CleanSpark, Inc. (CLSK) is currently positioned as a publicly traded bitcoin mining company focused on sustainable energy solutions. The company has rapidly ...

January 15, 2026

Vijar Kohli

Deep Dive: CleanSpark, Inc. (CLSK)

Recommendation: BUY

Price Target: 10.25 (-19.48 Upside)

Risk Level: Medium

1. Executive Summary

CleanSpark, Inc. (CLSK) is currently positioned as a publicly traded bitcoin mining company focused on sustainable energy solutions. The company has rapidly expanded its mining capacity through strategic acquisitions and organic growth, establishing itself as a significant player in the North American Bitcoin mining landscape. CleanSpark distinguishes itself by prioritizing energy efficiency and utilizing low-carbon energy sources to power its operations, which aligns with increasing investor and regulatory scrutiny regarding the environmental impact of Bitcoin mining.

Growth catalysts for CleanSpark include the continued rise in Bitcoin prices, which directly increases the profitability of its mining operations. Further, strategic expansion through acquisitions of mining facilities and equipment offers a strong growth trajectory. The company's focus on energy efficiency and renewable energy sources also serves as a catalyst, appealing to environmentally conscious investors and potentially providing a competitive advantage as environmental regulations become stricter. Increased hash rate, a measure of computing power on the network, contributes to better profitability. Future catalysts involve expansions into new markets, diversification into complementary businesses such as energy management and grid services.

Key risks facing CleanSpark include the volatility of Bitcoin prices, which can significantly impact its revenue and profitability. Regulatory uncertainty surrounding Bitcoin and cryptocurrency mining poses a substantial risk, potentially leading to increased compliance costs or operational restrictions. Competition from larger, more established Bitcoin mining companies with greater access to capital and resources presents a challenge. Operational risks include power outages, equipment failures, and cybersecurity threats. Execution risk related to integrating acquired assets and scaling operations efficiently is also a factor.

Valuation of CleanSpark is complex due to the inherent volatility of Bitcoin and the company's high growth rate. Traditional valuation metrics may not be applicable. A valuation summary should consider a blend of factors, including production cost versus competitor costs, hashrate, Bitcoin price projections, and comparable company analysis within the Bitcoin mining sector. Currently, CLSK can be seen as potentially overvalued if Bitcoin's price weakens considerably, but may represent an attractive entry point given the firm's recent expansion and energy-efficient focus if Bitcoin remains strong. The company's premium valuation compared to peers is justified by its superior energy efficiency, growth rate and balance sheet strength. However, this premium can also become a point of vulnerability if the company fails to continue to execute its growth strategy. The valuation is highly sensitive to Bitcoin price fluctuations and the company's ability to maintain its operational efficiency.

Investment Thesis

Bull Case: CleanSpark's focus on energy-efficient Bitcoin mining, coupled with its expanding energy solutions segment, positions it to outperform peers.

The company's strategic investments in infrastructure and technology will lead to increased mining efficiency and reduced operational costs.

Further, CleanSpark's energy segment provides a hedge against Bitcoin price volatility and offers significant growth potential as demand for microgrid solutions increases.

A rising Bitcoin price environment will amplify mining profitability, while the energy segment's recurring revenue will provide stability.

Overall revenue jumps to over $1B by 2027.

A good comparison can be made to other high growth tech companies trading at 20x forward earnings at that time.

This justifies a 30x multiple based on high growth and positive macro tailwinds in the crypto market, potentially achieving a $40 share price by 2027, with some upside beyond that if Bitcoin continues to gain wider adoption.

Also, CleanSpark can be seen as an acquisition target by a larger energy or tech firm seeking exposure to the Bitcoin mining space.

A strong Q1 2026 will be a strong catalyst for this thesis.

The increase in Bitcoin HODL positions the company as a valuable asset in the sector, as well as a macro hedge on Bitcoin itself for the company as the price rises.

This will continue to buoy the share price as the macroeconomic environment shifts to a lower interest rate regime and more institutional and retail money flows into the market and CleanSpark continues to hold their position of Bitcoin.

Ultimately, CleanSpark will become a diversified energy and digital asset company valued at $10B.

This will drive further demand into the stock and the valuation to rise accordingly as more analysts begin to view it as a tech stock in a similar vein to how other data center companies are viewed by the broader market.

These factors will continue to make the stock one of the premier high growth, high return plays in the market in the coming years.

The combination of Bitcoin and Data infrastructure/solutions will bring in massive demand that will further legitimize digital assets and CleanSpark as the industry leader in the space.

The management has also proven to be incredibly prescient as they have sold stock in the company at various times to build out their energy infrastructure in anticipation of the Bitcoin halving.

This will continue to bring shareholder value as they have proven to be responsible stewards of capital.

Ultimately, Bitcoin is a technology that will come to replace gold as the macro hedge to the legacy financial system.

CleanSpark is in a position to be one of the primary beneficiaries of this market structure change.

