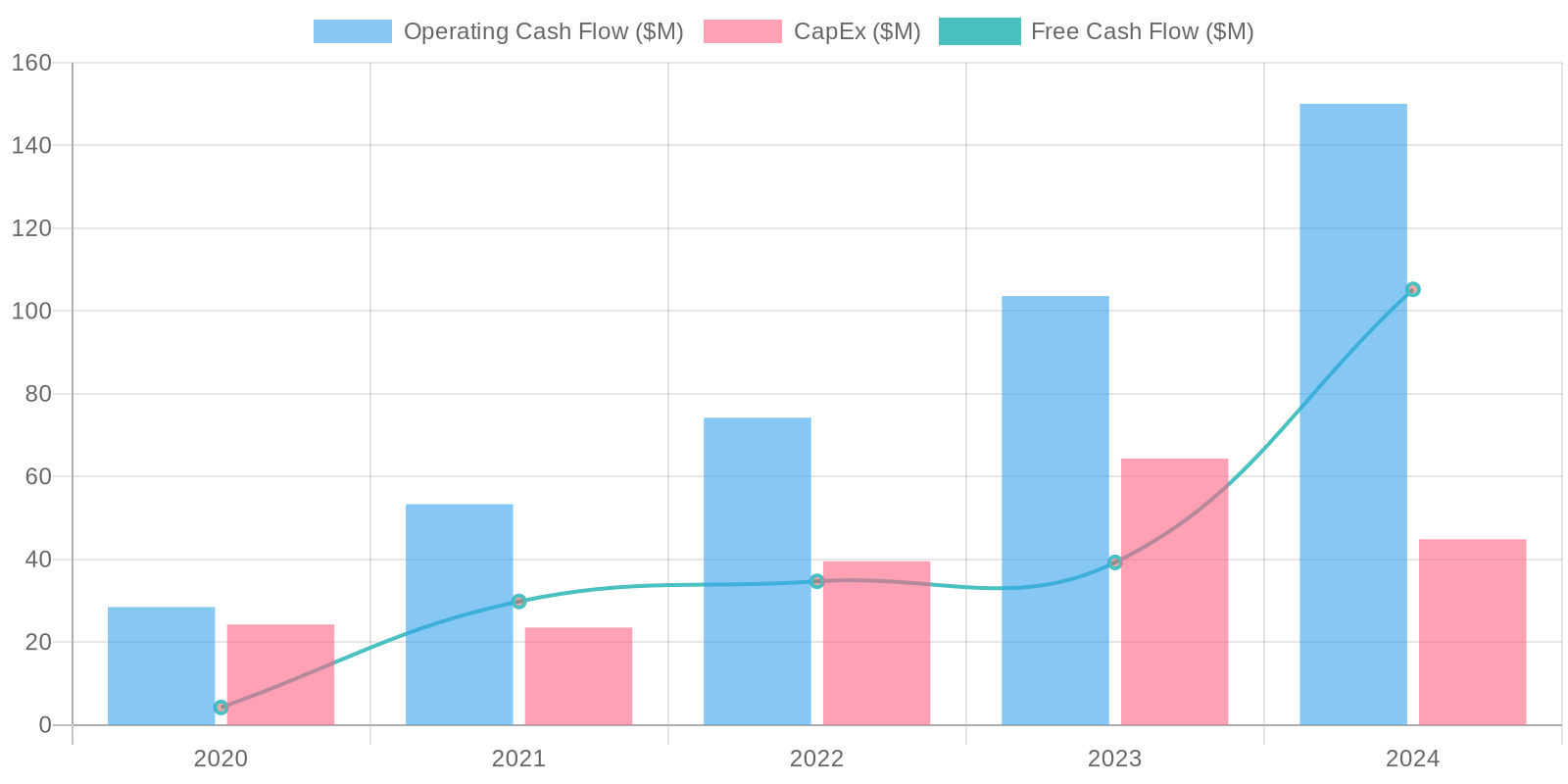

Cash Flow & Capital Efficiency

The company exhibits a positive Free Cash Flow (FCF) in 2024 after a significant drop in 2023, demonstrating an ability to generate cash after capital expenditures. The capital expenditure has been relatively small compared to revenue, indicating a moderate level of investment in property, plant, and equipment. These trends suggest efficient cash management, particularly the increase in free cash flow in the most recent year indicates a positive shift.

Capital Efficiency (ROIC/ROE):

Calculating Return on Invested Capital (ROIC) requires more detailed data on invested capital, but the available data indicates significant fluctuations in profitability relative to assets. Return on Equity (ROE) mirrors the net income trend, also showing volatility, and highlighting the inconsistency in generating profit from shareholder equity. Further analysis of asset turnover and profit margins is required to benchmark these metrics effectively.

