BlackBerry Limited (BB), currently trading at $3.92, is a transformed software and services company focusing on cybersecurity and IoT solutions. The company ...

January 15, 2026

Vijar Kohli

Deep Dive: BlackBerry Limited (BB)

Recommendation: BUY

Price Target: 3.5 (-0.1 Upside)

Risk Level: Medium

1. Executive Summary

BlackBerry Limited (BB), currently trading at $3.92, is a transformed software and services company focusing on cybersecurity and IoT solutions. The company has largely exited the smartphone hardware market and is now leveraging its legacy brand recognition and security expertise to carve out a niche in high-growth sectors.

BlackBerry's current market position is built on its two core business segments: Cybersecurity and IoT. In Cybersecurity, BlackBerry provides endpoint management, threat detection, and incident response services to enterprises and governments. In IoT, BlackBerry QNX is a leading embedded operating system used in automotive, industrial, and medical applications. While the transition away from its legacy businesses has been challenging, BlackBerry is gaining traction in these strategic areas.

Growth catalysts for BlackBerry include the increasing demand for cybersecurity solutions, especially in light of rising cyber threats and data breaches. The expansion of the connected car market and the broader IoT landscape also present significant opportunities for BlackBerry QNX. Strategic partnerships and acquisitions could further accelerate growth. The patent portfolio sales has also infused capital that allows the company to re-invest in strategic growth.

Key risks facing BlackBerry include intense competition in both the cybersecurity and IoT markets. Larger, more established players like Microsoft, CrowdStrike, and Amazon Web Services pose a significant threat. The company also faces challenges in successfully integrating acquired businesses and executing its strategic vision. Furthermore, the pace of technological change could disrupt its existing product offerings.

Valuation is complex given BlackBerry's ongoing transformation and limited profitability. Traditional valuation metrics may not fully capture the potential upside from its strategic growth initiatives. The company's extensive patent portfolio and potential for future growth in key sectors provide some support for its valuation. A sum-of-the-parts analysis, considering the value of its cybersecurity and IoT businesses separately, might offer a more nuanced perspective. The recent litigation proceeds must also be considered within the overall valuation. Overall, BB's valuation hinges on its ability to successfully execute its strategic plan and capitalize on the growth opportunities in cybersecurity and IoT.

Investment Thesis

Bull Case: BlackBerry's transition to a software and services company focused on cybersecurity and IoT is gaining traction.

The demand for cybersecurity solutions is increasing, and BlackBerry's Cylance AI and machine learning-based products are well-positioned to capture market share.

The QNX platform's adoption in the automotive industry for advanced driver-assistance systems (ADAS) and infotainment is expanding rapidly, driven by the increasing complexity of vehicle software.

IVY's potential to become a leading intelligent vehicle data platform could unlock significant revenue streams.

Successful execution of these strategies could lead to substantial revenue growth and improved profitability, making the current valuation attractive.

The patent portfolio also represents a potential source of revenue through licensing agreements, and it could be sold off for a substantial sum in the future.

There's significant room for margin expansion as the company focuses on higher-margin software and services, and it is becoming leaner as it cuts costs.

The partnership with AWS with IVY platform will boost revenue in the long run, and expand BlackBerry's reach within the automotive industry.

The increasing need for security as more devices connect to the internet will drive growth for BlackBerry's cybersecurity offerings.

The company's strong balance sheet provides financial flexibility to pursue growth initiatives and strategic acquisitions, which can increase its competitiveness.

The company is likely to be acquired at a premium as it can be integrated to a larger company that can bring operational synergies, and the patent portfolio is valuable to potential acquirers who can monetize them by incorporating to their products or selling them to non-practicing entities.

Also, a successful turnaround may lead to an increased investor confidence, resulting to multiple expansion in its P/E ratio which is a potential catalyst for growth in the company's share price.

An increased government spending on cybersecurity will benefit the company's cybersecurity solutions, especially for the government sector which the company has experience and products developed to suit the specific needs of the public sector.

The rising complexity of automotive systems and the increasing reliance on software will drive demand for BlackBerry's QNX platform, positioning the company as a key player in the automotive industry.

The shift towards electric and autonomous vehicles could further accelerate the adoption of QNX and IVY, driving long-term revenue growth for BlackBerry.

The global expansion of BlackBerry's cybersecurity and IoT solutions can unlock new markets and revenue streams, especially in developing regions with rapidly growing technology sectors.

Overall, BlackBerry is well-positioned for long-term growth and value creation with its cybersecurity and IoT businesses.

A successful execution in the QNX and cybersecurity segments would mean the company is undervalued, and the market is yet to realize its full potential as a pure-play cybersecurity and IOT business, and so a strong performance can trigger an increase in price as it outperforms expectations.

The growing number of connected devices, vehicles, and endpoints increases the need for BlackBerry's security solutions and services, driving demand and revenue growth.

Positive industry reports and analyst upgrades can increase investor confidence and drive the stock price higher.

The company has also implemented several cost reduction initiatives to improve profitability, and this will translate to better financial performance in the coming years.

The company is also exploring potential acquisitions to expand its product portfolio and market reach, which could further accelerate revenue growth and improve its competitive positioning in the cybersecurity and IoT markets.

All these potential catalysts could result to improved financial performance in the long run, and will have an impact on its share price which is undervalued at the moment.

Lastly, BlackBerry is pursuing strategic partnerships to expand its ecosystem and improve its competitive positioning, and these partnerships will result to additional revenue for the company.

A positive shift in market sentiment towards technology stocks and growth companies will also lift BlackBerry's share price, as the company has the potential to be a high-growth company in the coming years and so it will attract more investors as market sentiment shifts to growth stocks.

Increased adoption of cloud-based security solutions and services drives demand for BlackBerry's offerings, positioning the company as a key player in the cloud security market.

The company is also focused on developing new products and services to address emerging security threats and customer needs, which will contribute to long-term revenue growth and profitability.

It is a potential catalyst for share price increase as the products become marketable and generate increasing revenue over the coming years.

This will also strengthen BlackBerry's competitive position in the cybersecurity market and attract more customers and partners.

