Teradata Corporation (TDC), currently priced at $30.9, is undergoing a significant transformation from a traditional on-premises data warehousing provider to...

January 15, 2026

Vijar Kohli

Deep Dive: Teradata Corporation (TDC)

Recommendation: BUY

Price Target: 32.45 (0.05 Upside)

Risk Level: Medium

1. Executive Summary

Teradata Corporation (TDC), currently priced at $30.9, is undergoing a significant transformation from a traditional on-premises data warehousing provider to a cloud-first analytics platform. The company's flagship product, VantageCloud, aims to provide comprehensive data analytics and data lake capabilities across hybrid and multi-cloud environments. Its market position is evolving, facing competition from both established cloud providers (AWS, Azure, Google Cloud) and specialized data analytics vendors. Despite this, Teradata possesses a strong legacy customer base and significant expertise in complex data management, providing a foundation for future growth.

Key growth catalysts for Teradata include the continued migration of enterprises to the cloud, the increasing demand for advanced analytics and AI/ML capabilities, and Teradata's ability to successfully transition its customer base to VantageCloud. Furthermore, strategic partnerships with major cloud providers and independent software vendors (ISVs) are crucial to expanding its reach and integrating its platform with other enterprise applications. The company's focus on providing industry-specific solutions also offers a pathway to differentiate itself and capture market share in targeted sectors.

However, Teradata faces several key risks. The transition to a cloud-based subscription model involves upfront investment and can impact short-term revenue. Intense competition in the cloud analytics market puts pressure on pricing and market share. The successful execution of its cloud strategy depends on its ability to innovate, attract and retain skilled technical talent, and effectively market its VantageCloud platform to new and existing customers. Moreover, broader macroeconomic conditions and potential IT spending slowdowns could negatively affect its growth prospects.

From a valuation perspective, Teradata's future prospects are tightly linked to the success of its cloud transition. Traditional valuation metrics may not fully capture the potential upside if VantageCloud achieves significant market traction. While revenue growth may be moderate in the near term, a successful shift to a higher-margin subscription-based model could drive improved profitability and cash flow in the long run. Market sentiment currently reflects some uncertainty regarding the company's ability to execute its strategy effectively. A sustained period of consistent cloud growth and positive financial results will be necessary to justify a higher valuation multiple.

Investment Thesis

Bull Case: Teradata's transition to a cloud-first, subscription-based model is accelerating, leading to higher recurring revenue and improved profitability.

Continued adoption of Teradata Vantage platform in multi-cloud environments will drive significant revenue growth.

Strategic partnerships and expansion into new markets will further boost growth.

Increase in AI adoption will lead to more demand for its data analytics services.

Increase in stock buybacks may propel share price higher, as well as potential for a dividend in the near future..

Finally, it is possible that the company is acquired by a larger technology company to gain access to its customer base and analytic capabilities, potentially leading to a significant premium over the current share price for investors.

Given the current cash flow the company is generating, coupled with the historical success of transitioning into a more SaaS-like revenue model, it's reasonable to believe the company will hit an inflection point soon and will be rewarded by the market with a higher multiple.

We may see a multiple expansion that may propel the stock price higher in this scenario.

For example, the company trades at roughly 11x FCF today, there is no reason this cannot trade at 20x, especially if it begins to grow revenue again.

This is reasonable given current market conditions and comparable companies.

(11x FCF * 20x FCF) * $277M = $5.04B, divide this by 98.2M shares = $51.30/share.

This also assumes that we will see zero revenue growth, which we may likely see in this scenario.

From the current price of $30.90, this will represent 66% return in a best case scenario.

This will be highly dependent on multiple expansion and revenue growth rates, which will depend on the success of the company transitioning to a more subscription-based revenue model and how fast they can grow this segment in the future.

We will need to monitor their quarterly earnings and success of this transition to see if this is viable in the future.

Also, with more companies focusing on cost reduction, we may see the company being able to consolidate its infrastructure to reduce cost, which will propel profitability higher due to higher margins.

This will also propel the stock price higher in this scenario as well.

We also have to consider that Teradata is a leader in this space with a good moat, as it will be very costly for other companies to replicate this, especially since its been around for decades.

