Block, Inc. (SQ), currently trading at $83.46, operates a dual ecosystem comprising Square, a platform for sellers, and Cash App, a mobile payment service. S...

January 15, 2026

Vijar Kohli

Deep Dive: Block, Inc. (SQ)

Recommendation: BUY

Price Target: 95.45 (14.37 Upside)

Risk Level: Medium

1. Executive Summary

Block, Inc. (SQ), currently trading at $83.46, operates a dual ecosystem comprising Square, a platform for sellers, and Cash App, a mobile payment service. Square provides payment processing, software, and financial services to businesses of all sizes, enabling them to manage their operations and customer interactions. Cash App facilitates peer-to-peer payments, banking services, and investments for individuals. Block holds a significant market position in the digital payments space, particularly among small and medium-sized businesses (SMBs) and younger demographics. Its integrated hardware and software solutions for merchants differentiate it from competitors, while Cash App benefits from strong network effects and user adoption.

Growth catalysts for Block include continued expansion of both the Square and Cash App ecosystems. Square's growth is driven by expanding its product offerings (e.g., Square Loans, Square Banking), penetrating new vertical markets (e.g., restaurants, retail), and increasing international presence. Cash App's growth is fueled by increasing user engagement through new features like stock and Bitcoin trading, expanding its banking services, and attracting new users, especially those who are unbanked or underbanked. Furthermore, Block's investments in emerging technologies like blockchain and decentralized finance (DeFi) could unlock new growth opportunities in the future.

Key risks facing Block include intensifying competition from established players like PayPal and new entrants in the fintech space, regulatory scrutiny related to payment processing and cryptocurrency activities, and macroeconomic headwinds that could impact consumer spending and business investment. Specifically, increased interest rates can affect loan repayments and demand for Square's lending products. Moreover, fluctuations in cryptocurrency prices and regulatory changes in the crypto space can affect Cash App's Bitcoin trading business and its overall valuation. Execution risk related to integrating new acquisitions and developing innovative products also poses a challenge.

Valuation is a complex topic, but a general perspective can be given. While Block is not a value stock, due to its growth prospects, its valuation is supported by its strong revenue growth, gross profit margins, and potential for future profitability. However, concerns regarding its high operating expenses (especially related to marketing and product development), and dependence on transaction-based revenues can limit upside. A discounted cash flow (DCF) analysis, incorporating reasonable growth rates, profitability assumptions, and discount rates, is necessary to arrive at a precise valuation, considering both bullish and bearish scenarios.

Investment Thesis

Bull Case: Block's innovative ecosystem, combining Square's merchant solutions and Cash App's consumer finance platform, positions it for significant growth.

Increasing adoption of digital payments, expansion into new markets, and successful integration of Afterpay will drive revenue and profitability.

Block's focus on blockchain and decentralized technologies provides long-term upside potential.

The company's strong net cash position provides it with substantial flexibility to pursue strategic acquisitions and organic growth investments.

Block's recent focus on cost reduction and improved profitability should lead to strong earnings growth.

Square's robust seller ecosystem and Cash App's expanding user base create significant cross-selling opportunities.

Block's investments in new technologies such as blockchain and crypto could yield substantial returns over the long term.

Furthermore, the company's commitment to financial inclusion, by providing access to financial services for underserved populations, increases its market reach and societal impact, enhancing its long-term sustainability and appeal to socially responsible investors.

Finally, Block's proven ability to innovate and adapt to changing market conditions demonstrates its resilience and potential for sustained growth in the dynamic fintech landscape.

The company's shift toward prioritizing profitability and efficiency over pure growth is expected to lead to improved financial performance and higher investor confidence.

Bear Case: Increased competition from established players and new fintech startups will erode Block's market share.

Regulatory scrutiny and potential restrictions on cryptocurrency activities will negatively impact Block's growth.

Macroeconomic downturns will reduce consumer spending and business investment, hurting Block's transaction volumes.