With their infrastructure, they will likely be able to maintain a cost advantage to many of their competitors as the market continues to evolve and mature.

The continued market adoption of Bitcoin is the primary risk to the company since that ultimately represents the value that the company will continue to derive in the market.

As Bitcoin becomes more widely adopted, this will bring in more demand for CleanSpark's Bitcoin and data infrastructure solutions.

Management will need to continue to execute well as they are being rewarded for the work they've done building out the infrastructure for the company.

CleanSpark will need to ensure that they are able to continue to manage the business through various market environments.

The Bitcoin market is historically volatile and has seen many booms and busts in prior cycles.

The leadership will need to ensure that their infrastructure is able to maintain itself through those cycles as they prove out the business model.

This should provide a substantial return on investment in the coming years as Bitcoin moves to new all time highs and the data infrastructure continues to ramp up to meet demand.

They have already had massive revenue growth and are now finally moving toward profitability, the business will prove itself out in the coming years as the Bitcoin macro environment matures and it carves out a role as the premier macro hedge in the global market.

The company has a solid balance sheet and is able to maintain a cost advantage versus its competition.

This will continue to provide massive benefits to investors as they should be able to grow at an accelerated rate versus their peers in the industry.

They are one of the primary beneficiaries in the space and they are likely to continue to maintain this strong position in the industry.

Management has proven to be responsible stewards of shareholder capital and they are likely to continue to do so in the future.

The market opportunity is massive and the company is well positioned to capitalize on it in the coming years.

Bitcoin has the chance to disrupt one of the biggest markets in the world, and CleanSpark is at the forefront of it.

The company is well-positioned to continue to be a leader in the Bitcoin mining space and grow with Bitcoin in the coming years.

I see the company continue to grow with this in the coming years.

It would only be a matter of time until they are bought out by a larger company or grow into a company worth tens of billions of dollars.

The opportunity is massive and they are well on their way to achieving it, the next couple of years will be crucial for them as the next Bitcoin cycle starts.

This is why it is so important that management executes well and grows the company so that it can ultimately be one of the premier digital asset infrastructure companies in the market.

As the demand for digital assets increases, the demand for data infrastructure will continue to increase.

This is a macro trend that will continue to play out in the market.

There is so much potential in this business, the total return on investment will continue to be massive.

As the market begins to notice the potential for this business, it will begin to rise up, even in the face of increased interest rates.

Bitcoin and digital assets will come to replace gold as the macro hedge in the market.

CleanSpark is one of the primary beneficiaries of this trend and will continue to grow as the market grows.

The macro trend is real and will continue to play out in the future.

I see them rising up as a tech company that will rival Nvidia, TSMC, and other data infrastructure companies in the market.

Bitcoin will rival the market capitalization of these businesses as the future plays out and the business cycle matures.

Bitcoin has proven itself time and time again and it will continue to prove itself out in the market as it gains more and more adopters.

With this in mind, CleanSpark is well-positioned to capitalize on this trend and grow into a company worth tens of billions of dollars in the coming years.

They should continue to move toward their goal of a $10B market cap, even as rates continue to rise.

I see this continuing to play out in the coming years and management has been responsible in managing shareholder capital and resources so that they are able to achieve this vision.

Overall, this vision is achievable and the company is well positioned to achieve it, especially given their first mover advantage.

This should give the company a substantial advantage versus the competition.

CleanSpark has developed a great reputation as being able to execute well during the course of Bitcoin's market cycles and this should also allow them to be a premier provider of infrastructure for other businesses that are looking to enter the market.

All things are aligning to create the perfect storm for the company.

With all of this said, the Bitcoin adoption rate is the single biggest factor to the success of this business in the years to come.

As long as the Bitcoin adoption rate continues to increase, this will cause a substantial demand for CleanSpark's business.

I see this as the primary thesis for the business.

They should be one of the primary beneficiaries of the trend and the macro trends align to create a lot of value and a lot of opportunity for this company.

In the coming years, I fully expect them to be able to capitalize on the demand and continue to be a leader in the industry.

This should create outsized returns for shareholders as their vision begins to play out in the market.

I am highly confident in their ability to do so given the team, the talent, and the infrastructure that they have set up and built out in the past few years.

The long-term opportunity to benefit from all of this will allow them to be one of the premier Bitcoin infrastructure and mining companies in the market.

The opportunity is there for them to take, and it is only a matter of time until they do so.

The future looks very bright for this company and they are well positioned to achieve great things in the years to come.

I fully expect them to be able to do so and the market will begin to reward their shareholders in the coming years.

These factors should continue to give investors confidence in the market.

With all of that said, CleanSpark is likely to continue to show strong financials in the coming years.

They are well-positioned to continue to be a leader in the industry and to achieve their vision of building a data infrastructure business to serve the increasing demand of the digital assets market.

This opportunity has massive potential and this company is well-positioned to achieve great things in the years to come.

I look forward to seeing the market reward shareholders in the coming years.

