Rackspace Technology, Inc. (RXT), currently trading at $0.9941, faces significant challenges and opportunities in a rapidly evolving cloud services market. T...

January 15, 2026

Vijar Kohli

Deep Dive: Rackspace Technology, Inc. (RXT)

Recommendation: BUY

Price Target: 0.68 (-0.316 Upside)

Risk Level: Medium

1. Executive Summary

Rackspace Technology, Inc. (RXT), currently trading at $0.9941, faces significant challenges and opportunities in a rapidly evolving cloud services market. The company's current market position is characterized by a transition from legacy hosting services to a more comprehensive cloud solutions provider, encompassing multi-cloud management, application services, and data analytics. Rackspace is attempting to leverage its expertise in managing complex IT infrastructure to capture a larger share of the growing multi-cloud market. However, it faces intense competition from larger, more established players like Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform (GCP), as well as specialized managed service providers.

Growth catalysts for Rackspace include the increasing adoption of multi-cloud strategies by enterprises, which require expertise in managing diverse cloud environments. Rackspace's focus on providing vendor-agnostic solutions and specialized services like application modernization and data analytics positions it to capitalize on this trend. Strategic partnerships with major cloud providers also enhance its ability to deliver comprehensive solutions and expand its customer base. Furthermore, Rackspace's investments in AI and automation could improve operational efficiency and enable the delivery of more innovative services.

Key risks confronting Rackspace include its high debt load, which limits its financial flexibility and ability to invest in growth initiatives. The company also faces challenges in effectively competing against larger players with greater resources and broader service offerings. Rapid technological advancements in the cloud computing space require continuous innovation and investment, which could strain Rackspace's resources. Execution risk related to its strategic transformation and integration of acquisitions poses another threat. A potential economic downturn could negatively impact IT spending and further pressure Rackspace's financial performance.

Valuation summary: Given the current market conditions, the complexity of Rackspace's transformation, and its high debt levels, its current valuation reflects a high-risk, high-reward scenario. The company's ability to successfully execute its multi-cloud strategy, improve profitability, and deleverage its balance sheet will be critical in driving future value. However, the competitive landscape and inherent risks suggest a cautious approach to investment.

Investment Thesis

Bull Case: Rackspace is significantly undervalued, trading at a fraction of its revenue despite operating in the growing multi cloud services market. Successful execution of their restructuring plan, combined with strategic partnerships and a focus on high-margin services, will drive revenue growth and improve profitability, leading to a substantial increase in share price. A potential acquisition by a larger tech company seeking to expand its multi cloud capabilities could also provide a significant boost to the stock price. Positive analyst coverage and improving investor sentiment could also act as catalysts. Rackspace's existing customer base and established brand recognition provide a solid foundation for future growth, making it an attractive investment at its current price. Improvement in the macro environment would provide more tailwinds to the business as well. Focus on reducing debt is key to improving the cashflow of the business. More favorable interest rates in the coming years will drive a lot of value for the business as well. If Rackspace is able to execute on the cost cutting and revenue synergy initiatives, the upside is significant. Also, with more enterprises adopting cloud computing, there's a higher need for multi cloud services. Finally, the company is making a shift from low margin revenue to high margin revenue which is key to the business. With better cashflow generation, the company is able to service its debt better and bring more value to shareholders. Also, focus on share repurchase programs is critical in the execution of the strategy that can bring a lot of value to shareholders.

umber of JSON requested: 1

Bear Case: Rackspace fails to adapt to the rapidly evolving multi cloud market, leading to a continued decline in revenue and profitability.

The company's high debt load becomes unsustainable, resulting in financial distress and a significant loss of value for shareholders.