The Afterpay acquisition fails to deliver expected synergies and becomes a drag on profitability.

Furthermore, a significant data breach or security lapse could damage Block's reputation and lead to customer attrition, undermining its long-term prospects.

The company's inability to innovate and adapt to changing market trends could result in stagnation and loss of competitive edge.

Block's high operating expenses and stock-based compensation could continue to weigh on profitability, hindering its ability to generate sustainable earnings.

Finally, increasing interest rates and inflationary pressures could negatively impact consumer spending and business investment, further exacerbating the challenges facing Block's growth and profitability.

Conviction: High

2. Business Overview

Block, Inc., together with its subsidiaries, creates tools that enables sellers to accept card payments and provides reporting and analytics, and next-day settlement. It provides hardware products, including Magstripe reader, which enables swiped transactions of magnetic stripe cards; Contactless and chip reader that accepts Europay, MasterCard, and Visa (EMV) chip cards and Near Field Communication payments; Square Stand, which enables an iPad to be used as a payment terminal or full point of sale solution; Square Register that combines its hardware, point-of-sale software, and payments technology; Square Terminal, a payments device and receipt printer to replace traditional keypad terminals, which accepts tap, dip, and swipe payments. The company also offers various software products, including Square Point of Sale; Square Appointments; Square for Retail; Square for Restaurants; Square Online and Square Online Checkout; Square Invoices; Square Virtual Terminal; Square Team Management; Square Contracts; Square Loyalty, Marketing, and Gift Cards; and Square Dashboard. In addition, it offers a developer platform, which includes application programming interfaces and software development kits. Further, the company provides Cash App, which enables to send, spend, and store money; and Weebly that offers customers website hosting and domain name registration solutions. It serves in the United States, Canada, Japan, Australia, Ireland, France, Spain, and the United Kingdom. The company was formerly known as Square, Inc. and changed its name to Block, Inc. in December 2021. Block, Inc. was incorporated in 2009 and is based in San Francisco, California.

Competitive Moat (Narrow)

Trend: Stable

Ecosystem Lock-in (high switching costs), Strong brand with small businesses, Cash App's user base for P2P payments

The sector is expected to exhibit strong growth driven by digital transformation, increasing cloud adoption, the proliferation of data, and rising cybersecurity threats. Growth rates may vary by specific segment but overall expansion is anticipated to continue for the foreseeable future.

Regulatory Environment:

