Deep Dive: CCC Intelligent Solutions Holdings Inc. (CCCS)

Recommendation: HOLD Price Target: 9.5 (8.57 Upside) Risk Level: Medium

1. Executive Summary

CCC Intelligent Solutions Holdings Inc. (CCCS) operates in the technology sector, providing a cloud-based software platform for the property and casualty (P&C) insurance industry. The company's solutions connect insurers, repair facilities, automakers, part suppliers, and claimants, facilitating digital interactions and workflows throughout the insurance lifecycle. CCC's current market position is characterized by a strong presence in North America, serving a large network of insurance carriers and repair shops. However, increasing competition and the shift in the automotive industry toward electric vehicles (EVs) and advanced driver-assistance systems (ADAS) present both challenges and opportunities.

Growth catalysts for CCCS include the ongoing digital transformation within the insurance industry, which drives demand for its cloud-based solutions. Specifically, the increasing adoption of AI and machine learning for claims processing and fraud detection presents significant growth potential. Furthermore, the company's expansion into new markets and the development of innovative solutions for the EV and ADAS ecosystems are expected to fuel future growth. The integration of data analytics and insights into its platform further enhances its value proposition and customer retention.

Key risks facing CCCS encompass increasing competition from both established players and emerging startups in the insurance technology space. Economic downturns and volatility in the automotive industry can impact repair volumes and, consequently, the demand for CCC's services. Furthermore, the company's ability to adapt to evolving regulatory requirements and technological advancements, such as the proliferation of EVs and autonomous vehicles, is crucial for its long-term success. Data security and privacy concerns also pose ongoing risks.

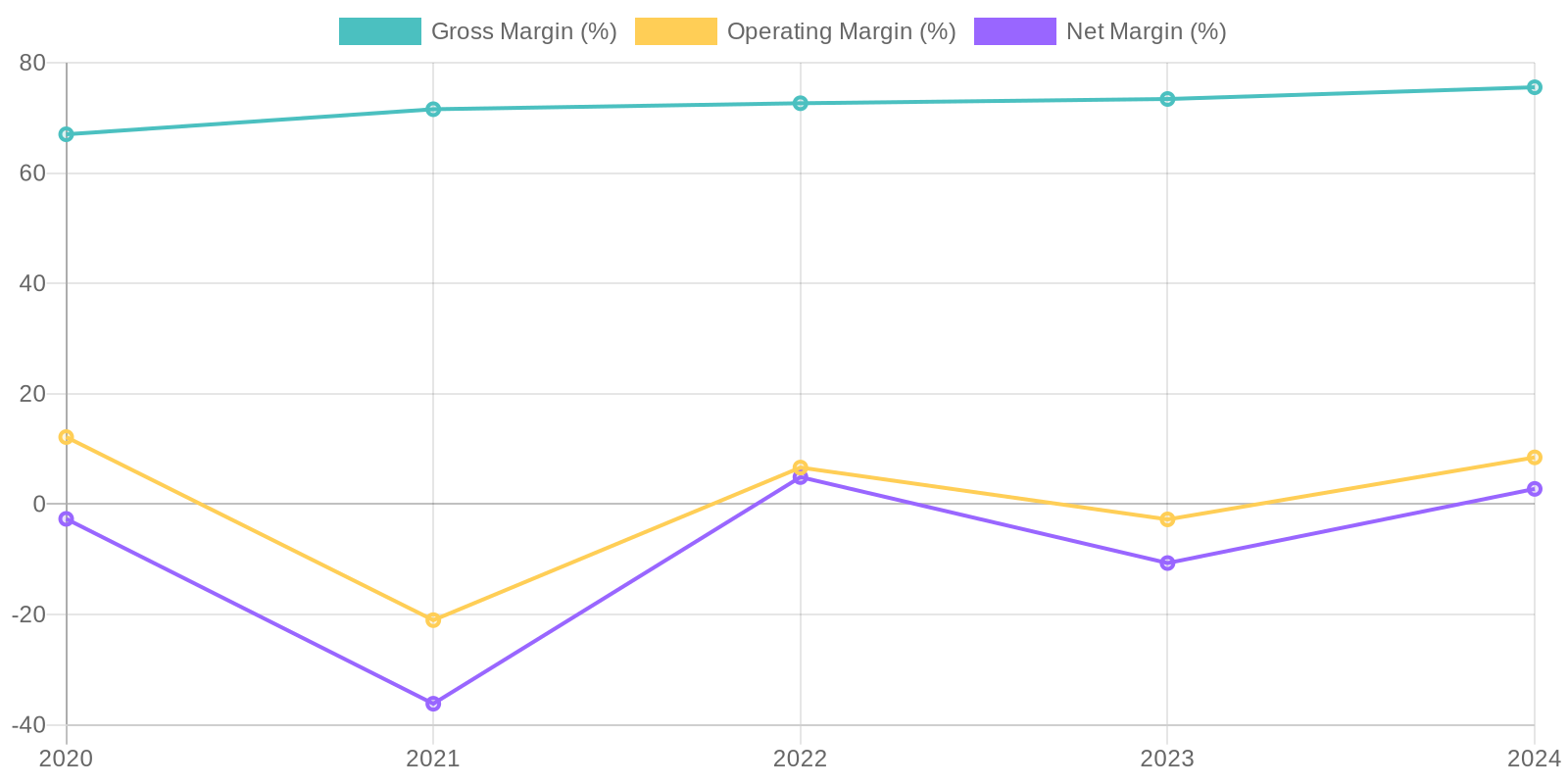

Given the current price of $8.75, a comprehensive valuation summary requires deeper financial analysis and benchmarking against peers. Factors to consider include CCC's revenue growth rate, profitability margins, and future cash flow projections. A discounted cash flow (DCF) analysis, compared to peer multiples, provides a more accurate valuation. The growth catalysts and risk factors outlined above should be carefully considered when assessing CCCS's long-term investment potential. Without detailed financial figures, a determination of whether CCCS is currently overvalued, undervalued, or fairly valued is not possible.

