Varonis Systems, Inc. (VRNS) operates in the data security and analytics market, focusing on protecting enterprise data stored across various platforms, incl...

January 15, 2026

Vijar Kohli

Deep Dive: Varonis Systems, Inc. (VRNS)

Recommendation: BUY

Price Target: 28.5 (-0.16 Upside)

Risk Level: Medium

1. Executive Summary

Varonis Systems, Inc. (VRNS) operates in the data security and analytics market, focusing on protecting enterprise data stored across various platforms, including on-premises and cloud environments. Their solutions provide visibility into data access and usage, detect insider threats and cyberattacks, and automate data governance tasks. Currently, Varonis is transitioning towards a subscription-based revenue model, which impacts short-term reported revenue but aims for more predictable and recurring long-term revenue streams. The company faces competition from both specialized security vendors and larger, diversified technology companies that offer overlapping functionalities within their broader portfolios. At a current price of $33.96, the stock's performance is significantly influenced by overall market sentiment towards growth stocks and the company's ability to successfully execute its transition to a subscription model.

Key growth catalysts for Varonis include the increasing complexity of data environments, driven by cloud adoption and hybrid IT architectures. This complexity creates greater challenges for organizations to secure and govern their data effectively, leading to higher demand for Varonis's solutions. Furthermore, rising cybersecurity threats, stricter data privacy regulations (such as GDPR and CCPA), and the growing awareness of insider threats are driving further adoption of data security solutions. Varonis's ability to innovate and expand its platform to cover emerging data sources and security threats will be crucial for maintaining its competitive advantage and driving future growth. Strategic partnerships and integrations with leading cloud providers and other security vendors can also accelerate market penetration.

Key risks for Varonis include intense competition in the data security market, which could pressure pricing and market share. The company's transition to a subscription model also poses a risk, as slower-than-expected adoption of subscriptions could negatively impact near-term revenue growth. Furthermore, macroeconomic factors, such as an economic downturn, could lead to reduced IT spending by organizations, affecting Varonis's sales. The company must effectively manage its operating expenses to achieve profitability and demonstrate the value proposition of its solutions to customers in a competitive landscape. Execution risk related to product development and sales strategy also remain key considerations.

Valuation of Varonis is complex, considering its ongoing transition. Traditional valuation metrics, such as price-to-earnings (P/E) ratio, may be less relevant during this period. Investors are likely focusing on metrics such as revenue growth rate, annual recurring revenue (ARR), and customer lifetime value (CLTV) to assess the company's long-term potential. A premium valuation would be justified if Varonis can consistently demonstrate strong ARR growth, high customer retention rates, and expanding gross margins. However, if growth slows or profitability remains elusive, the stock price could face downward pressure. A discounted cash flow (DCF) analysis, incorporating realistic growth assumptions and discount rates, would provide a more comprehensive valuation perspective.

Investment Thesis

Bull Case: Varonis will experience accelerated revenue growth due to increasing demand for data security solutions, driven by data breaches and evolving regulatory landscape.

Successful execution of its cloud strategy and expansion of its product offerings will further fuel growth and improve profitability.

Increased focus on profitability and cost optimization will lead to improved earnings and free cash flow generation.

Bear Case: Varonis's growth will be limited by increasing competition and slower adoption of its cloud solutions.

Inability to innovate and adapt to changing market conditions will lead to market share loss.

Increased debt burden and potential economic downturn will put pressure on profitability and financial stability.

