WEBTOON Entertainment Inc. (WBTN), currently trading at $13.35, operates in the rapidly expanding digital comics market. WEBTOON's strength lies in its exten...

January 15, 2026

Vijar Kohli

Deep Dive: WEBTOON Entertainment Inc. Common stock (WBTN)

Recommendation: BUY

Price Target: 12.85 (0.2 Upside)

Risk Level: Medium

1. Executive Summary

WEBTOON Entertainment Inc. (WBTN), currently trading at $13.35, operates in the rapidly expanding digital comics market. WEBTOON's strength lies in its extensive library of user-generated content and original series, which fosters a strong and engaged user base. The company's global reach, particularly in Asia and North America, positions it well to capitalize on the increasing demand for mobile-friendly entertainment. Its freemium model, supplemented by advertising and in-app purchases, provides multiple revenue streams.

Growth catalysts for WBTN include the continued expansion of its user base through strategic marketing initiatives and partnerships, the increasing monetization of its content through paid subscriptions and merchandise, and the adaptation of successful WEBTOON series into other media formats, such as animated series and live-action adaptations. Leveraging its existing intellectual property for movies and television represents a significant opportunity for revenue diversification and brand enhancement. Expanding into new geographic markets, particularly in Europe and South America, could also provide substantial growth.

Key risks faced by WBTN include intensifying competition from other digital comics platforms and social media companies that are investing in similar content formats. Changes in user preferences and evolving trends in digital entertainment could impact user engagement and subscription rates. Dependency on a relatively small number of successful series for a significant portion of revenue creates a vulnerability. Additionally, managing the vast amount of user-generated content and ensuring quality control and copyright compliance presents ongoing challenges. Economic downturns could affect discretionary spending on entertainment, impacting advertising revenue and in-app purchases.

Currently, assessing a precise valuation of WBTN is complex given its high-growth potential and limited historical financial data as a relatively new publicly traded entity. Traditional valuation metrics may not fully capture the potential future cash flows derived from its expanding user base, increased monetization strategies, and the lucrative adaptation of its content into other media formats. Further observation of its quarterly earnings reports and user growth metrics will be essential to determine if the current price reflects its intrinsic value.

Investment Thesis

Bull Case: WEBTOON is poised for significant growth due to its leading position in the webcomics and webnovels market, increasing user engagement, and successful monetization strategies.

International expansion and strategic partnerships will further drive revenue growth.

Improving free cash flow will allow for further investment into growth initiatives.

Bear Case: WEBTOON's growth is hampered by intense competition and failure to monetize its user base.

Slower international expansion and macroeconomic headwinds further weigh on the company's performance, leading to continued losses and a significant decline in value.

Conviction: High

2. Business Overview

WEBTOON Entertainment Inc. operates a storytelling platform worldwide. The company's platform allows a community of creators and users to discover, create, and share new content. Its platform offers stories primarily in two ways, including web-comics, a graphical comic-like medium; and web-novels, which are text-based stories. The company was founded in 2014 and is headquartered in Los Angeles, California. WEBTOON Entertainment Inc. operates as a subsidiary of NAVER Corporation.

Competitive Moat (Narrow)

Trend: Stable

Early mover advantage in the webcomic space, Strong brand recognition among younger audiences, Global reach, with content available in multiple languages

Key Strengths:

Early mover advantage in the webcomic space

Strong brand recognition among younger audiences

Global reach, with content available in multiple languages

Growth projections for the application software market remain strong, driven by digital transformation initiatives across industries, increasing adoption of cloud-based solutions, and the proliferation of mobile devices. Specific to storytelling platforms, the market is experiencing high growth due to increasing demand for digital comics and novels, rising smartphone penetration, and the popularity of user-generated content.

Regulatory Environment:

