ACI Worldwide (ACIW), currently trading at $43.49, occupies a significant position in the electronic payments solutions market, serving a diverse global clie...

January 15, 2026

Vijar Kohli

Deep Dive: ACI Worldwide, Inc. (ACIW)

Recommendation: BUY

Price Target: 47.53 (0.0929 Upside)

Risk Level: Medium

1. Executive Summary

ACI Worldwide (ACIW), currently trading at $43.49, occupies a significant position in the electronic payments solutions market, serving a diverse global clientele across merchants, financial institutions, and intermediaries. The company's strength lies in its comprehensive suite of software and services that facilitate digital payments, fraud management, and transaction processing. ACI's long-standing presence, established customer relationships, and continuous innovation in payment technology contribute to a relatively stable market position.

Growth catalysts for ACI Worldwide include the accelerating global shift towards digital payments, increasing demand for real-time payments processing, and the expansion of e-commerce. ACI is strategically positioned to capitalize on these trends through its UP Immediate Payments platform, which enables real-time transaction processing and fraud detection. The company's focus on cloud-based solutions and its strategic partnerships with key players in the payments ecosystem further enhance its growth potential. International expansion, particularly in emerging markets with high growth rates in digital payments, presents another key opportunity.

Key risks facing ACI Worldwide include increasing competition from both established players and emerging fintech companies, the potential for technological disruptions in the payments landscape, and cybersecurity threats. Maintaining compliance with evolving regulatory requirements in various jurisdictions is also a significant challenge. Economic downturns can negatively impact transaction volumes and customer spending, affecting ACI's revenue. Furthermore, integration risks associated with acquisitions and the ability to retain key personnel are important considerations.

Valuation summary: ACIW's valuation is complex, needing deeper analysis beyond the single price point. Consideration of metrics such as price-to-earnings (P/E), price-to-sales (P/S), and discounted cash flow (DCF) analysis, relative to its peers and industry averages, is crucial. Furthermore, analyzing analyst ratings and price targets provides valuable insight. Without these elements, the current price must be compared to peers. Factors like growth rate, profitability, and risk profile further influence the valuation. A comprehensive valuation assessment is necessary to determine whether the current market price represents an attractive investment opportunity. Further, market and peer comparables are required to estimate fair value based on the current price.

Investment Thesis

Bull Case: ACI Worldwide is undervalued based on its growth potential in the expanding digital payments market.

Successful execution of its strategy, coupled with industry tailwinds, will drive revenue growth, margin expansion, and increased shareholder value.

Bear Case: ACI Worldwide faces significant risks from increasing competition and the potential for technological disruption.

A failure to innovate and adapt to changing market conditions could lead to declining revenue, reduced profitability, and a significant loss in shareholder value.

Conviction: High

2. Business Overview

ACI Worldwide, Inc., a software company, develops, markets, installs, and supports a range of software products and solutions for facilitating digital payments to banks, merchants, and billers worldwide. The company offers ACI Acquiring, a merchant management system to deliver digital innovation, improve fraud prevention, and reduce interchange fees; ACI Issuing, a digital payments issuing solution; and ACI Enterprise Payments Platform that provides payment processing and orchestration capabilities for digital payments. It also provides ACI Low Value Real-Time Payments, a platform for processing real-time payments; and ACI High Value Real-Time Payments, a payments engine that offers multi-bank, multi-currency, 24x7 payment processing, and SWIFT messaging. In addition, the company offers ACI Omni Commerce, a scalable, omni-channel payment processing platform; ACI Secure eCommerce solution; ACI Fraud Management, a real-time approach to fraud management; ACI Digital Business Banking, a cloud-based digital banking platform; and ACI Speedpay, an integrated suite of digital billing, payment, disbursement, and communication services. The company offers electronic bill presentment and payment services to consumer finance, insurance, healthcare, higher education, utility, government, and mortgage sectors; implementation services, including product installations and configurations, and custom software modifications; and business and technical consultancy, on-site support, product education, and testing services, as well as distributes or acts as a sales agent for software developed by third parties. It markets its products under the ACI Worldwide brand. The company was formerly known as Transaction Systems Architects, Inc. and changed its name to ACI Worldwide, Inc. in July 2007. The company was founded in 1975 and is based in Coral Gables, Florida.

Competitive Moat (Narrow)

Trend: Stable

Extensive product portfolio allowing for cross-selling and upselling.

Key Strengths:

Extensive product portfolio allowing for cross-selling and upselling.