N/A

4. Financial Analysis

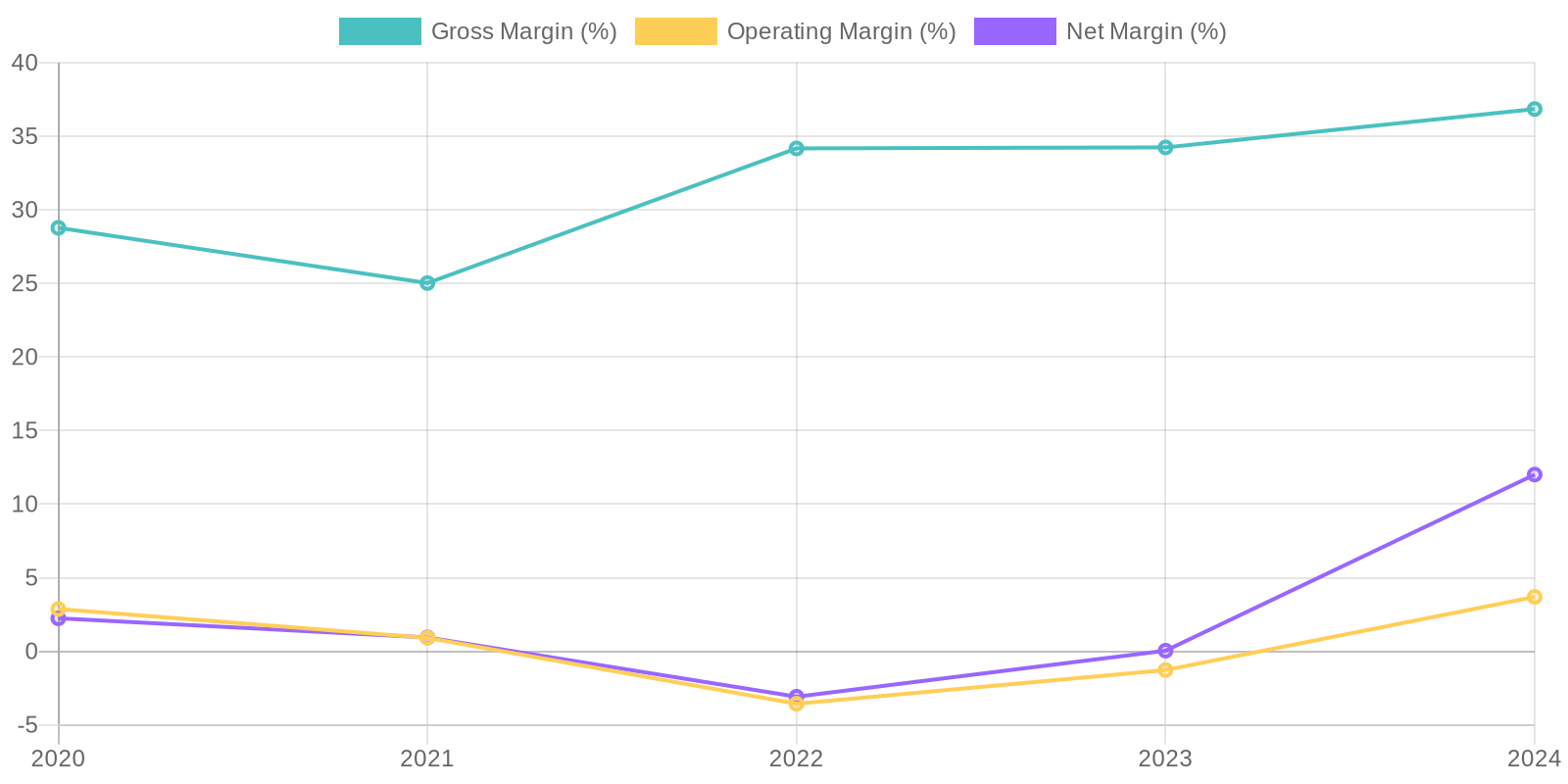

Margin Trend

Return on Invested Capital (ROIC) and Return on Equity (ROE) are crucial indicators of capital efficiency, but cannot be accurately derived from the information provided. To calculate ROIC, we require the invested capital figure, which is typically derived from the balance sheet by summing debt and equity, then subtracting non-operating assets. Similarly, ROE, which measures a company's profitability relative to shareholders' equity, cannot be precisely calculated without additional information on average equity and comprehensive income, warranting further investigation to fully ascertain the company's capital efficiency trends.

Revenue Quality

The company has demonstrated substantial revenue growth over the past five years, indicating a strong market position and effective sales strategies. The revenue increased from $9.5 billion in 2020 to $24.1 billion in 2024. Further analysis is needed to assess the percentage of recurring revenue versus transaction-based revenue to determine long-term sustainability, alongside examining customer concentration to ensure revenue streams are not overly reliant on a small number of clients, which can pose a risk if any of them discontinue their patronage.