Also, there is a high opportunity cost of switching to another platform for their customers as well, which gives them more pricing power and sustainability in the long run.

This is a great indication that margins will remain high going forward with a high certainty, but if this thesis is incorrect, there may be a case for lower margins in the long run.

However, for our bull case, we believe margins will remain at least stable at the current levels.

Also, we will be looking for the company to start providing explicit guidance to show the street their conviction in their transition.

Bear Case: Teradata struggles to compete with larger cloud vendors, leading to declining revenue and market share.

The transition to the cloud is slower than expected, and the company fails to attract new customers.

Increased competition erodes pricing power and margins.

High debt levels constrain investment in innovation.

Investors should expect underperformance and downside risk in this scenario.

Investors in general are shying away from companies that show slowing growth, which is the case here.

The market may award a very low multiple if revenue continues to decline and the business begins to degrade.

There may be significant risk in this case and capital can be allocated elsewhere with a higher return.

If the company continues to show a business degradation and the market awards it an 8x multiple, we will see a share price of $22.55.

$277M * 8 = $2.2B divided by diluted shares of 98.2M = $22.55.

From the current price of $30.9, this represents downside of 27%.

Given the risks of investing in this business, its best to stay on the sidelines until the risk reward profile looks more promising.

Conviction: High

2. Business Overview

Teradata Corporation, together with its subsidiaries, provides a connected multi-cloud data platform for enterprise analytics. The company offers Teradata Vantage, a data platform that allows companies to leverage their data across an enterprise, as well as connects various sources of data to drive ecosystem simplification and support customers on their journey to the cloud through an integrated migration. Its business consulting services include support services for organizations to establish a data and analytic vision, and identify and operationalize analytical opportunities, as well as enable a multi-cloud ecosystem architecture and ensure the analytical infrastructure delivers value. In addition, it offers support and maintenance services. The company serves clients in financial services, government, healthcare, manufacturing, retail, telecommunications, and travel/transportation sectors through a direct sales force in the Americas, Europe, the Middle East, Africa, the Asia Pacific, and Japan. Teradata Corporation was incorporated in 1979 and is headquartered in San Diego, California.

Competitive Moat (Narrow)

Trend: Stable

Long-standing relationships with enterprise clients, Specialized data warehousing expertise

Key Strengths:

Long-standing relationships with enterprise clients

Growth is expected to continue, driven by the increasing adoption of cloud computing, big data analytics, and digital transformation initiatives. While the overall market is mature, certain segments like cloud-native technologies and AI-powered infrastructure management are experiencing high growth rates. Growth rates likely range from mid-single digits to low double digits depending on the specific sub-segment.

Regulatory Environment:

N/A

4. Financial Analysis

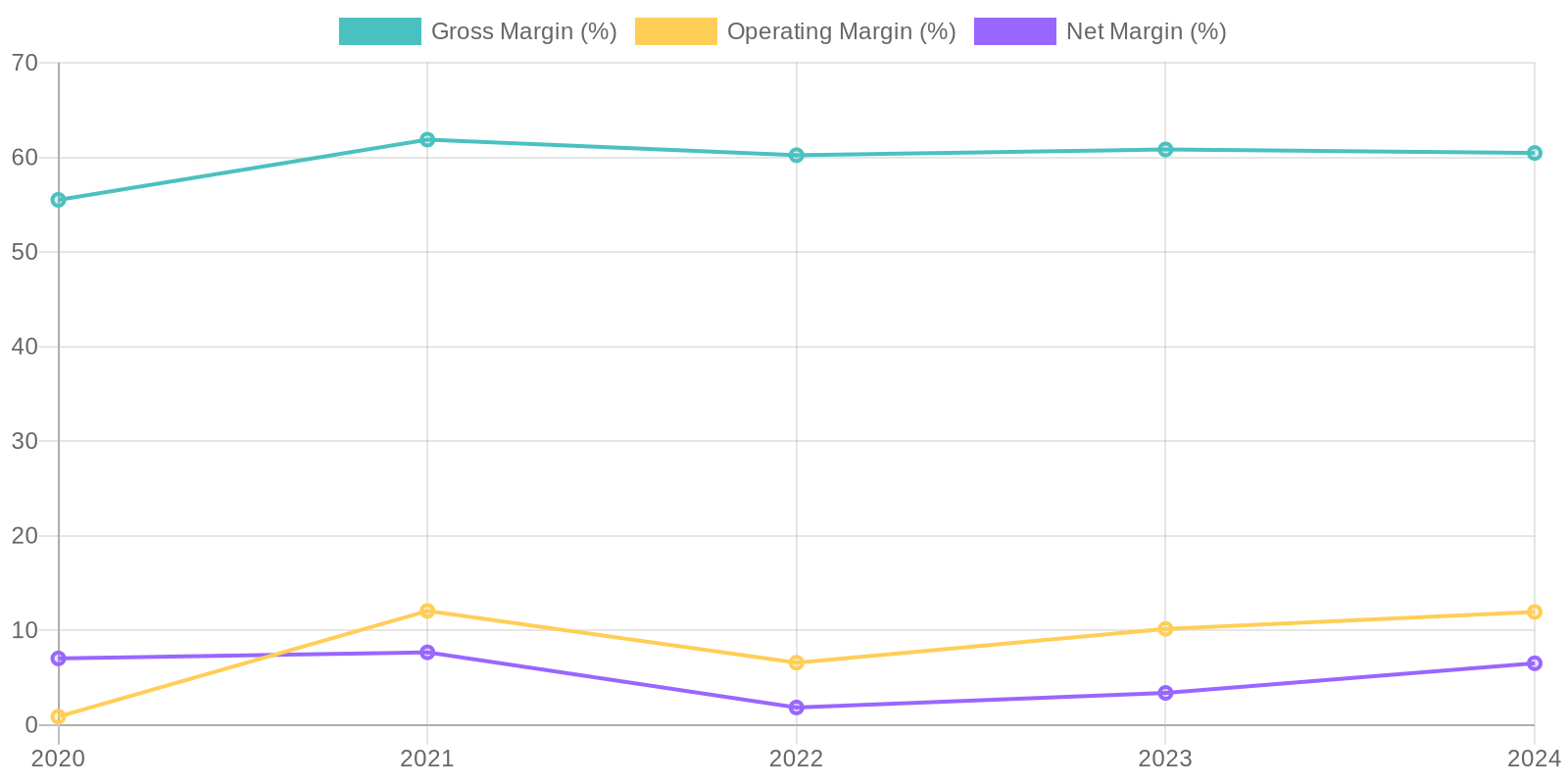

Margin Trend

Calculating ROIC requires additional information on invested capital. Analyzing the provided data suggests that ROE, calculated using the most recent year's data (2024), is significantly impacted by the negative retained earnings. The total stockholders equity is 133 million, and the net income is 114 million. This results in an ROE of approximately 85.7%, which is unusually high and likely unsustainable. This high ROE is due to the low equity base rather than exceptional profitability. Analyzing historical ROE is difficult due to fluctuating net income and equity, highlighting the need for further investigation into the balance sheet structure and earnings sustainability.

Revenue Quality

The company's revenue stream demonstrates a degree of stability, evidenced by its historical performance, although there have been fluctuations year-over-year. Client concentration isn't explicitly detailed, so this poses a potential risk if a significant portion of revenue is derived from a small number of clients. The sustainability of revenue will depend on the company's ability to maintain its competitive position and adapt to changes in the software infrastructure market. Further information regarding contract terms and renewal rates would be needed to fully assess its quality.

