Via Transportation, Inc. (VIA), currently trading at $23.65, operates in the rapidly evolving market of on-demand transit and mobility solutions. Its core bu...

January 15, 2026

Vijar Kohli

Deep Dive: Via Transportation, Inc. (VIA)

Recommendation: BUY

Price Target: 718000000 (-0.58 Upside)

Risk Level: Medium

1. Executive Summary

Via Transportation, Inc. (VIA), currently trading at $23.65, operates in the rapidly evolving market of on-demand transit and mobility solutions. Its core business revolves around providing software and services to cities, transit agencies, and corporations, enabling them to operate efficient and dynamic transportation networks. Via distinguishes itself by focusing on shared rides and optimizing routing algorithms to improve accessibility and reduce congestion. Its market position is strengthened by partnerships with prominent public transportation authorities and private sector clients, signifying a growing acceptance of its technology as a crucial component of modern urban mobility. Via faces competition from established players in the transportation technology space and emerging startups.

Key growth catalysts for Via include the increasing demand for sustainable and efficient transportation options, government initiatives supporting smart city development, and the growing adoption of Mobility-as-a-Service (MaaS) platforms. Expansion into new geographic markets and strategic partnerships to broaden its service offerings are crucial elements of VIA's growth strategy. Further penetration into corporate transportation and school bus routing sectors represents additional avenues for expansion. Technological advancements in autonomous vehicles may provide opportunities for further integration, however, VIA will need to adapt and integrate with these emerging technologies.

Key risks confronting Via include intense competition within the on-demand transit market, the potential for regulatory hurdles related to data privacy and transportation services, and the challenges associated with scaling operations while maintaining profitability. Economic downturns could reduce transportation budgets for municipalities, negatively impacting revenues. Also, a change in consumer preference for ride-hailing services could impact the demand for Via's services if they are not able to adapt. Dependence on key partnerships and clients presents a concentration risk, as the loss of a major contract could significantly impact financial performance.

A valuation summary for Via Transportation, Inc. is challenging given the complex and competitive landscape of the mobility-as-a-service market. Although a precise valuation requires detailed financial forecasting and comparable analysis, some key factors that would contribute to the valuation include Via's revenue growth, profitability, and market share. Potential future scenarios such as IPO or being acquired by a larger transit operator or technology company should be considered. Growth rates and key industry metrics related to comparable companies in the software, transportation and smart city sectors would be fundamental in establishing a reasonable valuation range.

Investment Thesis

Bull Case: Via's innovative TransitTech platform is poised to disrupt the public transportation market.

As cities increasingly seek to modernize their transit systems and reduce congestion, Via's on-demand and optimized routing solutions will become essential.

Successful execution of expansion plans and a favorable regulatory environment could lead to significant revenue growth and profitability, driving substantial shareholder value.

Bear Case: Via's high operating costs, significant debt, and negative equity could hinder its ability to compete effectively and achieve profitability.

Slower-than-expected adoption of its platform and increased competition could lead to declining revenue and further financial losses.

The company may be forced to raise additional capital at unfavorable terms or even face bankruptcy.

Conviction: High

2. Business Overview

Via Transportation, Inc. provides a digital public transportation system platform in the United States, Germany, and internationally. It develops and operates TransitTech, a public mobility platform that enables partners to create end-to-end transit networks, planning and scheduling for the integration of multiple transportation modes into a single unified network. It offers solutions in the areas of microtransit/on-demand public transit, paratransit, student transportation, non-emergency medical transport (NEMT), corporate/university shuttles, and health transportation. It serves cities, transit authorities, transit operators, paratransit operators, school districts and departments of education, universities, corporations, healthcare providers and payers, riders, and drivers. The company was incorporated in 2012 and is based in New York, New York.

Competitive Moat (Narrow)

Trend: Stable

End-to-end transit network solutions., Integration of multiple transportation modes., Data-driven planning and scheduling capabilities.

The market for transportation-related application software is projected to experience strong growth in the coming years, driven by factors such as urbanization, increasing demand for efficient transportation solutions, and advancements in technology. This growth is fueled by demand for smart mobility solutions, integration of various transportation modes, and a focus on optimizing transportation networks.