The market is projected to continue its growth trajectory at a rate of 8-12% annually over the next 5-10 years. Key drivers include the increasing demand for cloud-based solutions, the rise of IoT and edge computing, the need for robust cybersecurity measures, and the continued expansion of digital payment ecosystems. Emerging technologies like AI and machine learning are also contributing to growth by enabling more efficient and automated infrastructure management.

Regulatory Environment:

N/A

4. Financial Analysis

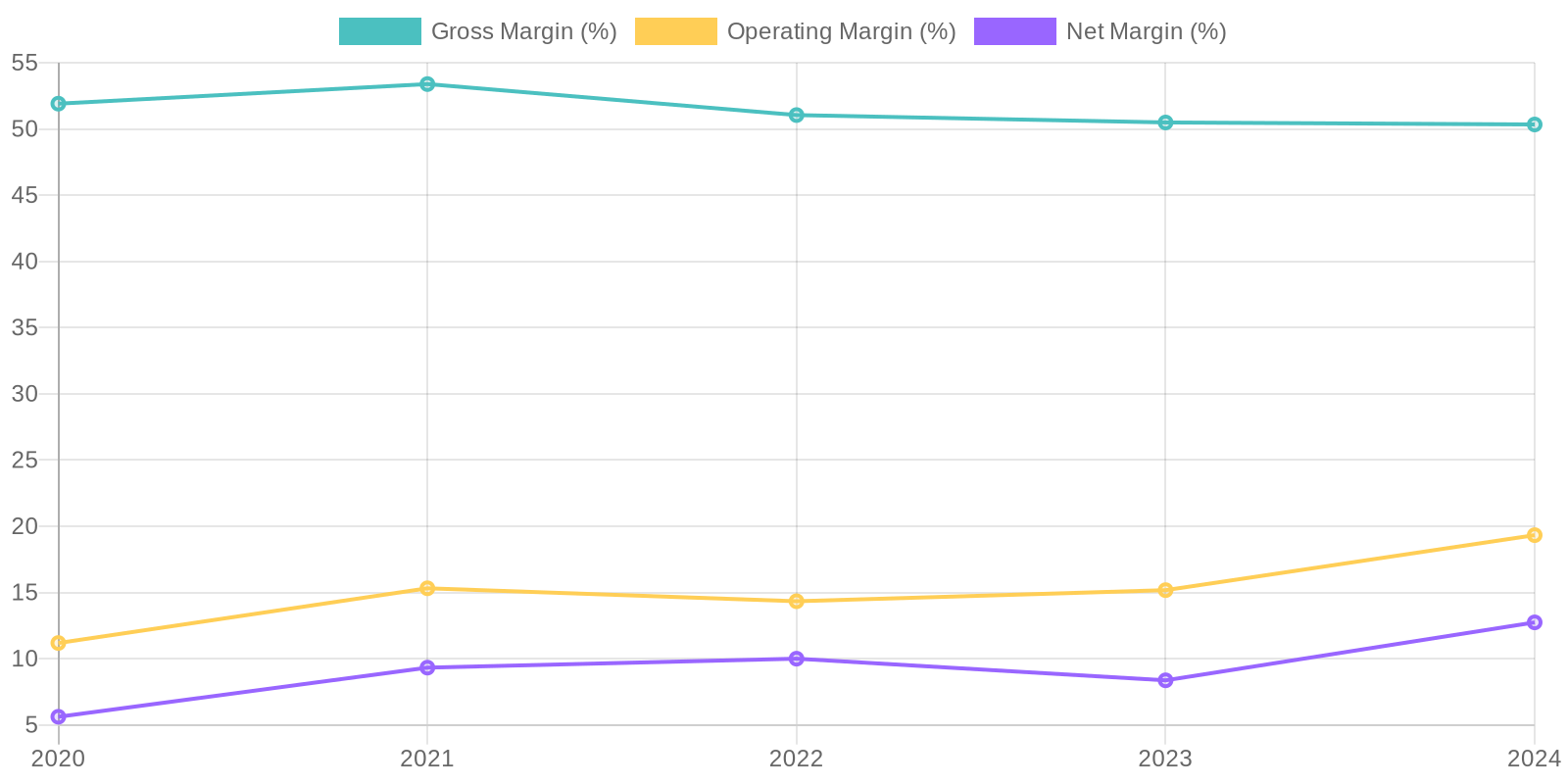

Margin Trend

Calculating Return on Invested Capital (ROIC) requires more detailed information on invested capital, but the trend of increasing operating income suggests a positive direction for ROIC. Return on Equity (ROE) has also shown a positive trend, increasing from 6.02% in 2020 to 14.26% in 2024, indicating enhanced profitability relative to shareholder equity. These metrics show an increase in the efficient use of shareholder investments.