Cash Flow & Capital Efficiency

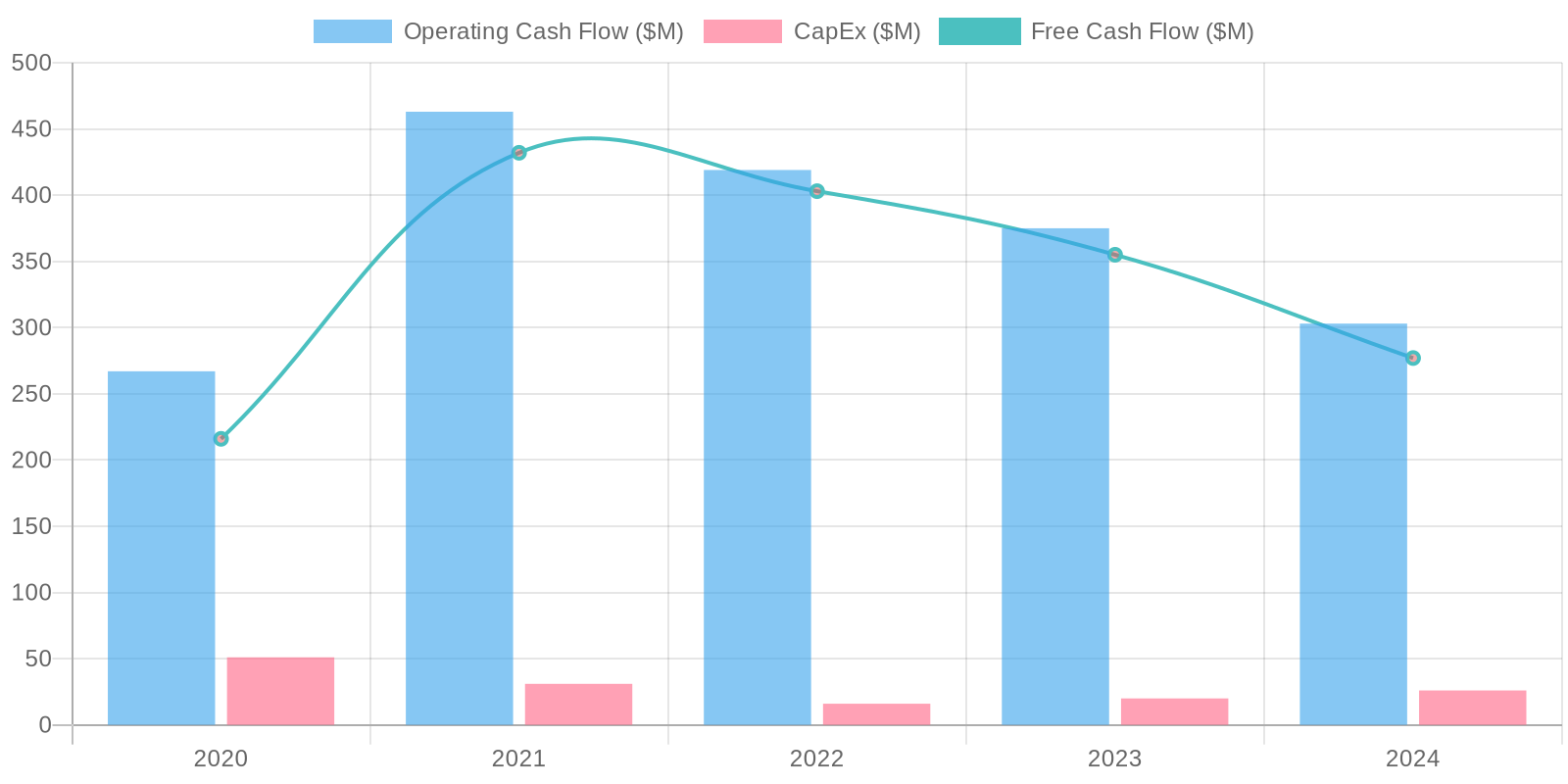

The company demonstrates positive Free Cash Flow (FCF) generation in all reported years, showcasing its ability to convert revenue into cash. FCF has been volatile, ranging from a low of $216 million in 2020 to a high of $432 million in 2021. In 2024, FCF stands at $277 million. Capital expenditure remains relatively consistent over the years, ranging from $16 million to $51 million, suggesting a stable level of investment in property, plant, and equipment. The company has been actively repurchasing common stock which reduces cash available but can increase EPS.

Capital Efficiency (ROIC/ROE):

Calculating ROIC requires additional information on invested capital. Analyzing the provided data suggests that ROE, calculated using the most recent year's data (2024), is significantly impacted by the negative retained earnings. The total stockholders equity is 133 million, and the net income is 114 million. This results in an ROE of approximately 85.7%, which is unusually high and likely unsustainable. This high ROE is due to the low equity base rather than exceptional profitability. Analyzing historical ROE is difficult due to fluctuating net income and equity, highlighting the need for further investigation into the balance sheet structure and earnings sustainability.