Cash Flow & Capital Efficiency

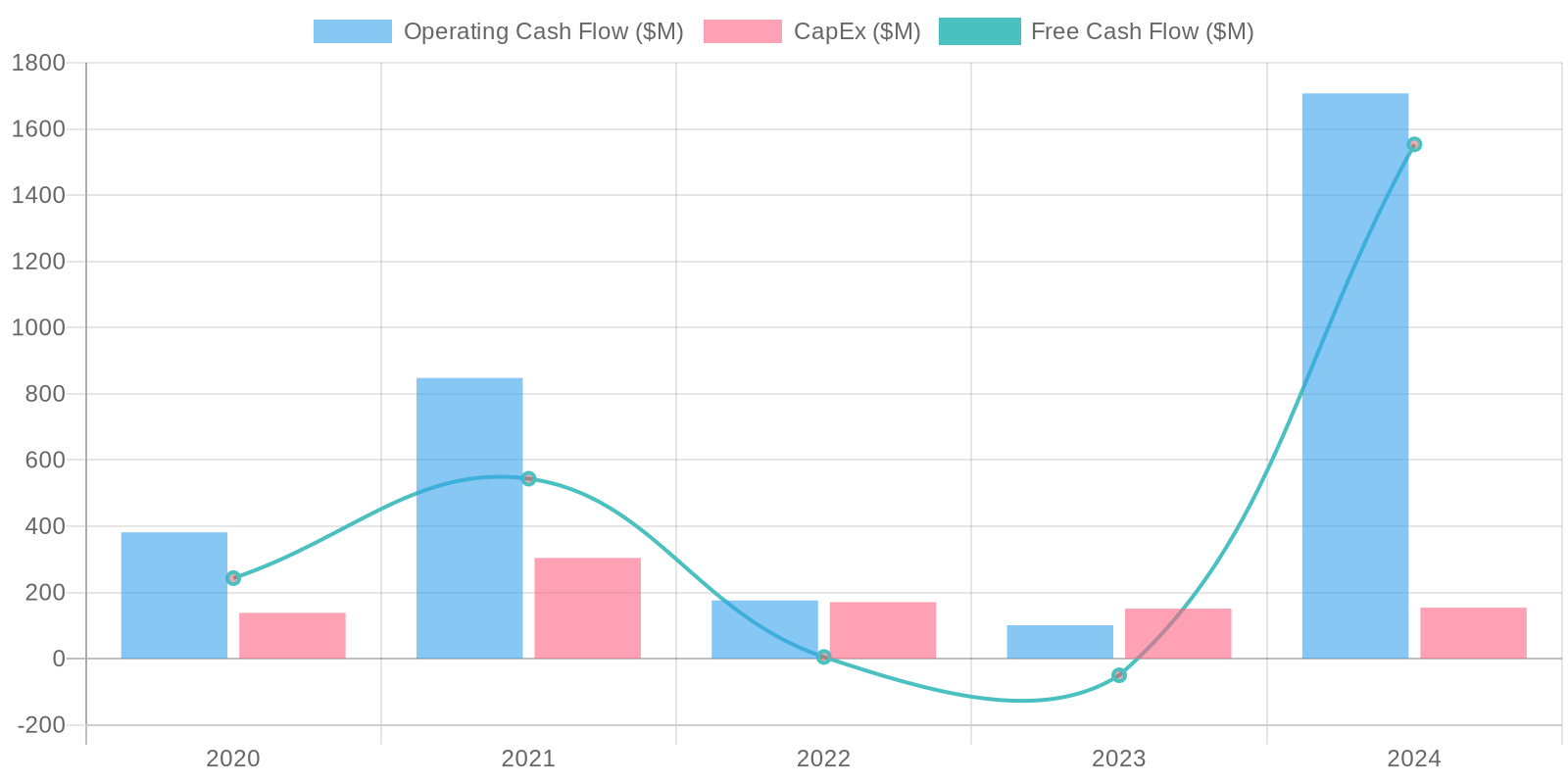

The company shows a strong Free Cash Flow (FCF) generation in 2024, with $1.55 billion reported, a significant increase from previous years. A concerning FCF of negative $50 million was generated in 2023. Capital expenditure remains relatively stable, between $134 million and $171 million. The cash flow from operations is consistently positive, but it is significantly affected by changes in working capital and other non-cash items.