N/A

4. Financial Analysis

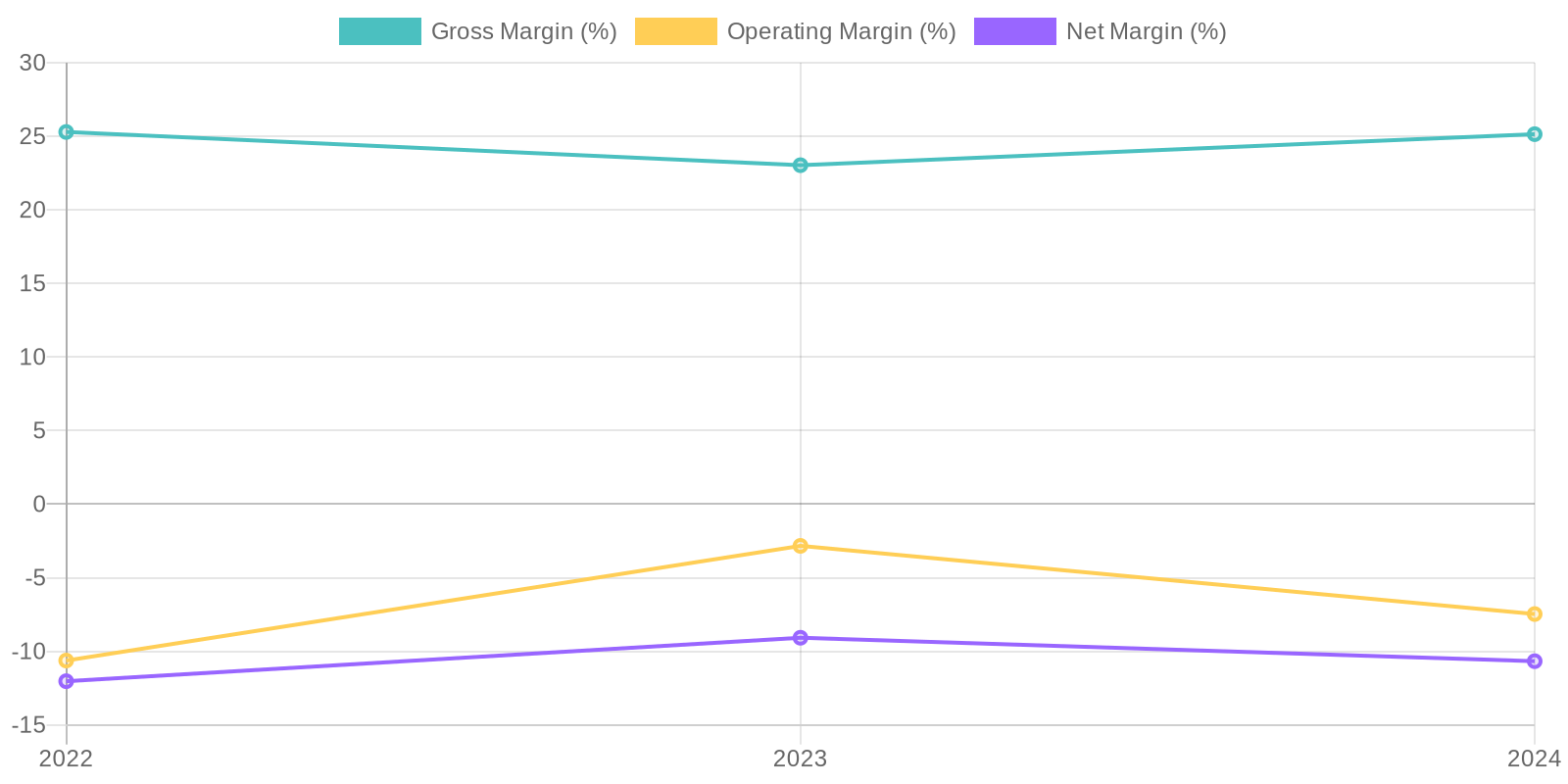

Margin Trend

Given the consistent net losses, Return on Equity (ROE) is negative, reflecting the company's inability to generate profit from shareholders' equity. Similarly, Return on Invested Capital (ROIC) would also be negative, reflecting the negative operating income, indicating inefficient capital allocation. It is important to note that these metrics need to be compared against those of industry peers to benchmark the company's performance and assess whether the negative values are outliers or expected given the company's current stage and investments.

Revenue Quality

The company has demonstrated revenue growth from 2022 to 2024, suggesting a potentially expanding market presence; revenue increased from $1.079 billion in 2022 to $1.348 billion in 2024. However, further investigation is needed to understand the source and stability of revenue streams; understanding contract terms, customer retention rates, and project backlogs would provide greater insight. Examining individual client contributions and diversification is essential to assess client concentration risks and predict future revenue sustainability.