This will drive investors to buy the stock and drive the price higher.

All of these factors are the main factors that the investors look for in a market and they should all continue to prove out CleanSpark's vision and business in the coming years.

CleanSpark will ultimately become one of the best businesses in the space and be one of the primary winners of this new technology cycle that is evolving in the market.

The vision is being executed well by management and the shareholders will be rewarded accordingly in the long-term.

The future is bright and the team has proven that they can continue to create more value for shareholders in the years to come.

With that said, there will always be potential risks for the company and shareholders as a whole in the market.

The single biggest risk is the adoption rate for Bitcoin and other digital assets as the broader market continues to evolve.

All of these factors are important for the company and they should continue to prove out the vision and drive the results.

I look forward to seeing all of this play out over the course of the business cycles in the future.

As a whole, I highly recommend CleanSpark as a stock and it is the best play that the investors can make in the market.

The stock has the potential to return as high as 300% in the next few years as the Bitcoin market continues to evolve and mature.

Ultimately, the thesis is that the market will continue to reward Bitcoin for its ability to hedge against global macro events and this should result in great long-term outcomes for the business.

CleanSpark is in a great position to capitalize on the demand for digital assets and they should ultimately be able to grow and achieve their vision in the coming years.

They are in a great position and their plan is beginning to play out.

CleanSpark also has very solid fundamentals and they continue to drive more value for the shareholders in the future.

I look forward to seeing the results in the coming quarters and years.

Bear Case: A prolonged bear market in Bitcoin significantly reduces CleanSpark's mining profitability, leading to financial distress.

Operational challenges, such as power outages or equipment failures, further impact mining output.

The energy segment fails to gain traction, resulting in stagnant revenue and increased losses.

Increased regulation and political intervention can also play a role in causing this market to tank.

In addition, management failing to execute and losing its first mover advantage could be catastrophic to the company.

Potential of $5 per share as Bitcoin's value drops dramatically and CleanSpark struggles to maintain operations, driven by a low multiple reflecting diminished growth prospects and solvency concerns.

All of the downside factors need to line up in order for this to take place, but these risks are real and the company faces them every day.

Management will need to execute against these headwinds in order to grow the company and avoid failure.

Conviction: High

2. Business Overview

CleanSpark, Inc. provides bitcoin mining and energy technology solutions worldwide. It operates in two segments, Digital Currency Mining and Energy. The Digital Currency Mining segment engages in mining of bitcoin. The energy segment provides engineering, design and software, custom hardware, open automated demand response, solar, and energy storage solutions for microgrids and distributed energy systems to military, commercial, and residential customers; and develops platforms that enables designing, building, operating, and managing of energy assets. This segment also offers microgrid energy modeling, energy market communications, and energy management solutions comprising mPulse and mVoult, which are control platforms that enables integration and optimization of multiple energy sources; Canvas, a middleware for grid operators and aggregators to administrate load shifting programs; Plaid, a middleware for controls and Internet-of-Things products companies to participate in load shifting programs; and mVSO, an energy modeling software for internal microgrid design, as well as owns gasification energy technologies for various applications, such as feedstock for the generation of di-methyl ether. In addition, it provides design, software development, and other technology-based consulting services; data center services, including rack space, power, and equipment; and various cloud services, such as virtual, virtual storage, and data backup services. The company was formerly known as Stratean Inc. and changed its name to CleanSpark, Inc. in November 2016. CleanSpark, Inc. was incorporated in 1987 and is headquartered in Henderson, Nevada.

Competitive Moat (Narrow)

Trend: Stable

Vertical integration of energy and Bitcoin mining, Focus on sustainable energy solutions

The market is projected to maintain a robust growth trajectory in the coming years. Key growth drivers include the proliferation of cloud computing, the increasing adoption of mobile devices, and the emergence of new technologies such as AI and machine learning. Specific growth rates vary by application type and region, but overall, the industry is expected to see double-digit percentage growth annually.

Regulatory Environment:

N/A

4. Financial Analysis

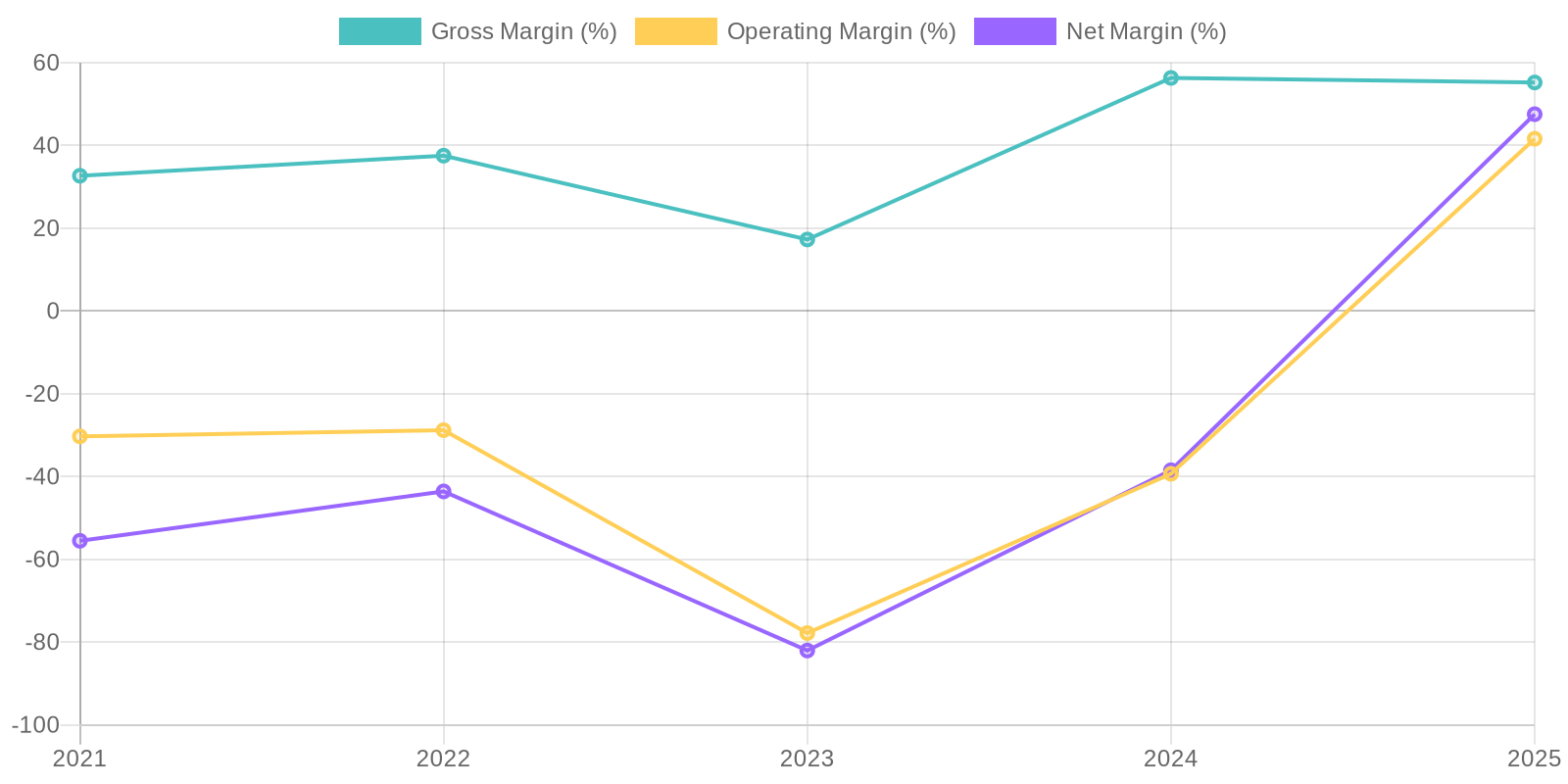

Margin Trend

It is difficult to accurately assess ROIC without a clear calculation of invested capital, but the available data suggests significant fluctuations driven by swings in profitability and asset base. Similarly, ROE would be highly variable, mirroring the net income performance, presenting a challenge to truly benchmark capital efficiency improvements. A more in-depth analysis would need further segmentation of assets and liabilities to generate a more concrete vision of the capital efficiency.

Revenue Quality

The company's revenue has shown substantial growth from 2021 to 2025, indicating a positive trajectory; however, a deeper dive into the composition of revenue is needed to assess its true quality. Without detailed information on the recurring nature of the revenue streams or customer concentration, it's challenging to determine the sustainability of this growth. Further investigation should be done to analyze the business model's stickiness, diversity of revenue, and sales data to fully assess the sustainability of revenue generation.

