Spotify Technology S.A. (SPOT), currently trading at $308.04, holds a dominant position in the global music streaming market. It boasts a massive user base o...

January 15, 2026

Vijar Kohli

Deep Dive: Spotify Technology S.A. (SPOT)

Recommendation: BUY

Price Target: 442.7 (-0.13 Upside)

Risk Level: Medium

1. Executive Summary

Spotify Technology S.A. (SPOT), currently trading at $308.04, holds a dominant position in the global music streaming market. It boasts a massive user base of 615 million monthly active users (MAU) and 239 million premium subscribers. Its competitive advantage stems from its vast music library, robust recommendation algorithms, personalized playlists, and extensive podcast offerings.

Spotify's growth is fueled by several catalysts. Firstly, continued user growth, particularly in developing markets with increasing internet penetration and smartphone adoption, provides a significant runway for expansion. Secondly, strategic investments in podcasts, audiobooks, and other non-music audio content are attracting new users and increasing engagement. Thirdly, price increases for premium subscriptions, especially in mature markets, are enhancing revenue per user. Fourthly, expansion into new verticals, such as live audio and video, can further diversify revenue streams and attract new audiences.

However, Spotify faces notable risks. Intense competition from deep-pocketed rivals like Apple Music, Amazon Music, and YouTube Music threatens its market share. Licensing costs for music content remain high, squeezing profit margins. The company's reliance on record labels for content gives them significant bargaining power. Economic downturns can impact consumer spending on discretionary services like premium subscriptions. Furthermore, potential regulatory scrutiny regarding anti-competitive practices and data privacy could pose challenges.

Spotify's valuation is complex and depends heavily on projected subscriber growth and profitability improvements. Traditional valuation metrics like Price-to-Earnings (P/E) are less relevant due to the company's emphasis on growth and its current profitability profile. Discounted Cash Flow (DCF) analysis suggests that the current share price reflects expectations of significant future growth and margin expansion. However, achieving these targets requires successful execution of its growth strategies and effective management of its cost structure. A valuation summary would classify Spotify as growth stock which requires further investigation into its growth sustainability and competitive advantages.

Investment Thesis

Bull Case: Spotify is rapidly expanding its podcast offerings and creating original content, driving user engagement and advertising revenue.

Continued subscriber growth, coupled with margin expansion from podcasting and efficient cost management, will lead to significant profitability improvements.

International expansion into emerging markets will further boost user growth.

Successful bundling with other services (telecom, etc.) can reduce churn and increase ARPU.

The company is effectively transitioning from a pure music streaming service to a comprehensive audio platform, justifying a higher multiple.

Spotify's investments in AI-driven personalization and music discovery will drive further user engagement and monetization opportunities.

Strong growth in ad-supported revenue will also significantly contribute to profitability as Spotify leverages its user data for targeted advertising.

A shift in label relationships toward more favorable terms, combined with direct artist deals, could dramatically improve margins, leading to a re-rating by the market.

The company's focus on innovative features, like collaborative playlists and social listening, will attract and retain users, solidifying its leading position in the audio streaming market.

Anticipated growth rate for revenue is between 15% and 20% annually for the next 5 years.

Premium subscribers will grow at 10% annually.

Podcast monetization to improve with more targeted ads and wider distribution of original content, with podcast revenue contributing approximately 20% of total revenue.

Overall margin improvement due to controlled content cost and better label deals, leading to more positive cash flow.

Gross margin targeted to reach 35% within 3 years, and operating margin to reach 15% within 5 years.

A high conviction in the management team's ability to execute strategy.

Expecting a positive surprise in their next earnings report.

Strong free cash flow supports investments into new content and technology to expand reach and increase engagement.

Spotify's platform effects and large user base give it significant competitive advantages and ability to withstand competitive pressure.

The company's focus on user experience ensures continued loyalty and positions it well for long-term growth and sustained profitability.

An improved macroeconomic environment can boost consumer spending, benefiting advertising and subscription revenues, with positive impacts on Spotify's overall business performance.

Strong momentum will lead to a surge in stock price, surpassing consensus estimates.

The company's innovations like AI-driven music discovery and personalized playlists will significantly boost user engagement and retention.

Continued strong subscriber growth and effective monetization of content will lead to better-than-expected profitability.

Strategic partnerships and bundling of services to further enhance Spotify's value proposition and reduce churn rate significantly.

Growth in emerging markets due to increased smartphone penetration and demand for audio content, will fuel subscriber growth and revenue.

