Digital Turbine (APPS) operates in the mobile advertising technology space, connecting mobile operators and OEMs (Original Equipment Manufacturers) with app ...

January 15, 2026

Vijar Kohli

Deep Dive: Digital Turbine, Inc. (APPS)

Recommendation: BUY

Price Target: 3.66 (-30.55 Upside)

Risk Level: Medium

1. Executive Summary

Digital Turbine (APPS) operates in the mobile advertising technology space, connecting mobile operators and OEMs (Original Equipment Manufacturers) with app developers and advertisers. The company's primary value proposition lies in its ability to facilitate app discovery and pre-installation on mobile devices, creating a more seamless user experience and driving higher app adoption rates. Currently, Digital Turbine faces a challenging market environment marked by reduced advertising budgets and evolving privacy regulations.

Growth catalysts for Digital Turbine include expanding its global footprint, particularly in emerging markets where smartphone adoption is rapidly increasing. The company's investments in innovative ad formats and its focus on enhancing the user experience can also drive growth by attracting more advertisers and improving ad engagement. Furthermore, strategic partnerships with mobile carriers and OEMs remain crucial for expanding its pre-installation reach and securing valuable distribution channels. The potential for increased adoption of 5G technology and the resulting rise in mobile data consumption could further stimulate demand for mobile advertising.

Key risks confronting Digital Turbine include intense competition from larger and more established players in the ad tech industry, such as Google and Facebook (Meta). Evolving privacy regulations, such as Apple's App Tracking Transparency (ATT), pose a significant challenge by limiting the ability to track user behavior and personalize ads effectively, impacting ad revenue. Macroeconomic headwinds and potential reductions in advertising spend by businesses due to economic uncertainty represent further risks to revenue growth. Finally, dependence on key partnerships and reliance on pre-installation agreements create concentration risk and could negatively impact performance if these relationships deteriorate or agreements are not renewed.

At a current price of $5.27, Digital Turbine's valuation reflects the aforementioned challenges and risks. While the company's growth prospects remain intact, the uncertainty surrounding privacy regulations and the competitive landscape contribute to a cautious market sentiment. A comprehensive valuation would require a discounted cash flow analysis, considering various growth scenarios, discount rates, and terminal value assumptions. Furthermore, relative valuation metrics such as price-to-sales and price-to-earnings ratios, compared to peers in the ad tech industry, can provide additional insights into the company's valuation. A complete assessment would need to consider the potential for a turnaround, given the low share price and the company's growth initiatives, alongside the significant risks involved.

Investment Thesis

Bull Case: Digital Turbine is poised for significant growth as it capitalizes on the increasing demand for mobile advertising solutions.

The company's innovative on-device media platform, combined with its strategic acquisitions, positions it as a leader in the industry.

As the company successfully integrates its acquisitions, expands its market reach, and achieves profitability, the stock price will appreciate substantially.

Bear Case: Digital Turbine faces significant challenges in the competitive mobile advertising market.

Failure to effectively integrate acquisitions, adapt to regulatory changes, and achieve profitability could lead to substantial losses for investors.

The company's high debt levels and negative free cash flow further exacerbate the risks.

Conviction: High

2. Business Overview

Digital Turbine, Inc., through its subsidiaries, operates a mobile growth platform for advertisers, publishers, carriers, and device original equipment manufacturers (OEMs). The company operates through three segments: On Device Media, In App Media AdColony, and In App Media Fyber. Its application media platform delivers mobile applications to various publishers, carriers, OEMs, and devices; and content media platform offers news, weather, sports, and other content, as well as programmatic advertising, and sponsored and editorial content media. The company also provides an end-to-end platform for brands, agencies, publishers, and application developers to deliver advertising to consumers on mobile devices; and a platform that allows mobile application developers and digital publishers to monetize their content through display, native, and video advertising. It operates in the United States, Canada, Europe, the Middle East, Africa, the Asia Pacific, China, Mexico, Central America, and South America. The company is headquartered in Austin, Texas.

Continued growth is projected, fueled by rising mobile ad spending, the increasing demand for personalized user experiences, and the expansion of mobile gaming and e-commerce. Emerging markets also present significant growth opportunities. Growth in programmatic advertising and video advertising, two areas Digital Turbine focuses on, are expected to outpace overall market growth.

