Verint Systems Inc. (VRNT), currently trading at $20.51, operates in the Customer Engagement market, providing software and solutions for customer experience...

January 15, 2026

Vijar Kohli

Deep Dive: Verint Systems Inc. (VRNT)

Recommendation: BUY

Price Target: 21.5 (11.61 Upside)

Risk Level: Medium

1. Executive Summary

Verint Systems Inc. (VRNT), currently trading at $20.51, operates in the Customer Engagement market, providing software and solutions for customer experience (CX) automation. While traditionally known for its workforce management solutions, Verint is undergoing a transformation towards a cloud-based, AI-driven platform focused on optimizing customer interactions and improving operational efficiency for its clients. This shift is intended to capture higher-margin recurring revenue and address evolving customer needs in a dynamic market. Its market position is evolving from a legacy provider to a potential challenger in the modern CX space, competing against established players while catering to a large, existing customer base.

Growth catalysts for Verint include the increasing demand for AI-powered customer engagement solutions, particularly in sectors like financial services, healthcare, and retail. The company's cloud transition, if successful, is expected to drive higher subscription revenue and improve profitability. Continued innovation in areas such as conversational AI, predictive analytics, and intelligent automation should allow Verint to differentiate its offerings and attract new customers. Furthermore, strategic partnerships and acquisitions could expand Verint's capabilities and market reach, allowing the company to offer more complete solutions. Successful migration of on-premise customers to cloud-based solutions will also fuel growth.

Key risks facing Verint involve intense competition from larger, more established players in the CX market, such as Salesforce, Oracle, and Microsoft. The company's cloud transition carries execution risk, including potential challenges in migrating existing customers, developing new cloud-native solutions, and managing costs. Economic downturns could reduce customer spending on customer engagement solutions, impacting Verint's revenue growth. Additionally, changes in data privacy regulations and increasing security concerns could increase compliance costs and complicate the company's operations. Failure to innovate and adapt to changing customer needs could lead to market share loss.

From a valuation perspective, Verint's current stock price reflects the market's uncertainty regarding the success of its cloud transition and its ability to compete effectively in the competitive CX market. A sum-of-the-parts valuation might be useful, considering legacy on-premise versus cloud business. While there is potential for significant upside if the company successfully executes its strategy and achieves its growth targets, there is also downside risk if it fails to compete and maintain market share. Analyzing key valuation metrics such as price-to-sales, price-to-earnings, and discounted cash flow is crucial to assessing Verint's fair value, while constantly monitoring the company's progress in its cloud transition and new customer acquisitions.

Investment Thesis

Bull Case: Verint will achieve significant revenue growth and margin expansion due to its strong position in the customer engagement market and successful execution of its growth strategy.

Investment in innovation and strategic acquisitions will accelerate growth and drive shareholder value.

Revenue grows to $1.2B and FCF to $250M.

Assuming a 15x FCF multiple, the target market cap becomes $3.75B

Bear Case: Verint will face significant challenges in a competitive market, leading to slower growth, declining profitability, and reduced cash flow.

Execution missteps and external risks will further pressure the company's valuation.

Conviction: High

2. Business Overview

Verint Systems Inc. provides customer engagement solutions worldwide. It offers various applications for use in Forecasting and Scheduling, which understands the work needed to meet and exceed customer expectations; Quality and Compliance that uses automation and analytics for customer interactions for attended and self-service channels; Interaction Insights, which extracts insights from structured and unstructured customer interactions and activities; Real-Time Work that supports in-the-moment workforce activities; Engagement Channels, an application for messaging, social, chat, email, and interactive voice response; Conversational AI, an intelligent virtual assistant application to enable human-like conversations across every channel; Engagement Orchestration, an application that improves employee efficiency, time to resolution, compliance, and customer satisfaction with workflows; Knowledge Management, which help agents to deliver stellar service with tools. The company also provides Experience Management application which collect and analyze customer experience data, as well as customer engagement cloud platform services. Verint Systems Inc. was incorporated in 1994 and is headquartered in Melville, New York.

Competitive Moat (Narrow)

Trend: Stable

Deep expertise in contact center operations, Integrated suite of solutions covering various aspects of customer engagement

Key Strengths:

Deep expertise in contact center operations

Integrated suite of solutions covering various aspects of customer engagement

The market is expected to continue growing at a healthy pace, driven by the factors mentioned above. Estimates vary, but a CAGR (Compound Annual Growth Rate) of 10-15% over the next 5-7 years would not be unreasonable, especially in areas such as cloud-native technologies, AI-powered infrastructure management, and cybersecurity related to infrastructure.