Regulatory Environment:

N/A

4. Financial Analysis

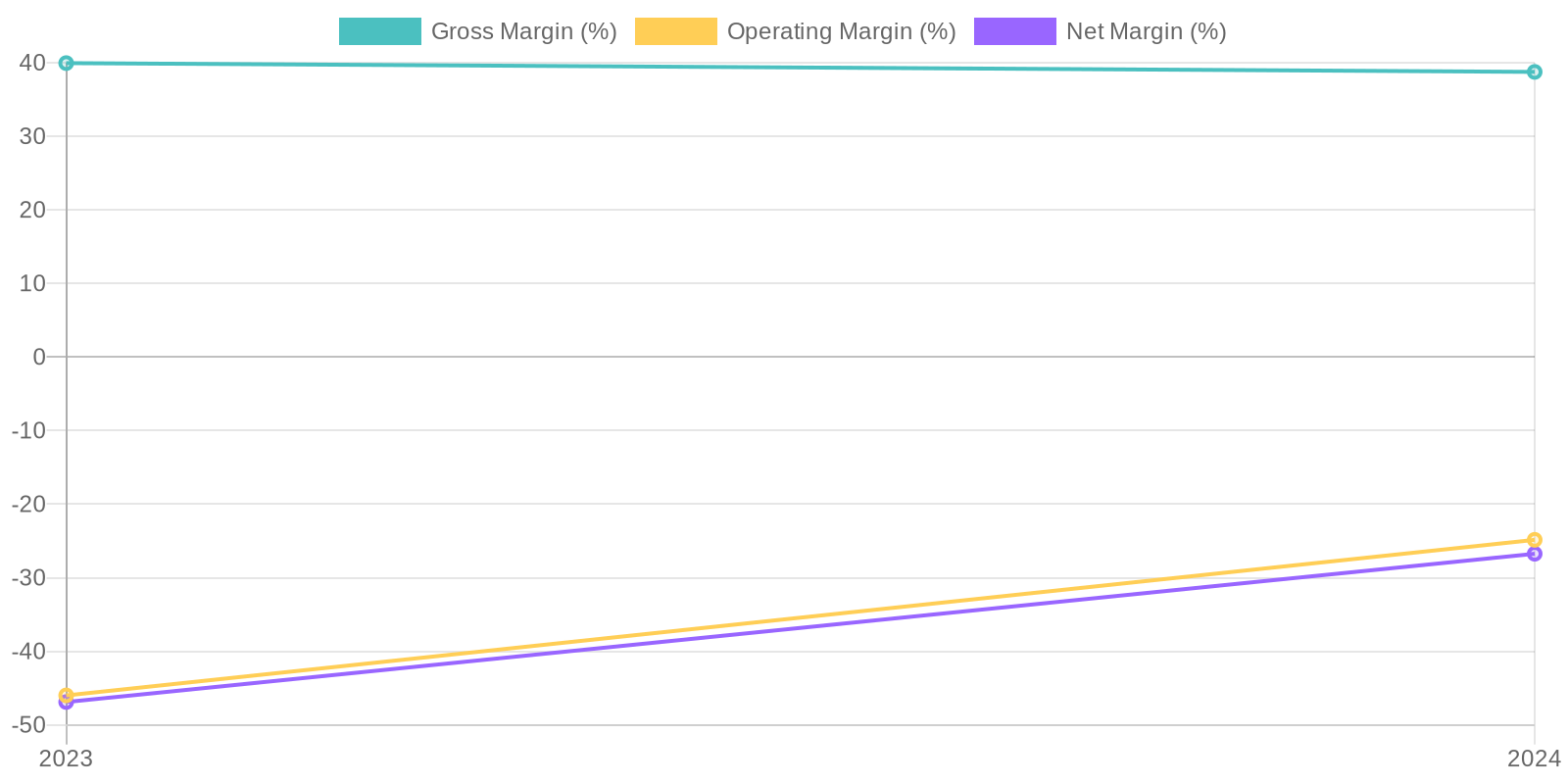

Margin Trend

Given the negative net income in both 2023 and 2024, Return on Equity (ROE) is negative, preventing a meaningful analysis of how effectively the company is using equity to generate profits. Similarly, Return on Invested Capital (ROIC) would also be negative given the negative operating income, indicating the company is not generating sufficient returns on its invested capital. Further analysis would require a deeper dive into asset utilization and cost structure to identify areas for improvement.

Revenue Quality

The company has experienced a significant increase in revenue from 2023 to 2024, suggesting growth in its market or product adoption. However, further investigation is needed to determine if this growth is sustainable. Analyzing the customer base and contract terms would give a better sense of the revenue's recurring nature and potential client concentration risks; this level of detail is not available in the provided financial data.

