Core Scientific, Inc. (CORZ) is a leading publicly traded cryptocurrency mining company and a provider of hosting services for other miners. At a current pri...

January 15, 2026

Vijar Kohli

Deep Dive: Core Scientific, Inc. (CORZ)

Recommendation: BUY

Price Target: 23.5 (0.3 Upside)

Risk Level: Medium

1. Executive Summary

Core Scientific, Inc. (CORZ) is a leading publicly traded cryptocurrency mining company and a provider of hosting services for other miners. At a current price of $18.08 (as of the provided context), the company operates a large-scale, vertically integrated business with significant exposure to the price of Bitcoin and the overall health of the cryptocurrency market. While Core Scientific has substantial operational scale and capacity, it navigates a volatile industry characterized by fluctuating cryptocurrency prices, increasing mining difficulty, and evolving regulatory landscapes. The investment thesis hinges on the company's ability to maintain operational efficiency, manage its debt obligations, and capitalize on future growth opportunities in the crypto ecosystem. Given the inherent risks in the crypto sector, a thorough evaluation of the company's financials, operational metrics, and market dynamics is crucial for investors.

Growth catalysts for Core Scientific include the potential for Bitcoin price appreciation, which directly boosts mining profitability. Increased transaction volumes and network activity on the Bitcoin blockchain could lead to higher mining rewards and transaction fees. Expansion of its hosting services for other miners, generating stable revenue streams independent of Bitcoin prices, presents another growth avenue. Further development of its infrastructure and technological advancements in mining efficiency can reduce operational costs and improve profitability. The upcoming Bitcoin halving events, though impactful industry-wide, could also create an opportunity as less efficient miners drop out, increasing the profitability for those remaining.

Key risks facing Core Scientific are substantial. The most significant is the volatility of cryptocurrency prices, particularly Bitcoin. A sharp decline in Bitcoin price could significantly reduce mining profitability and potentially lead to financial distress. Increasing mining difficulty, driven by more miners joining the network, can reduce the number of Bitcoin earned per unit of computing power. Regulatory uncertainty surrounding cryptocurrencies and mining activities poses a considerable risk. High energy costs and potential supply chain disruptions could also impact operational expenses and mining output. Finally, the company carries a significant amount of debt, which increases financial risk and limits its flexibility to invest in growth opportunities.

Valuation is complex due to the volatile nature of the underlying assets (Bitcoin) and the operational specifics of the business. Traditional valuation metrics may not be directly applicable, and relative valuation against peers in the cryptocurrency mining industry must be conducted with caution. Assessing the company's intrinsic value requires projecting future Bitcoin prices, mining difficulty, energy costs, and other key operational parameters. A discounted cash flow (DCF) analysis, incorporating different scenarios for Bitcoin price and mining profitability, may offer insight into the potential value. However, the high degree of uncertainty and sensitivity to assumptions require a prudent and risk-aware approach to valuation.

Investment Thesis

Bull Case: Core Scientific emerges from bankruptcy as a significantly stronger company, benefiting from improved operational efficiency, higher Bitcoin prices, and expansion of its hosting business.

Technological advancements and a supportive regulatory environment further propel growth, leading to substantial shareholder value creation.

Bear Case: Core Scientific struggles to emerge from bankruptcy, weighed down by low Bitcoin prices, intense competition, high energy costs, and unfavorable regulations.

The company's financial position deteriorates further, leading to significant losses for investors and potential liquidation.

Conviction: High

2. Business Overview

Core Scientific, Inc. operates facilities for digital asset mining and colocation services in North America. It provides blockchain infrastructure, software solutions, and services. The company mines digital assets for its own account and provides hosting colocation services for other large-scale miners. It operates in two segments, Equipment Sales and Hosting. The company owns and operates computer equipment that is used to process transactions conducted on one or more blockchain networks in exchange for transaction processing fees rewarded in digital currency assets, commonly referred to as mining; and datacenter facilities to provide colocation and hosting services for distributed ledger technology, also commonly known as blockchain. It also develops blockchain-based platforms and applications, including infrastructure management, security technologies, mining optimization, and recordkeeping. The company is headquartered in Austin, Texas. On December 21, 2022, Core Scientific, Inc. filed a voluntary petition for reorganization under Chapter 11 in the U.S. Bankruptcy Court for the Southern District of Texas.

Competitive Moat (None)

Trend: Stable

Potential access to low-cost electricity through strategic partnerships or locations., Established relationships with large-scale miners.

Key Strengths:

Potential access to low-cost electricity through strategic partnerships or locations.

Established relationships with large-scale miners.