The company's ROIC and ROE cannot be reliably calculated with the information provided; further information such as invested capital is needed for ROIC. Reviewing the trends in invested capital, including working capital, along with the trends in the components of Net Income will be necessary to calculate ROIC. Similarly, ROE requires a calculation using the equity data; any insights will hinge on a consistent and reliable methodology. More detailed segmented data is needed to create these calculations.

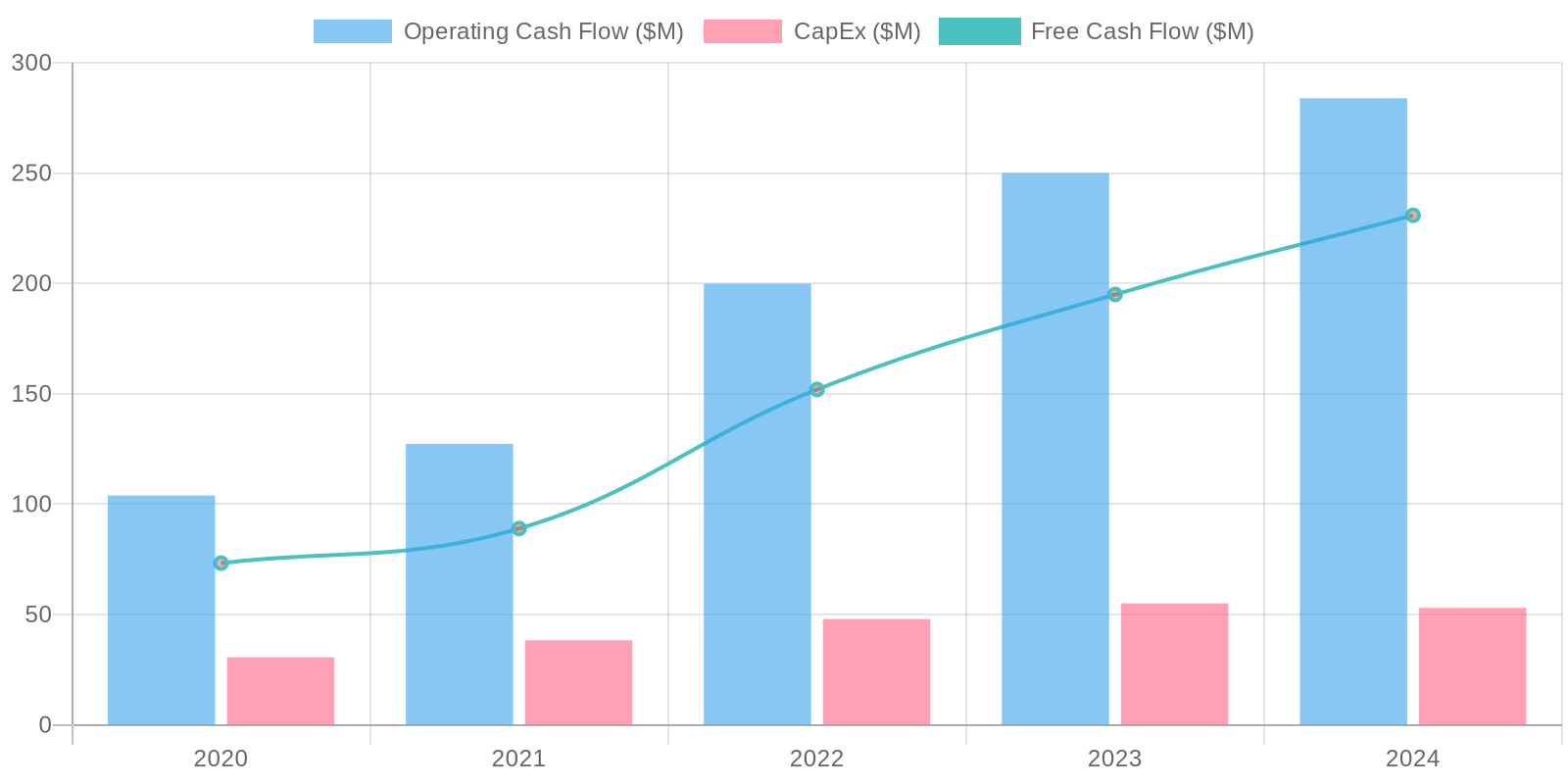

The company's ROIC and ROE cannot be reliably calculated with the information provided; further information such as invested capital is needed for ROIC. Reviewing the trends in invested capital, including working capital, along with the trends in the components of Net Income will be necessary to calculate ROIC. Similarly, ROE requires a calculation using the equity data; any insights will hinge on a consistent and reliable methodology. More detailed segmented data is needed to create these calculations. The company showcases a generally positive trend in operating cash flow, with significant fluctuations that mirror its profitability. The free cash flow (FCF) generation improved significantly in 2024 reaching $230.874 million, indicating a greater ability to fund operations and investments. Capital expenditure remained relatively stable in recent years, and this relative stability warrants deeper investigation.

The company showcases a generally positive trend in operating cash flow, with significant fluctuations that mirror its profitability. The free cash flow (FCF) generation improved significantly in 2024 reaching $230.874 million, indicating a greater ability to fund operations and investments. Capital expenditure remained relatively stable in recent years, and this relative stability warrants deeper investigation.