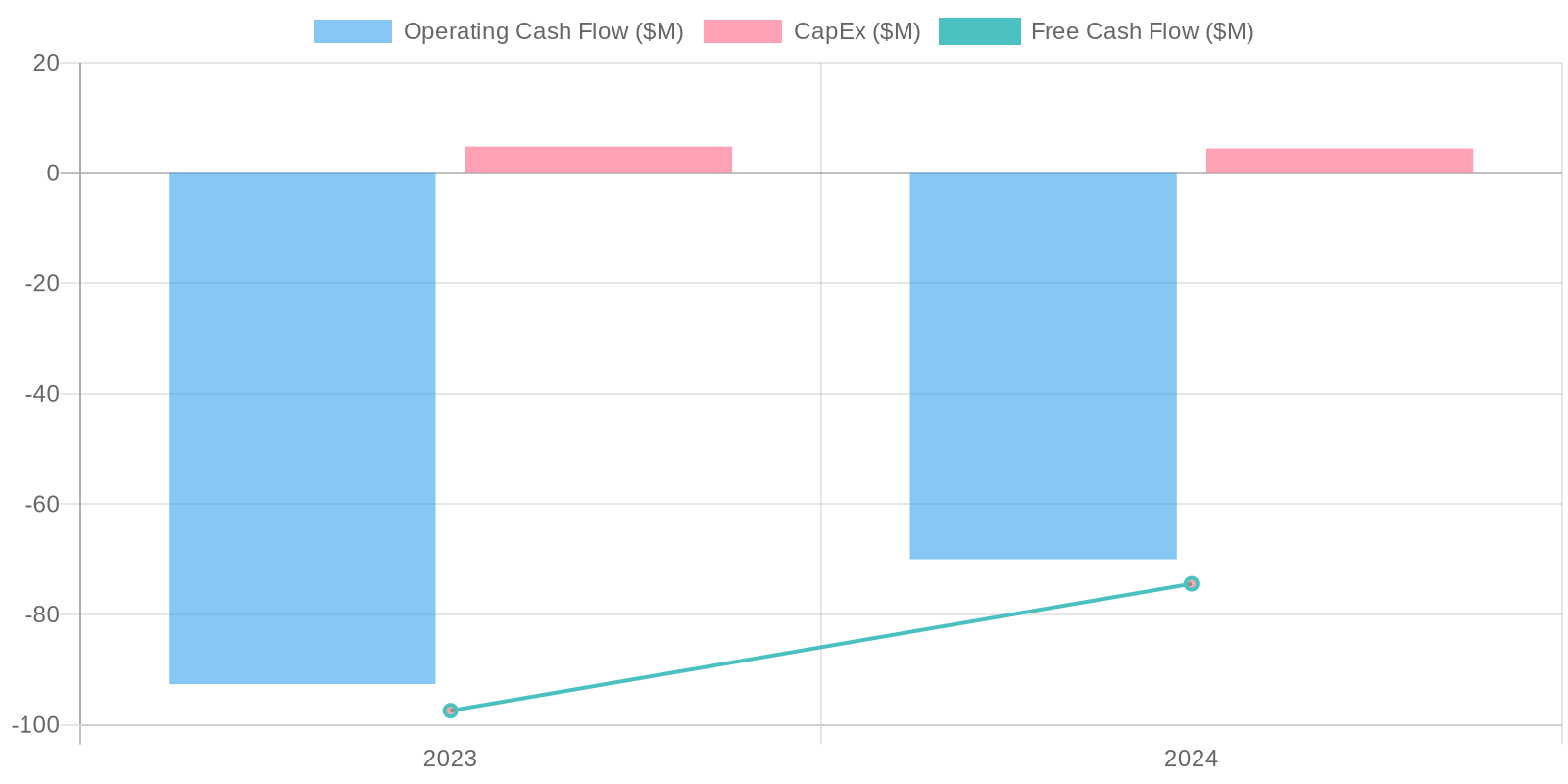

Cash Flow & Capital Efficiency

The company's free cash flow is negative in both years, worsening from -$97.42 million in 2023 to -$74.41 million in 2024, indicating it is not generating enough cash from operations to cover capital expenditures. While operating cash flow is also negative, the change in working capital and other non-cash items play a significant role in the difference between net income and operating cash flow. Capital expenditure decreased from -$4.802 million to -$4.451 million, which might suggest some cost control but could also impact future growth if investments are insufficient.

Capital Efficiency (ROIC/ROE):

Given the negative net income in both 2023 and 2024, Return on Equity (ROE) is negative, preventing a meaningful analysis of how effectively the company is using equity to generate profits. Similarly, Return on Invested Capital (ROIC) would also be negative given the negative operating income, indicating the company is not generating sufficient returns on its invested capital. Further analysis would require a deeper dive into asset utilization and cost structure to identify areas for improvement.