Regulatory Environment:

N/A

4. Financial Analysis

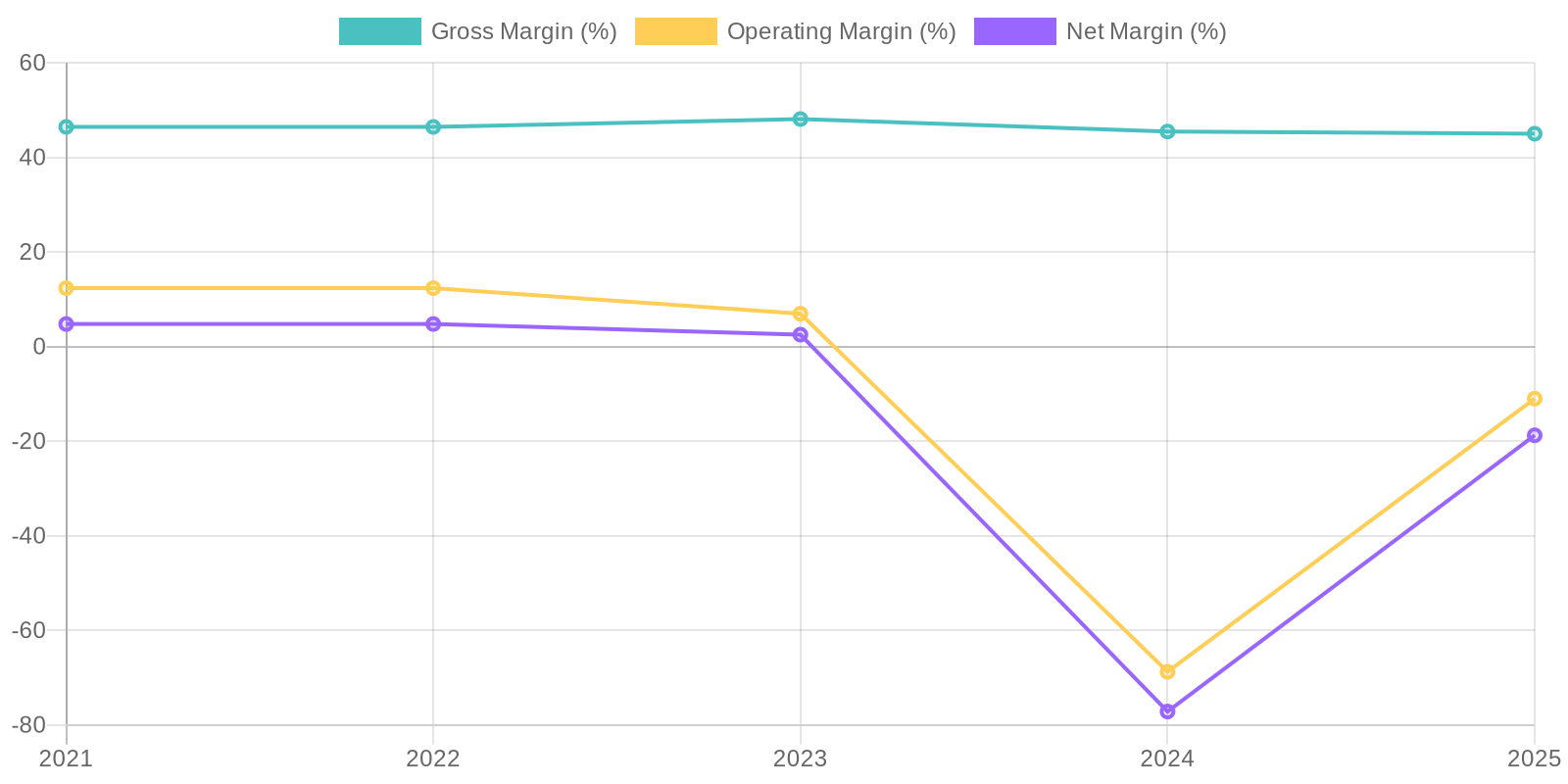

Margin Trend

Given the net losses reported in recent years, Return on Invested Capital (ROIC) and Return on Equity (ROE) are expected to be negative, reflecting the company's inability to generate profits from its capital investments. The negative ROIC suggests that the company's investments are not creating value, while the negative ROE indicates that shareholder equity is diminishing. It is critical to evaluate the efficiency of asset utilization and the effectiveness of capital allocation decisions to identify areas for improvement and restore profitability.

Revenue Quality

The company's revenue has shown volatility over the past five years, with a peak in 2022 and 2021 followed by a decline in 2025. This inconsistent revenue trend suggests potential challenges in retaining customers or adapting to market changes. It is important to investigate the client concentration and contract terms to determine if any major client losses or unfavorable contract adjustments may have contributed to the revenue decline. A detailed analysis of sales data, customer churn rates, and new customer acquisition costs could provide additional insights into the sustainability of their revenue streams.