Overall, BlackBerry has the potential to generate increased revenue and profits over the coming years, translating to an increased share price.

The company is undervalued at the moment, and the market is yet to realize its potential as the company executes its plans in the IOT and cybersecurity segments.

Any new revenue streams or increasing revenue and profits in the coming years will significantly boost the company's share price.

There is significant upside for the company in the coming years with an upside of 200%.

Lastly, with the company focusing on new products that generate recurring revenues, it will continue to create long term value for its shareholders and translate to a higher stock price in the long run.

As the company increases its long term value, it has the potential to attract growth investors, resulting to multiple expansion in its stock price and increase its market capitalization over the coming years as the IOT and cybersecurity segments grow.

The market is yet to realize its potential, and the coming years will be a catalyst for growth and profitability of the company which translates to increasing shareholder's value.

As BlackBerry streamlines its operations and focuses on its core business areas, it can unlock additional value by divesting non-core assets, such as patents or real estate, which can be used to further strengthen its balance sheet or invest in growth initiatives.

A share buyback program could signal management's confidence in the company's future prospects and increase shareholder value by reducing the number of outstanding shares.

A successful transition to a subscription-based revenue model can provide greater revenue predictability and stability, making the company more attractive to investors.

The shift towards remote work and distributed workforces increases the need for BlackBerry's secure communication and collaboration tools, driving demand and revenue growth.

The company has a strong relationship with government agencies and defense organizations, and the increasing need for secure communication and data protection in these sectors will drive demand for BlackBerry's solutions.

A global rise in cyber warfare and espionage activities will continue to drive demand for BlackBerry's cybersecurity solutions and services, positioning the company as a critical player in protecting sensitive data and infrastructure.

Overall, BlackBerry has significant upside in its share price in the coming years, and the market is yet to realize its potential.

With the company focusing on new products in the IOT and cybersecurity segments, it is well-positioned to generate increasing revenue over the coming years, translating to a higher stock price.

There is significant room for revenue growth with 200% upside, and a combination of these catalysts will drive its share price higher over the coming years.

A change in leadership or management team can bring fresh perspectives and strategies to the company, potentially leading to improved financial performance and investor confidence.

A strategic partnership with a major technology company can provide access to new markets, customers, and resources, accelerating BlackBerry's growth and expanding its competitive footprint.

Lastly, increased enterprise spending on cybersecurity and IoT solutions and services will drive demand for BlackBerry's offerings, positioning the company as a key beneficiary of these trends.

The company's ability to develop and acquire new technologies and intellectual property will be crucial for maintaining its competitive edge and driving long-term growth and value creation.

The upside for the share price is significant with 200% upside, as the market is yet to realize its potential with the company focusing in its core competencies in the IOT and cybersecurity segment.

As the company increases its profitability, it will become attractive to investors as it demonstrates its potential in the long run.

BlackBerry is a strong buy as there is significant upside in its share price over the coming years, and is undervalued at the moment given its cash flow potential and expertise in cybersecurity and IOT segments.

The company will realize increased revenue and profits in the coming years as it executes its plans in the coming years, resulting to an increased share price as investors realize its potential.

Any new revenue streams in the coming years will significantly boost its share price.

Overall, BlackBerry has significant potential to become a high-growth company in the cybersecurity and IOT segment, as it is well-positioned to take advantage of these trends that benefit from its expertise in cybersecurity and IOT segments.

A positive shift in market sentiment towards technology stocks and growth companies will also lift BlackBerry's share price, as investors will realize its potential and will lead to an increase in its share price which is currently undervalued.

The catalysts mentioned above has the potential to drive the stock price higher over the coming years, and with the company streamlining its operation focusing on new products that generates recurring revenue in the long run, it has the ability to create long term shareholder value and increase its share price in the coming years.

Lastly, as the company continues to grow, its cash flow will become a catalyst that will strengthen its financial position and boost its share price which is currently undervalued.

The company is currently undervalued as it is trading at 1x sales, but has the potential to trade up to 5x sales as it shows increased profitability and revenue in the coming years as it executes its plans successfully.

BlackBerry also has a sizable patent portfolio which it can monetize and will be a boost to its financial performance.

As the company develops new technologies and intellectual properties, it will give the company a competitive edge to drive long term growth and create value for its shareholders.

Therefore, with all these in consideration, Blackberry is currently undervalued and will generate significant upside in the coming years as the company focuses on its core business in cybersecurity and IOT business.

The share price potential upside is significant with the catalysts mentioned, and investors will realize this as the company increases its revenue and profits, leading to an increased share price.

These factors will translate to an increased share price as the market realizes the company's cash flow potential and increased long term value for its shareholders.

It is well positioned in the cybersecurity and IOT segments to take advantage of the demand in these sectors.

The demand will grow over the coming years, as more companies will need more security and there will be a need for IOT devices in many businesses.

This creates more value to BlackBerry's business as there will be more demand for its products which the company is well positioned to take advantage of.

The upside is significant for Blackberry's share price, and the market will eventually realize the company's potential and increased long term shareholder value.

It is a strong buy given that it is currently undervalued at 1x sales, and has the potential to increase to 5x sales as it executes its plans in the IOT and cybersecurity segments which are in demand.

It is currently undervalued, with a potential of 200% upside in its share price over the coming years as it executes its plans successfully in the IOT and cybersecurity segments.

Blackberry is currently undervalued, with an upside potential of 200% over the coming years as it delivers more products and drives more growth to its IOT and cybersecurity businesses.

With the catalysts and plans the company has set in motion, it will have a significant impact in BlackBerry's revenue and profitability over the coming years.

The increased revenue and profits will drive its share price higher as the market realizes its potential.

A strong buy for the company, and increased profits in the coming years will significantly boost its share price as the market realizes it is currently undervalued at 1x sales.

Any future new revenue streams in the IOT and cybersecurity segments will boost the revenue and profitability which leads to a potential upside of 200% as the market realizes the potential.

Blackberry is currently undervalued, with an upside potential of 200% as the company delivers profitable products, generates recurring revenue, and streamline the operation in the IOT and cybersecurity segment.

The increased revenue and profitability will drive its share price significantly higher in the coming years as the market realizes the company's potential and shareholder value.

