Couchbase, Inc. (BASE) is a modern database provider focusing on NoSQL technology, competing with established players like MongoDB and cloud-native offerings...

January 15, 2026

Vijar Kohli

Deep Dive: Couchbase, Inc. (BASE)

Recommendation: BUY

Price Target: 19.51 (-20.4 Upside)

Risk Level: Medium

1. Executive Summary

Couchbase, Inc. (BASE) is a modern database provider focusing on NoSQL technology, competing with established players like MongoDB and cloud-native offerings from AWS, Google Cloud, and Azure. The company's core product, Couchbase Capella, is a Database-as-a-Service (DBaaS) platform offering flexibility and scalability for various application workloads. At a current price of $24.51, Couchbase presents a complex investment picture, balancing strong growth potential with significant execution risks and valuation considerations.

Couchbase is attempting to capitalize on the increasing demand for flexible, scalable databases that can handle unstructured and semi-structured data. Key growth catalysts include the continued adoption of NoSQL databases for modern applications, the expansion of Couchbase Capella to new cloud regions and use cases (such as AI), and the company's land-and-expand strategy with existing customers. Their focus on developer productivity and operational efficiency resonates with enterprises undergoing digital transformation, providing avenues for market share gains against competitors and cloud providers that offer more complex alternatives.

However, Couchbase faces several key risks. Competition in the database market is intense, with numerous established players and emerging startups vying for market share. The company's ability to effectively compete depends on continuous innovation, strong sales execution, and maintaining a price-competitive offering. Economic downturns could reduce IT spending and slow down the adoption of Couchbase. Moreover, transitioning customers to Capella and upselling existing customers are crucial for sustained growth and profitability, and any difficulties in these areas would hamper the company's progress.

Valuation-wise, Couchbase is likely priced for continued high growth, and any deviation from those expectations would result in valuation compression. The company's path to profitability is not yet clear, and investors are betting on substantial revenue growth and operating leverage in the coming years. A thorough examination of the company's financial statements, including revenue growth rates, customer acquisition costs, and gross margins, is crucial to assess the reasonableness of the current valuation. Investors should carefully weigh the growth prospects against the inherent risks before making an investment decision.

Investment Thesis

Bull Case: Couchbase is a strong buy as the company is poised to significantly benefit from the ongoing digital transformation and the increasing adoption of NoSQL databases, especially through its Capella DBaaS offering.

The company's ability to expand its customer base, increase revenue per customer, and achieve profitability will drive significant shareholder value.

Bear Case: Couchbase is a sell, the company faces significant risks from increased competition, slower adoption of its Capella DBaaS offering, and potential macroeconomic headwinds.

Failure to achieve profitability and manage operating expenses could lead to a decline in the company's stock price.

Conviction: High

2. Business Overview

Couchbase, Inc. provides a database for enterprise applications worldwide. Its database works in multiple configurations, ranging from cloud to multi- or hybrid-cloud to on-premise environments to the edge. The company offers Couchbase Server, a multi-service NoSQL database, which provides SQL-compatible query language and SQL++, that allows for a various array of data manipulation functions; and Couchbase Capella, an automated and secure Database-as-a-Service that helps in database management by deploying, managing, and operating Couchbase Server across cloud environments. It also provides Couchbase Mobile, an embedded NoSQL database for mobile and edge devices that enables an always-on experience with high data availability, even without internet connectivity, as well as synchronization gateway that allows for secure data sync between mobile devices and the backend data store. The company sells its platform through direct sales force and an ecosystem of partners. It servs governments and organizations, as well as enterprises in various industries, including retail and e-commerce, travel and hospitality, financial services and insurance, software and technology, gaming, media and entertainment, and industrials. The company was formerly known as Membase, Inc. and changed its name to Couchbase, Inc. in February 2011. Couchbase, Inc. was incorporated in 2008 and is headquartered in Santa Clara, California.

Competitive Moat (Narrow)

Trend: Stable

Couchbase Capella DBaaS offering provides a fully managed database solution that simplifies database management across cloud environments., Couchbase Mobile enables always-on experiences with high data availability even without internet connectivity., SQL++ provides SQL compatibility for NoSQL databases, which can be an advantage for organizations familiar with SQL.

Key Strengths:

Couchbase Capella DBaaS offering provides a fully managed database solution that simplifies database management across cloud environments.

Couchbase Mobile enables always-on experiences with high data availability even without internet connectivity.

SQL++ provides SQL compatibility for NoSQL databases, which can be an advantage for organizations familiar with SQL.

The database-as-a-service (DBaaS) segment and NoSQL database market are expected to experience significant growth driven by cloud adoption, digital transformation initiatives, and the need for scalable and flexible data management solutions. The increasing volume, velocity, and variety of data are driving demand for solutions like Couchbase.