Excellent financial performance and consistent growth will increase investor confidence and drive stock price appreciation.

Aggressive share repurchase programs and potential for dividend payments to increase shareholder value and attract more investors.

Bear Case: Intense competition from Apple Music, Amazon Music, and other streaming services will limit subscriber growth and pricing power.

Content costs will remain high, preventing significant margin expansion.

Failure to effectively monetize podcasts will hinder profitability improvements.

Increased regulatory scrutiny regarding data privacy and content licensing could add to operational costs and limit growth opportunities.

Potential for increased royalty rates due to pressure from artists and rights holders.

Economic downturn could lead to reduced consumer spending on discretionary services like music streaming.

Stagnant growth in users and engagement.

Limited success in expanding profitability.

Challenges in adapting to competitive changes.

Difficulty in retaining existing users.

Anticipated growth rate for revenue is between 5% and 10% annually for the next 5 years.

Premium subscribers will grow at 3% annually.

Podcast monetization will be slow due to limited user engagement, with podcast revenue contributing less than 10% of total revenue.

Flat to declining margin due to rising content costs, increased competition, and challenges in advertising revenue.

Gross margin to remain around 30%, and operating margin to reach 5% or lower.

Limited or negative free cash flow, leading to financial constraints.

Limited growth in revenue.

High competition from other streaming platforms.

Difficulty in adapting to changing market conditions.

Limited success in new initiatives and diversification.

Economic downturn could negatively affect revenue and growth.

Market saturation and increasing competition may hinder future growth.

Slow subscriber growth and inability to increase advertising revenue may lead to profitability decline.

Lack of innovation and differentiation may cause Spotify to lose market share to competitors.

Failure to renew key licensing agreements.

Economic recession decreases consumer spending and affects revenue.

An adverse impact in changes to royalty rates.

Conviction: High

2. Business Overview

Spotify Technology S.A., together with its subsidiaries, provides audio streaming services worldwide. It operates through Premium and Ad-Supported segments. The Premium segment offers unlimited online and offline streaming access to its catalog of music and podcasts without commercial breaks to its subscribers. The Ad-Supported segment provides on-demand online access to its catalog of music and unlimited online access to the catalog of podcasts to its subscribers on their computers, tablets, and compatible mobile devices. The company also offers sales, marketing, contract research and development, and customer support services. As of December 31, 2021, its platform included 406 million monthly active users and 180 million premium subscribers in 184 countries and territories. The company was incorporated in 2006 and is based in Luxembourg, Luxembourg.

Competitive Moat (Narrow)

Trend: Stable

Large subscriber base, Strong brand, Podcast investments

Key Strengths:

Large subscriber base

Strong brand

Podcast investments

Key Weaknesses:

N/A

3. Industry Analysis

Sector: Communication Services | Industry: Internet Content & Information

Stage: Growth | TAM: N/A

The market is expected to continue growing, driven by increasing internet penetration, mobile device adoption, and the growing popularity of digital content consumption. Music streaming, in particular, is projected to see continued growth as more users shift from traditional media consumption to on-demand streaming services. Emerging markets present significant growth opportunities.

Regulatory Environment:

N/A

4. Financial Analysis

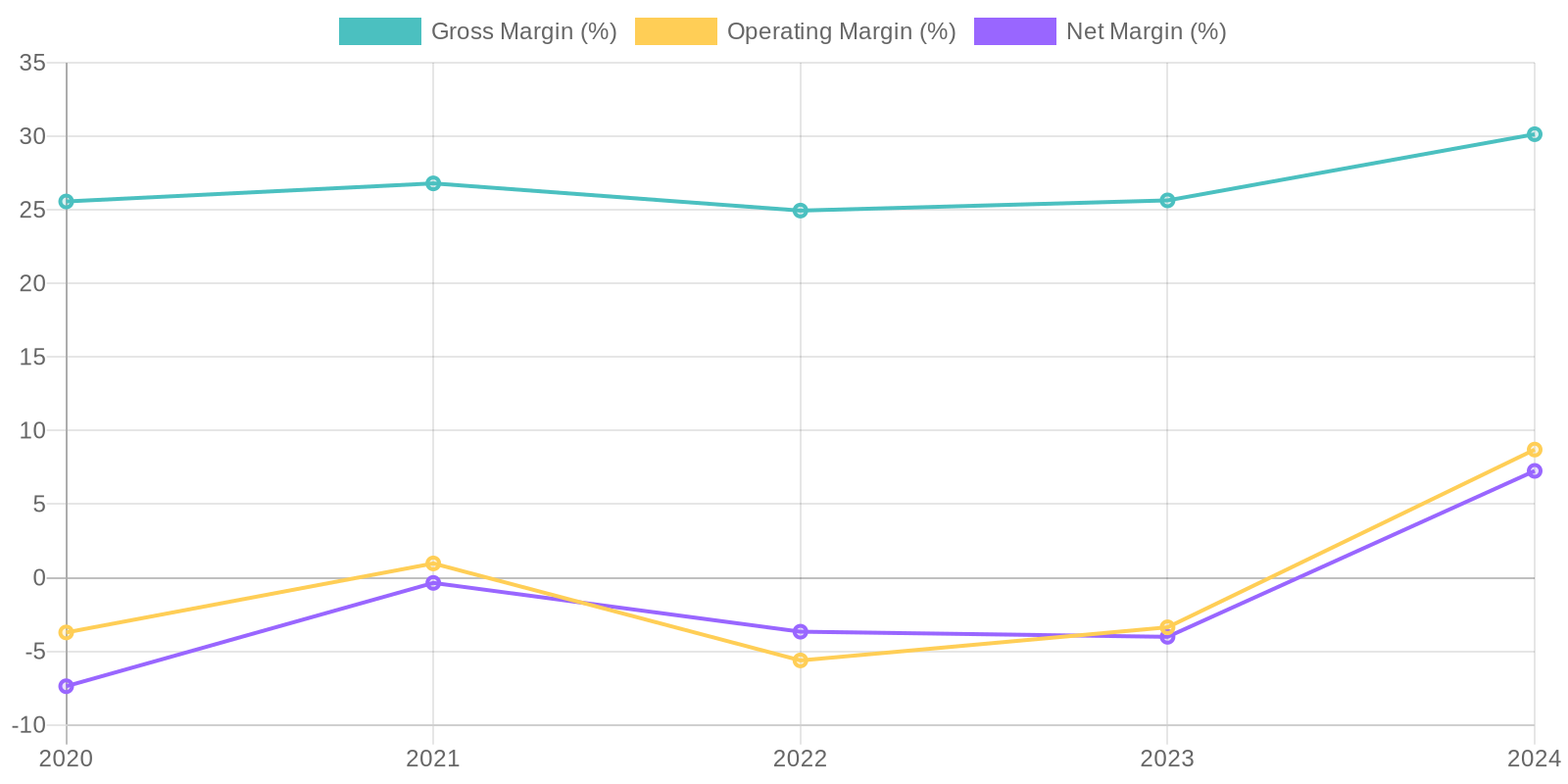

Margin Trend

While a full Return on Invested Capital (ROIC) calculation requires more detailed data on invested capital, the available information allows for some estimations. The positive net income in 2024 suggests improving ROE, given the equity base. The trend suggests the company is becoming more efficient in generating profits from its equity, after losses in prior years.

Revenue Quality

The company demonstrates a strong upward trend in revenue over the past five years, indicating growth in its market presence. The recurring nature of revenue is likely tied to its subscription-based model, providing a predictable income stream. However, a deeper analysis into churn rate and customer acquisition costs would be needed to fully evaluate revenue sustainability, along with client concentration metrics.