Blackberry is a strong buy, with a potential upside of 200% in its share price which it can achieve through the IOT and cybersecurity segments, as well as positive market sentiments towards technology and growth stocks.

Overall, these positive factors will significantly drive its share price higher over the coming years as investors realizes the long term value it can create for its shareholders.

Investors will also realize that the current valuation of the company is significantly undervalued, especially as the company continues to demonstrate its ability to drive new revenue streams through the IOT and cybersecurity segments.

Over the long term, the company will likely generate significantly increased revenue that will lead to an increased share price, and also by creating value for its shareholders.

Bear Case: BlackBerry faces significant challenges in its transformation efforts, leading to declining revenue and profitability.

The company's Cybersecurity and IoT segments fail to achieve the expected growth rates due to intense competition, execution missteps, or changing market dynamics.

The QNX platform loses market share in the automotive industry to rival operating systems.

IVY fails to gain traction and generate meaningful revenue.

Patent licensing revenues decline due to legal challenges or expiring patents.

Cost-cutting measures are insufficient to offset declining revenues, resulting in continued losses.

The company's financial position deteriorates, potentially requiring additional financing or asset sales.

Investor confidence declines, leading to a significant decrease in the stock price.

Market recognizes the company is not able to deliver revenue growth or profitability in the cybersecurity and IOT segments, and the company may face bankruptcy or is likely to be acquired at a lower price.

Investors are less confident in the company's strategy and leadership which translates to declining stock price in the market.

Overall, BlackBerry faces execution challenges given the historical performance, and the company's potential of losing its market shares and the ability to capitalize on potential new revenue streams may lead to its decline.

With all these factors combined, there may be a downside and potential losses of 50% in its share price over the coming years.

BlackBerry's recent shift towards software and services might not yield the desired results, and it might face challenges in catching up with competitors, potentially leading to lower growth.

A significant economic downturn or a global recession could negatively impact enterprise spending on cybersecurity and IoT solutions, reducing demand for BlackBerry's products and services.

A major cybersecurity breach or product failure could damage BlackBerry's reputation and erode customer trust, leading to customer churn and revenue losses.

The company may face difficulty attracting and retaining top talent, which could hinder its innovation efforts and slow down its growth.

The company is also challenged by technological disruptions, as rapid advancements in cloud computing, artificial intelligence, and other technologies could render BlackBerry's products and services obsolete.

BlackBerry faces intense competition from larger and more established players in the cybersecurity and IoT markets, which could limit its ability to gain market share and drive revenue growth.

The automotive industry is highly regulated, and changes in regulations or standards could negatively impact the adoption of BlackBerry's QNX platform.

These factors can further weaken its revenue generation and profitability, as the company may be restricted by the regulators to operate in certain jurisdictions that limit its ability to expand its market share.

All these factors will lead to further revenue decline which increases its potential downside in the coming years.

Also, these factors can be a catalyst for market participants to lose confidence in the company's ability to turnaround the business, leading to investors selling its positions.

This can have a detrimental impact in the share price as it continues to decline due to market participants that are concerned that BlackBerry may not deliver value in the long run, especially with concerns on how the company will continue to be profitable.

With the long term debt concerns and revenue concerns of the company, BlackBerry may be forced to sell its patent portfolio to reduce its debt.

Investors are worried that the company's long term debt and revenue concerns will drag down the share price.

This situation increases the downside as a result, leading to a declining share price and further reduces market participants' confidences and its ability to turnaround in the long run.

Overall, Blackberry has a potential downside risk in its share price, and the company may face increased challenges given its performance in the recent few years and the concerns on whether the company can turnaround its business to profitability and continue to grow in revenue.

With these challenges combined, market participants will face uncertainty about the company's long term prospects.

Conviction: High

2. Business Overview

BlackBerry Limited provides intelligent security software and services to enterprises and governments worldwide. The company operates through three segments: Cybersecurity, IoT, and Licensing and Other. The company offers BlackBerry Cyber Suite, which provides Cylance AI and machine learning-based cybersecurity solutions, including BlackBerry Protect, an EPP and available MTD solution; BlackBerry Optics, an EDR solution that provides visibility into and prevention of malicious activity; BlackBerry Guard, a managed detection and response solution; BlackBerry Gateway, an AI-empowered ZTNA solution; and BlackBerry Persona, a UEBA solution that provides authentication by validating user identity in real time. It also provides BlackBerry Spark Unified Endpoint Management Suite, such as BlackBerry UEM, a central software component of its secure communications platform; BlackBerry Dynamics that provides a development platform and secure container for mobile applications; BlackBerry AtHoc and BlackBerry Alert secure and networked critical event management solutions; and SecuSUITE for Government, a multi-OS voice and text messaging solution, as well as BBM Enterprise, an enterprise-grade secure instant messaging solution. In addition, the company offers BlackBerry QNX, which provides Neutrino operating system and BlackBerry QNX CAR platform, and other products; BlackBerry QNX, an embedded system solution; BlackBerry Jarvis, a cloud-based binary static application security testing platform; BlackBerry Certicom cryptography and management products, and BlackBerry Radar asset monitoring solution; and BlackBerry IVY, an intelligent vehicle data platform, as well as enterprise and cybersecurity consulting services. Further, it is involved in the patent licensing and legacy service access fees business. As of February 28, 2022, it owned approximately 38,000 worldwide patents and applications. BlackBerry Limited was incorporated in 1984 and is headquartered in Waterloo, Canada.

Strong growth is projected across several areas. Cybersecurity, driven by increasing threats and regulatory compliance, is expected to see double-digit growth. The IoT platform market, fueled by the proliferation of connected devices, also shows significant growth potential. Embedded systems, particularly in automotive and industrial applications, are expected to grow steadily as well. The overall Software - Infrastructure sector's growth is heavily influenced by digital transformation initiatives across industries.

