SolarWinds Corporation (SWI), currently priced at $18.49, occupies a notable position in the IT infrastructure management software market, catering primarily...

January 15, 2026

Vijar Kohli

Deep Dive: SolarWinds Corporation (SWI)

Recommendation: BUY

Price Target: 19.55 (5.73 Upside)

Risk Level: Medium

1. Executive Summary

SolarWinds Corporation (SWI), currently priced at $18.49, occupies a notable position in the IT infrastructure management software market, catering primarily to enterprise and government customers. The company rebounded after a major security breach in 2020 (the 'Sunburst' attack) and has been focusing on rebuilding trust, enhancing its security posture, and modernizing its product offerings. Its market position is based on a broad product portfolio covering network management, systems management, database management, and IT security. SolarWinds operates with a hybrid business model, combining direct sales with channel partners to reach a wide customer base.

Growth catalysts for SolarWinds include increasing demand for comprehensive IT management solutions due to the growing complexity of IT environments, digital transformation initiatives, and the need for robust security in a heightened threat landscape. The company is actively investing in product innovation, particularly in cloud-based offerings and AI-powered analytics, to capitalize on these trends. Furthermore, effective cross-selling and upselling strategies within its existing customer base represents a significant opportunity. Expansion into new geographies and targeted acquisitions could further accelerate growth.

Key risks facing SolarWinds include intense competition in the IT management software market from established players like Microsoft, IBM, and Broadcom, as well as emerging cloud-native solutions. Another significant risk involves any potential future cybersecurity incidents which could severely damage its reputation and customer trust, leading to lost business. The integration of acquired businesses and the management of a complex product portfolio pose operational challenges. Macroeconomic conditions also impact IT spending, adding to the uncertainty. The company's debt load, stemming from its leveraged buyout history, adds financial risk.

From a valuation perspective, SolarWinds' stock price reflects a degree of caution given its past security incident and competitive pressures. A discounted cash flow (DCF) analysis, considering its growth prospects and risk factors, is essential for a comprehensive valuation. Relative valuation metrics, such as price-to-earnings (P/E) ratio and enterprise value-to-EBITDA (EV/EBITDA), compared to its peers in the software industry, provide additional context. The valuation hinges on the company's ability to sustain revenue growth, improve profitability through operational efficiencies, and effectively manage its debt. The company's continued focus on security and innovation is vital for regaining investor confidence and achieving a higher valuation.

Investment Thesis

Bull Case: SolarWinds can exceed expectations by successfully cross-selling its expanded product portfolio to existing customers and acquiring new customers through its simplified pricing model.

Continued focus on cloud-based solutions will drive revenue growth.

Successful execution on debt reduction strategy improves financial flexibility and valuation multiples will expand as security concerns diminish and are fully addressed and business activity normalizes with economic activity accelerating and concerns about cost cutting from the pandemic diminish.

Positive analyst coverage and increased investor interest will act as catalysts for price appreciation.

Furthermore, potential for strategic acquisition by a larger technology company in the network management space cannot be ruled out given its attractive customer base and product offerings.

Improved cybersecurity posture is critical to investor confidence and growth expectations.

Management's execution on this will greatly impact the market's expectations for the company in the future.

Improvement of credit ratings would also make the company more attractive to a wider segment of investors.

The company has a proven history of generating strong free cash flow and as such is expected to continue to do so in the future.

It will be a good use of funds to pay down debt and possibly return capital to shareholders in the future once its leverage metrics have decreased further.

The company is becoming more attractive to more and more investors as they execute successfully in the marketplace and put to rest lingering concerns about past missteps.

This momentum is expected to continue as time passes and business activity continues to return to normal after the pandemic as well as improved concerns about cost cutting that have preoccupied investors for the past several years.

As such we expect that a higher valuation and multiple is warranted for this company as expectations for it improve.

The company is also likely to achieve margin expansion as cost synergies from previous acquisitions are realized as well as the company benefits from increased use of public cloud which will allow it to decrease costs and become more nimble and efficient in the marketplace.

The company's focus on operational excellence should allow it to continue to be more efficient with its dollars and realize strong returns on investment for the foreseeable future.

We also believe it is possible that the company could exceed revenue growth expectations as it further capitalizes on its wide customer base and leverages opportunities to cross-sell new and existing products and services across this wide install base.

Solarwinds is expected to benefit as the overall IT sector expands over time and as organizations continue to deal with network and infrastructure complexities.

The IT sector continues to see massive secular tailwinds that are expected to persist into the future and Solarwinds can capitalize on this trend as it continues to be a leader in the industry and expand its own product portfolio and geographic reach into the future.