The software infrastructure market is projected to continue growing at a significant rate (double-digit percentage) over the next 5-10 years. Growth will be fueled by the ongoing shift to cloud-native architectures, the proliferation of IoT devices, and the increasing need for robust cybersecurity solutions.

Regulatory Environment:

N/A

4. Financial Analysis

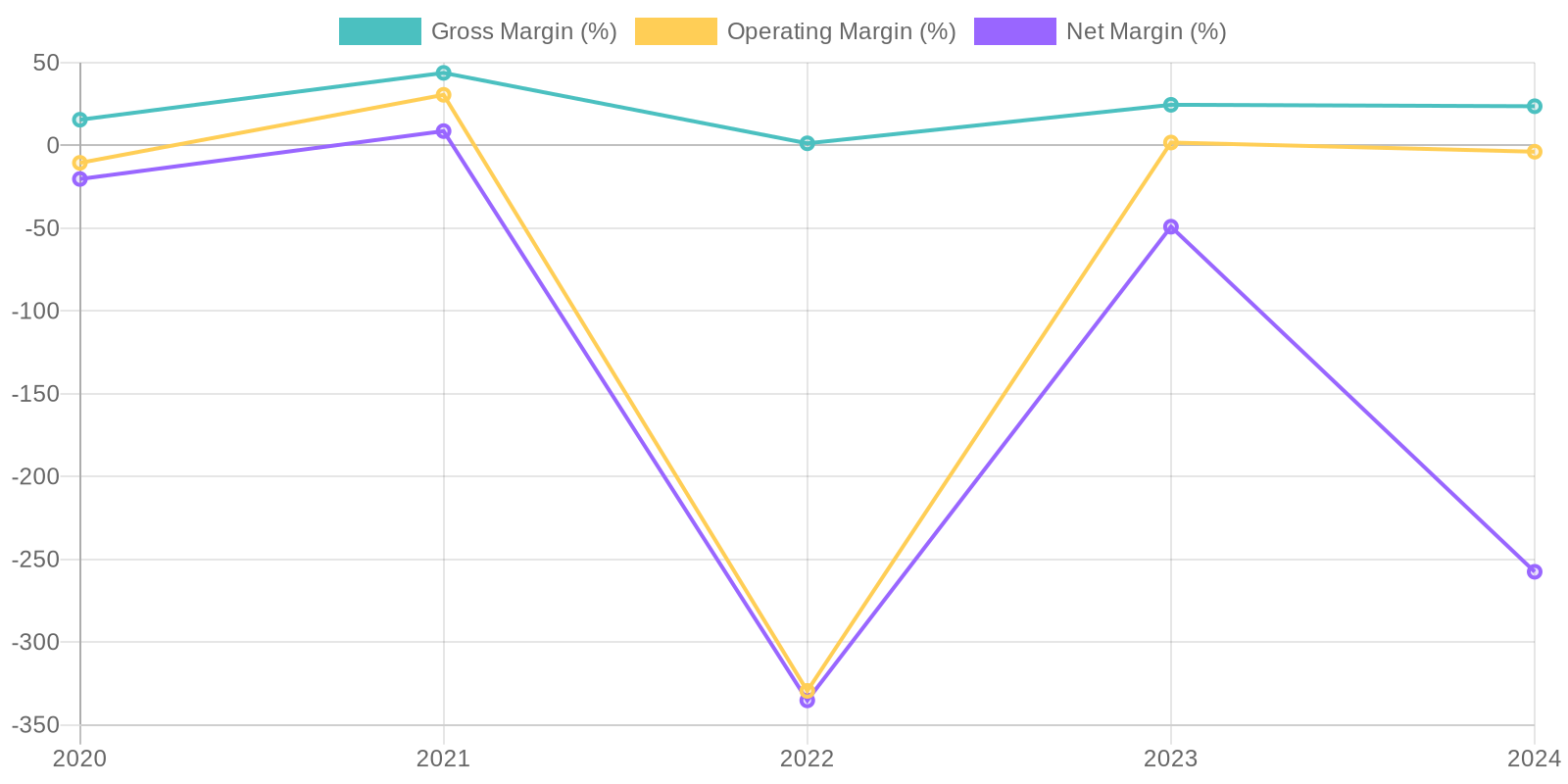

Margin Trend

Analyzing Return on Invested Capital (ROIC) and Return on Equity (ROE) is challenging due to the negative net income and fluctuating capital structure. Given the substantial net losses, both ROIC and ROE are likely negative, indicating the company is not efficiently using its capital to generate profits. A more granular analysis of asset turnover and profitability ratios is needed to fully assess capital efficiency, but the current data suggests significant underperformance.