Regulatory Environment:

N/A

4. Financial Analysis

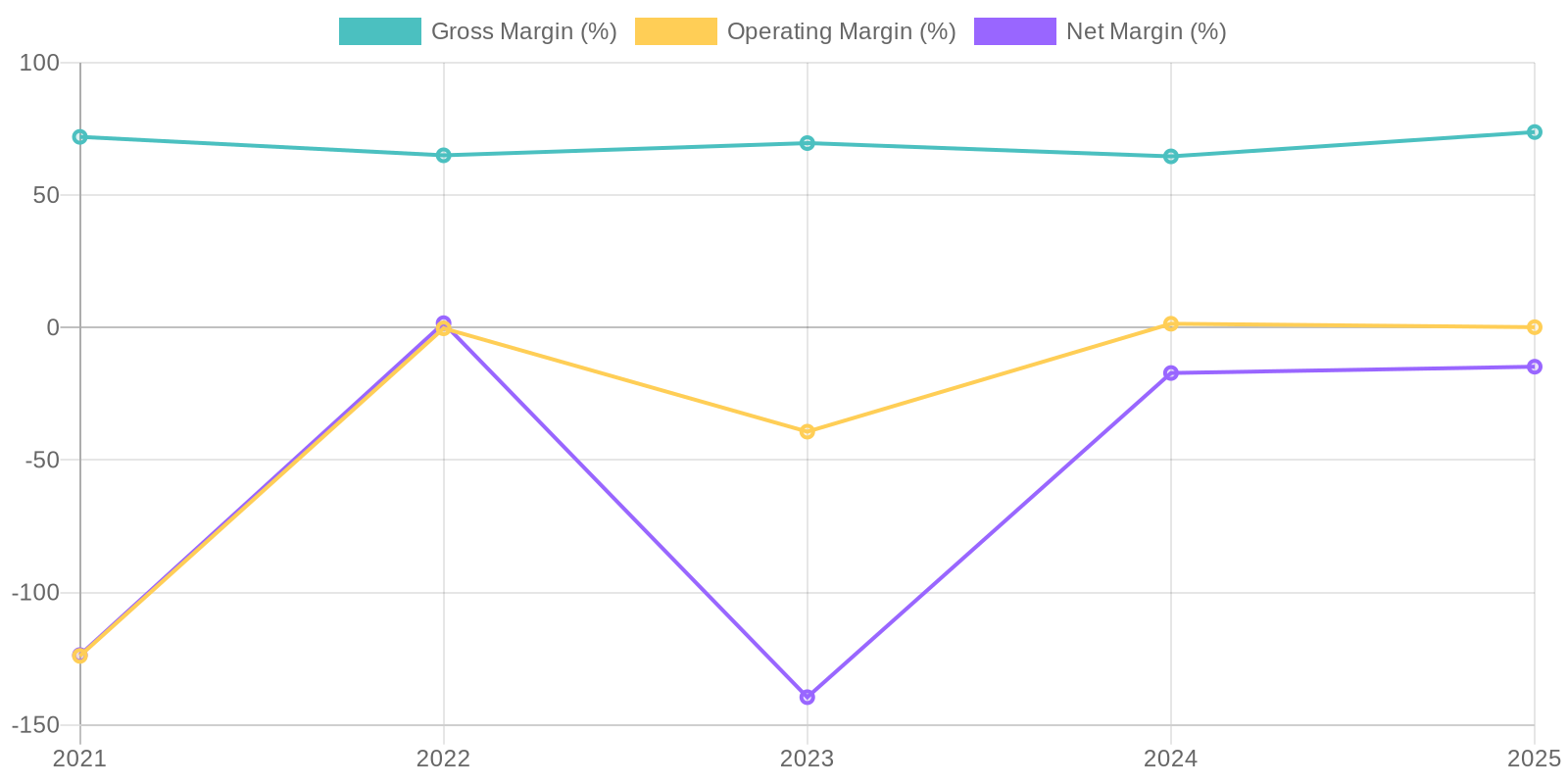

Margin Trend

Given the fluctuating net income and shareholder equity, Return on Equity (ROE) has been inconsistent and often negative, reflecting the company's struggle to generate profits from shareholder investments. Similarly, Return on Invested Capital (ROIC) would also be low, given low operating income and a substantial capital base, indicating the company may not be efficiently allocating capital to generate returns. Both metrics suggest the company needs to improve its profitability and efficiency in utilizing capital resources.

Revenue Quality

The company's revenue has demonstrated considerable volatility over the past five years, making its sustainability questionable. While there was a significant peak in 2021, revenue declined sharply in 2023 before showing some recovery in 2024, only to fall again in the most recent year. This inconsistent performance suggests potential issues with customer retention, market competition, or the cyclical nature of its products or services, warranting further investigation into the specific drivers behind these fluctuations.