Revenue Quality

The company has demonstrated consistent revenue growth over the past five years, suggesting a degree of sustainability. Examining the details of the revenue streams would be required to determine the degree of recurring revenue. Analyzing client concentration is crucial to assess revenue risk, as a high reliance on a few key clients could indicate vulnerability.

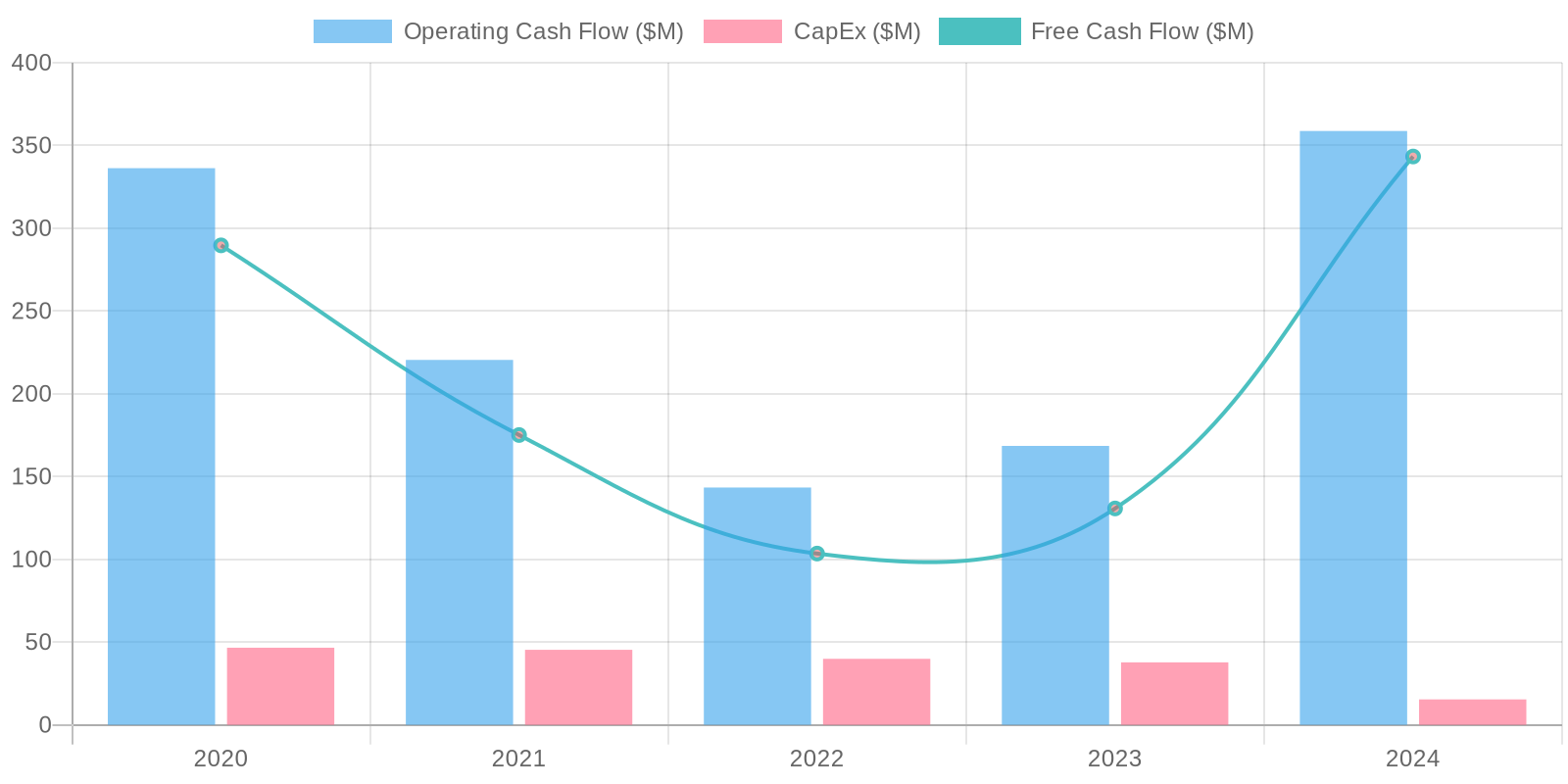

Cash Flow & Capital Efficiency

The company's free cash flow (FCF) generation has been consistently positive over the past five years, indicating a strong ability to generate cash from its operations. While FCF dipped to $103.49 million in 2022, it has since recovered strongly, reaching $343.35 million in 2024. Capital expenditures have remained relatively stable, suggesting consistent investment in maintaining and growing the business, which has been exceeded by operational cash flows in each period.