Regulatory Environment:

N/A

4. Financial Analysis

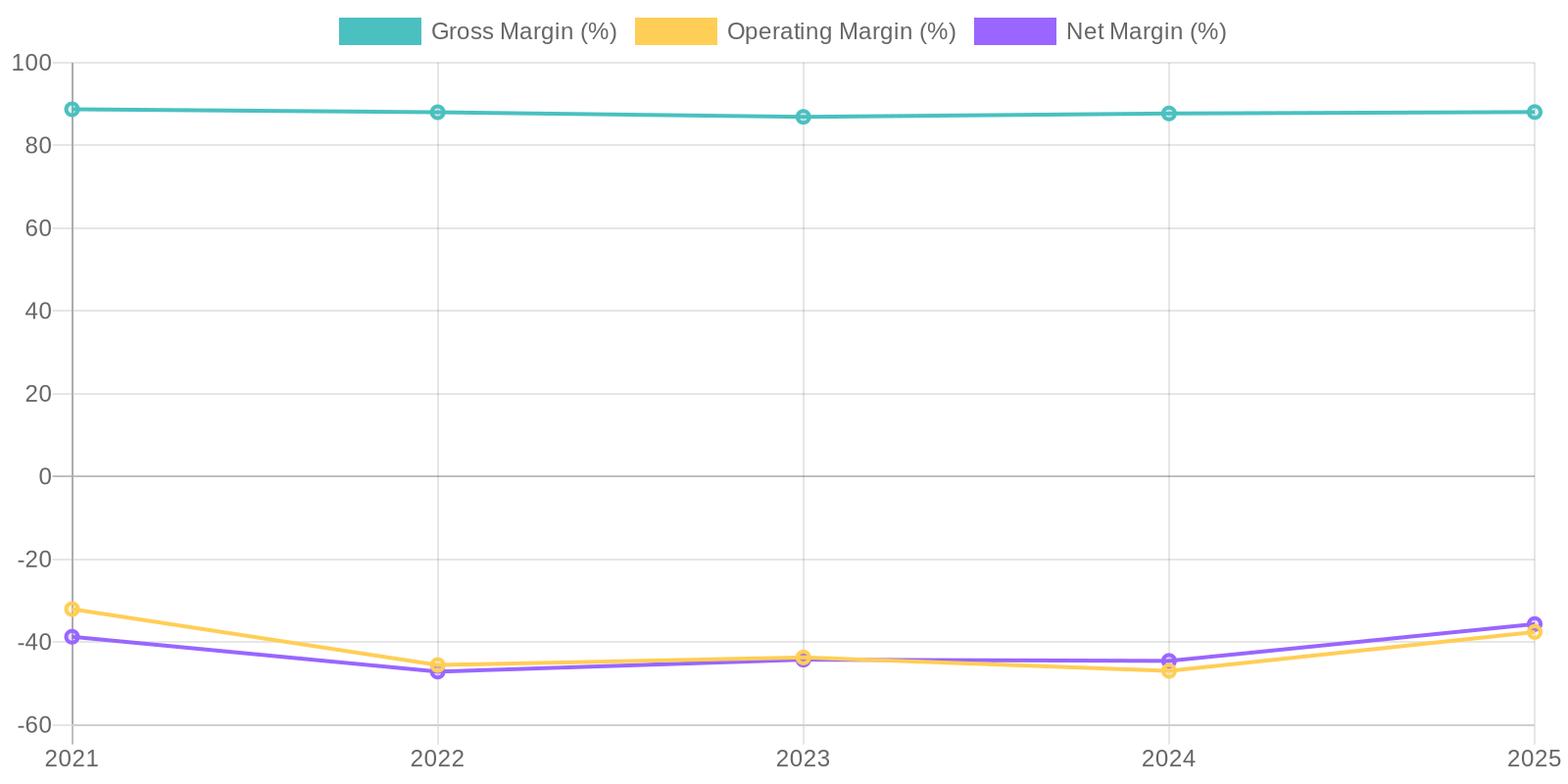

Margin Trend

Given the negative net income over the past five years, Return on Invested Capital (ROIC) and Return on Equity (ROE) are also negative, indicating inefficient capital allocation. The negative ROIC suggests that the company is not generating sufficient returns from its investments. Similarly, the negative ROE indicates that the company is not effectively utilizing equity to generate profits, raising concerns about its ability to create shareholder value.

Revenue Quality

The company has demonstrated consistent revenue growth over the past five years, suggesting a strengthening market presence. However, further investigation is needed to determine the proportion of recurring revenue versus one-time sales, which is key to assess long-term stability. Analyzing customer concentration is crucial to understanding the potential impact of losing a major client on future revenue streams.