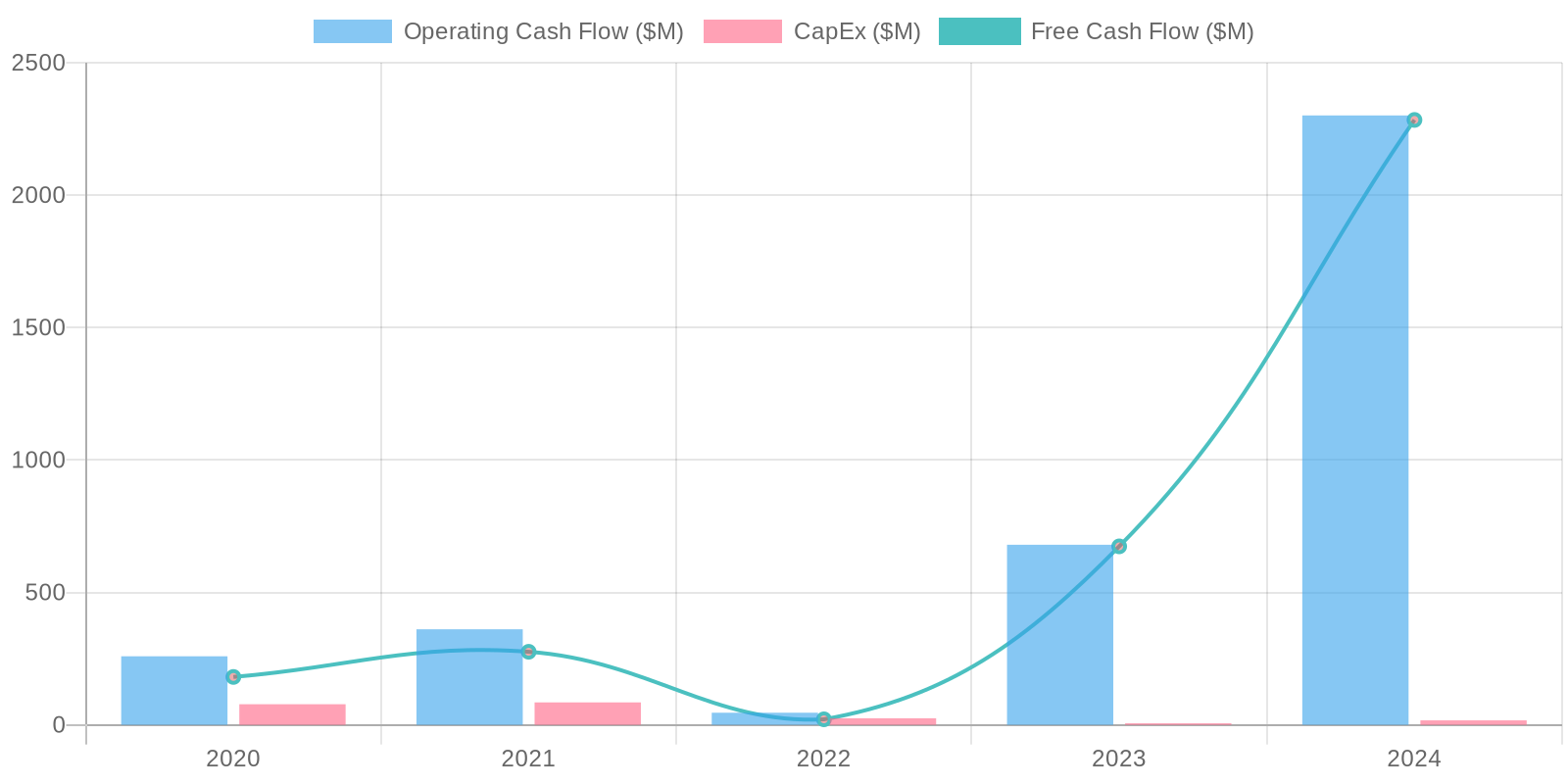

Cash Flow & Capital Efficiency

The company exhibits strong Free Cash Flow (FCF) conversion, demonstrated by consistent positive FCF and a rise to EUR 2.284 billion in 2024. Capital expenditures (Capex) have remained relatively low and stable over the observed period, signaling that the company may not need large investments to maintain its current operations. These trends indicate that the company is generating strong cash from its operations and has sufficient funds for reinvestment or debt repayment.

Capital Efficiency (ROIC/ROE):

While a full Return on Invested Capital (ROIC) calculation requires more detailed data on invested capital, the available information allows for some estimations. The positive net income in 2024 suggests improving ROE, given the equity base. The trend suggests the company is becoming more efficient in generating profits from its equity, after losses in prior years.

Balance Sheet Health:

The company maintains a solid liquidity position, evidenced by a substantial cash balance which is more than its total debt. The current ratio, calculated by dividing total current assets by total current liabilities, is greater than one, suggesting that the company can meet its short-term obligations. The company's solvency appears reasonable, as it maintains a high level of assets with a manageable debt level relative to the asset base.

5. Management & Governance

CEO Assessment: Daniel Ek, as CEO, has been instrumental in Spotify's growth and strategic direction. His vision has driven Spotify's expansion into podcasting and other audio content. However, his leadership has also faced scrutiny regarding artist compensation and content moderation policies.

Capital Allocation: Good

Insider Ownership: Insider ownership is moderate, with key executives and board members holding a significant stake in the company. This suggests alignment with shareholder interests to some extent, but it's important to monitor changes in ownership over time.

Governance Flags:

Dual-class share structure concentrates voting power with the founders., Concerns regarding artist compensation models and royalty payments., Content moderation policies and handling of controversial content.