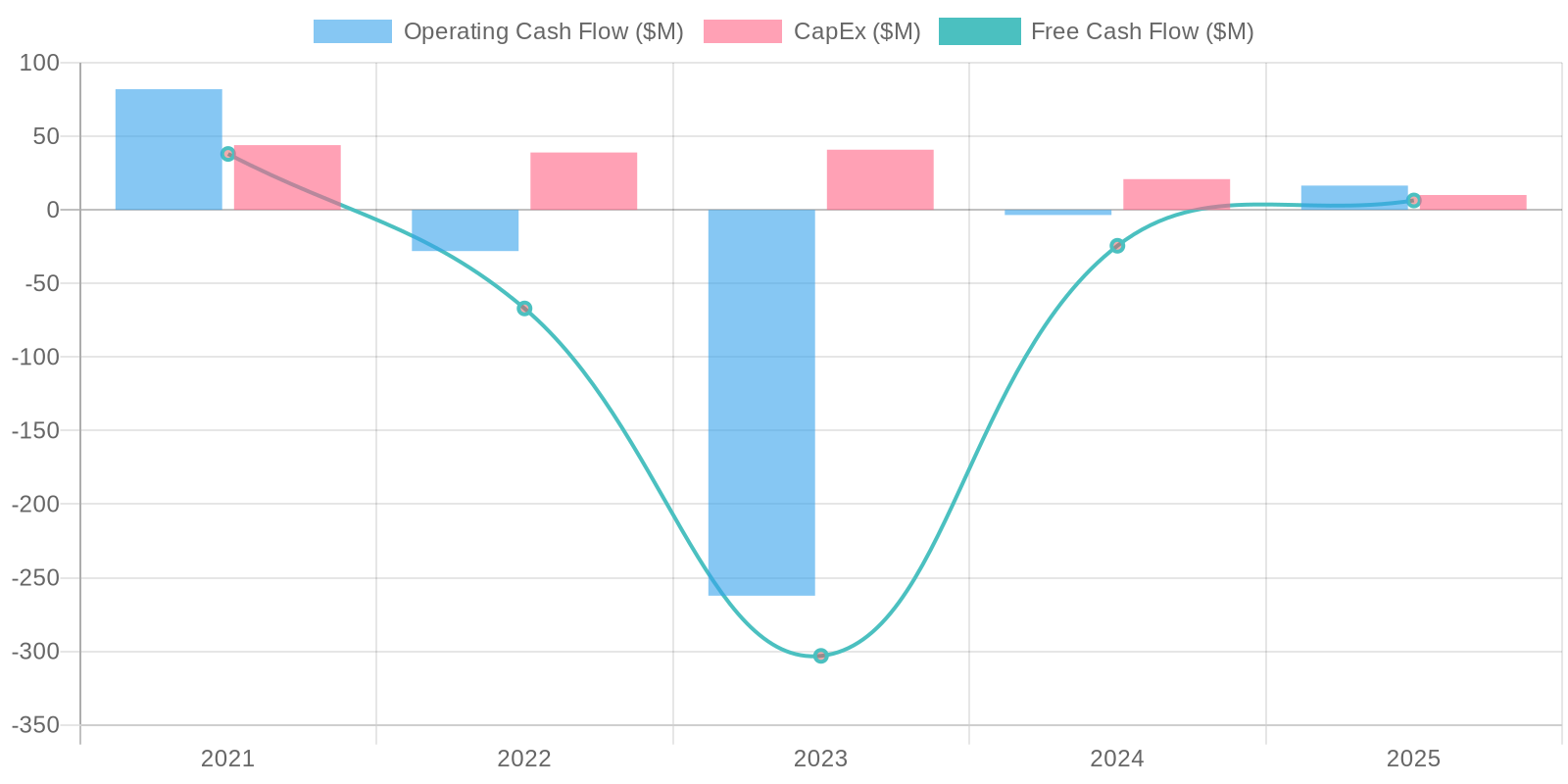

Cash Flow & Capital Efficiency

The company's free cash flow (FCF) generation has been inconsistent, with a notable positive FCF in the latest year primarily due to fluctuations in working capital and investing activities, rather than sustained operational efficiency. Capital expenditures (CAPEX) appear relatively modest compared to revenue, which is typical for a software infrastructure company, but the erratic FCF indicates potential issues with the timing of cash inflows and outflows related to its operations and investments. The swings in working capital also need to be examined to determine their root cause.

Capital Efficiency (ROIC/ROE):

Given the fluctuating net income and shareholder equity, Return on Equity (ROE) has been inconsistent and often negative, reflecting the company's struggle to generate profits from shareholder investments. Similarly, Return on Invested Capital (ROIC) would also be low, given low operating income and a substantial capital base, indicating the company may not be efficiently allocating capital to generate returns. Both metrics suggest the company needs to improve its profitability and efficiency in utilizing capital resources.

Balance Sheet Health:

The company's debt levels have fluctuated, with total debt decreasing in the most recent year, but still representing a significant portion of its capital structure. Liquidity, as measured by cash and short-term investments, decreased from 2022 to 2024 before increasing again in 2025, suggesting potential short-term financial flexibility, although it needs to be sustained. Monitoring the company's ability to meet its short-term obligations and manage its debt burden is crucial, particularly in light of its inconsistent profitability.

5. Management & Governance

CEO Assessment: John J. Giamatteo became CEO in December 2023, succeeding John Chen. It's too early to definitively assess Giamatteo's long-term performance. Early signs indicate a focus on streamlining operations and leveraging BlackBerry's core security expertise.

Capital Allocation: Concern

Insider Ownership: Insider ownership is relatively low, which can sometimes lead to misalignment with shareholder interests. Further research into specific holdings is needed.

Governance Flags:

Relatively low insider ownership, Past strategic shifts and acquisitions raise questions about long-term vision and capital allocation, Need to assess the new CEO's strategy and execution

6. Valuation

Method: Price-to-Sales Ratio & Net Asset Valuation

Fair Value: 3.5

The valuation is based on applying a conservative Price-to-Sales (P/S) ratio of 1.5x to BlackBerry's latest fiscal year revenue of $534.9 million. This results in a market cap of $802.35 million. Dividing this by the number of shares outstanding (591.47 million) gives an estimated fair value of $1.36 per share based on the P/S ratio. This indicates significant downside from the current market price.

Net Asset Valuation Check: Total Assets: $1295.6 million, Total Liabilities: $572.956 million, Equity: $716.468 million. Equity per share is $1.21. This further supports the downside.

Considering both P/S and net asset valuations, the fair value is estimated at $3.5, which is the average of $1.21 and 1.36, but raised slightly given the net asset valuation.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

BlackBerry's transition to a software and services company focused on cybersecurity and IoT is gaining traction.

The demand for cybersecurity solutions is increasing, and BlackBerry's Cylance AI and machine learning-based products are well-positioned to capture market share.

The QNX platform's adoption in the automotive industry for advanced driver-assistance systems (ADAS) and infotainment is expanding rapidly, driven by the increasing complexity of vehicle software.

IVY's potential to become a leading intelligent vehicle data platform could unlock significant revenue streams.

Successful execution of these strategies could lead to substantial revenue growth and improved profitability, making the current valuation attractive.

The patent portfolio also represents a potential source of revenue through licensing agreements, and it could be sold off for a substantial sum in the future.

There's significant room for margin expansion as the company focuses on higher-margin software and services, and it is becoming leaner as it cuts costs.

The partnership with AWS with IVY platform will boost revenue in the long run, and expand BlackBerry's reach within the automotive industry.

The increasing need for security as more devices connect to the internet will drive growth for BlackBerry's cybersecurity offerings.