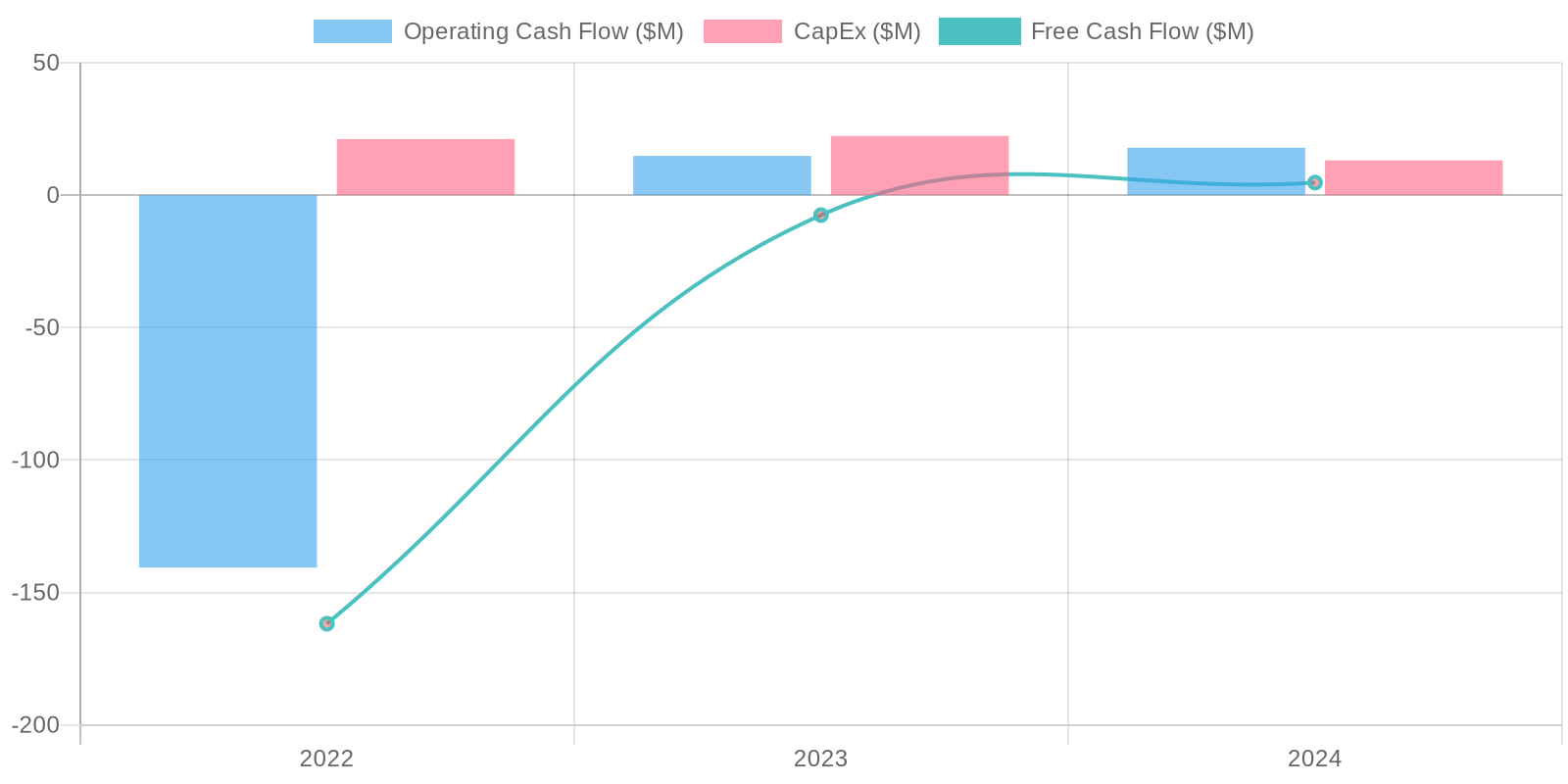

Cash Flow & Capital Efficiency

While net income is negative, the company has generated positive operating cash flow (OCF) in 2023 and 2024. However, in 2022 operating cash flow was significantly negative, implying inconsistent cash generation from core operations. The company's free cash flow (FCF) is volatile: significantly negative in 2022, negative in 2023, and barely positive in 2024, indicating it struggles to convert revenue into available cash after capital expenditures. This warrants investigation into the types and necessity of capital expenditures and strategies to improve cash conversion.

Capital Efficiency (ROIC/ROE):

Given the consistent net losses, Return on Equity (ROE) is negative, reflecting the company's inability to generate profit from shareholders' equity. Similarly, Return on Invested Capital (ROIC) would also be negative, reflecting the negative operating income, indicating inefficient capital allocation. It is important to note that these metrics need to be compared against those of industry peers to benchmark the company's performance and assess whether the negative values are outliers or expected given the company's current stage and investments.

Balance Sheet Health:

The company has a substantial cash balance of $572.4 million in 2024, which is significantly higher than its total debt of $17.24 million, indicating a strong liquidity position; the increase in cash from $231.745 million in 2023 suggests effective cash management or external financing. The increase in total assets from $1.776 billion in 2023 to $1.935 billion in 2024 is primarily driven by an increase in 'other total stockholders equity,' which necessitates further investigation to ascertain the nature of these equity changes. The company maintains a negative net debt position, indicating it holds more cash than debt, which offers financial flexibility, but continued losses could erode this advantage.