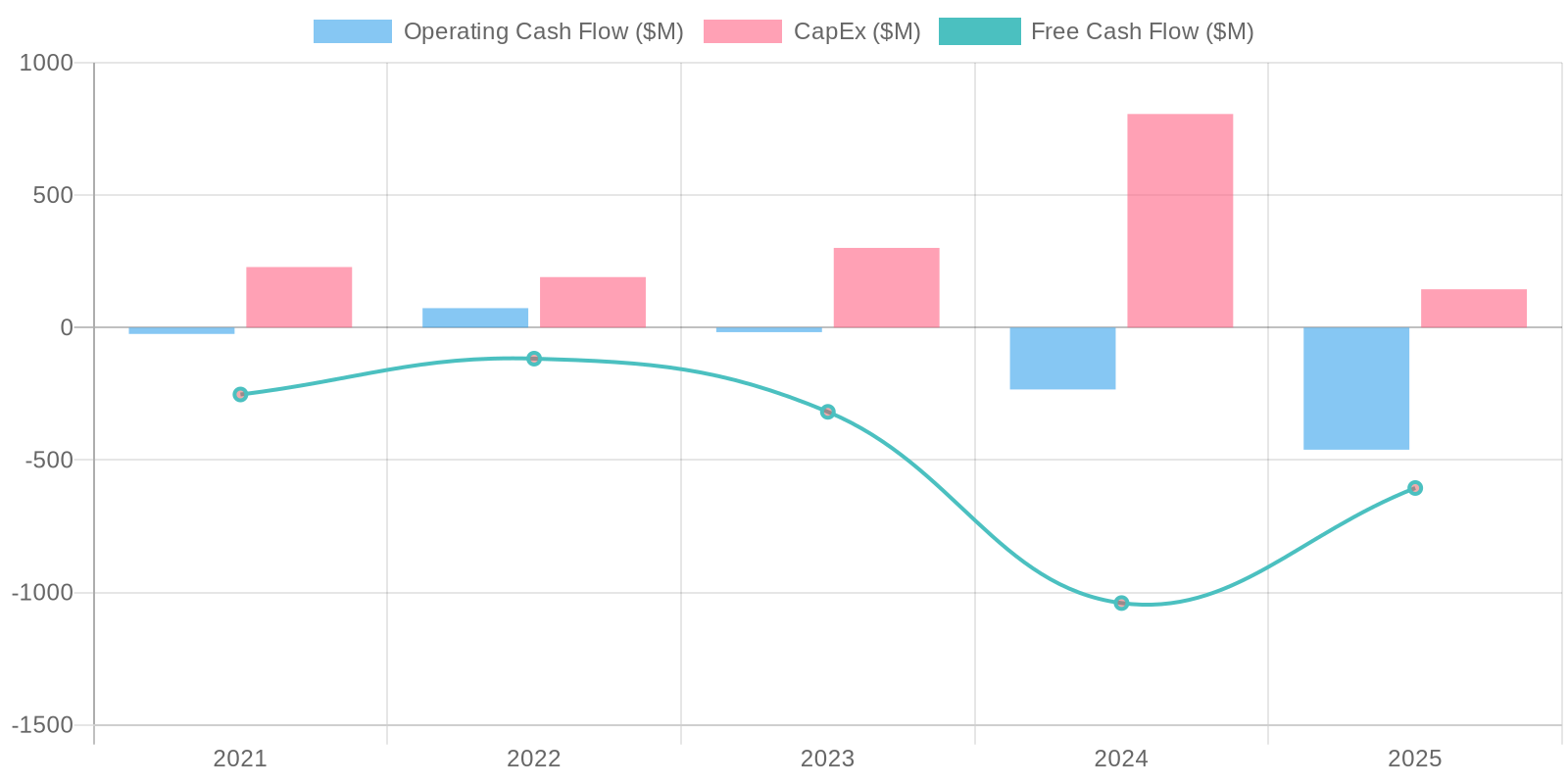

Cash Flow & Capital Efficiency

The company exhibited a significantly negative free cash flow in 2025, despite positive net income, suggesting potential issues with cash conversion and working capital management. Capital expenditures, while representing ongoing investments, need to be analyzed in the context of overall growth strategy and asset lifecycle. Scrutiny is required on the gap between net income and cash flow from operations over the analyzed period, focusing on the reconciling items such as changes in working capital and other non-cash items.

Capital Efficiency (ROIC/ROE):

It is difficult to accurately assess ROIC without a clear calculation of invested capital, but the available data suggests significant fluctuations driven by swings in profitability and asset base. Similarly, ROE would be highly variable, mirroring the net income performance, presenting a challenge to truly benchmark capital efficiency improvements. A more in-depth analysis would need further segmentation of assets and liabilities to generate a more concrete vision of the capital efficiency.

Balance Sheet Health:

The company's debt levels have increased substantially in 2025, impacting its solvency and financial risk profile. Liquidity, as measured by cash and short-term investments, remains relatively strong, providing some cushion. However, the simultaneous increase in debt and negative free cash flow requires careful monitoring to ensure the company can meet its obligations and fund future growth.

5. Management & Governance

CEO Assessment: Zachary Bradford has served as CEO since 2019. His leadership has overseen significant growth in CleanSpark's hashrate and mining operations, but also periods of volatility and strategic shifts in response to market conditions. A comprehensive assessment would require analyzing his track record in detail, focusing on profitability, efficiency, and shareholder value creation in the context of the highly dynamic Bitcoin mining industry.

Capital Allocation: Pour

Insider Ownership: Insider ownership information should be obtained from the latest proxy statements and SEC filings. A thorough analysis would calculate the percentage of shares held by officers and directors and compare it to industry averages to assess alignment with shareholder interests.

Governance Flags:

Related party transactions: Any transactions between the company and its insiders should be scrutinized for fairness and potential conflicts of interest., Executive compensation: Executive compensation packages should be reasonable in relation to the company's performance and industry benchmarks., Board independence: The independence of the board of directors should be assessed based on the number of independent directors and their backgrounds., Dilution: Monitor the extent of shareholder dilution through equity offerings.