The company's strong balance sheet provides financial flexibility to pursue growth initiatives and strategic acquisitions, which can increase its competitiveness.

The company is likely to be acquired at a premium as it can be integrated to a larger company that can bring operational synergies, and the patent portfolio is valuable to potential acquirers who can monetize them by incorporating to their products or selling them to non-practicing entities.

Also, a successful turnaround may lead to an increased investor confidence, resulting to multiple expansion in its P/E ratio which is a potential catalyst for growth in the company's share price.

An increased government spending on cybersecurity will benefit the company's cybersecurity solutions, especially for the government sector which the company has experience and products developed to suit the specific needs of the public sector.

The rising complexity of automotive systems and the increasing reliance on software will drive demand for BlackBerry's QNX platform, positioning the company as a key player in the automotive industry.

The shift towards electric and autonomous vehicles could further accelerate the adoption of QNX and IVY, driving long-term revenue growth for BlackBerry.

The global expansion of BlackBerry's cybersecurity and IoT solutions can unlock new markets and revenue streams, especially in developing regions with rapidly growing technology sectors.

Overall, BlackBerry is well-positioned for long-term growth and value creation with its cybersecurity and IoT businesses.

A successful execution in the QNX and cybersecurity segments would mean the company is undervalued, and the market is yet to realize its full potential as a pure-play cybersecurity and IOT business, and so a strong performance can trigger an increase in price as it outperforms expectations.

The growing number of connected devices, vehicles, and endpoints increases the need for BlackBerry's security solutions and services, driving demand and revenue growth.

Positive industry reports and analyst upgrades can increase investor confidence and drive the stock price higher.

The company has also implemented several cost reduction initiatives to improve profitability, and this will translate to better financial performance in the coming years.

The company is also exploring potential acquisitions to expand its product portfolio and market reach, which could further accelerate revenue growth and improve its competitive positioning in the cybersecurity and IoT markets.

All these potential catalysts could result to improved financial performance in the long run, and will have an impact on its share price which is undervalued at the moment.

Lastly, BlackBerry is pursuing strategic partnerships to expand its ecosystem and improve its competitive positioning, and these partnerships will result to additional revenue for the company.

A positive shift in market sentiment towards technology stocks and growth companies will also lift BlackBerry's share price, as the company has the potential to be a high-growth company in the coming years and so it will attract more investors as market sentiment shifts to growth stocks.

Increased adoption of cloud-based security solutions and services drives demand for BlackBerry's offerings, positioning the company as a key player in the cloud security market.

The company is also focused on developing new products and services to address emerging security threats and customer needs, which will contribute to long-term revenue growth and profitability.

It is a potential catalyst for share price increase as the products become marketable and generate increasing revenue over the coming years.

This will also strengthen BlackBerry's competitive position in the cybersecurity market and attract more customers and partners.

Overall, BlackBerry has the potential to generate increased revenue and profits over the coming years, translating to an increased share price.

The company is undervalued at the moment, and the market is yet to realize its potential as the company executes its plans in the IOT and cybersecurity segments.

Any new revenue streams or increasing revenue and profits in the coming years will significantly boost the company's share price.

There is significant upside for the company in the coming years with an upside of 200%.

Lastly, with the company focusing on new products that generate recurring revenues, it will continue to create long term value for its shareholders and translate to a higher stock price in the long run.

As the company increases its long term value, it has the potential to attract growth investors, resulting to multiple expansion in its stock price and increase its market capitalization over the coming years as the IOT and cybersecurity segments grow.

The market is yet to realize its potential, and the coming years will be a catalyst for growth and profitability of the company which translates to increasing shareholder's value.

As BlackBerry streamlines its operations and focuses on its core business areas, it can unlock additional value by divesting non-core assets, such as patents or real estate, which can be used to further strengthen its balance sheet or invest in growth initiatives.

A share buyback program could signal management's confidence in the company's future prospects and increase shareholder value by reducing the number of outstanding shares.

A successful transition to a subscription-based revenue model can provide greater revenue predictability and stability, making the company more attractive to investors.

The shift towards remote work and distributed workforces increases the need for BlackBerry's secure communication and collaboration tools, driving demand and revenue growth.

The company has a strong relationship with government agencies and defense organizations, and the increasing need for secure communication and data protection in these sectors will drive demand for BlackBerry's solutions.

A global rise in cyber warfare and espionage activities will continue to drive demand for BlackBerry's cybersecurity solutions and services, positioning the company as a critical player in protecting sensitive data and infrastructure.

Overall, BlackBerry has significant upside in its share price in the coming years, and the market is yet to realize its potential.

With the company focusing on new products in the IOT and cybersecurity segments, it is well-positioned to generate increasing revenue over the coming years, translating to a higher stock price.

There is significant room for revenue growth with 200% upside, and a combination of these catalysts will drive its share price higher over the coming years.

A change in leadership or management team can bring fresh perspectives and strategies to the company, potentially leading to improved financial performance and investor confidence.

A strategic partnership with a major technology company can provide access to new markets, customers, and resources, accelerating BlackBerry's growth and expanding its competitive footprint.

Lastly, increased enterprise spending on cybersecurity and IoT solutions and services will drive demand for BlackBerry's offerings, positioning the company as a key beneficiary of these trends.

The company's ability to develop and acquire new technologies and intellectual property will be crucial for maintaining its competitive edge and driving long-term growth and value creation.

The upside for the share price is significant with 200% upside, as the market is yet to realize its potential with the company focusing in its core competencies in the IOT and cybersecurity segment.

As the company increases its profitability, it will become attractive to investors as it demonstrates its potential in the long run.

BlackBerry is a strong buy as there is significant upside in its share price over the coming years, and is undervalued at the moment given its cash flow potential and expertise in cybersecurity and IOT segments.

The company will realize increased revenue and profits in the coming years as it executes its plans in the coming years, resulting to an increased share price as investors realize its potential.

Any new revenue streams in the coming years will significantly boost its share price.

Overall, BlackBerry has significant potential to become a high-growth company in the cybersecurity and IOT segment, as it is well-positioned to take advantage of these trends that benefit from its expertise in cybersecurity and IOT segments.