Regulatory Environment:

N/A

4. Financial Analysis

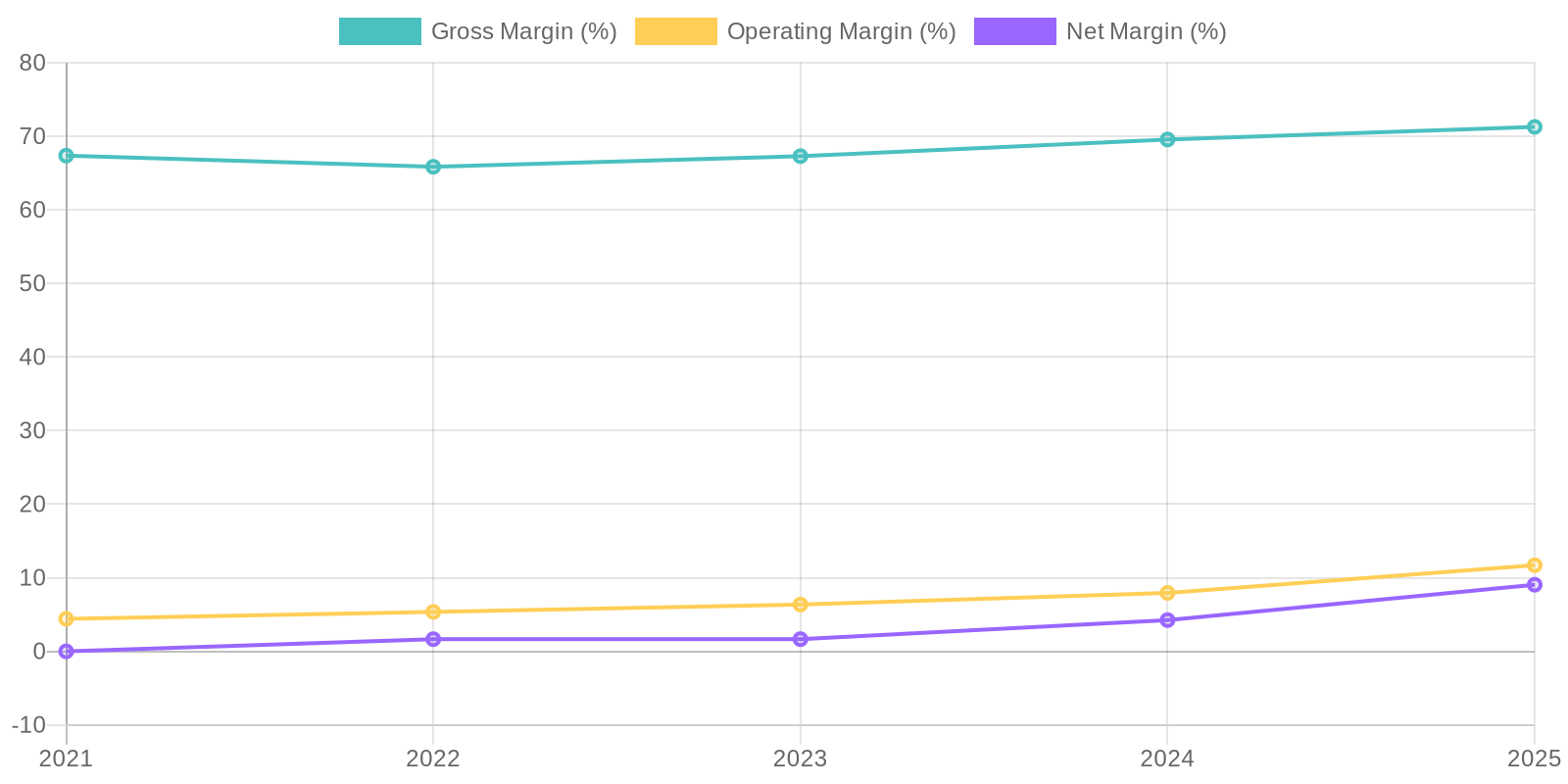

Margin Trend

Return on Invested Capital (ROIC) and Return on Equity (ROE) cannot be accurately calculated with the provided information without additional details on invested capital. However, given the fluctuations in net income and a generally increasing trend in total equity, it is likely that both ROIC and ROE have also experienced volatility over the period. A detailed analysis of the components of invested capital and equity would be required for a more precise assessment.

Revenue Quality

The company's revenue stream shows a generally stable trend over the past five years, with a slight dip in 2022 before recovering. Further investigation would be needed to determine the proportion of recurring revenue versus one-time sales to assess the long-term sustainability of revenue. Client concentration should also be examined to understand the potential impact of losing a major customer.