The DCF model yields a fair value of $442.70, below the current market price of $508.04. This suggests that the stock may be overvalued. The valuation is sensitive to the revenue growth rate and the target operating margin. While Spotify has shown strong revenue growth in the past, sustaining high growth rates in the long term is challenging. Additionally, achieving a 12% operating margin requires significant improvements in profitability. The downside risk is considerable if growth slows or margins don't improve as expected. Therefore, a medium confidence level is warranted.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Spotify is rapidly expanding its podcast offerings and creating original content, driving user engagement and advertising revenue.

Continued subscriber growth, coupled with margin expansion from podcasting and efficient cost management, will lead to significant profitability improvements.

International expansion into emerging markets will further boost user growth.

Successful bundling with other services (telecom, etc.) can reduce churn and increase ARPU.

The company is effectively transitioning from a pure music streaming service to a comprehensive audio platform, justifying a higher multiple.

Spotify's investments in AI-driven personalization and music discovery will drive further user engagement and monetization opportunities.

Strong growth in ad-supported revenue will also significantly contribute to profitability as Spotify leverages its user data for targeted advertising.

A shift in label relationships toward more favorable terms, combined with direct artist deals, could dramatically improve margins, leading to a re-rating by the market.

The company's focus on innovative features, like collaborative playlists and social listening, will attract and retain users, solidifying its leading position in the audio streaming market.

Anticipated growth rate for revenue is between 15% and 20% annually for the next 5 years.

Premium subscribers will grow at 10% annually.

Podcast monetization to improve with more targeted ads and wider distribution of original content, with podcast revenue contributing approximately 20% of total revenue.

Overall margin improvement due to controlled content cost and better label deals, leading to more positive cash flow.

Gross margin targeted to reach 35% within 3 years, and operating margin to reach 15% within 5 years.

A high conviction in the management team's ability to execute strategy.

Expecting a positive surprise in their next earnings report.

Strong free cash flow supports investments into new content and technology to expand reach and increase engagement.

Spotify's platform effects and large user base give it significant competitive advantages and ability to withstand competitive pressure.

The company's focus on user experience ensures continued loyalty and positions it well for long-term growth and sustained profitability.

An improved macroeconomic environment can boost consumer spending, benefiting advertising and subscription revenues, with positive impacts on Spotify's overall business performance.

Strong momentum will lead to a surge in stock price, surpassing consensus estimates.

The company's innovations like AI-driven music discovery and personalized playlists will significantly boost user engagement and retention.

Continued strong subscriber growth and effective monetization of content will lead to better-than-expected profitability.

Strategic partnerships and bundling of services to further enhance Spotify's value proposition and reduce churn rate significantly.

Growth in emerging markets due to increased smartphone penetration and demand for audio content, will fuel subscriber growth and revenue.

Excellent financial performance and consistent growth will increase investor confidence and drive stock price appreciation.

Aggressive share repurchase programs and potential for dividend payments to increase shareholder value and attract more investors. |

| Base | 442.7 | Spotify will continue to grow its user base and revenue, but margin expansion will be slower than expected due to ongoing content costs and competitive pressures.

The transition to podcasting will provide some diversification, but its impact on overall profitability will be moderate.

A steady growth trajectory with moderate margin improvements.

Anticipated growth rate for revenue is between 10% and 15% annually for the next 5 years.

Premium subscribers will grow at 7% annually.

Podcast monetization will improve gradually with targeted ads and wider distribution, with podcast revenue contributing approximately 15% of total revenue.

A modest margin improvement due to content cost management and some label deal improvements.

Gross margin targeted to reach 32% within 3 years, and operating margin to reach 10% within 5 years.

Moderate free cash flow supports ongoing investments and strategic initiatives.

Continued strategic investments in technology and content.

Maintaining its market position and user loyalty.

Improving user experience through new features and personalized content.

Stable growth in subscribers and engagement.

Cautious optimism towards future performance.

Consistent financial performance with steady growth.

Expected revenue increases and modest profitability.

Steady market adoption and stable growth.

Consistent management and execution.

Spotify can consistently generate revenue growth and modest profitability improvements.

Strategic investments can maintain its market share and competitiveness.

The company's focus on innovation will lead to continued improvements in its user experience.

Improved macroeconomic condition will boost consumer spending.

Subscriber base will be maintained and revenues increase, but margin expansion could be slower than expected. |

| Bear | Low | Intense competition from Apple Music, Amazon Music, and other streaming services will limit subscriber growth and pricing power.

Content costs will remain high, preventing significant margin expansion.