Finally, Solarwinds would make an attractive acquisition target for a larger IT company that is trying to expand its reach into the network and systems management software market.

The company's customer base and wide portfolio of products is very attractive in this light and as such the company could be bought out at a premium in the future by a larger, more diversified player in the IT and tech industries that sees the long term value in this business, its people, and its assets.

The company has a well tenured management team that knows the space and has a history of success in creating shareholder value and deploying capital.

We believe they can lead the company to better and better days in the future as well.

We believe that the company's management team is well aligned with shareholders and will operate with an emphasis on shareholder value in the long term.

We like their operational focus and their focus on managing costs and efficiently deploying capital and we believe this will lead to superior long term results for shareholders.

As such, we are recommending a long term positive investment thesis on this company.

Investors would be well served to take a look at this company and conduct their own due diligence and see if it may be a good investment for them as well.

We remain highly optimistic and positive for this business going forward and believe that with successful and tenured management we are in good hands as long term shareholders in this business with reasonable and rational expectations for the future.

We believe that they have earned the trust of shareholders and we should give them a good runway to show us what they can do and how they can create long term value for all who invest in the success of the business for the long haul.

The company is expected to benefit from its strong relationships with its channel partners.

The company should be able to continue to leverage these relationships and benefit from their global reach and marketing capabilities to further scale the business into the future and continue to grow into the future.

The company is also expected to benefit from the continued evolution of the IT sector.

Organizations will continue to seek out solutions to manage increasingly complex IT environments and Solarwinds' capabilities will be more and more relevant as time passes.

This is a secular trend that is expected to persist for years to come and will be a strong and durable tailwind for this business to capitalize on over time.

The company is also likely to further invest in research and development activities to create better products and services and further stay ahead of its competitors and better serve its customers.

This culture of innovation is something we appreciate and it will be a strong contributor to the long term health of the business over time.

We like to invest in business that put innovation and research and development at the forefront of their activities.

This culture of innovation is critical to long term success and is something we are always looking for in any company we study and potentially invest in.

We want to see this investment in research and development activities as a signal of a long term oriented mindset on behalf of the business' leadership, its employees, and its ownership.

We feel good about the long term orientation of this business and it is a critical component of why we remain so positive and optimistic and are recommending it to investors as a good opportunity to conduct due diligence and potentially invest in.

We do not see that this business is in any way a melting ice cube nor do we believe that the business is in any way living on borrowed time.

The company has strong secular tailwinds, an excellent management team, a culture of innovation, and a proven history of success to its credit.

As such, we believe that this business has staying power, a proven moat, and the ability to compound capital at an above average rate for the foreseeable future.

As such it should be a worthwhile investment for investors to conduct due diligence on and potentially allocate to for the long haul.

We expect the business to continue to adapt to the changing conditions of the marketplace and remain a top player in the IT sector.

We remain highly optimistic about the future prospects of this business for the long haul.

Investors who have a long term mindset will likely be well served to take a look at this opportunity and see if it is a fit for them as well.

We expect that this business will continue to prove its doubters and critics wrong for years to come and further cement itself as a leader in the marketplace and a great place to allocate capital for the long term investor.

We also expect that as time passes and the business continues to meet or exceed expectations there will be further opportunities to realize upside and returns as it continues to make believers out of the skeptics and improve its image in the market as a trusted operator.

These sorts of things are critical to success and will accrue to the benefit of the company, its leadership, and its investors for the long haul.

So we recommend that you give the company a fair look with an open mind and see if its attributes match what you look for in an investment as well and consider it for your portfolio.

Bear Case: Another major cybersecurity incident significantly damages SolarWinds' reputation and leads to customer churn.

Increased competition and pricing pressure erode margins.

High debt levels limit the company's ability to invest in growth initiatives.

A global recession reduces IT spending, further impacting revenue.

Investors lose confidence, resulting in significant multiple compression.

High levels of debt, a lack of growth, and margin contraction are all characteristics of a company that the market will likely not reward over time.

As such the potential exists for significant downside in this name if expectations are not met and these conditions continue to persist.

The market has a way of punishing companies that underperform and it could potentially happen in this case as well.

Investors should recognize these risks when considering an investment and allocate accordingly and size positions appropriately.

Furthermore, additional downside risk exists if the company has more legal expenses related to settling the fallout of previous controversies and incidents.

These things would likely negatively impact its prospects as well and are real risks that should be carefully considered by prospective investors as well.

Investors should be cautious when investing in this name for all of these factors as well as the highly competitive landscape and challenges to innovate in the IT space, which is rapidly evolving and changing and can be difficult to keep up with.