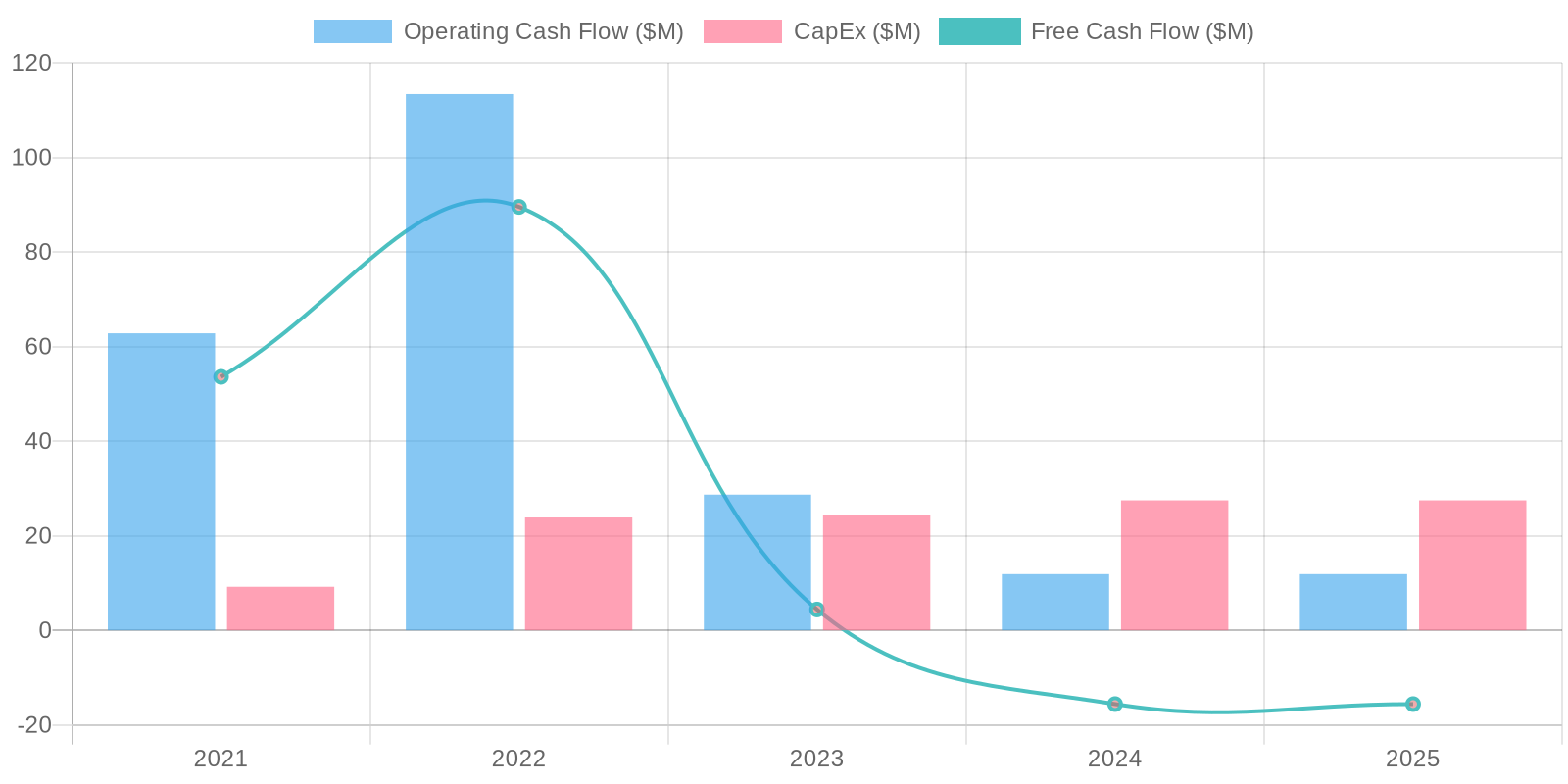

Cash Flow & Capital Efficiency

The company's Free Cash Flow (FCF) has been negative in two of the last three years, indicating that the company is not generating enough cash from its operations to cover its capital expenditures. In 2025, both operating cash flow and FCF were negative, raising concerns about the company's ability to fund its operations and investments. A detailed review of capital expenditure projects and their returns is warranted to determine whether these investments are likely to improve cash flow in the future.

Capital Efficiency (ROIC/ROE):

Given the net losses reported in recent years, Return on Invested Capital (ROIC) and Return on Equity (ROE) are expected to be negative, reflecting the company's inability to generate profits from its capital investments. The negative ROIC suggests that the company's investments are not creating value, while the negative ROE indicates that shareholder equity is diminishing. It is critical to evaluate the efficiency of asset utilization and the effectiveness of capital allocation decisions to identify areas for improvement and restore profitability.