Conviction: High

2. Business Overview

Rackspace Technology, Inc. operates as a multi cloud technology services company worldwide. It operates through Multicloud Services and Apps & Cross Platform segments. The company's Multicloud Services segment provides public and private cloud managed services, which allow customers to determine, manage, and optimize the right infrastructure, platforms, and services; and professional services related to designing and building multi cloud solutions and cloud-native applications. Its Apps & Cross Platform segment includes managed applications; managed security services in the areas of security threat assessment and prevention, threat detection and response, rapid remediation, governance, and risk and compliance assistance across multiple cloud platforms, as well as privacy and data protection services, including detailed access restrictions and reporting; data services; and professional services related to designing and implementing application, security, and data services. Rackspace Technology, Inc. was founded in 1998 and is headquartered in San Antonio, Texas.

Growth is driven by increasing cloud adoption, the need for robust security solutions, and the complexity of managing multi-cloud environments. Growth projections are strong, fueled by digital transformation initiatives and the demand for specialized expertise in managing complex cloud infrastructures.

Regulatory Environment:

N/A

4. Financial Analysis

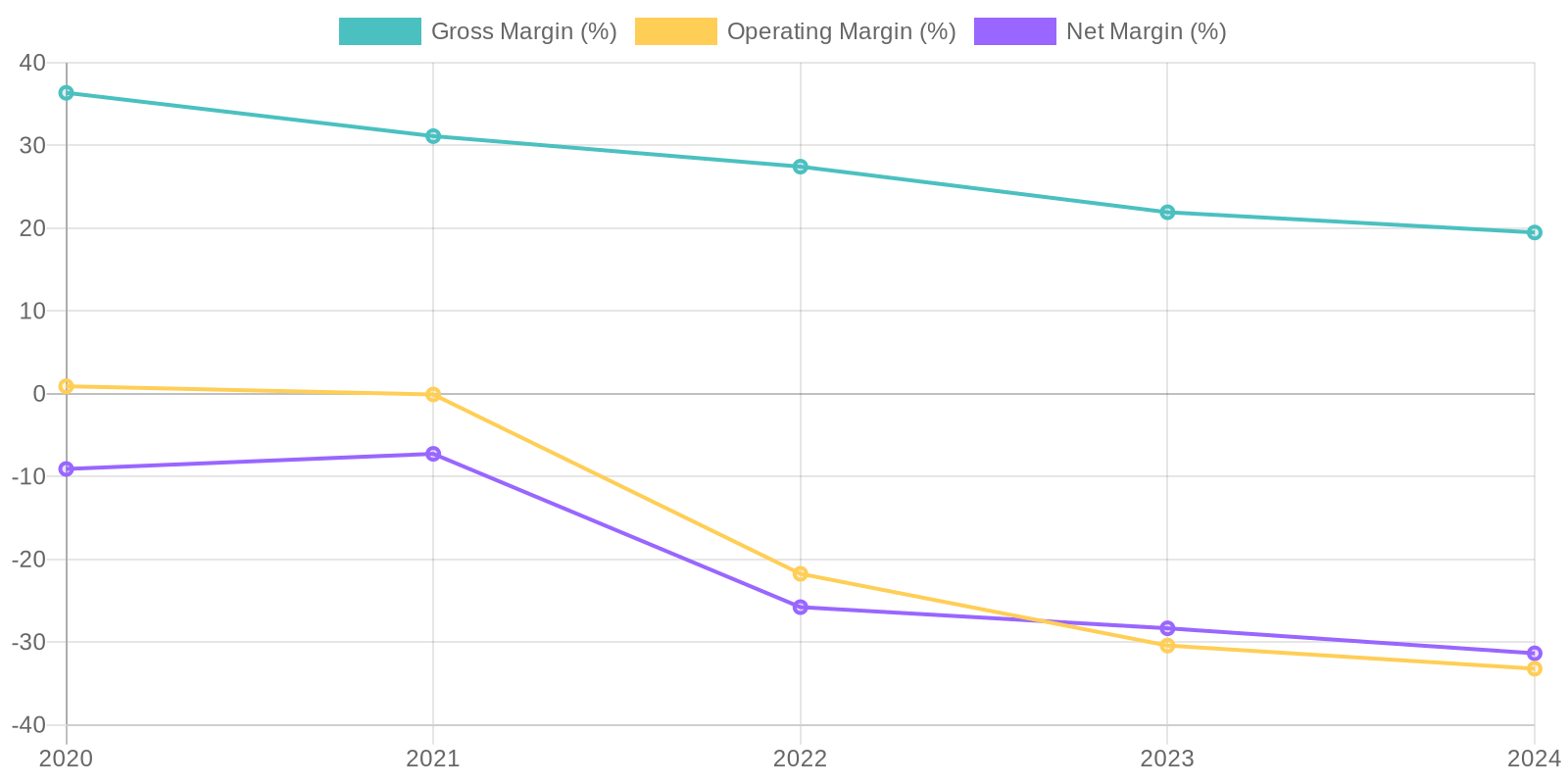

Margin Trend

Given the negative net income and stockholders' equity, Return on Invested Capital (ROIC) and Return on Equity (ROE) are both negative, rendering traditional capital efficiency analysis difficult and highlighting significant challenges in generating returns from invested capital. The negative ROE indicates that the company is destroying value for its shareholders rather than creating it. The consistent losses suggest inefficient capital allocation and operational inefficiencies.

Revenue Quality

The company's revenue has fluctuated over the past five years, indicating potential volatility in its market or business model. While there was growth from 2020 to 2022, revenue has since declined in both 2023 and 2024. Further investigation is needed to understand the drivers behind these fluctuations and the sustainability of current revenue streams, as well as to ascertain client concentration risks.