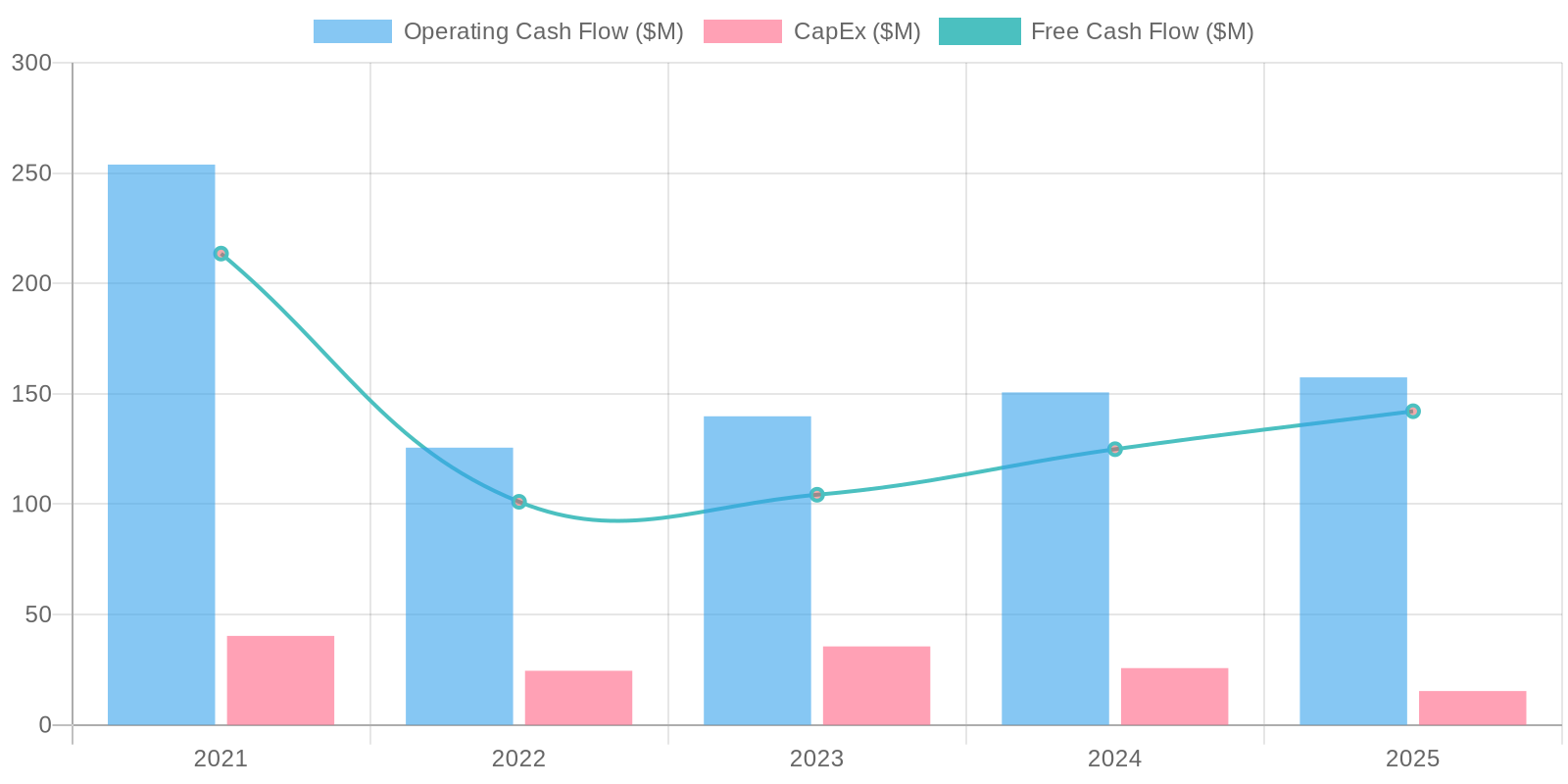

Cash Flow & Capital Efficiency

Free cash flow has been generally positive, though fluctuating, indicating the company's ability to generate cash after capital expenditures. Capital expenditure appears relatively stable, suggesting consistent investment in property, plant, and equipment. The conversion of net income to operating cash flow varies, influenced by non-cash items such as depreciation and stock-based compensation, as well as changes in working capital.

Capital Efficiency (ROIC/ROE):

Return on Invested Capital (ROIC) and Return on Equity (ROE) cannot be accurately calculated with the provided information without additional details on invested capital. However, given the fluctuations in net income and a generally increasing trend in total equity, it is likely that both ROIC and ROE have also experienced volatility over the period. A detailed analysis of the components of invested capital and equity would be required for a more precise assessment.