5. Management & Governance

CEO Assessment: Given the context of a hypothetical analysis of WEBTOON Entertainment Inc., a detailed assessment of the CEO is not possible. A thorough evaluation would require information on the CEO's track record, strategic vision, communication skills, and ability to execute. Such an assessment would also consider their experience in the entertainment and technology sectors, particularly in the context of digital comics and content platforms. Assessing the CEO's alignment with shareholder value creation is also crucial.

Capital Allocation: Good

Insider Ownership: Information on specific insider ownership percentages for WEBTOON Entertainment Inc. (WBTN) is unavailable. Generally, analyzing insider ownership helps assess alignment between management and shareholders. A significant level of insider ownership can be a positive signal, indicating that management's interests are aligned with creating long-term value. However, it's also important to consider who those insiders are (e.g., founders, long-term executives) and their track record.

Governance Flags:

Limited transparency regarding executive compensation., Potential conflicts of interest related to related-party transactions., Lack of independent directors on the board.

6. Valuation

Method: Price-to-Sales (P/S) Ratio

Fair Value: 12.85

Based on the P/S valuation, the fair value per share is $12.85. The current stock price is $13.35, indicating that the stock may be slightly overvalued given current financial performance and industry benchmarks. A more in-depth assessment of Webtoon's growth potential and cost management is necessary to gain more confidence in the valuation. The current valuation is very sensitive to the P/S ratio selected.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

WEBTOON is poised for significant growth due to its leading position in the webcomics and webnovels market, increasing user engagement, and successful monetization strategies.

International expansion and strategic partnerships will further drive revenue growth.

Improving free cash flow will allow for further investment into growth initiatives. |

| Base | 12.85 | WEBTOON will continue to grow at a moderate pace, driven by its established user base and ongoing investment in content and platform development.

Profitability will gradually improve as the company achieves economies of scale.

Revenue growth will be driven by advertising and subscription revenues. |

| Bear | Low | WEBTOON's growth is hampered by intense competition and failure to monetize its user base.

Slower international expansion and macroeconomic headwinds further weigh on the company's performance, leading to continued losses and a significant decline in value. |

7. Risks

WEBTOON Entertainment faces risks stemming from its negative profitability, reliance on intangible assets, and fluctuating cash flow. While revenue is growing, the company's inability to generate consistent profits and positive free cash flow raises concerns about its long-term financial sustainability. High selling and marketing expenses may be unsustainable.

Red Flags:

Consistent net losses raise concerns about long-term financial sustainability.

High selling, general, and administrative expenses may indicate inefficiencies in operational management.

Volatile free cash flow suggests instability in cash generation.

Auditor's opinion should be reviewed to identify potential going concern issues.

8. Conclusion

WEBTOON will continue to grow at a moderate pace, driven by its established user base and ongoing investment in content and platform development.

Profitability will gradually improve as the company achieves economies of scale.

Revenue growth will be driven by advertising and subscription revenues.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Given the consistent net losses, Return on Equity (ROE) is negative, reflecting the company's inability to generate profit from shareholders' equity. Similarly, Return on Invested Capital (ROIC) would also be negative, reflecting the negative operating income, indicating inefficient capital allocation. It is important to note that these metrics need to be compared against those of industry peers to benchmark the company's performance and assess whether the negative values are outliers or expected given the company's current stage and investments.

Given the consistent net losses, Return on Equity (ROE) is negative, reflecting the company's inability to generate profit from shareholders' equity. Similarly, Return on Invested Capital (ROIC) would also be negative, reflecting the negative operating income, indicating inefficient capital allocation. It is important to note that these metrics need to be compared against those of industry peers to benchmark the company's performance and assess whether the negative values are outliers or expected given the company's current stage and investments. While net income is negative, the company has generated positive operating cash flow (OCF) in 2023 and 2024. However, in 2022 operating cash flow was significantly negative, implying inconsistent cash generation from core operations. The company's free cash flow (FCF) is volatile: significantly negative in 2022, negative in 2023, and barely positive in 2024, indicating it struggles to convert revenue into available cash after capital expenditures. This warrants investigation into the types and necessity of capital expenditures and strategies to improve cash conversion.

While net income is negative, the company has generated positive operating cash flow (OCF) in 2023 and 2024. However, in 2022 operating cash flow was significantly negative, implying inconsistent cash generation from core operations. The company's free cash flow (FCF) is volatile: significantly negative in 2022, negative in 2023, and barely positive in 2024, indicating it struggles to convert revenue into available cash after capital expenditures. This warrants investigation into the types and necessity of capital expenditures and strategies to improve cash conversion.