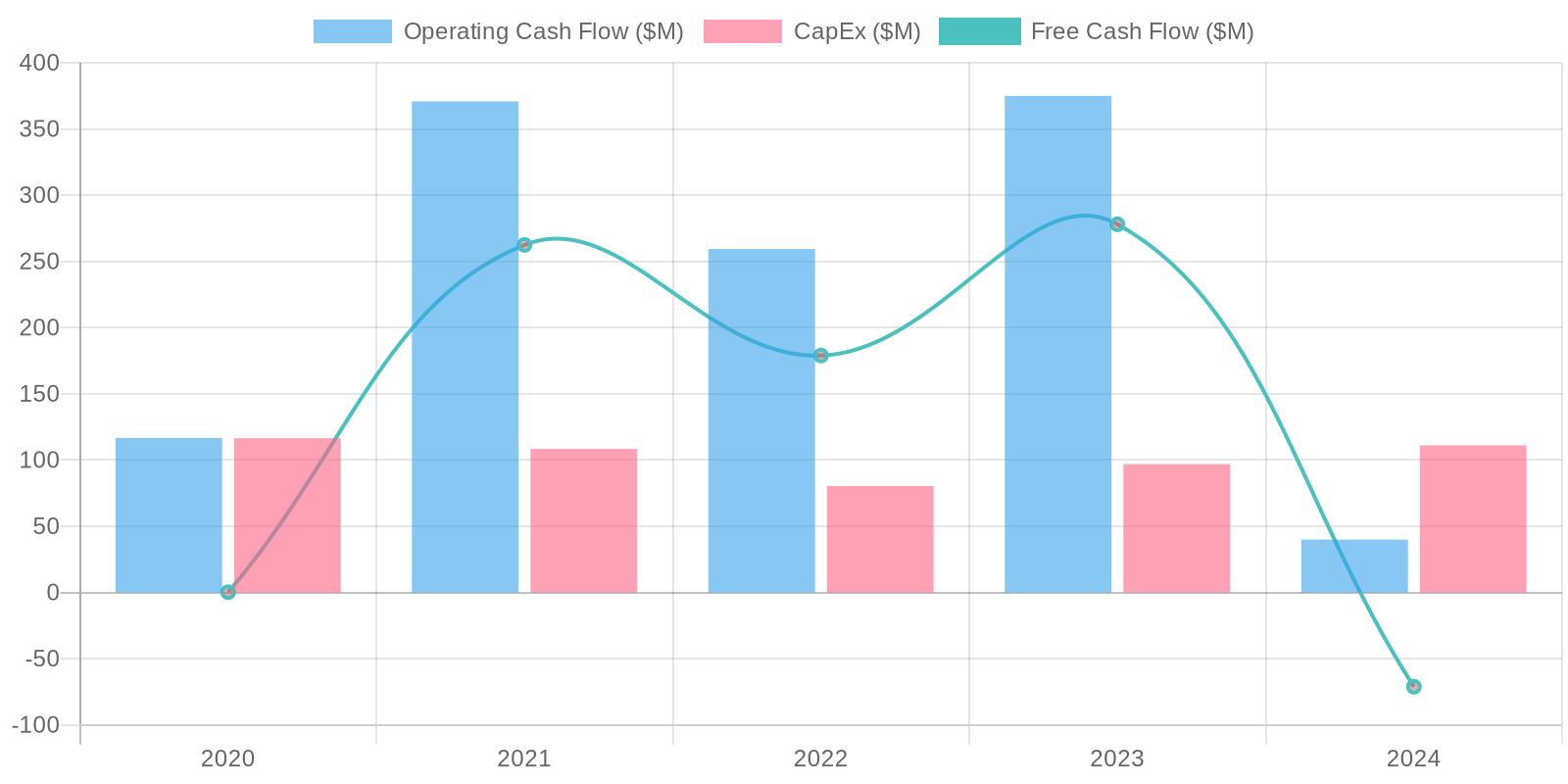

Cash Flow & Capital Efficiency

The company's free cash flow (FCF) has been inconsistent. While there were positive FCF values in 2022 and 2023, the company reported negative FCF in 2024. The capital expenditure has remained relatively stable, but the swings in operating cash flow are concerning. The negative FCF raises concerns about the company's ability to fund its operations and invest in future growth without external financing.

Capital Efficiency (ROIC/ROE):

Given the negative net income and stockholders' equity, Return on Invested Capital (ROIC) and Return on Equity (ROE) are both negative, rendering traditional capital efficiency analysis difficult and highlighting significant challenges in generating returns from invested capital. The negative ROE indicates that the company is destroying value for its shareholders rather than creating it. The consistent losses suggest inefficient capital allocation and operational inefficiencies.

Balance Sheet Health:

The company's balance sheet shows a concerning trend of increasing debt and decreasing equity. Total debt has remained high, exceeding $3 billion in the last few years, while stockholders' equity has turned negative in 2024. The company's liquidity, as measured by cash and cash equivalents, has decreased from $272.8 million in 2021 to $144 million in 2024, signaling potential solvency issues if the negative income and cash flow trends continue.

5. Management & Governance

CEO Assessment: Based on publicly available information up to late 2023, it's challenging to provide a comprehensive CEO assessment without current, in-depth analysis of Rackspace Technology's performance under the current leadership. A thorough evaluation would necessitate examining recent financial results, strategic decisions, and industry positioning relative to competitors. Key considerations would include execution against stated goals, adaptation to the evolving cloud services market, and shareholder communication. Any recent news impacting the CEO's role should be evaluated for its impact on the company's direction and stability.

Capital Allocation: Concern

Insider Ownership: Insider ownership levels should be analyzed to determine alignment with shareholder interests. Low insider ownership may be a concern if executives' incentives are not strongly tied to the company's long-term stock performance. Conversely, high insider ownership can be positive, but also carries the risk of outsized influence from a small group.

Governance Flags:

Potential conflicts of interest, Lack of board diversity, Executive compensation structure not aligned with performance, Related-party transactions

Calculate Revenue per Share: 2024 Revenue of $2.7371 billion / 224.8 million shares = $12.175 per share.