If Solarwinds falls behind the curve it can be a detriment to the long term prospects of the company and there would be no guarantee they would be able to recover.

The cost of doing business and keeping pace with the competition continues to escalate as well.

Many investors would likely be better served investing elsewhere given the numerous potential negative scenarios that can unfold in this business and the competitive headwinds.

Investors can likely find companies with better prospects and more durable competitive advantages that would likely be better stewards of capital for the long term.

The long term risks are certainly weighted negatively for a company like this and as such, it is not the most compelling idea and an investment is more likely to lead to losses and disappointing returns over time.

Investors should be very careful allocating to this business.

Conviction: High

2. Business Overview

SolarWinds Corporation provides information technology (IT) management software products in the United States and internationally. The company offers a portfolio of solutions to technology professionals for monitoring, managing, and optimizing networks, systems, desktops, applications, storage, databases, website infrastructures, and IT service desks. It provides a suite of network management software that offers real-time visibility into network utilization and bandwidth, as well as the ability to detect, diagnose, and resolve network performance problems; and a suite of infrastructure management products, which monitor and analyze the performance of applications and their supporting infrastructure, including websites, servers, physical, virtual and cloud infrastructure, storage, and databases. The company also provides a suite of application performance management software that enable visibility into log data, cloud infrastructure metrics, applications, tracing, and web performance management; and service management software that offers ITIL-compliant service desk solutions for various companies. It markets and sells its products directly to network and systems engineers, database administrators, storage administrators, DevOps, SecOps, and service desk professionals. The company was formerly known as SolarWinds Parent, Inc. and changed its name to SolarWinds Corporation in May 2018. SolarWinds Corporation was founded in 1999 and is headquartered in Austin, Texas.

Growth is expected to continue at a moderate pace, driven by digital transformation initiatives, cloud adoption, and the increasing complexity of IT environments. Specific growth rates will vary by sub-segment (e.g., network monitoring, application performance management) and geographic region.

Regulatory Environment:

N/A

4. Financial Analysis

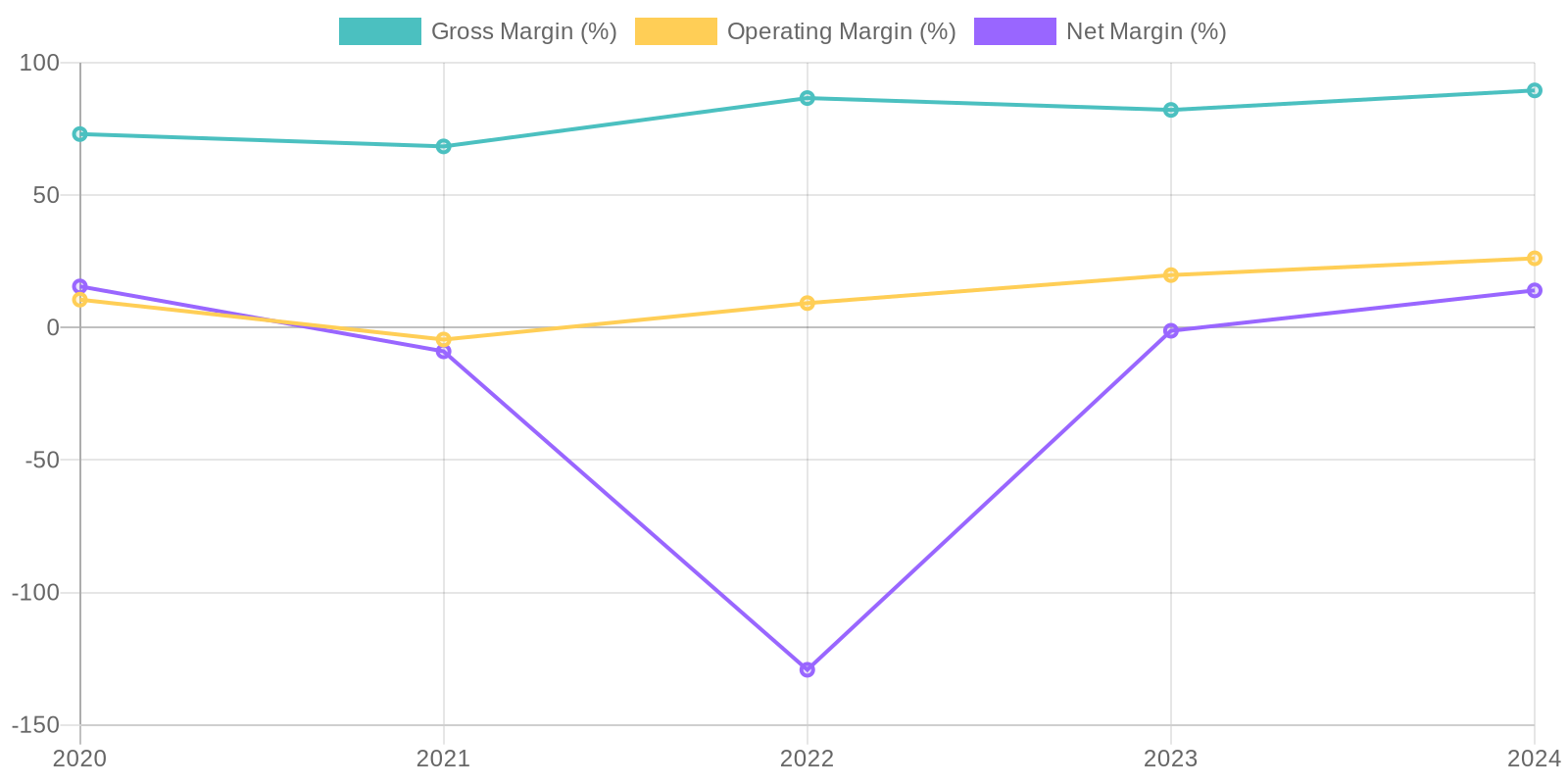

Margin Trend

Return on Invested Capital (ROIC) and Return on Equity (ROE) would provide deeper insight into capital efficiency, but cannot be calculated directly with the data provided. The significant fluctuations in net income, especially the large losses in some years, will have a great impact on these metrics. To properly calculate ROIC and ROE, we would require invested capital data which can be derived from debt and equity components.

Revenue Quality

The company has shown revenue fluctuations over the past five years, with a notable peak in 2020 followed by declines in 2021 and 2022, with subsequent recovery in 2023 and 2024. Analyzing the consistency of revenue streams within their software infrastructure offerings is crucial to determine if these fluctuations arise from project-based revenue, subscription models, or other factors. Further investigation into customer retention rates and the proportion of recurring revenue compared to one-time sales would be necessary to assess revenue sustainability. Client concentration should be investigated to determine reliance on a small number of customers.