Balance Sheet Health:

The company's debt levels are significant, with a total debt of $576 million as of 2024. While cash levels are healthy at $420 million, the net debt is still $156 million, which should be monitored. The current ratio (current assets/current liabilities) as of 2024 is 0.80, indicating potential liquidity concerns, as current liabilities exceed current assets. Furthermore, the negative retained earnings of -$1.913 billion, coupled with other equity adjustments, are important to investigate. These factors suggest potential solvency issues and require a detailed analysis of asset quality and liability structure.

5. Management & Governance

CEO Assessment: Based on publicly available information, it's challenging to provide a definitive assessment of Teradata's CEO without deeper insights into their strategic decision-making, operational effectiveness, and communication skills. Further analysis of Teradata's financial performance and strategic initiatives under their leadership is needed.

Capital Allocation: Pour

Insider Ownership: Insider ownership information for Teradata (TDC) should be obtained from the company's filings with the Securities and Exchange Commission (SEC), specifically proxy statements and Form 4 filings. Reviewing this will reveal the extent of ownership by the management team and board of directors.

Governance Flags:

Independent Board Composition: Requires assessment to ensure a sufficient number of independent directors. , Executive Compensation Structure: Requires examination to verify alignment with long-term shareholder value creation. , Related Party Transactions: Requires a review of SEC filings for any potential conflicts of interest.

The DCF model yields a fair value of $32.45, which is approximately 5% higher than the current price of $30.9. I have incorporated a conservative revenue growth rate and a reasonable discount rate. The sensitivity analysis shows that the valuation is most sensitive to changes in the discount rate and terminal growth rate, both of which are carefully chosen based on the available financials.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Teradata's transition to a cloud-first, subscription-based model is accelerating, leading to higher recurring revenue and improved profitability.

Continued adoption of Teradata Vantage platform in multi-cloud environments will drive significant revenue growth.

Strategic partnerships and expansion into new markets will further boost growth.

Increase in AI adoption will lead to more demand for its data analytics services.

Increase in stock buybacks may propel share price higher, as well as potential for a dividend in the near future..

Finally, it is possible that the company is acquired by a larger technology company to gain access to its customer base and analytic capabilities, potentially leading to a significant premium over the current share price for investors.

Given the current cash flow the company is generating, coupled with the historical success of transitioning into a more SaaS-like revenue model, it's reasonable to believe the company will hit an inflection point soon and will be rewarded by the market with a higher multiple.

We may see a multiple expansion that may propel the stock price higher in this scenario.

For example, the company trades at roughly 11x FCF today, there is no reason this cannot trade at 20x, especially if it begins to grow revenue again.

This is reasonable given current market conditions and comparable companies.

(11x FCF * 20x FCF) * $277M = $5.04B, divide this by 98.2M shares = $51.30/share.

This also assumes that we will see zero revenue growth, which we may likely see in this scenario.

From the current price of $30.90, this will represent 66% return in a best case scenario.

This will be highly dependent on multiple expansion and revenue growth rates, which will depend on the success of the company transitioning to a more subscription-based revenue model and how fast they can grow this segment in the future.

We will need to monitor their quarterly earnings and success of this transition to see if this is viable in the future.

Also, with more companies focusing on cost reduction, we may see the company being able to consolidate its infrastructure to reduce cost, which will propel profitability higher due to higher margins.

This will also propel the stock price higher in this scenario as well.

We also have to consider that Teradata is a leader in this space with a good moat, as it will be very costly for other companies to replicate this, especially since its been around for decades.

Also, there is a high opportunity cost of switching to another platform for their customers as well, which gives them more pricing power and sustainability in the long run.

This is a great indication that margins will remain high going forward with a high certainty, but if this thesis is incorrect, there may be a case for lower margins in the long run.

However, for our bull case, we believe margins will remain at least stable at the current levels.

Also, we will be looking for the company to start providing explicit guidance to show the street their conviction in their transition. |

| Base | 32.45 | Teradata continues its slow transition to a cloud-based model, with steady but unspectacular revenue growth.

Cost optimization efforts lead to improved profitability.