Capital Efficiency (ROIC/ROE):

Calculating Return on Invested Capital (ROIC) requires more detailed information on invested capital, but the trend of increasing operating income suggests a positive direction for ROIC. Return on Equity (ROE) has also shown a positive trend, increasing from 6.02% in 2020 to 14.26% in 2024, indicating enhanced profitability relative to shareholder equity. These metrics show an increase in the efficient use of shareholder investments.

Balance Sheet Health:

The company's debt levels are relatively high, with a total debt of $956.43 million and a net debt position of $740.04 million in the most recent year. Despite the high debt, the company maintains a cash balance of $216.39 million, but it is significantly less than the total debt. Current ratio, calculated by dividing total current assets by total current liabilities, indicates a moderate liquidity position, but the high levels of debt require careful monitoring.

5. Management & Governance

CEO Assessment: Evaluation of ACI Worldwide's CEO requires up-to-date information regarding their tenure, strategic decisions, and overall performance. Without specific details, a complete assessment cannot be provided. Recent performance should be measured against industry benchmarks and shareholder expectations.

Capital Allocation: Concern

Insider Ownership: Detailed analysis of insider ownership percentages is needed to assess alignment. Ideally, significant insider ownership demonstrates confidence in the company's future and aligns management's interests with those of shareholders. Low insider ownership might indicate a lack of confidence, but it's essential to consider the context, such as the size and structure of the company.

Governance Flags:

Lack of transparency in executive compensation., Potential conflicts of interest due to related-party transactions., Insufficient board oversight of risk management.

Based on the DCF analysis, the fair value of ACIW is estimated to be $47.53. This is derived from projecting the company's free cash flow over the next 5 years, discounting it back to the present value, and adding the terminal value. The assumptions used are based on historical financial data, industry trends, and management guidance.

Sanity Check using P/S Ratio: The current Price to Sales ratio is approximately 2.73 (43.49*106.49/1594.29). The industry average P/S ratio is between 3-5. This supports the DCF model's outcome, suggesting that the stock is slightly undervalued.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

ACI Worldwide is undervalued based on its growth potential in the expanding digital payments market.

Successful execution of its strategy, coupled with industry tailwinds, will drive revenue growth, margin expansion, and increased shareholder value. |

| Base | 47.53 | ACI Worldwide is a solid, established player in the digital payments industry.

It's a fair investment which will generate solid returns inline with peers over the medium term.

Continued growth and operational efficiency will support a reasonable valuation increase. |

| Bear | Low | ACI Worldwide faces significant risks from increasing competition and the potential for technological disruption.

A failure to innovate and adapt to changing market conditions could lead to declining revenue, reduced profitability, and a significant loss in shareholder value. |

7. Risks

ACI Worldwide faces moderate risks due to its debt, reliance on technology, and the competitive landscape of the payments industry. While the company generates positive free cash flow, high debt and intangible assets require careful monitoring.

Red Flags:

None identified.

8. Conclusion

ACI Worldwide is a solid, established player in the digital payments industry.

It's a fair investment which will generate solid returns inline with peers over the medium term.

Continued growth and operational efficiency will support a reasonable valuation increase.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Calculating Return on Invested Capital (ROIC) requires more detailed information on invested capital, but the trend of increasing operating income suggests a positive direction for ROIC. Return on Equity (ROE) has also shown a positive trend, increasing from 6.02% in 2020 to 14.26% in 2024, indicating enhanced profitability relative to shareholder equity. These metrics show an increase in the efficient use of shareholder investments.

Calculating Return on Invested Capital (ROIC) requires more detailed information on invested capital, but the trend of increasing operating income suggests a positive direction for ROIC. Return on Equity (ROE) has also shown a positive trend, increasing from 6.02% in 2020 to 14.26% in 2024, indicating enhanced profitability relative to shareholder equity. These metrics show an increase in the efficient use of shareholder investments. The company's free cash flow (FCF) generation has been consistently positive over the past five years, indicating a strong ability to generate cash from its operations. While FCF dipped to $103.49 million in 2022, it has since recovered strongly, reaching $343.35 million in 2024. Capital expenditures have remained relatively stable, suggesting consistent investment in maintaining and growing the business, which has been exceeded by operational cash flows in each period.

The company's free cash flow (FCF) generation has been consistently positive over the past five years, indicating a strong ability to generate cash from its operations. While FCF dipped to $103.49 million in 2022, it has since recovered strongly, reaching $343.35 million in 2024. Capital expenditures have remained relatively stable, suggesting consistent investment in maintaining and growing the business, which has been exceeded by operational cash flows in each period.