Balance Sheet Health:

The company's debt levels are substantial, with total debt significantly exceeding its cash reserves. The debt has increased steadily from $16 million in 2021 to over $418 million in 2025, signaling a heightened financial risk. While current assets exceed current liabilities, the company's negative retained earnings and substantial long-term debt raise concerns about its long-term solvency and financial stability, indicating the need for careful debt management and strategies to improve profitability and build equity.

5. Management & Governance

CEO Assessment: Assessment of Digital Turbine's CEO is unavailable without real-time data. A comprehensive evaluation would require analyzing their strategic decisions, communication style, and track record in driving growth and innovation within the company.

Capital Allocation: Good

Insider Ownership: Detailed insider ownership data requires access to current filings. Generally, it's important to analyze the percentage of shares held by the management team and board members to gauge their alignment with shareholder interests. A significant stake can indicate strong alignment, while a low percentage might raise concerns.

Governance Flags:

Potential conflicts of interest, Executive compensation structure

6. Valuation

Method: Price-to-Sales (P/S) Ratio

Fair Value: 3.66

Calculate Market Cap: Fair Value = P/S Ratio * Revenue.

Fair Value = 3.5 * $490.51 million = $1716.79 million.

Determine shares outstanding: Market Cap / Shares Outstanding = Fair Value Per Share.

$1716.79 / 47054841.75 = 3.65

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Digital Turbine is poised for significant growth as it capitalizes on the increasing demand for mobile advertising solutions.

The company's innovative on-device media platform, combined with its strategic acquisitions, positions it as a leader in the industry.

As the company successfully integrates its acquisitions, expands its market reach, and achieves profitability, the stock price will appreciate substantially. |

| Base | 3.66 | Digital Turbine will continue to be a relevant player in the mobile advertising market, achieving moderate growth and profitability improvements.

The company's existing platform and customer relationships provide a solid foundation for future success.

However, increased competition and macroeconomic headwinds may limit the company's growth potential. |

| Bear | Low | Digital Turbine faces significant challenges in the competitive mobile advertising market.

Failure to effectively integrate acquisitions, adapt to regulatory changes, and achieve profitability could lead to substantial losses for investors.

The company's high debt levels and negative free cash flow further exacerbate the risks. |

7. Risks

Digital Turbine's high debt, negative income, and negative free cash flow, coupled with substantial goodwill, make it a risky investment. Declining profitability and aggressive acquisitions are major concerns.

Red Flags:

Consistent Net Losses

Increasing Debt Levels

Negative Free Cash Flow

Volatile Revenue Trends

High Goodwill and Intangible Assets

8. Conclusion

Digital Turbine will continue to be a relevant player in the mobile advertising market, achieving moderate growth and profitability improvements.

The company's existing platform and customer relationships provide a solid foundation for future success.

However, increased competition and macroeconomic headwinds may limit the company's growth potential.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Given the net losses reported in recent years, Return on Invested Capital (ROIC) and Return on Equity (ROE) are expected to be negative, reflecting the company's inability to generate profits from its capital investments. The negative ROIC suggests that the company's investments are not creating value, while the negative ROE indicates that shareholder equity is diminishing. It is critical to evaluate the efficiency of asset utilization and the effectiveness of capital allocation decisions to identify areas for improvement and restore profitability.

Given the net losses reported in recent years, Return on Invested Capital (ROIC) and Return on Equity (ROE) are expected to be negative, reflecting the company's inability to generate profits from its capital investments. The negative ROIC suggests that the company's investments are not creating value, while the negative ROE indicates that shareholder equity is diminishing. It is critical to evaluate the efficiency of asset utilization and the effectiveness of capital allocation decisions to identify areas for improvement and restore profitability. The company's Free Cash Flow (FCF) has been negative in two of the last three years, indicating that the company is not generating enough cash from its operations to cover its capital expenditures. In 2025, both operating cash flow and FCF were negative, raising concerns about the company's ability to fund its operations and investments. A detailed review of capital expenditure projects and their returns is warranted to determine whether these investments are likely to improve cash flow in the future.

The company's Free Cash Flow (FCF) has been negative in two of the last three years, indicating that the company is not generating enough cash from its operations to cover its capital expenditures. In 2025, both operating cash flow and FCF were negative, raising concerns about the company's ability to fund its operations and investments. A detailed review of capital expenditure projects and their returns is warranted to determine whether these investments are likely to improve cash flow in the future.