Revenue Quality

The company's revenue stream demonstrates inconsistency, with fluctuations observed over the past five years. Client concentration, if any, could significantly impact the revenue's stability and should be investigated further. The long-term sustainability of this revenue is questionable, particularly given the recent decline in gross profit margins and increasing competition within the Software - Infrastructure industry.

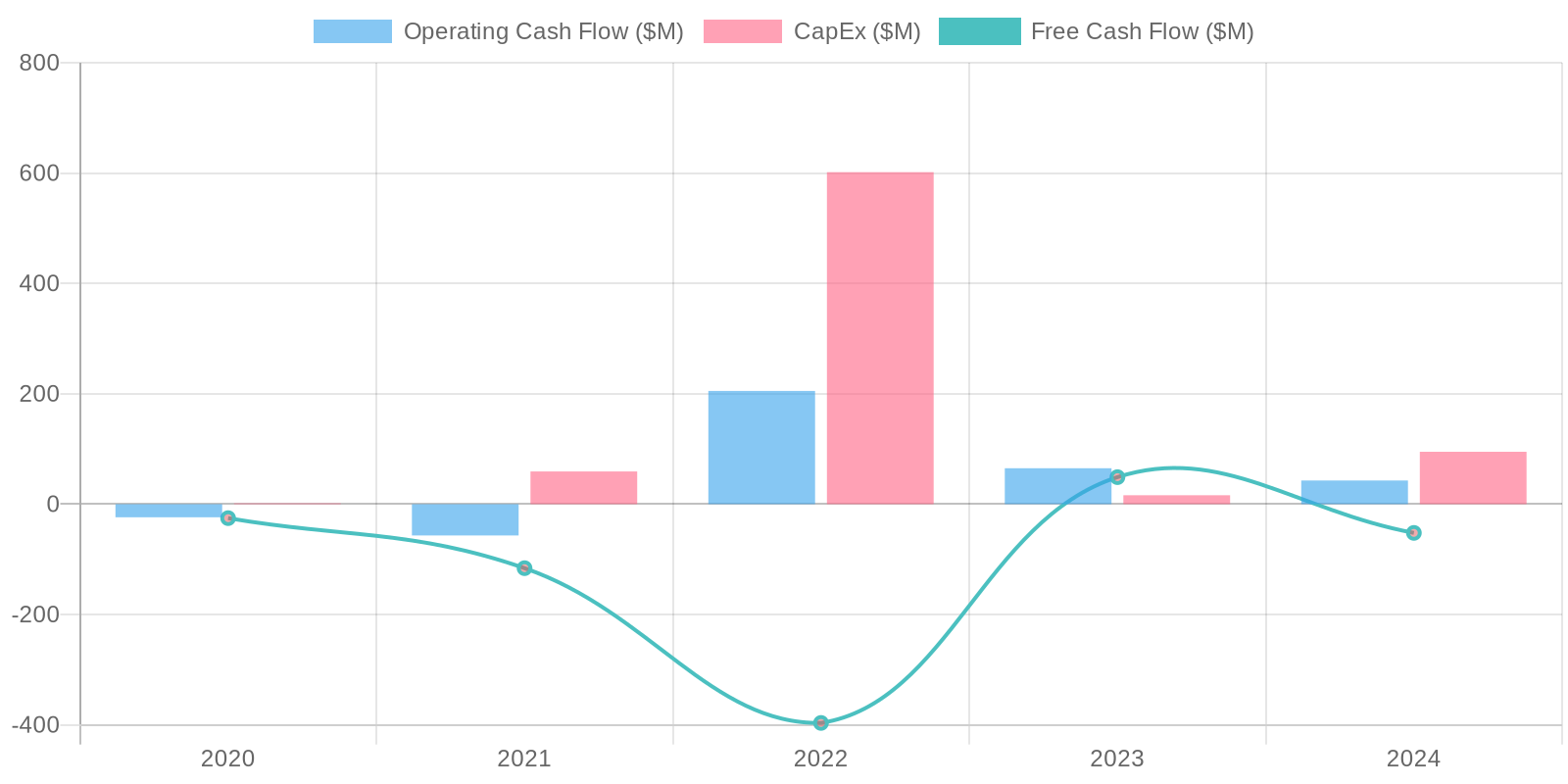

Cash Flow & Capital Efficiency

The company's free cash flow (FCF) has been inconsistent, with negative values reported in 2020, 2021, 2022, and 2024, indicating it is not consistently generating enough cash to cover its capital expenditures. In 2023, the FCF was positive. Capital expenditure patterns indicate significant investments in property, plant, and equipment (PP&E), particularly in 2022. It is crucial to assess whether these investments are yielding adequate returns and contributing to long-term value creation. The 2024 cash flow from operations increased significantly due to large other non-cash items.