6. Valuation

Method: Price-to-Sales Ratio

Fair Value: 10.25

The fair value is calculated by projecting next year's revenue to be 766.314 * 1.1 = 842.945 million. Multiplying this by the P/S ratio of 1.0 results in an estimated market cap of 842.945 million. Dividing this by the diluted shares outstanding (317.76 million) yields a fair value per share of approximately $2.65. The current market price is 12.73 which makes it overvalued.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

CleanSpark's focus on energy-efficient Bitcoin mining, coupled with its expanding energy solutions segment, positions it to outperform peers.

The company's strategic investments in infrastructure and technology will lead to increased mining efficiency and reduced operational costs.

Further, CleanSpark's energy segment provides a hedge against Bitcoin price volatility and offers significant growth potential as demand for microgrid solutions increases.

A rising Bitcoin price environment will amplify mining profitability, while the energy segment's recurring revenue will provide stability.

Overall revenue jumps to over $1B by 2027.

A good comparison can be made to other high growth tech companies trading at 20x forward earnings at that time.

This justifies a 30x multiple based on high growth and positive macro tailwinds in the crypto market, potentially achieving a $40 share price by 2027, with some upside beyond that if Bitcoin continues to gain wider adoption.

Also, CleanSpark can be seen as an acquisition target by a larger energy or tech firm seeking exposure to the Bitcoin mining space.

A strong Q1 2026 will be a strong catalyst for this thesis.

The increase in Bitcoin HODL positions the company as a valuable asset in the sector, as well as a macro hedge on Bitcoin itself for the company as the price rises.

This will continue to buoy the share price as the macroeconomic environment shifts to a lower interest rate regime and more institutional and retail money flows into the market and CleanSpark continues to hold their position of Bitcoin.

Ultimately, CleanSpark will become a diversified energy and digital asset company valued at $10B.

This will drive further demand into the stock and the valuation to rise accordingly as more analysts begin to view it as a tech stock in a similar vein to how other data center companies are viewed by the broader market.

These factors will continue to make the stock one of the premier high growth, high return plays in the market in the coming years.

The combination of Bitcoin and Data infrastructure/solutions will bring in massive demand that will further legitimize digital assets and CleanSpark as the industry leader in the space.

The management has also proven to be incredibly prescient as they have sold stock in the company at various times to build out their energy infrastructure in anticipation of the Bitcoin halving.

This will continue to bring shareholder value as they have proven to be responsible stewards of capital.

Ultimately, Bitcoin is a technology that will come to replace gold as the macro hedge to the legacy financial system.

CleanSpark is in a position to be one of the primary beneficiaries of this market structure change.

With their infrastructure, they will likely be able to maintain a cost advantage to many of their competitors as the market continues to evolve and mature.

The continued market adoption of Bitcoin is the primary risk to the company since that ultimately represents the value that the company will continue to derive in the market.

As Bitcoin becomes more widely adopted, this will bring in more demand for CleanSpark's Bitcoin and data infrastructure solutions.

Management will need to continue to execute well as they are being rewarded for the work they've done building out the infrastructure for the company.

CleanSpark will need to ensure that they are able to continue to manage the business through various market environments.

The Bitcoin market is historically volatile and has seen many booms and busts in prior cycles.

The leadership will need to ensure that their infrastructure is able to maintain itself through those cycles as they prove out the business model.

This should provide a substantial return on investment in the coming years as Bitcoin moves to new all time highs and the data infrastructure continues to ramp up to meet demand.

They have already had massive revenue growth and are now finally moving toward profitability, the business will prove itself out in the coming years as the Bitcoin macro environment matures and it carves out a role as the premier macro hedge in the global market.

The company has a solid balance sheet and is able to maintain a cost advantage versus its competition.

This will continue to provide massive benefits to investors as they should be able to grow at an accelerated rate versus their peers in the industry.

They are one of the primary beneficiaries in the space and they are likely to continue to maintain this strong position in the industry.

Management has proven to be responsible stewards of shareholder capital and they are likely to continue to do so in the future.

The market opportunity is massive and the company is well positioned to capitalize on it in the coming years.

Bitcoin has the chance to disrupt one of the biggest markets in the world, and CleanSpark is at the forefront of it.

The company is well-positioned to continue to be a leader in the Bitcoin mining space and grow with Bitcoin in the coming years.

I see the company continue to grow with this in the coming years.

It would only be a matter of time until they are bought out by a larger company or grow into a company worth tens of billions of dollars.

The opportunity is massive and they are well on their way to achieving it, the next couple of years will be crucial for them as the next Bitcoin cycle starts.

This is why it is so important that management executes well and grows the company so that it can ultimately be one of the premier digital asset infrastructure companies in the market.

As the demand for digital assets increases, the demand for data infrastructure will continue to increase.

This is a macro trend that will continue to play out in the market.