Conviction: High

2. Business Overview

Varonis Systems, Inc. provides software products and services that allow enterprises to manage, analyze, alert, and secure enterprise data in North America, Europe, the Middle East, Africa, and internationally. Its software enables enterprises to protect data stored on premises and in the cloud, including sensitive files and emails; confidential personal data belonging to customers, and patients and employees' data; financial records; strategic and product plans; and other intellectual property. The company offers DatAdvantage that captures, aggregates, normalizes, and analyzes every data access event for users on Windows and UNIX/Linux servers, storage devices, email systems, Intranet servers, cloud applications, and data stores; and DatAlert that profiles users, devices, and their behaviors related to systems and data, detects and alerts on deviations that indicate compromise, and provides a Web-based dashboard and investigative interface. It also provides Data Classification Engine that identifies and tags data based on criteria set in various metadata dimensions, as well as provides business and information technology (IT) personnel with actionable intelligence about data; and DataPrivilege, which offers a self-service Web portal that allows users to request access to data necessary for their business functions, and owners to grant access without IT intervention. In addition, the company provides Data Transport Engine, which provides an execution engine that unifies the manipulation of data and metadata, translating business decisions, and instructions into technical commands, such as data migration or archiving; and DatAnswers that offers search functionality for enterprise data. Varonis Systems, Inc. sells products and services through a network of distributors and resellers. The company serves IT, security, and business personnel. Varonis Systems, Inc. was incorporated in 2004 and is headquartered in New York, New York.

Competitive Moat (Narrow)

Trend: Stable

Specialization in data access governance., Platform that manages on-premise and cloud data security., Analytics capabilities for data breach detection., Established customer base in compliance heavy industries.

Key Strengths:

Specialization in data access governance.

Platform that manages on-premise and cloud data security.

Analytics capabilities for data breach detection.

Established customer base in compliance heavy industries.

The market is projected to continue growing at a healthy rate, driven by increasing data volumes, rising cybersecurity threats, and the shift to cloud computing. Demand for data privacy and compliance solutions is also fueling growth. Cloud adoption and complex data environments are significant growth drivers.

Regulatory Environment:

N/A

4. Financial Analysis

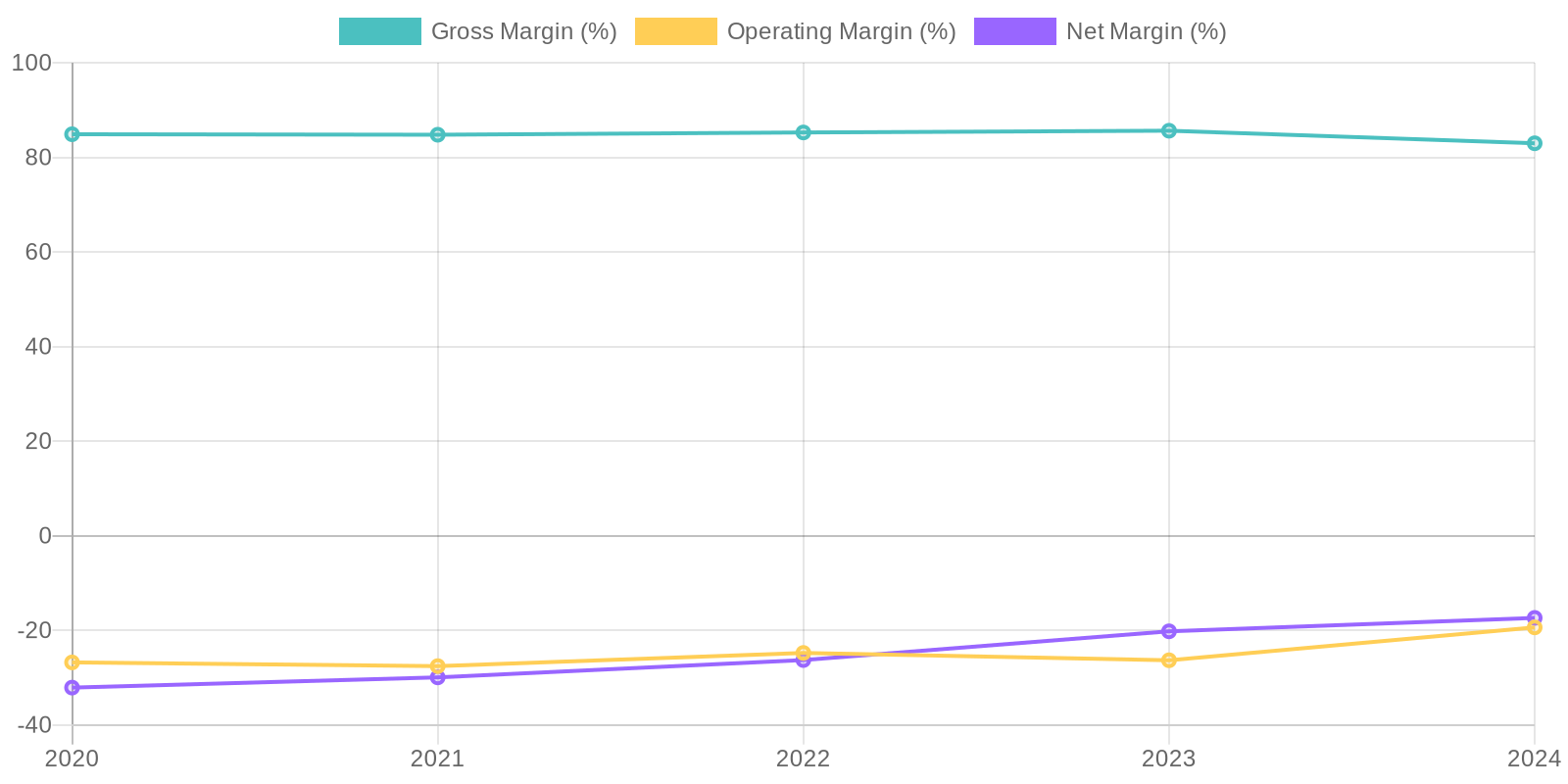

Margin Trend

Given the negative net income figures for the past five years, Return on Invested Capital (ROIC) and Return on Equity (ROE) would also be negative, indicating inefficient use of capital. It is crucial to assess how effectively Veronis is deploying its investments and equity to generate profits and improve these metrics. Analyzing the specific drivers behind these negative returns is essential for developing strategies to enhance capital efficiency.

Revenue Quality

Veronis's revenue has generally increased over the past five years, suggesting growth in its market or successful sales strategies, though 2024 showed only slight growth. It is important to investigate the sources of revenue to assess whether they are one-time projects or from consistent subscriptions. High client concentration would pose a risk if a major client were to leave, necessitating diversification to ensure continued revenue streams.