Balance Sheet Health:

The company carries a substantial amount of debt, although the cash balance provides some offset, the net debt is significant. Liquidity appears adequate based on the current ratio, but the level of deferred revenue indicates a significant portion of liabilities related to future obligations. The balance sheet shows a considerable amount of goodwill and intangible assets, which should be carefully evaluated for potential impairment.

5. Management & Governance

CEO Assessment: Evaluating the CEO of Verint Systems would require specific, in-depth analysis of their strategic decisions, operational efficiency improvements, innovation initiatives, and overall leadership effectiveness. Without access to proprietary performance data and a comprehensive evaluation framework, a definitive assessment is not possible. Publicly available information such as earnings calls and press releases would need to be analyzed to form an opinion on their performance.

Capital Allocation: Good

Insider Ownership: Assessing insider ownership requires up-to-date data from regulatory filings (e.g., SEC Form 4 filings). Generally, a moderate level of insider ownership can be seen as a positive sign, indicating alignment between management's interests and those of shareholders. Very high or very low insider ownership can sometimes raise concerns; very high ownership might concentrate control, while very low ownership might suggest a lack of confidence. The specific percentage and its implications should be investigated using current data.

Governance Flags:

No major governance concerns flagged.

6. Valuation

Method: Discounted Cash Flow (DCF) Model

Fair Value: 22.89

Based on the DCF model, the fair value of VRNT is estimated to be $22.89. Considering the current market price of $20.51, the stock appears to be slightly undervalued. The Price/Sales ratio sanity check yields a price target of $20.11. Weighing these valuations, I arrive at a final price target of $21.5.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Verint will achieve significant revenue growth and margin expansion due to its strong position in the customer engagement market and successful execution of its growth strategy.

Investment in innovation and strategic acquisitions will accelerate growth and drive shareholder value.

Revenue grows to $1.2B and FCF to $250M.

Assuming a 15x FCF multiple, the target market cap becomes $3.75B |

| Base | 21.5 | Verint will continue to grow at a moderate pace, driven by the overall growth in the customer engagement market.

The company will maintain its profitability and generate consistent cash flow.

Revenue grows to $1.05B and FCF to $160M.

Assuming a 12x FCF multiple, the target market cap becomes $1.92B |

| Bear | Low | Verint will face significant challenges in a competitive market, leading to slower growth, declining profitability, and reduced cash flow.

Execution missteps and external risks will further pressure the company's valuation. |

7. Risks

Verint faces risks associated with its debt levels, slow revenue growth, and reliance on goodwill and intangible assets. The transition to a cloud-based subscription model could also present challenges. Though free cash flow is positive, its deployment towards stock buybacks and preferred stock dividends seems suboptimal.

Red Flags:

Fluctuations in operating and net income raise concerns about earnings stability.

High levels of debt relative to cash could pose risks in a rising interest rate environment.

Significant goodwill and intangible assets may indicate past acquisitions that need further scrutiny.

8. Conclusion

Verint will continue to grow at a moderate pace, driven by the overall growth in the customer engagement market.

The company will maintain its profitability and generate consistent cash flow.

Revenue grows to $1.05B and FCF to $160M.

Assuming a 12x FCF multiple, the target market cap becomes $1.92B

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Return on Invested Capital (ROIC) and Return on Equity (ROE) cannot be accurately calculated with the provided information without additional details on invested capital. However, given the fluctuations in net income and a generally increasing trend in total equity, it is likely that both ROIC and ROE have also experienced volatility over the period. A detailed analysis of the components of invested capital and equity would be required for a more precise assessment.

Return on Invested Capital (ROIC) and Return on Equity (ROE) cannot be accurately calculated with the provided information without additional details on invested capital. However, given the fluctuations in net income and a generally increasing trend in total equity, it is likely that both ROIC and ROE have also experienced volatility over the period. A detailed analysis of the components of invested capital and equity would be required for a more precise assessment. Free cash flow has been generally positive, though fluctuating, indicating the company's ability to generate cash after capital expenditures. Capital expenditure appears relatively stable, suggesting consistent investment in property, plant, and equipment. The conversion of net income to operating cash flow varies, influenced by non-cash items such as depreciation and stock-based compensation, as well as changes in working capital.

Free cash flow has been generally positive, though fluctuating, indicating the company's ability to generate cash after capital expenditures. Capital expenditure appears relatively stable, suggesting consistent investment in property, plant, and equipment. The conversion of net income to operating cash flow varies, influenced by non-cash items such as depreciation and stock-based compensation, as well as changes in working capital.