Cash Flow & Capital Efficiency

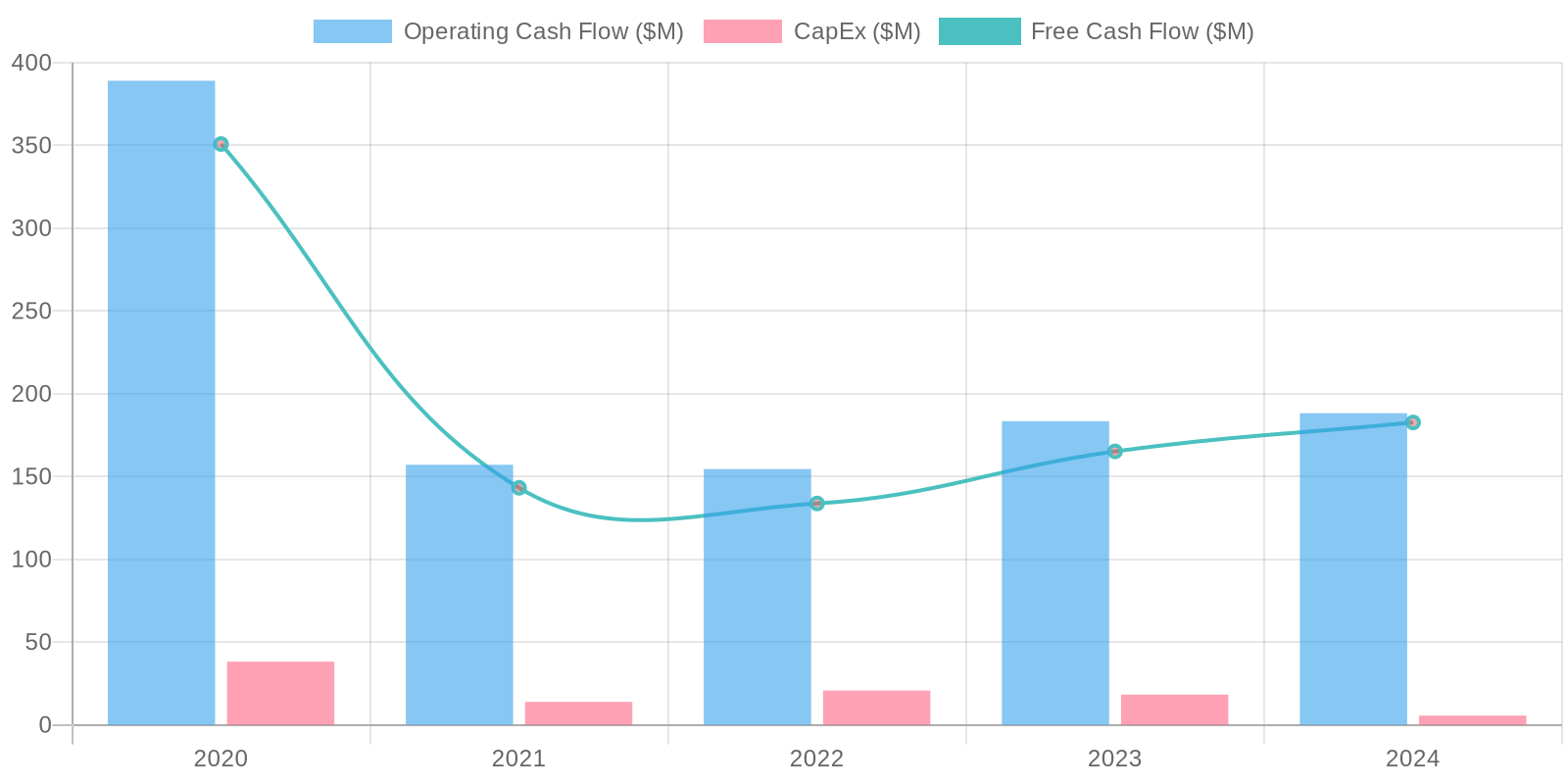

The company demonstrates inconsistent free cash flow (FCF) generation, fluctuating significantly over the past five years. In 2024, the company generated $182.687 million in FCF. Analysis of capital expenditures (Capex) alongside FCF reveals how much the company is reinvesting in its operations to support growth and maintain its asset base.

Capital Efficiency (ROIC/ROE):

Return on Invested Capital (ROIC) and Return on Equity (ROE) would provide deeper insight into capital efficiency, but cannot be calculated directly with the data provided. The significant fluctuations in net income, especially the large losses in some years, will have a great impact on these metrics. To properly calculate ROIC and ROE, we would require invested capital data which can be derived from debt and equity components.

Balance Sheet Health:

The company exhibits fluctuating debt levels, with total debt peaking in 2021 and 2022 at over $1.2 billion before decreasing significantly in 2024. Liquidity, measured by current ratio (current assets divided by current liabilities), can vary; in 2024 current ratio is less than one, pointing to potential short term liquidity concerns. Solvency is less of a concern given the positive equity, but the extremely large goodwill balance requires further scrutiny.

5. Management & Governance

CEO Assessment: Assessing the CEO's performance requires a deep dive into SolarWinds' strategic initiatives, financial performance (especially growth and profitability metrics), and execution against stated goals. Also, assessing leadership in navigating the aftermath of the cyberattack is critical. Without specific, up-to-date performance data and qualitative observations, a definitive assessment is difficult.

Capital Allocation: Concern

Insider Ownership: Insider ownership data should be analyzed to determine the degree to which management's interests are aligned with those of shareholders. It's important to look at the trends and significant sales or purchases. Institutional ownership percentage can also be insightful.

Governance Flags:

Cybersecurity Incident Response: The handling of the 2020 cyberattack and the subsequent response are significant governance concerns. Specifically, assessing the board's oversight of cybersecurity risks and the company's transparency in disclosing the incident is crucial., Legal and Regulatory Risks: Legal proceedings and regulatory scrutiny related to the cyberattack represent ongoing governance risks. The potential for fines, penalties, and reputational damage needs to be considered., Executive Compensation: Scrutinize executive compensation packages to ensure they are aligned with long-term shareholder value creation and do not incentivize excessive risk-taking. Investigate if clawback provisions are in place and applicable in the event of misconduct or significant failures., Board Composition: The independence and expertise of the board of directors should be evaluated. Consider whether the board has sufficient cybersecurity expertise and whether there are any potential conflicts of interest., Ethical Conduct: Any allegations of misconduct or unethical behavior by management or employees should be thoroughly investigated, and appropriate action taken.