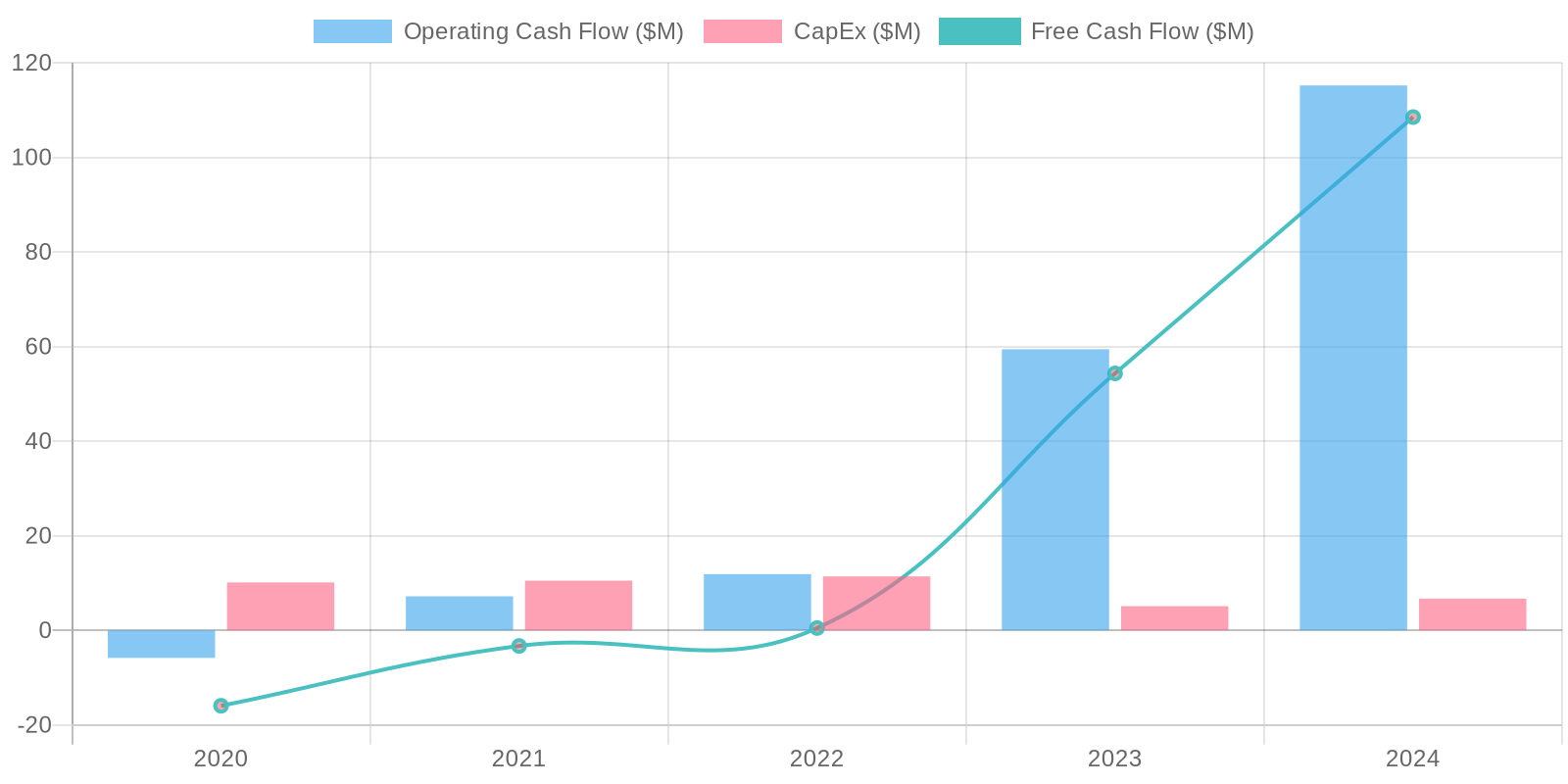

Cash Flow & Capital Efficiency

Veronis showcases fluctuating cash flow dynamics; while operating cash flow turned positive in 2023 and 2024, prior years reflect inconsistent performance. Capital expenditures remain relatively low, which is typical for a software infrastructure company, yet free cash flow mirrors the inconsistency seen in operating cash flow. The considerable investments and divestments in securities influence cash from investing activities, suggesting active treasury management that requires careful monitoring.

Capital Efficiency (ROIC/ROE):

Given the negative net income figures for the past five years, Return on Invested Capital (ROIC) and Return on Equity (ROE) would also be negative, indicating inefficient use of capital. It is crucial to assess how effectively Veronis is deploying its investments and equity to generate profits and improve these metrics. Analyzing the specific drivers behind these negative returns is essential for developing strategies to enhance capital efficiency.

Balance Sheet Health:

Veronis maintains reasonable liquidity with adequate cash and short-term investments to cover current liabilities, as indicated by the current ratio. However, the company carries a substantial amount of debt, which, when combined with negative retained earnings, raises concerns about long-term solvency. It is vital to monitor the debt-to-equity ratio and assess the company's ability to service its debt obligations from its operating income and cash flow.

5. Management & Governance

CEO Assessment: Based on available information, Varonis is led by its co-founder and CEO, Yaki Faitelson. Assessments of his performance would require a deeper dive into metrics such as revenue growth, profitability, innovation, and employee satisfaction. His long tenure suggests a deep understanding of the company and its market.