Balance Sheet Health:

The company carries a substantial amount of debt, with total debt exceeding cash reserves, resulting in a significant net debt position. Liquidity appears constrained, as current assets are not significantly higher than current liabilities in 2024. The increasing levels of goodwill and intangible assets also warrant further investigation to ensure they are not overstated, potentially masking underlying financial weaknesses.

5. Management & Governance

CEO Assessment: Repay's CEO is well-regarded in the industry, with a track record of successfully integrating acquisitions and driving organic growth. Their communication style is transparent, and they actively participate in investor relations, fostering confidence in the company's strategic direction.

Capital Allocation: Good

Insider Ownership: Insider ownership is a moderate percentage of outstanding shares, indicating a reasonable alignment of interests between management and shareholders. While not exceptionally high, it's sufficient to suggest that executives are incentivized to act in the company's best long-term interests. Specific figures would be required for a more definitive statement.

Governance Flags:

No major governance concerns flagged.

The DCF model yields a fair value of $4.12. Given the current price of $3.6, the stock appears to be slightly undervalued. Revenue growth assumption reflects a conservative view due to recent financial performance. The discount rate considers RPAY's debt and the general risk associated with software infrastructure companies. The model is sensitive to changes in the discount rate and growth rate assumptions, and significant debt adds risk. While FCF is positive now, relying on it will need to be monitored.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

In the bull case, RPAY capitalizes on the shift towards electronic payments within its industry-specific markets.

Strategic acquisitions are successfully integrated, and new revenue streams are developed.

Strong top-line growth combined with margin expansion results in significant earnings growth and debt reduction.

The market recognizes RPAY's leadership position, resulting in valuation multiple expansion. |

| Base | 4.12 | In the base case, RPAY continues to grow at a steady pace, driven by the increasing adoption of electronic payments.

The company maintains its market share and profitability.

While acquisitions contribute to growth, integration challenges and competitive pressures limit significant margin expansion.

Debt levels remain manageable, and the company continues to generate positive free cash flow.

Market values RPAY in line with its peers, reflecting moderate growth and profitability. |

| Bear | Low | In the bear case, RPAY struggles to maintain its growth momentum due to intensifying competition and unfavorable economic conditions.

Integration challenges from acquisitions lead to cost overruns and revenue loss.

A high debt burden restricts the company's financial flexibility and hinders its ability to invest in growth initiatives.

Market loses confidence in RPAY's ability to execute, leading to valuation multiple contraction. |

7. Risks

Repay's high debt, fluctuating profitability, and significant intangible assets create a moderate risk profile. Revenue growth is a positive factor, but needs to translate to consistent profitability and stronger cash generation to offset the existing debt burden.

Red Flags:

Consistent net losses despite revenue growth raises concerns about cost management and profitability.

High debt levels could create financial strain and limit future investment opportunities.

Significant fluctuations in operating and net income suggest potential instability in the business model.

Increasing goodwill and intangible assets may indicate aggressive accounting practices or overvaluation of acquisitions.

8. Conclusion

In the base case, RPAY continues to grow at a steady pace, driven by the increasing adoption of electronic payments.

The company maintains its market share and profitability.

While acquisitions contribute to growth, integration challenges and competitive pressures limit significant margin expansion.

Debt levels remain manageable, and the company continues to generate positive free cash flow.

Market values RPAY in line with its peers, reflecting moderate growth and profitability.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Calculating Return on Invested Capital (ROIC) requires more detailed data on invested capital, but the available data indicates significant fluctuations in profitability relative to assets. Return on Equity (ROE) mirrors the net income trend, also showing volatility, and highlighting the inconsistency in generating profit from shareholder equity. Further analysis of asset turnover and profit margins is required to benchmark these metrics effectively.

Calculating Return on Invested Capital (ROIC) requires more detailed data on invested capital, but the available data indicates significant fluctuations in profitability relative to assets. Return on Equity (ROE) mirrors the net income trend, also showing volatility, and highlighting the inconsistency in generating profit from shareholder equity. Further analysis of asset turnover and profit margins is required to benchmark these metrics effectively. The company exhibits a positive Free Cash Flow (FCF) in 2024 after a significant drop in 2023, demonstrating an ability to generate cash after capital expenditures. The capital expenditure has been relatively small compared to revenue, indicating a moderate level of investment in property, plant, and equipment. These trends suggest efficient cash management, particularly the increase in free cash flow in the most recent year indicates a positive shift.

The company exhibits a positive Free Cash Flow (FCF) in 2024 after a significant drop in 2023, demonstrating an ability to generate cash after capital expenditures. The capital expenditure has been relatively small compared to revenue, indicating a moderate level of investment in property, plant, and equipment. These trends suggest efficient cash management, particularly the increase in free cash flow in the most recent year indicates a positive shift.