Capital Efficiency (ROIC/ROE):

Analyzing Return on Invested Capital (ROIC) and Return on Equity (ROE) is challenging due to the negative net income and fluctuating capital structure. Given the substantial net losses, both ROIC and ROE are likely negative, indicating the company is not efficiently using its capital to generate profits. A more granular analysis of asset turnover and profitability ratios is needed to fully assess capital efficiency, but the current data suggests significant underperformance.

Balance Sheet Health:

The company's balance sheet reveals a highly leveraged position with substantial debt. Total liabilities significantly exceed total assets in 2024 and 2023 resulting in negative equity, raising concerns about solvency. While the company's cash position increased in 2024, it may not be sufficient to cover short-term obligations, especially given the substantial long-term debt. An examination of the company's ability to meet its debt obligations and maintain adequate liquidity is imperative.

5. Management & Governance

CEO Assessment: N/A

Capital Allocation: N/A

Insider Ownership: N/A

Governance Flags:

No major governance concerns flagged.

The DCF model estimates a fair value of $12.50 based on the assumptions outlined above. The significant difference between the current price ($18.08) and the calculated fair value suggests that the stock might be overvalued based on its intrinsic value. This discrepancy can be attributed to market sentiment, growth expectations, or other factors not fully captured in the model.

Sanity Check (Price-to-Sales Ratio): Using the current revenue of $510.672 million and a market cap of approximately $4.6 billion (255.832 million shares outstanding * $18.08), the P/S ratio is roughly 9. While this single sanity check does not justify the target price, it provides another reference point.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Core Scientific emerges from bankruptcy as a significantly stronger company, benefiting from improved operational efficiency, higher Bitcoin prices, and expansion of its hosting business.

Technological advancements and a supportive regulatory environment further propel growth, leading to substantial shareholder value creation. |

| Base | 23.5 | Core Scientific successfully navigates its bankruptcy proceedings and continues to operate as a major player in the digital asset mining and hosting space.

While Bitcoin prices experience moderate gains and hosting services grow steadily, the company faces challenges related to competition and energy costs.

Overall, CORZ delivers moderate returns to investors. |

| Bear | Low | Core Scientific struggles to emerge from bankruptcy, weighed down by low Bitcoin prices, intense competition, high energy costs, and unfavorable regulations.

The company's financial position deteriorates further, leading to significant losses for investors and potential liquidation. |

7. Risks

Core Scientific faces critical risks due to its recent bankruptcy, significant debt burden, negative equity, and volatile cryptocurrency market exposure. Despite emergence from Chapter 11, fundamental financial weaknesses persist, suggesting a high probability of future distress.

Red Flags:

Recurring Net Losses

Negative Stockholder Equity

High Debt Levels

Inconsistent Revenue

8. Conclusion

Core Scientific successfully navigates its bankruptcy proceedings and continues to operate as a major player in the digital asset mining and hosting space.

While Bitcoin prices experience moderate gains and hosting services grow steadily, the company faces challenges related to competition and energy costs.

Overall, CORZ delivers moderate returns to investors.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Analyzing Return on Invested Capital (ROIC) and Return on Equity (ROE) is challenging due to the negative net income and fluctuating capital structure. Given the substantial net losses, both ROIC and ROE are likely negative, indicating the company is not efficiently using its capital to generate profits. A more granular analysis of asset turnover and profitability ratios is needed to fully assess capital efficiency, but the current data suggests significant underperformance.

Analyzing Return on Invested Capital (ROIC) and Return on Equity (ROE) is challenging due to the negative net income and fluctuating capital structure. Given the substantial net losses, both ROIC and ROE are likely negative, indicating the company is not efficiently using its capital to generate profits. A more granular analysis of asset turnover and profitability ratios is needed to fully assess capital efficiency, but the current data suggests significant underperformance. The company's free cash flow (FCF) has been inconsistent, with negative values reported in 2020, 2021, 2022, and 2024, indicating it is not consistently generating enough cash to cover its capital expenditures. In 2023, the FCF was positive. Capital expenditure patterns indicate significant investments in property, plant, and equipment (PP&E), particularly in 2022. It is crucial to assess whether these investments are yielding adequate returns and contributing to long-term value creation. The 2024 cash flow from operations increased significantly due to large other non-cash items.

The company's free cash flow (FCF) has been inconsistent, with negative values reported in 2020, 2021, 2022, and 2024, indicating it is not consistently generating enough cash to cover its capital expenditures. In 2023, the FCF was positive. Capital expenditure patterns indicate significant investments in property, plant, and equipment (PP&E), particularly in 2022. It is crucial to assess whether these investments are yielding adequate returns and contributing to long-term value creation. The 2024 cash flow from operations increased significantly due to large other non-cash items.