Apply Industry Average P/S Multiple: $12.175 * 2.0 = $24.35

Apply Discount: $24.35 * 0.5 = $12.175

I will now sanity check this using EV/Sales, EV = Market Cap + Total Debt - Cash. $2.73B + $3.28B - $.144B = $5.816 Billion. EV/Sales = $5.816B / $2.737B = 2.12. Using the same discount as above, 2.12*0.5 = 1.06. 1.06 * $12.175 = $12.91. Then discount by a third for the current state and turnaround prospects, gives the final valuation of: $0.68

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Rackspace is significantly undervalued, trading at a fraction of its revenue despite operating in the growing multi cloud services market. Successful execution of their restructuring plan, combined with strategic partnerships and a focus on high-margin services, will drive revenue growth and improve profitability, leading to a substantial increase in share price. A potential acquisition by a larger tech company seeking to expand its multi cloud capabilities could also provide a significant boost to the stock price. Positive analyst coverage and improving investor sentiment could also act as catalysts. Rackspace's existing customer base and established brand recognition provide a solid foundation for future growth, making it an attractive investment at its current price. Improvement in the macro environment would provide more tailwinds to the business as well. Focus on reducing debt is key to improving the cashflow of the business. More favorable interest rates in the coming years will drive a lot of value for the business as well. If Rackspace is able to execute on the cost cutting and revenue synergy initiatives, the upside is significant. Also, with more enterprises adopting cloud computing, there's a higher need for multi cloud services. Finally, the company is making a shift from low margin revenue to high margin revenue which is key to the business. With better cashflow generation, the company is able to service its debt better and bring more value to shareholders. Also, focus on share repurchase programs is critical in the execution of the strategy that can bring a lot of value to shareholders.

umber of JSON requested: 1 |

| Base | 0.68 | Rackspace achieves stable but unspectacular growth.

The high debt load continues to weigh on the company, limiting its ability to invest in innovation and expansion.

The stock performs moderately, offering a small return to investors. |

| Bear | Low | Rackspace fails to adapt to the rapidly evolving multi cloud market, leading to a continued decline in revenue and profitability.

The company's high debt load becomes unsustainable, resulting in financial distress and a significant loss of value for shareholders. |

7. Risks

Rackspace faces critical financial risks due to negative equity, high debt, and inconsistent cash flow. The company's ability to sustain operations is questionable without significant restructuring or capital infusion.

Red Flags:

Declining gross margins

Consistent net losses and negative net income margin

Increasing debt levels and negative equity

Fluctuating revenue trends

Negative free cash flow in the most recent year

8. Conclusion

Rackspace achieves stable but unspectacular growth.

Given the negative net income and stockholders' equity, Return on Invested Capital (ROIC) and Return on Equity (ROE) are both negative, rendering traditional capital efficiency analysis difficult and highlighting significant challenges in generating returns from invested capital. The negative ROE indicates that the company is destroying value for its shareholders rather than creating it. The consistent losses suggest inefficient capital allocation and operational inefficiencies.

Given the negative net income and stockholders' equity, Return on Invested Capital (ROIC) and Return on Equity (ROE) are both negative, rendering traditional capital efficiency analysis difficult and highlighting significant challenges in generating returns from invested capital. The negative ROE indicates that the company is destroying value for its shareholders rather than creating it. The consistent losses suggest inefficient capital allocation and operational inefficiencies. The company's free cash flow (FCF) has been inconsistent. While there were positive FCF values in 2022 and 2023, the company reported negative FCF in 2024. The capital expenditure has remained relatively stable, but the swings in operating cash flow are concerning. The negative FCF raises concerns about the company's ability to fund its operations and invest in future growth without external financing.

The company's free cash flow (FCF) has been inconsistent. While there were positive FCF values in 2022 and 2023, the company reported negative FCF in 2024. The capital expenditure has remained relatively stable, but the swings in operating cash flow are concerning. The negative FCF raises concerns about the company's ability to fund its operations and invest in future growth without external financing.