Capital Efficiency (ROIC/ROE):

Return on Invested Capital (ROIC) and Return on Equity (ROE) are crucial indicators of capital efficiency, but cannot be accurately derived from the information provided. To calculate ROIC, we require the invested capital figure, which is typically derived from the balance sheet by summing debt and equity, then subtracting non-operating assets. Similarly, ROE, which measures a company's profitability relative to shareholders' equity, cannot be precisely calculated without additional information on average equity and comprehensive income, warranting further investigation to fully ascertain the company's capital efficiency trends.

Balance Sheet Health:

The company holds a substantial cash reserve of $12.3 billion in 2024, providing a strong liquidity cushion. Total debt stands at $7.9 billion, with a net debt position of negative $4.3 billion, indicating that the company's cash exceeds its debt obligations. The increase in goodwill and intangible assets over the years should be monitored for potential impairment issues.

5. Management & Governance

CEO Assessment: Jack Dorsey, as CEO, has a strong track record of innovation at Block, but his dual role as CEO of Twitter (now X) has raised concerns about focus. Recent emphasis on Bitcoin and blockchain initiatives demonstrates a clear vision, though execution and market reception remain key performance indicators.

Capital Allocation: Good

Insider Ownership: Insider ownership is significant, with Jack Dorsey holding a substantial stake. This generally aligns management's interests with shareholders, but also concentrates voting power.

Governance Flags:

CEO duality (until Dorsey stepped down from Twitter), Concentrated voting power due to insider ownership

The DCF model indicates a fair value of $95.45 based on the projected free cash flows. A discount rate of 11% reflects the risk associated with the company's future earnings, while the declining growth rate is applied based on the historical revenue growth trends. Improvements in operating margin are expected as the company achieves scale. The terminal growth rate represents the expected sustainable long-term growth rate of the company beyond the projection period. The current market price of $83.46 suggests that Block is undervalued. The target price is $95.45.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Block's innovative ecosystem, combining Square's merchant solutions and Cash App's consumer finance platform, positions it for significant growth.

Increasing adoption of digital payments, expansion into new markets, and successful integration of Afterpay will drive revenue and profitability.

Block's focus on blockchain and decentralized technologies provides long-term upside potential.

The company's strong net cash position provides it with substantial flexibility to pursue strategic acquisitions and organic growth investments.

Block's recent focus on cost reduction and improved profitability should lead to strong earnings growth.

Square's robust seller ecosystem and Cash App's expanding user base create significant cross-selling opportunities.

Block's investments in new technologies such as blockchain and crypto could yield substantial returns over the long term.

Furthermore, the company's commitment to financial inclusion, by providing access to financial services for underserved populations, increases its market reach and societal impact, enhancing its long-term sustainability and appeal to socially responsible investors.

Finally, Block's proven ability to innovate and adapt to changing market conditions demonstrates its resilience and potential for sustained growth in the dynamic fintech landscape.

The company's shift toward prioritizing profitability and efficiency over pure growth is expected to lead to improved financial performance and higher investor confidence. |

| Base | 95.45 | Block will continue to grow its core businesses of Square and Cash App, albeit at a more moderate pace than in the past.

Increased competition in the payments and consumer finance space, along with macroeconomic headwinds, will limit growth.

Block's profitability will improve as it realizes synergies from past acquisitions and focuses on cost management.

The Afterpay integration will be moderately successful.

Furthermore, the company's ability to navigate regulatory challenges and maintain a competitive edge in the rapidly evolving fintech landscape will be crucial for sustaining long-term growth and profitability.

Block's reliance on transaction-based revenue makes it vulnerable to economic downturns and fluctuations in consumer spending, which could impact its financial performance.

The company's investments in new technologies, such as blockchain and crypto, carry inherent risks and uncertainties, and their success cannot be guaranteed.

Furthermore, maintaining customer trust and data security is paramount for Block's reputation and long-term viability, as any breaches or negative incidents could erode user confidence and damage the brand.