Failure to effectively monetize podcasts will hinder profitability improvements.

Increased regulatory scrutiny regarding data privacy and content licensing could add to operational costs and limit growth opportunities.

Potential for increased royalty rates due to pressure from artists and rights holders.

Economic downturn could lead to reduced consumer spending on discretionary services like music streaming.

Stagnant growth in users and engagement.

Limited success in expanding profitability.

Challenges in adapting to competitive changes.

Difficulty in retaining existing users.

Anticipated growth rate for revenue is between 5% and 10% annually for the next 5 years.

Premium subscribers will grow at 3% annually.

Podcast monetization will be slow due to limited user engagement, with podcast revenue contributing less than 10% of total revenue.

Flat to declining margin due to rising content costs, increased competition, and challenges in advertising revenue.

Gross margin to remain around 30%, and operating margin to reach 5% or lower.

Limited or negative free cash flow, leading to financial constraints.

Limited growth in revenue.

High competition from other streaming platforms.

Difficulty in adapting to changing market conditions.

Limited success in new initiatives and diversification.

Economic downturn could negatively affect revenue and growth.

Market saturation and increasing competition may hinder future growth.

Slow subscriber growth and inability to increase advertising revenue may lead to profitability decline.

Lack of innovation and differentiation may cause Spotify to lose market share to competitors.

Failure to renew key licensing agreements.

Economic recession decreases consumer spending and affects revenue.

An adverse impact in changes to royalty rates. |

7. Risks

Spotify's improving profitability and strong revenue growth are counterbalanced by its relatively low gross margins, dependence on content providers (music labels), and increasingly competitive market. While recent financial performance is positive, historical losses and a significant debt burden introduce a level of risk. Future profitability hinges on maintaining subscriber growth, controlling content costs, and fending off competitors.

Red Flags:

None identified.

8. Conclusion

Spotify will continue to grow its user base and revenue, but margin expansion will be slower than expected due to ongoing content costs and competitive pressures.

The transition to podcasting will provide some diversification, but its impact on overall profitability will be moderate.

A steady growth trajectory with moderate margin improvements.

Anticipated growth rate for revenue is between 10% and 15% annually for the next 5 years.

Premium subscribers will grow at 7% annually.

Podcast monetization will improve gradually with targeted ads and wider distribution, with podcast revenue contributing approximately 15% of total revenue.

A modest margin improvement due to content cost management and some label deal improvements.

Gross margin targeted to reach 32% within 3 years, and operating margin to reach 10% within 5 years.

Moderate free cash flow supports ongoing investments and strategic initiatives.

Continued strategic investments in technology and content.

Maintaining its market position and user loyalty.

Improving user experience through new features and personalized content.

Stable growth in subscribers and engagement.

Cautious optimism towards future performance.

Consistent financial performance with steady growth.

Expected revenue increases and modest profitability.

Steady market adoption and stable growth.

Consistent management and execution.

Spotify can consistently generate revenue growth and modest profitability improvements.

Strategic investments can maintain its market share and competitiveness.

The company's focus on innovation will lead to continued improvements in its user experience.

Improved macroeconomic condition will boost consumer spending.

Subscriber base will be maintained and revenues increase, but margin expansion could be slower than expected.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

While a full Return on Invested Capital (ROIC) calculation requires more detailed data on invested capital, the available information allows for some estimations. The positive net income in 2024 suggests improving ROE, given the equity base. The trend suggests the company is becoming more efficient in generating profits from its equity, after losses in prior years.

While a full Return on Invested Capital (ROIC) calculation requires more detailed data on invested capital, the available information allows for some estimations. The positive net income in 2024 suggests improving ROE, given the equity base. The trend suggests the company is becoming more efficient in generating profits from its equity, after losses in prior years. The company exhibits strong Free Cash Flow (FCF) conversion, demonstrated by consistent positive FCF and a rise to EUR 2.284 billion in 2024. Capital expenditures (Capex) have remained relatively low and stable over the observed period, signaling that the company may not need large investments to maintain its current operations. These trends indicate that the company is generating strong cash from its operations and has sufficient funds for reinvestment or debt repayment.

The company exhibits strong Free Cash Flow (FCF) conversion, demonstrated by consistent positive FCF and a rise to EUR 2.284 billion in 2024. Capital expenditures (Capex) have remained relatively low and stable over the observed period, signaling that the company may not need large investments to maintain its current operations. These trends indicate that the company is generating strong cash from its operations and has sufficient funds for reinvestment or debt repayment.