Capital Allocation: Good

Insider Ownership: Insider ownership details for Varonis should be examined to determine the level of alignment between management and shareholders. A review of recent SEC filings (Form 4s) would provide precise figures on stock ownership by key executives and board members. Generally, higher insider ownership is viewed positively.

Governance Flags:

No major governance concerns flagged.

The DCF valuation indicates a fair value of $28.50, which is below the current market price of $33.96. This suggests that the stock might be overvalued based on the selected assumptions. The negative upside indicates the potential for price decrease, while the downside represents the risk of further decline from the calculated fair value. The analysis considers revenue growth, profitability, and the time value of money. The confidence level is medium because while the DCF model is robust, the assumptions about future growth and discount rate could significantly impact the outcome.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Varonis will experience accelerated revenue growth due to increasing demand for data security solutions, driven by data breaches and evolving regulatory landscape.

Successful execution of its cloud strategy and expansion of its product offerings will further fuel growth and improve profitability.

Increased focus on profitability and cost optimization will lead to improved earnings and free cash flow generation. |

| Base | 28.5 | Varonis will continue to grow its revenue at a moderate pace, driven by the increasing importance of data security.

The company will maintain its market position but may face challenges from larger competitors.

Profitability will improve gradually as the company scales its operations. |

| Bear | Low | Varonis's growth will be limited by increasing competition and slower adoption of its cloud solutions.

Inability to innovate and adapt to changing market conditions will lead to market share loss.

Increased debt burden and potential economic downturn will put pressure on profitability and financial stability. |

7. Risks

Varonis faces moderate risks stemming from consistent net losses, high debt levels, and significant operating expenses despite revenue growth. The reliance on debt and the composition of assets raise concerns about financial flexibility and long-term sustainability. High SG&A as a percentage of revenue suggests sales and marketing are very expensive compared to returns.

Red Flags:

Consistent net losses over the past five years raise concerns about the long-term viability of the company.

High debt levels compared to equity could create financial strain and limit future growth opportunities.

Significant selling, general, and administrative expenses are eating into gross profits, suggesting inefficiencies in operations or excessive spending.

Fluctuating cash flows and reliance on investment activities for liquidity necessitate close scrutiny of treasury management practices.

8. Conclusion

Varonis will continue to grow its revenue at a moderate pace, driven by the increasing importance of data security.

The company will maintain its market position but may face challenges from larger competitors.

Profitability will improve gradually as the company scales its operations.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Given the negative net income figures for the past five years, Return on Invested Capital (ROIC) and Return on Equity (ROE) would also be negative, indicating inefficient use of capital. It is crucial to assess how effectively Veronis is deploying its investments and equity to generate profits and improve these metrics. Analyzing the specific drivers behind these negative returns is essential for developing strategies to enhance capital efficiency.

Given the negative net income figures for the past five years, Return on Invested Capital (ROIC) and Return on Equity (ROE) would also be negative, indicating inefficient use of capital. It is crucial to assess how effectively Veronis is deploying its investments and equity to generate profits and improve these metrics. Analyzing the specific drivers behind these negative returns is essential for developing strategies to enhance capital efficiency. Veronis showcases fluctuating cash flow dynamics; while operating cash flow turned positive in 2023 and 2024, prior years reflect inconsistent performance. Capital expenditures remain relatively low, which is typical for a software infrastructure company, yet free cash flow mirrors the inconsistency seen in operating cash flow. The considerable investments and divestments in securities influence cash from investing activities, suggesting active treasury management that requires careful monitoring.

Veronis showcases fluctuating cash flow dynamics; while operating cash flow turned positive in 2023 and 2024, prior years reflect inconsistent performance. Capital expenditures remain relatively low, which is typical for a software infrastructure company, yet free cash flow mirrors the inconsistency seen in operating cash flow. The considerable investments and divestments in securities influence cash from investing activities, suggesting active treasury management that requires careful monitoring.