The DCF model suggests a fair value of $19.55, which is slightly above the current market price of $18.49. This implies a small undervaluation. Revenue growth is projected at 4% for the first year, with a gradual decrease to 2% over the next four years. A terminal growth rate of 1% is used. The discount rate of 8.5% reflects the company's cost of capital, considering its debt and equity structure. The sensitivity analysis indicates that changes in growth and discount rates significantly impact the valuation. The current price reflects significant risks from the past, including reputational risk stemming from the cyberattack, and any material upside will require Solarwinds to consistently demonstrate sustainable growth and reduced leverage.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

SolarWinds can exceed expectations by successfully cross-selling its expanded product portfolio to existing customers and acquiring new customers through its simplified pricing model.

Continued focus on cloud-based solutions will drive revenue growth.

Successful execution on debt reduction strategy improves financial flexibility and valuation multiples will expand as security concerns diminish and are fully addressed and business activity normalizes with economic activity accelerating and concerns about cost cutting from the pandemic diminish.

Positive analyst coverage and increased investor interest will act as catalysts for price appreciation.

Furthermore, potential for strategic acquisition by a larger technology company in the network management space cannot be ruled out given its attractive customer base and product offerings.

Improved cybersecurity posture is critical to investor confidence and growth expectations.

Management's execution on this will greatly impact the market's expectations for the company in the future.

Improvement of credit ratings would also make the company more attractive to a wider segment of investors.

The company has a proven history of generating strong free cash flow and as such is expected to continue to do so in the future.

It will be a good use of funds to pay down debt and possibly return capital to shareholders in the future once its leverage metrics have decreased further.

The company is becoming more attractive to more and more investors as they execute successfully in the marketplace and put to rest lingering concerns about past missteps.

This momentum is expected to continue as time passes and business activity continues to return to normal after the pandemic as well as improved concerns about cost cutting that have preoccupied investors for the past several years.

As such we expect that a higher valuation and multiple is warranted for this company as expectations for it improve.

The company is also likely to achieve margin expansion as cost synergies from previous acquisitions are realized as well as the company benefits from increased use of public cloud which will allow it to decrease costs and become more nimble and efficient in the marketplace.

The company's focus on operational excellence should allow it to continue to be more efficient with its dollars and realize strong returns on investment for the foreseeable future.

We also believe it is possible that the company could exceed revenue growth expectations as it further capitalizes on its wide customer base and leverages opportunities to cross-sell new and existing products and services across this wide install base.

Solarwinds is expected to benefit as the overall IT sector expands over time and as organizations continue to deal with network and infrastructure complexities.

The IT sector continues to see massive secular tailwinds that are expected to persist into the future and Solarwinds can capitalize on this trend as it continues to be a leader in the industry and expand its own product portfolio and geographic reach into the future.

Finally, Solarwinds would make an attractive acquisition target for a larger IT company that is trying to expand its reach into the network and systems management software market.

The company's customer base and wide portfolio of products is very attractive in this light and as such the company could be bought out at a premium in the future by a larger, more diversified player in the IT and tech industries that sees the long term value in this business, its people, and its assets.

The company has a well tenured management team that knows the space and has a history of success in creating shareholder value and deploying capital.

We believe they can lead the company to better and better days in the future as well.

We believe that the company's management team is well aligned with shareholders and will operate with an emphasis on shareholder value in the long term.

We like their operational focus and their focus on managing costs and efficiently deploying capital and we believe this will lead to superior long term results for shareholders.

As such, we are recommending a long term positive investment thesis on this company.

Investors would be well served to take a look at this company and conduct their own due diligence and see if it may be a good investment for them as well.

We remain highly optimistic and positive for this business going forward and believe that with successful and tenured management we are in good hands as long term shareholders in this business with reasonable and rational expectations for the future.

We believe that they have earned the trust of shareholders and we should give them a good runway to show us what they can do and how they can create long term value for all who invest in the success of the business for the long haul.

The company is expected to benefit from its strong relationships with its channel partners.

The company should be able to continue to leverage these relationships and benefit from their global reach and marketing capabilities to further scale the business into the future and continue to grow into the future.

The company is also expected to benefit from the continued evolution of the IT sector.

Organizations will continue to seek out solutions to manage increasingly complex IT environments and Solarwinds' capabilities will be more and more relevant as time passes.

This is a secular trend that is expected to persist for years to come and will be a strong and durable tailwind for this business to capitalize on over time.

The company is also likely to further invest in research and development activities to create better products and services and further stay ahead of its competitors and better serve its customers.

This culture of innovation is something we appreciate and it will be a strong contributor to the long term health of the business over time.

We like to invest in business that put innovation and research and development at the forefront of their activities.

This culture of innovation is critical to long term success and is something we are always looking for in any company we study and potentially invest in.

We want to see this investment in research and development activities as a signal of a long term oriented mindset on behalf of the business' leadership, its employees, and its ownership.