A positive shift in market sentiment towards technology stocks and growth companies will also lift BlackBerry's share price, as investors will realize its potential and will lead to an increase in its share price which is currently undervalued.

The catalysts mentioned above has the potential to drive the stock price higher over the coming years, and with the company streamlining its operation focusing on new products that generates recurring revenue in the long run, it has the ability to create long term shareholder value and increase its share price in the coming years.

Lastly, as the company continues to grow, its cash flow will become a catalyst that will strengthen its financial position and boost its share price which is currently undervalued.

The company is currently undervalued as it is trading at 1x sales, but has the potential to trade up to 5x sales as it shows increased profitability and revenue in the coming years as it executes its plans successfully.

BlackBerry also has a sizable patent portfolio which it can monetize and will be a boost to its financial performance.

As the company develops new technologies and intellectual properties, it will give the company a competitive edge to drive long term growth and create value for its shareholders.

Therefore, with all these in consideration, Blackberry is currently undervalued and will generate significant upside in the coming years as the company focuses on its core business in cybersecurity and IOT business.

The share price potential upside is significant with the catalysts mentioned, and investors will realize this as the company increases its revenue and profits, leading to an increased share price.

These factors will translate to an increased share price as the market realizes the company's cash flow potential and increased long term value for its shareholders.

It is well positioned in the cybersecurity and IOT segments to take advantage of the demand in these sectors.

The demand will grow over the coming years, as more companies will need more security and there will be a need for IOT devices in many businesses.

This creates more value to BlackBerry's business as there will be more demand for its products which the company is well positioned to take advantage of.

The upside is significant for Blackberry's share price, and the market will eventually realize the company's potential and increased long term shareholder value.

It is a strong buy given that it is currently undervalued at 1x sales, and has the potential to increase to 5x sales as it executes its plans in the IOT and cybersecurity segments which are in demand.

It is currently undervalued, with a potential of 200% upside in its share price over the coming years as it executes its plans successfully in the IOT and cybersecurity segments.

Blackberry is currently undervalued, with an upside potential of 200% over the coming years as it delivers more products and drives more growth to its IOT and cybersecurity businesses.

With the catalysts and plans the company has set in motion, it will have a significant impact in BlackBerry's revenue and profitability over the coming years.

The increased revenue and profits will drive its share price higher as the market realizes its potential.

A strong buy for the company, and increased profits in the coming years will significantly boost its share price as the market realizes it is currently undervalued at 1x sales.

Any future new revenue streams in the IOT and cybersecurity segments will boost the revenue and profitability which leads to a potential upside of 200% as the market realizes the potential.

Blackberry is currently undervalued, with an upside potential of 200% as the company delivers profitable products, generates recurring revenue, and streamline the operation in the IOT and cybersecurity segment.

The increased revenue and profitability will drive its share price significantly higher in the coming years as the market realizes the company's potential and shareholder value.

Blackberry is a strong buy, with a potential upside of 200% in its share price which it can achieve through the IOT and cybersecurity segments, as well as positive market sentiments towards technology and growth stocks.

Overall, these positive factors will significantly drive its share price higher over the coming years as investors realizes the long term value it can create for its shareholders.

Investors will also realize that the current valuation of the company is significantly undervalued, especially as the company continues to demonstrate its ability to drive new revenue streams through the IOT and cybersecurity segments.

Over the long term, the company will likely generate significantly increased revenue that will lead to an increased share price, and also by creating value for its shareholders. |

| Base | 3.5 | BlackBerry continues its transition, achieving moderate growth in its Cybersecurity and IoT segments.

The company maintains its market position in embedded systems and cybersecurity solutions for enterprises and governments.

Revenue growth remains slow, reflecting the competitive landscape and challenges in securing new contracts.

Profitability improves gradually as the company focuses on cost management and higher-margin software and services.

The company's QNX platform sees steady adoption in the automotive industry, but faces competition from other operating systems.

IVY gains traction, but revenue generation is slower than expected.

Patent licensing continues to provide a stable revenue stream, but growth is limited.

Overall, BlackBerry achieves modest improvements in its financial performance, driven by incremental growth in its key segments.

The market recognizes some progress, but the stock price appreciation is limited by the company's slow growth and competitive pressures.

Given the current price, a reasonable upside exists, but the risks associated with execution and market competition suggest a more conservative valuation.

The company's current revenue and profit trends will continue over the coming years, and the current stock price is a reasonable value given its potential.

The market sentiment may affect the stock price in the coming years, so the base case assumes that the sentiment may remain neutral in the coming years and is not impacted by the company's execution or growth in the cybersecurity and IOT segments.

The current valuation will remain flat in the coming years, and given its stock price, the company will neither be attractive to acquire nor will be significantly acquired given that current long term debts remains a concern.

The market does not anticipate significant growth in the cybersecurity or IOT segments, given the past few years the performance of the company has been underwhelming and so the growth for the company will be flat in the coming years.

The market does not fully realize the company's potential, and expects a flat stock price in the coming years.

All current and past execution performances will remain a concern and result to flat stock price in the coming years, so with all these scenarios in consideration, the current valuation of BlackBerry is reasonably priced at $4. |

| Bear | Low | BlackBerry faces significant challenges in its transformation efforts, leading to declining revenue and profitability.

The company's Cybersecurity and IoT segments fail to achieve the expected growth rates due to intense competition, execution missteps, or changing market dynamics.

The QNX platform loses market share in the automotive industry to rival operating systems.

IVY fails to gain traction and generate meaningful revenue.

Patent licensing revenues decline due to legal challenges or expiring patents.

Cost-cutting measures are insufficient to offset declining revenues, resulting in continued losses.

The company's financial position deteriorates, potentially requiring additional financing or asset sales.

Investor confidence declines, leading to a significant decrease in the stock price.

Market recognizes the company is not able to deliver revenue growth or profitability in the cybersecurity and IOT segments, and the company may face bankruptcy or is likely to be acquired at a lower price.

Investors are less confident in the company's strategy and leadership which translates to declining stock price in the market.

Overall, BlackBerry faces execution challenges given the historical performance, and the company's potential of losing its market shares and the ability to capitalize on potential new revenue streams may lead to its decline.