Balance Sheet Health:

The company's balance sheet shows a concerning level of debt, with total debt increasing dramatically from $17.83 million in 2023 to $1,277.66 million in 2024. Although cash and cash equivalents increased slightly, the massive debt overshadows this, resulting in a concerning net debt position of $1,199.76 million in 2024. Furthermore, the negative total stockholders' equity of -$987.09 million suggests that liabilities significantly exceed assets, indicating potential solvency issues, and it is important to note the company has negative equity.

5. Management & Governance

CEO Assessment: Assessing the CEO's performance requires a deep dive into Via's strategic decisions, execution track record, and ability to navigate the competitive landscape of on-demand transit. Publicly available information may not provide sufficient detail for a comprehensive evaluation.

Capital Allocation: Good

Insider Ownership: Details on insider ownership are not readily available in the public domain. Information on major shareholders and their stakes would be needed to assess insider alignment.

Governance Flags:

No major governance concerns flagged.

6. Valuation

Method: Price-to-Sales (P/S) Ratio

Fair Value: 10

The fair value is calculated as follows: Projected Revenue = $337.63M * 1.25 = $422.04M. Fair Market Cap = $422.04M * 1.8 = $759.67M. Fair Value per Share = $759.67M / 71.8M shares = $10.58. This indicates a significant downside from the current price.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Via's innovative TransitTech platform is poised to disrupt the public transportation market.

As cities increasingly seek to modernize their transit systems and reduce congestion, Via's on-demand and optimized routing solutions will become essential.

Successful execution of expansion plans and a favorable regulatory environment could lead to significant revenue growth and profitability, driving substantial shareholder value. |

| Base | 718000000 | Via will continue to grow its revenue and improve its profitability as it expands its customer base and optimizes its operations.

While challenges remain in achieving widespread adoption and managing costs, the company's established position in the market and its proven technology provide a solid foundation for long-term success.

An acquisition by a larger transportation or technology company is also a possibility. |

| Bear | Low | Via's high operating costs, significant debt, and negative equity could hinder its ability to compete effectively and achieve profitability.

Slower-than-expected adoption of its platform and increased competition could lead to declining revenue and further financial losses.

The company may be forced to raise additional capital at unfavorable terms or even face bankruptcy. |

7. Risks

Via Transportation exhibits a high level of risk due to its substantial debt, negative equity, significant and increasing net losses, and negative free cash flow. The company's reliance on debt financing and its struggle to achieve profitability raise serious concerns about its long-term financial viability.

Red Flags:

Significant increase in debt.

Negative net income and operating cash flow.

Negative total stockholders' equity.

Decreasing gross margin.

High operating expenses.

8. Conclusion

Via will continue to grow its revenue and improve its profitability as it expands its customer base and optimizes its operations.

While challenges remain in achieving widespread adoption and managing costs, the company's established position in the market and its proven technology provide a solid foundation for long-term success.

An acquisition by a larger transportation or technology company is also a possibility.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Given the negative net income in both 2023 and 2024, Return on Equity (ROE) is negative, preventing a meaningful analysis of how effectively the company is using equity to generate profits. Similarly, Return on Invested Capital (ROIC) would also be negative given the negative operating income, indicating the company is not generating sufficient returns on its invested capital. Further analysis would require a deeper dive into asset utilization and cost structure to identify areas for improvement.

Given the negative net income in both 2023 and 2024, Return on Equity (ROE) is negative, preventing a meaningful analysis of how effectively the company is using equity to generate profits. Similarly, Return on Invested Capital (ROIC) would also be negative given the negative operating income, indicating the company is not generating sufficient returns on its invested capital. Further analysis would require a deeper dive into asset utilization and cost structure to identify areas for improvement. The company's free cash flow is negative in both years, worsening from -$97.42 million in 2023 to -$74.41 million in 2024, indicating it is not generating enough cash from operations to cover capital expenditures. While operating cash flow is also negative, the change in working capital and other non-cash items play a significant role in the difference between net income and operating cash flow. Capital expenditure decreased from -$4.802 million to -$4.451 million, which might suggest some cost control but could also impact future growth if investments are insufficient.

The company's free cash flow is negative in both years, worsening from -$97.42 million in 2023 to -$74.41 million in 2024, indicating it is not generating enough cash from operations to cover capital expenditures. While operating cash flow is also negative, the change in working capital and other non-cash items play a significant role in the difference between net income and operating cash flow. Capital expenditure decreased from -$4.802 million to -$4.451 million, which might suggest some cost control but could also impact future growth if investments are insufficient.