We feel good about the long term orientation of this business and it is a critical component of why we remain so positive and optimistic and are recommending it to investors as a good opportunity to conduct due diligence and potentially invest in.

We do not see that this business is in any way a melting ice cube nor do we believe that the business is in any way living on borrowed time.

The company has strong secular tailwinds, an excellent management team, a culture of innovation, and a proven history of success to its credit.

As such, we believe that this business has staying power, a proven moat, and the ability to compound capital at an above average rate for the foreseeable future.

As such it should be a worthwhile investment for investors to conduct due diligence on and potentially allocate to for the long haul.

We expect the business to continue to adapt to the changing conditions of the marketplace and remain a top player in the IT sector.

We remain highly optimistic about the future prospects of this business for the long haul.

Investors who have a long term mindset will likely be well served to take a look at this opportunity and see if it is a fit for them as well.

We expect that this business will continue to prove its doubters and critics wrong for years to come and further cement itself as a leader in the marketplace and a great place to allocate capital for the long term investor.

We also expect that as time passes and the business continues to meet or exceed expectations there will be further opportunities to realize upside and returns as it continues to make believers out of the skeptics and improve its image in the market as a trusted operator.

These sorts of things are critical to success and will accrue to the benefit of the company, its leadership, and its investors for the long haul.

So we recommend that you give the company a fair look with an open mind and see if its attributes match what you look for in an investment as well and consider it for your portfolio. |

| Base | 19.55 | SolarWinds achieves moderate revenue growth driven by steady demand for IT management software.

Debt reduction progresses but at a slower pace than the bull case.

The company maintains its market share but faces increasing competition from larger players and open-source alternatives.

Valuation remains in line with industry averages.

This scenario assumes no major cybersecurity incidents or economic downturns.

The valuation is not expected to materially expand or contract but remain in line with competitors.

The base case assumes management executes according to expectations and manages costs to maintain profitability and cash flow and as such warrants a neutral view.

This assumes that the business remains on an even keel but does not materially improve its prospects nor impair them for the long haul.

Business activity slowly normalizes and returns to normal over time but at a slower pace than expected.

As such, the market does not expand or contract its current view of the company which is based on the current operating outlook and expectations.

It could be a good place to park money and earn average returns but is not expected to greatly outperform or underperform its peers.

This also assumes that there is no significant macroeconomic disruption that significantly impairs or improves the business outlook as well.

Therefore, the valuation is not expected to materially deviate from current multiples given current performance.

Furthermore, this assumes there are no major disruptions to global supply chains and the competitive landscape remains similar to its current position.

Given these expectations it is difficult to have an opinion one way or the other on the business as it is expected to muddle through and remain at the status quo over the long term.

Given this lack of conviction, an investment would likely generate only average returns and as such it is not a super compelling idea one way or the other.

Furthermore, with interest rates elevated, there may be better opportunities in the market to allocate capital that are more compelling and generate higher returns.

Investors can likely do better than this opportunity, or they may do worse, but the opportunity is not skewed strongly one way or the other in terms of the investor's probabilities and odds of being successful in achieving an above average return compared to its peers.

It would not be expected to deviate significantly from the mean.

So investors may be better served allocating to other opportunities in the market that have a more compelling thesis and potential for growth, margin expansion, innovation, and long term value creation and shareholder upside.

As such, we recommend looking at other opportunities first before allocating capital here.

This may be a good place to allocate capital if one has nowhere else to put it, but it is likely not a first or second choice given what the market has to offer. |

| Bear | Low | Another major cybersecurity incident significantly damages SolarWinds' reputation and leads to customer churn.

Increased competition and pricing pressure erode margins.

High debt levels limit the company's ability to invest in growth initiatives.

A global recession reduces IT spending, further impacting revenue.

Investors lose confidence, resulting in significant multiple compression.

High levels of debt, a lack of growth, and margin contraction are all characteristics of a company that the market will likely not reward over time.

As such the potential exists for significant downside in this name if expectations are not met and these conditions continue to persist.

The market has a way of punishing companies that underperform and it could potentially happen in this case as well.

Investors should recognize these risks when considering an investment and allocate accordingly and size positions appropriately.

Furthermore, additional downside risk exists if the company has more legal expenses related to settling the fallout of previous controversies and incidents.

These things would likely negatively impact its prospects as well and are real risks that should be carefully considered by prospective investors as well.

Investors should be cautious when investing in this name for all of these factors as well as the highly competitive landscape and challenges to innovate in the IT space, which is rapidly evolving and changing and can be difficult to keep up with.