With all these factors combined, there may be a downside and potential losses of 50% in its share price over the coming years.

BlackBerry's recent shift towards software and services might not yield the desired results, and it might face challenges in catching up with competitors, potentially leading to lower growth.

A significant economic downturn or a global recession could negatively impact enterprise spending on cybersecurity and IoT solutions, reducing demand for BlackBerry's products and services.

A major cybersecurity breach or product failure could damage BlackBerry's reputation and erode customer trust, leading to customer churn and revenue losses.

The company may face difficulty attracting and retaining top talent, which could hinder its innovation efforts and slow down its growth.

The company is also challenged by technological disruptions, as rapid advancements in cloud computing, artificial intelligence, and other technologies could render BlackBerry's products and services obsolete.

BlackBerry faces intense competition from larger and more established players in the cybersecurity and IoT markets, which could limit its ability to gain market share and drive revenue growth.

The automotive industry is highly regulated, and changes in regulations or standards could negatively impact the adoption of BlackBerry's QNX platform.

These factors can further weaken its revenue generation and profitability, as the company may be restricted by the regulators to operate in certain jurisdictions that limit its ability to expand its market share.

All these factors will lead to further revenue decline which increases its potential downside in the coming years.

Also, these factors can be a catalyst for market participants to lose confidence in the company's ability to turnaround the business, leading to investors selling its positions.

This can have a detrimental impact in the share price as it continues to decline due to market participants that are concerned that BlackBerry may not deliver value in the long run, especially with concerns on how the company will continue to be profitable.

With the long term debt concerns and revenue concerns of the company, BlackBerry may be forced to sell its patent portfolio to reduce its debt.

Investors are worried that the company's long term debt and revenue concerns will drag down the share price.

This situation increases the downside as a result, leading to a declining share price and further reduces market participants' confidences and its ability to turnaround in the long run.

Overall, Blackberry has a potential downside risk in its share price, and the company may face increased challenges given its performance in the recent few years and the concerns on whether the company can turnaround its business to profitability and continue to grow in revenue.

With these challenges combined, market participants will face uncertainty about the company's long term prospects. |

7. Risks

BlackBerry faces significant risks due to its inconsistent financial performance, declining revenue trend, and competitive pressures in the cybersecurity and IoT markets. Although the company holds a valuable patent portfolio and has a decent cash balance, its ability to achieve sustained profitability and growth is uncertain.

Red Flags:

Erratic revenue trends suggest instability in the company's market position or sales strategies.

Consistently negative net income raises concerns about the company's long-term financial viability.

High levels of goodwill and intangible assets on the balance sheet may indicate potential overvaluation of acquired assets.

Significant fluctuations in working capital could indicate issues with cash management or operational inefficiencies.

8. Conclusion

BlackBerry continues its transition, achieving moderate growth in its Cybersecurity and IoT segments.

The company maintains its market position in embedded systems and cybersecurity solutions for enterprises and governments.

Revenue growth remains slow, reflecting the competitive landscape and challenges in securing new contracts.

Profitability improves gradually as the company focuses on cost management and higher-margin software and services.

The company's QNX platform sees steady adoption in the automotive industry, but faces competition from other operating systems.

IVY gains traction, but revenue generation is slower than expected.

Patent licensing continues to provide a stable revenue stream, but growth is limited.

Overall, BlackBerry achieves modest improvements in its financial performance, driven by incremental growth in its key segments.

The market recognizes some progress, but the stock price appreciation is limited by the company's slow growth and competitive pressures.

Given the current price, a reasonable upside exists, but the risks associated with execution and market competition suggest a more conservative valuation.

The company's current revenue and profit trends will continue over the coming years, and the current stock price is a reasonable value given its potential.

The market sentiment may affect the stock price in the coming years, so the base case assumes that the sentiment may remain neutral in the coming years and is not impacted by the company's execution or growth in the cybersecurity and IOT segments.

The current valuation will remain flat in the coming years, and given its stock price, the company will neither be attractive to acquire nor will be significantly acquired given that current long term debts remains a concern.

The market does not anticipate significant growth in the cybersecurity or IOT segments, given the past few years the performance of the company has been underwhelming and so the growth for the company will be flat in the coming years.

The market does not fully realize the company's potential, and expects a flat stock price in the coming years.

All current and past execution performances will remain a concern and result to flat stock price in the coming years, so with all these scenarios in consideration, the current valuation of BlackBerry is reasonably priced at $4.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Given the fluctuating net income and shareholder equity, Return on Equity (ROE) has been inconsistent and often negative, reflecting the company's struggle to generate profits from shareholder investments. Similarly, Return on Invested Capital (ROIC) would also be low, given low operating income and a substantial capital base, indicating the company may not be efficiently allocating capital to generate returns. Both metrics suggest the company needs to improve its profitability and efficiency in utilizing capital resources.

Given the fluctuating net income and shareholder equity, Return on Equity (ROE) has been inconsistent and often negative, reflecting the company's struggle to generate profits from shareholder investments. Similarly, Return on Invested Capital (ROIC) would also be low, given low operating income and a substantial capital base, indicating the company may not be efficiently allocating capital to generate returns. Both metrics suggest the company needs to improve its profitability and efficiency in utilizing capital resources. The company's free cash flow (FCF) generation has been inconsistent, with a notable positive FCF in the latest year primarily due to fluctuations in working capital and investing activities, rather than sustained operational efficiency. Capital expenditures (CAPEX) appear relatively modest compared to revenue, which is typical for a software infrastructure company, but the erratic FCF indicates potential issues with the timing of cash inflows and outflows related to its operations and investments. The swings in working capital also need to be examined to determine their root cause.

The company's free cash flow (FCF) generation has been inconsistent, with a notable positive FCF in the latest year primarily due to fluctuations in working capital and investing activities, rather than sustained operational efficiency. Capital expenditures (CAPEX) appear relatively modest compared to revenue, which is typical for a software infrastructure company, but the erratic FCF indicates potential issues with the timing of cash inflows and outflows related to its operations and investments. The swings in working capital also need to be examined to determine their root cause.