Finally, the company's exposure to regulatory changes and compliance requirements in the financial services industry adds complexity and costs to its operations, requiring ongoing vigilance and adaptation. |

| Bear | Low | Increased competition from established players and new fintech startups will erode Block's market share.

Regulatory scrutiny and potential restrictions on cryptocurrency activities will negatively impact Block's growth.

Macroeconomic downturns will reduce consumer spending and business investment, hurting Block's transaction volumes.

The Afterpay acquisition fails to deliver expected synergies and becomes a drag on profitability.

Furthermore, a significant data breach or security lapse could damage Block's reputation and lead to customer attrition, undermining its long-term prospects.

The company's inability to innovate and adapt to changing market trends could result in stagnation and loss of competitive edge.

Block's high operating expenses and stock-based compensation could continue to weigh on profitability, hindering its ability to generate sustainable earnings.

Finally, increasing interest rates and inflationary pressures could negatively impact consumer spending and business investment, further exacerbating the challenges facing Block's growth and profitability. |

7. Risks

Block, Inc. exhibits a mixed risk profile. While it has a strong revenue base and substantial cash holdings, inconsistent profitability, significant debt, and a large proportion of intangible assets raise concerns. Regulatory risks and competition further contribute to the overall risk level.

Red Flags:

None identified.

8. Conclusion

Block will continue to grow its core businesses of Square and Cash App, albeit at a more moderate pace than in the past.

Increased competition in the payments and consumer finance space, along with macroeconomic headwinds, will limit growth.

Block's profitability will improve as it realizes synergies from past acquisitions and focuses on cost management.

The Afterpay integration will be moderately successful.

Furthermore, the company's ability to navigate regulatory challenges and maintain a competitive edge in the rapidly evolving fintech landscape will be crucial for sustaining long-term growth and profitability.

Block's reliance on transaction-based revenue makes it vulnerable to economic downturns and fluctuations in consumer spending, which could impact its financial performance.

The company's investments in new technologies, such as blockchain and crypto, carry inherent risks and uncertainties, and their success cannot be guaranteed.

Furthermore, maintaining customer trust and data security is paramount for Block's reputation and long-term viability, as any breaches or negative incidents could erode user confidence and damage the brand.

Finally, the company's exposure to regulatory changes and compliance requirements in the financial services industry adds complexity and costs to its operations, requiring ongoing vigilance and adaptation.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Return on Invested Capital (ROIC) and Return on Equity (ROE) are crucial indicators of capital efficiency, but cannot be accurately derived from the information provided. To calculate ROIC, we require the invested capital figure, which is typically derived from the balance sheet by summing debt and equity, then subtracting non-operating assets. Similarly, ROE, which measures a company's profitability relative to shareholders' equity, cannot be precisely calculated without additional information on average equity and comprehensive income, warranting further investigation to fully ascertain the company's capital efficiency trends.

Return on Invested Capital (ROIC) and Return on Equity (ROE) are crucial indicators of capital efficiency, but cannot be accurately derived from the information provided. To calculate ROIC, we require the invested capital figure, which is typically derived from the balance sheet by summing debt and equity, then subtracting non-operating assets. Similarly, ROE, which measures a company's profitability relative to shareholders' equity, cannot be precisely calculated without additional information on average equity and comprehensive income, warranting further investigation to fully ascertain the company's capital efficiency trends. The company shows a strong Free Cash Flow (FCF) generation in 2024, with $1.55 billion reported, a significant increase from previous years. A concerning FCF of negative $50 million was generated in 2023. Capital expenditure remains relatively stable, between $134 million and $171 million. The cash flow from operations is consistently positive, but it is significantly affected by changes in working capital and other non-cash items.

The company shows a strong Free Cash Flow (FCF) generation in 2024, with $1.55 billion reported, a significant increase from previous years. A concerning FCF of negative $50 million was generated in 2023. Capital expenditure remains relatively stable, between $134 million and $171 million. The cash flow from operations is consistently positive, but it is significantly affected by changes in working capital and other non-cash items.