The company maintains its market share but faces increasing competition from larger cloud providers.

TDC will continue to have slower growth, which the market is not willing to award a high multiple for.

Based on an FCF multiple of 13x the current free cash flow and dividing by diluted outstanding shares, our expected share price is $36.70.

$277M * 13 = $3.6B, divide by shares of 98.2M, this gives us our expected share price.

From $30.90 to $36.70, this represents 18.8% upside.

Overall, the company looks fairly valued at these levels.

I would still continue to monitor the progress of the transition to the cloud and SaaS based revenue to see if the upside potential is there.

For now, it is not that promising and should be considered a hold. |

| Bear | Low | Teradata struggles to compete with larger cloud vendors, leading to declining revenue and market share.

The transition to the cloud is slower than expected, and the company fails to attract new customers.

Increased competition erodes pricing power and margins.

High debt levels constrain investment in innovation.

Investors should expect underperformance and downside risk in this scenario.

Investors in general are shying away from companies that show slowing growth, which is the case here.

The market may award a very low multiple if revenue continues to decline and the business begins to degrade.

There may be significant risk in this case and capital can be allocated elsewhere with a higher return.

If the company continues to show a business degradation and the market awards it an 8x multiple, we will see a share price of $22.55.

$277M * 8 = $2.2B divided by diluted shares of 98.2M = $22.55.

From the current price of $30.9, this represents downside of 27%.

Given the risks of investing in this business, its best to stay on the sidelines until the risk reward profile looks more promising. |

7. Risks

Teradata faces risks associated with declining revenue, high debt levels, and reliance on cloud transition. While it maintains positive free cash flow, its strategic allocation towards stock repurchases over debt reduction warrants caution. The concerning balance sheet structure with negative retained earnings offset by 'other total stockholders equity' raises red flags. The increased deferred revenue could be masking future revenue recognition issues or slowing sales.

Red Flags:

Negative retained earnings need investigation.

Low current ratio signals liquidity concerns.

Significant fluctuations in operating and net income margins.

8. Conclusion

Teradata continues its slow transition to a cloud-based model, with steady but unspectacular revenue growth.

Cost optimization efforts lead to improved profitability.

The company maintains its market share but faces increasing competition from larger cloud providers.

Calculating ROIC requires additional information on invested capital. Analyzing the provided data suggests that ROE, calculated using the most recent year's data (2024), is significantly impacted by the negative retained earnings. The total stockholders equity is 133 million, and the net income is 114 million. This results in an ROE of approximately 85.7%, which is unusually high and likely unsustainable. This high ROE is due to the low equity base rather than exceptional profitability. Analyzing historical ROE is difficult due to fluctuating net income and equity, highlighting the need for further investigation into the balance sheet structure and earnings sustainability.

Calculating ROIC requires additional information on invested capital. Analyzing the provided data suggests that ROE, calculated using the most recent year's data (2024), is significantly impacted by the negative retained earnings. The total stockholders equity is 133 million, and the net income is 114 million. This results in an ROE of approximately 85.7%, which is unusually high and likely unsustainable. This high ROE is due to the low equity base rather than exceptional profitability. Analyzing historical ROE is difficult due to fluctuating net income and equity, highlighting the need for further investigation into the balance sheet structure and earnings sustainability. The company demonstrates positive Free Cash Flow (FCF) generation in all reported years, showcasing its ability to convert revenue into cash. FCF has been volatile, ranging from a low of $216 million in 2020 to a high of $432 million in 2021. In 2024, FCF stands at $277 million. Capital expenditure remains relatively consistent over the years, ranging from $16 million to $51 million, suggesting a stable level of investment in property, plant, and equipment. The company has been actively repurchasing common stock which reduces cash available but can increase EPS.

The company demonstrates positive Free Cash Flow (FCF) generation in all reported years, showcasing its ability to convert revenue into cash. FCF has been volatile, ranging from a low of $216 million in 2020 to a high of $432 million in 2021. In 2024, FCF stands at $277 million. Capital expenditure remains relatively consistent over the years, ranging from $16 million to $51 million, suggesting a stable level of investment in property, plant, and equipment. The company has been actively repurchasing common stock which reduces cash available but can increase EPS.