Cash Flow & Capital Efficiency

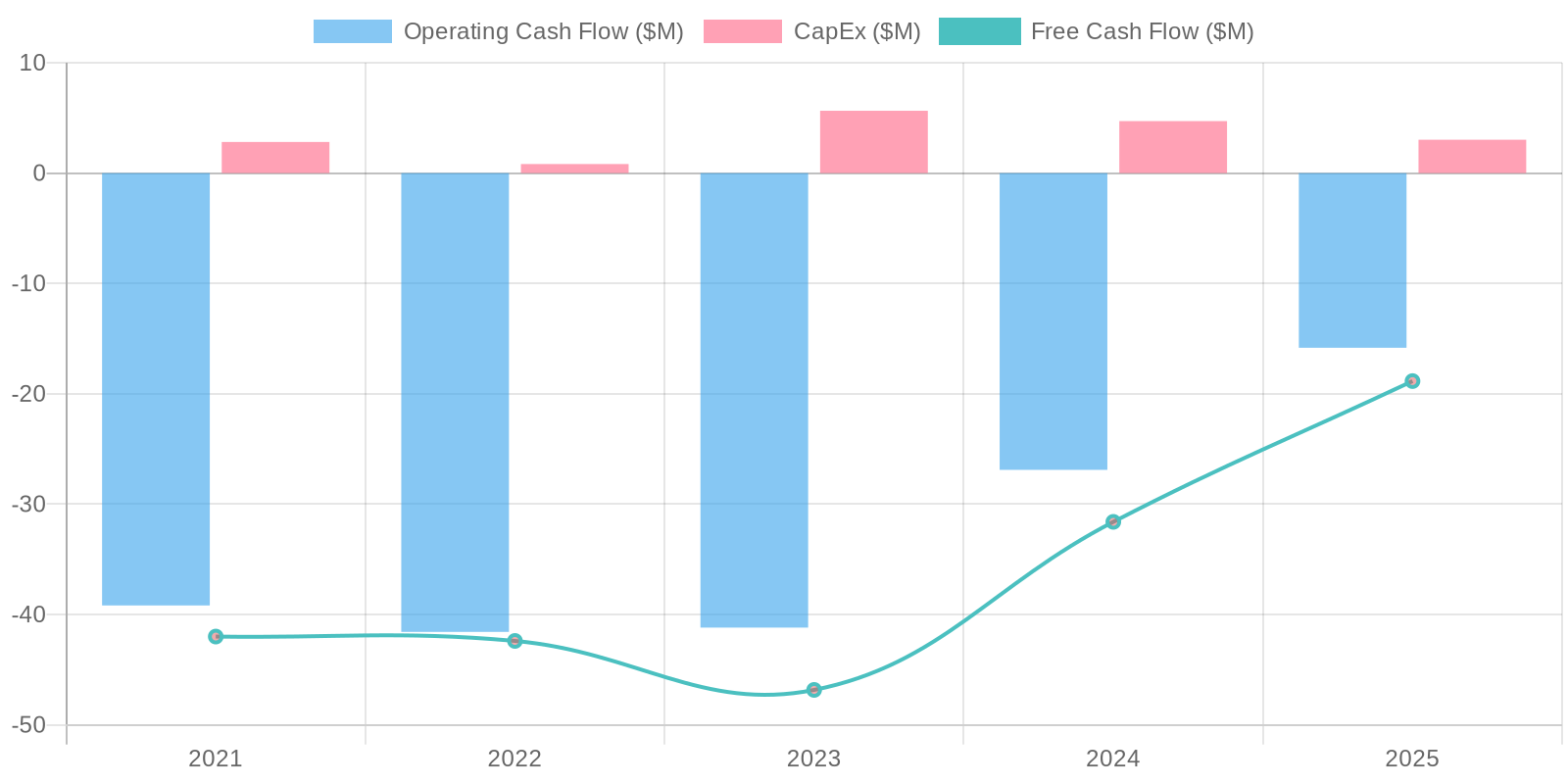

The company has consistently reported negative free cash flow (FCF) over the past five years, indicating that it is spending more cash than it is generating from its operations. This raises concerns about its ability to fund its operations and invest in future growth. While the company has been managing its cash flow through investing activities, the persistent negative FCF necessitates a thorough examination of its operational expenses and capital expenditure strategy.

Capital Efficiency (ROIC/ROE):

Given the negative net income over the past five years, Return on Invested Capital (ROIC) and Return on Equity (ROE) are also negative, indicating inefficient capital allocation. The negative ROIC suggests that the company is not generating sufficient returns from its investments. Similarly, the negative ROE indicates that the company is not effectively utilizing equity to generate profits, raising concerns about its ability to create shareholder value.