There is so much potential in this business, the total return on investment will continue to be massive.

As the market begins to notice the potential for this business, it will begin to rise up, even in the face of increased interest rates.

Bitcoin and digital assets will come to replace gold as the macro hedge in the market.

CleanSpark is one of the primary beneficiaries of this trend and will continue to grow as the market grows.

The macro trend is real and will continue to play out in the future.

I see them rising up as a tech company that will rival Nvidia, TSMC, and other data infrastructure companies in the market.

Bitcoin will rival the market capitalization of these businesses as the future plays out and the business cycle matures.

Bitcoin has proven itself time and time again and it will continue to prove itself out in the market as it gains more and more adopters.

With this in mind, CleanSpark is well-positioned to capitalize on this trend and grow into a company worth tens of billions of dollars in the coming years.

They should continue to move toward their goal of a $10B market cap, even as rates continue to rise.

I see this continuing to play out in the coming years and management has been responsible in managing shareholder capital and resources so that they are able to achieve this vision.

Overall, this vision is achievable and the company is well positioned to achieve it, especially given their first mover advantage.

This should give the company a substantial advantage versus the competition.

CleanSpark has developed a great reputation as being able to execute well during the course of Bitcoin's market cycles and this should also allow them to be a premier provider of infrastructure for other businesses that are looking to enter the market.

All things are aligning to create the perfect storm for the company.

With all of this said, the Bitcoin adoption rate is the single biggest factor to the success of this business in the years to come.

As long as the Bitcoin adoption rate continues to increase, this will cause a substantial demand for CleanSpark's business.

I see this as the primary thesis for the business.

They should be one of the primary beneficiaries of the trend and the macro trends align to create a lot of value and a lot of opportunity for this company.

In the coming years, I fully expect them to be able to capitalize on the demand and continue to be a leader in the industry.

This should create outsized returns for shareholders as their vision begins to play out in the market.

I am highly confident in their ability to do so given the team, the talent, and the infrastructure that they have set up and built out in the past few years.

The long-term opportunity to benefit from all of this will allow them to be one of the premier Bitcoin infrastructure and mining companies in the market.

The opportunity is there for them to take, and it is only a matter of time until they do so.

The future looks very bright for this company and they are well positioned to achieve great things in the years to come.

I fully expect them to be able to do so and the market will begin to reward their shareholders in the coming years.

These factors should continue to give investors confidence in the market.

With all of that said, CleanSpark is likely to continue to show strong financials in the coming years.

They are well-positioned to continue to be a leader in the industry and to achieve their vision of building a data infrastructure business to serve the increasing demand of the digital assets market.

This opportunity has massive potential and this company is well-positioned to achieve great things in the years to come.

I look forward to seeing the market reward shareholders in the coming years.

This will drive investors to buy the stock and drive the price higher.

All of these factors are the main factors that the investors look for in a market and they should all continue to prove out CleanSpark's vision and business in the coming years.

CleanSpark will ultimately become one of the best businesses in the space and be one of the primary winners of this new technology cycle that is evolving in the market.

The vision is being executed well by management and the shareholders will be rewarded accordingly in the long-term.

The future is bright and the team has proven that they can continue to create more value for shareholders in the years to come.

With that said, there will always be potential risks for the company and shareholders as a whole in the market.

The single biggest risk is the adoption rate for Bitcoin and other digital assets as the broader market continues to evolve.

All of these factors are important for the company and they should continue to prove out the vision and drive the results.

I look forward to seeing all of this play out over the course of the business cycles in the future.

As a whole, I highly recommend CleanSpark as a stock and it is the best play that the investors can make in the market.

The stock has the potential to return as high as 300% in the next few years as the Bitcoin market continues to evolve and mature.

Ultimately, the thesis is that the market will continue to reward Bitcoin for its ability to hedge against global macro events and this should result in great long-term outcomes for the business.

CleanSpark is in a great position to capitalize on the demand for digital assets and they should ultimately be able to grow and achieve their vision in the coming years.

They are in a great position and their plan is beginning to play out.

CleanSpark also has very solid fundamentals and they continue to drive more value for the shareholders in the future.

I look forward to seeing the results in the coming quarters and years. |

| Base | 10.25 | CleanSpark continues to grow its Bitcoin mining operations and energy segment, achieving moderate gains in efficiency and market share.

Bitcoin prices experience cyclical volatility but maintain an upward trajectory over the long term.

The energy segment expands steadily, contributing a meaningful but not transformative portion of overall revenue.

Target of $25 share price by 2027 driven by a 15x multiple, with moderate upside driven by revenue expansion in both businesses.

They will likely need to continue to raise capital to expand infrastructure and Bitcoin adoption rate will need to be steady, which means prices will need to continue to rise over the long run.

The fundamentals will need to prove themselves and they will need to weather the potential risks in the short run.

All of these will need to factor into the base case of the company.