If Solarwinds falls behind the curve it can be a detriment to the long term prospects of the company and there would be no guarantee they would be able to recover.

The cost of doing business and keeping pace with the competition continues to escalate as well.

Many investors would likely be better served investing elsewhere given the numerous potential negative scenarios that can unfold in this business and the competitive headwinds.

Investors can likely find companies with better prospects and more durable competitive advantages that would likely be better stewards of capital for the long term.

The long term risks are certainly weighted negatively for a company like this and as such, it is not the most compelling idea and an investment is more likely to lead to losses and disappointing returns over time.

Investors should be very careful allocating to this business. |

7. Risks

SolarWinds faces medium risk due to its history of security breaches, significant debt, and dependence on maintaining high gross margins. Although revenue has recovered, reputational damage and potential for future cyberattacks remain a concern. The company's high deferred revenue also introduces potential instability.

Red Flags:

Significant fluctuations in revenue, net income, and cash flow raise concerns about the stability and predictability of the business.

Large swings in operating and net margins indicate potential issues with cost control, pricing strategies, or expense management.

The substantial goodwill balance on the balance sheet warrants scrutiny, as it may be subject to impairment if the acquired businesses do not perform as expected.

The decreasing cash balance in 2024 compared to prior periods, along with increased common stock repurchases and dividends paid, could signal potential issues with cash management or capital allocation priorities.

8. Conclusion

SolarWinds achieves moderate revenue growth driven by steady demand for IT management software.

Debt reduction progresses but at a slower pace than the bull case.

The company maintains its market share but faces increasing competition from larger players and open-source alternatives.

Valuation remains in line with industry averages.

This scenario assumes no major cybersecurity incidents or economic downturns.

The valuation is not expected to materially expand or contract but remain in line with competitors.

The base case assumes management executes according to expectations and manages costs to maintain profitability and cash flow and as such warrants a neutral view.

This assumes that the business remains on an even keel but does not materially improve its prospects nor impair them for the long haul.

Business activity slowly normalizes and returns to normal over time but at a slower pace than expected.

As such, the market does not expand or contract its current view of the company which is based on the current operating outlook and expectations.

It could be a good place to park money and earn average returns but is not expected to greatly outperform or underperform its peers.

This also assumes that there is no significant macroeconomic disruption that significantly impairs or improves the business outlook as well.

Therefore, the valuation is not expected to materially deviate from current multiples given current performance.

Furthermore, this assumes there are no major disruptions to global supply chains and the competitive landscape remains similar to its current position.

Given these expectations it is difficult to have an opinion one way or the other on the business as it is expected to muddle through and remain at the status quo over the long term.

Given this lack of conviction, an investment would likely generate only average returns and as such it is not a super compelling idea one way or the other.

Furthermore, with interest rates elevated, there may be better opportunities in the market to allocate capital that are more compelling and generate higher returns.

Investors can likely do better than this opportunity, or they may do worse, but the opportunity is not skewed strongly one way or the other in terms of the investor's probabilities and odds of being successful in achieving an above average return compared to its peers.

It would not be expected to deviate significantly from the mean.

So investors may be better served allocating to other opportunities in the market that have a more compelling thesis and potential for growth, margin expansion, innovation, and long term value creation and shareholder upside.

As such, we recommend looking at other opportunities first before allocating capital here.

This may be a good place to allocate capital if one has nowhere else to put it, but it is likely not a first or second choice given what the market has to offer.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Return on Invested Capital (ROIC) and Return on Equity (ROE) would provide deeper insight into capital efficiency, but cannot be calculated directly with the data provided. The significant fluctuations in net income, especially the large losses in some years, will have a great impact on these metrics. To properly calculate ROIC and ROE, we would require invested capital data which can be derived from debt and equity components.

Return on Invested Capital (ROIC) and Return on Equity (ROE) would provide deeper insight into capital efficiency, but cannot be calculated directly with the data provided. The significant fluctuations in net income, especially the large losses in some years, will have a great impact on these metrics. To properly calculate ROIC and ROE, we would require invested capital data which can be derived from debt and equity components. The company demonstrates inconsistent free cash flow (FCF) generation, fluctuating significantly over the past five years. In 2024, the company generated $182.687 million in FCF. Analysis of capital expenditures (Capex) alongside FCF reveals how much the company is reinvesting in its operations to support growth and maintain its asset base.

The company demonstrates inconsistent free cash flow (FCF) generation, fluctuating significantly over the past five years. In 2024, the company generated $182.687 million in FCF. Analysis of capital expenditures (Capex) alongside FCF reveals how much the company is reinvesting in its operations to support growth and maintain its asset base.