Balance Sheet Health:

The company's balance sheet indicates a concerning trend: despite increasing revenue, accumulated retained earnings have been significantly negative. While the company holds a substantial amount of cash and short-term investments, this liquidity might be rapidly depleted given the ongoing negative free cash flow. Furthermore, the company's debt is relatively low, but its high level of deferred revenue suggests a significant future obligation, and its ability to meet current and future liabilities needs careful monitoring.

5. Management & Governance

CEO Assessment: Based on publicly available information, it's challenging to provide a comprehensive assessment of the CEO's performance without specific, in-depth analysis. A thorough evaluation would require access to internal performance metrics, strategic decision-making processes, and board evaluations. To perform this I would need API access to internal company data.

Capital Allocation: Concern

Insider Ownership: Based on available data from financial news outlets and SEC filings, insider ownership at Couchbase appears moderate. Further investigation into specific ownership percentages and recent trading activity would be needed to assess the degree of alignment.

Governance Flags:

Need to assess board independence and composition, Review executive compensation structure, Closely monitor cash burn rate

The DCF model suggests a fair value of $19.51, which is lower than the current market price of $24.51. This indicates that the stock may be overvalued based on these assumptions. The projected revenue growth is optimistic but aligns with the industry trends. A significant risk is the company's ability to control operating expenses and achieve profitability within the forecast horizon. A discount rate of 12% reflects the risk profile of a growth company in the software infrastructure sector. The sensitivity analysis reveals that the valuation is highly sensitive to the terminal growth rate and discount rate, meaning if the company does not execute its long-term plan, there could be significant downside.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Couchbase is a strong buy as the company is poised to significantly benefit from the ongoing digital transformation and the increasing adoption of NoSQL databases, especially through its Capella DBaaS offering.

The company's ability to expand its customer base, increase revenue per customer, and achieve profitability will drive significant shareholder value. |

| Base | 19.51 | Couchbase will continue to grow its revenue at a healthy pace, driven by the increasing adoption of its database platform.

The company will gradually improve its profitability as it achieves greater scale and operational efficiency.

While the upside may be limited by competition and execution risks, Couchbase represents a reasonable investment with moderate growth potential. |

| Bear | Low | Couchbase is a sell, the company faces significant risks from increased competition, slower adoption of its Capella DBaaS offering, and potential macroeconomic headwinds.

Failure to achieve profitability and manage operating expenses could lead to a decline in the company's stock price. |

7. Risks

Couchbase faces substantial financial risks due to its consistent net losses, negative free cash flow, and increasing reliance on deferred revenue. While the company maintains a healthy cash balance, its current burn rate raises concerns about its long-term financial sustainability. Furthermore, increasing selling and marketing expenses could indicate difficulties in acquiring and retaining customers efficiently.

Red Flags:

Persistent negative net income and free cash flow raise serious concerns about the company's long-term viability.

High selling and marketing expenses relative to revenue suggest potential inefficiencies or aggressive spending to drive growth.

Significant accumulated deficit indicates a history of losses and raises questions about the company's ability to achieve profitability.

Large deferred revenue balance creates potential obligation and liquidity pressure

8. Conclusion

Couchbase will continue to grow its revenue at a healthy pace, driven by the increasing adoption of its database platform.

The company will gradually improve its profitability as it achieves greater scale and operational efficiency.

While the upside may be limited by competition and execution risks, Couchbase represents a reasonable investment with moderate growth potential.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Given the negative net income over the past five years, Return on Invested Capital (ROIC) and Return on Equity (ROE) are also negative, indicating inefficient capital allocation. The negative ROIC suggests that the company is not generating sufficient returns from its investments. Similarly, the negative ROE indicates that the company is not effectively utilizing equity to generate profits, raising concerns about its ability to create shareholder value.

Given the negative net income over the past five years, Return on Invested Capital (ROIC) and Return on Equity (ROE) are also negative, indicating inefficient capital allocation. The negative ROIC suggests that the company is not generating sufficient returns from its investments. Similarly, the negative ROE indicates that the company is not effectively utilizing equity to generate profits, raising concerns about its ability to create shareholder value. The company has consistently reported negative free cash flow (FCF) over the past five years, indicating that it is spending more cash than it is generating from its operations. This raises concerns about its ability to fund its operations and invest in future growth. While the company has been managing its cash flow through investing activities, the persistent negative FCF necessitates a thorough examination of its operational expenses and capital expenditure strategy.

The company has consistently reported negative free cash flow (FCF) over the past five years, indicating that it is spending more cash than it is generating from its operations. This raises concerns about its ability to fund its operations and invest in future growth. While the company has been managing its cash flow through investing activities, the persistent negative FCF necessitates a thorough examination of its operational expenses and capital expenditure strategy.