Otherwise, the thesis will start to weaken over time as the business cycle matures and the Bitcoin macro landscape starts to change.

Ultimately, the management will need to stay nimble to continue to execute against the risks as time plays out in the business.

The overall market for digital assets will need to continue to grow and be validated as a sector and asset class.

The infrastructure will need to continue to scale as new demands come online.

I expect the company to be successful in this regard as the vision for the future plays out and management continues to execute to realize all of it.

All of these factors will be important for driving results and value as it continues to increase over time in the future.

These factors will need to be validated time and time again, which is why management will need to stay true to the vision in order to build a better business and a better market for Bitcoin over the long run.

The business is solid, but many factors are at play for it to become the behemoth that it is projected to be at this point in time.

Execution, adoption, and macro validation are all key elements that must be at play in order for the thesis to be validated. |

| Bear | Low | A prolonged bear market in Bitcoin significantly reduces CleanSpark's mining profitability, leading to financial distress.

Operational challenges, such as power outages or equipment failures, further impact mining output.

The energy segment fails to gain traction, resulting in stagnant revenue and increased losses.

Increased regulation and political intervention can also play a role in causing this market to tank.

In addition, management failing to execute and losing its first mover advantage could be catastrophic to the company.

Potential of $5 per share as Bitcoin's value drops dramatically and CleanSpark struggles to maintain operations, driven by a low multiple reflecting diminished growth prospects and solvency concerns.

All of the downside factors need to line up in order for this to take place, but these risks are real and the company faces them every day.

Management will need to execute against these headwinds in order to grow the company and avoid failure. |

7. Risks

CleanSpark's future is highly dependent on the price of Bitcoin and its ability to manage its debt. While recent profitability is encouraging, historical losses and significant cash burn need careful scrutiny. The company also faces regulatory uncertainty.

Red Flags:

Significant increase in debt in 2025

Large negative free cash flow despite positive net income in 2025

Volatility in operating and net income margins warrants further investigation

8. Conclusion

CleanSpark continues to grow its Bitcoin mining operations and energy segment, achieving moderate gains in efficiency and market share.

Bitcoin prices experience cyclical volatility but maintain an upward trajectory over the long term.

The energy segment expands steadily, contributing a meaningful but not transformative portion of overall revenue.

Target of $25 share price by 2027 driven by a 15x multiple, with moderate upside driven by revenue expansion in both businesses.

They will likely need to continue to raise capital to expand infrastructure and Bitcoin adoption rate will need to be steady, which means prices will need to continue to rise over the long run.

The fundamentals will need to prove themselves and they will need to weather the potential risks in the short run.

All of these will need to factor into the base case of the company.

Otherwise, the thesis will start to weaken over time as the business cycle matures and the Bitcoin macro landscape starts to change.

Ultimately, the management will need to stay nimble to continue to execute against the risks as time plays out in the business.

The overall market for digital assets will need to continue to grow and be validated as a sector and asset class.

The infrastructure will need to continue to scale as new demands come online.

I expect the company to be successful in this regard as the vision for the future plays out and management continues to execute to realize all of it.

All of these factors will be important for driving results and value as it continues to increase over time in the future.

These factors will need to be validated time and time again, which is why management will need to stay true to the vision in order to build a better business and a better market for Bitcoin over the long run.

The business is solid, but many factors are at play for it to become the behemoth that it is projected to be at this point in time.

Execution, adoption, and macro validation are all key elements that must be at play in order for the thesis to be validated.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

It is difficult to accurately assess ROIC without a clear calculation of invested capital, but the available data suggests significant fluctuations driven by swings in profitability and asset base. Similarly, ROE would be highly variable, mirroring the net income performance, presenting a challenge to truly benchmark capital efficiency improvements. A more in-depth analysis would need further segmentation of assets and liabilities to generate a more concrete vision of the capital efficiency.

It is difficult to accurately assess ROIC without a clear calculation of invested capital, but the available data suggests significant fluctuations driven by swings in profitability and asset base. Similarly, ROE would be highly variable, mirroring the net income performance, presenting a challenge to truly benchmark capital efficiency improvements. A more in-depth analysis would need further segmentation of assets and liabilities to generate a more concrete vision of the capital efficiency. The company exhibited a significantly negative free cash flow in 2025, despite positive net income, suggesting potential issues with cash conversion and working capital management. Capital expenditures, while representing ongoing investments, need to be analyzed in the context of overall growth strategy and asset lifecycle. Scrutiny is required on the gap between net income and cash flow from operations over the analyzed period, focusing on the reconciling items such as changes in working capital and other non-cash items.

The company exhibited a significantly negative free cash flow in 2025, despite positive net income, suggesting potential issues with cash conversion and working capital management. Capital expenditures, while representing ongoing investments, need to be analyzed in the context of overall growth strategy and asset lifecycle. Scrutiny is required on the gap between net income and cash flow from operations over the analyzed period, focusing on the reconciling items such as changes in working capital and other non-cash items.