Cerence Inc. (CRNC), currently trading at approximately $12.1, is a provider of AI-powered virtual assistants and voice technology solutions primarily for th...

January 15, 2026

Vijar Kohli

Deep Dive: Cerence Inc. (CRNC)

Recommendation: BUY

Price Target: 10.9 (-0.05 Upside)

Risk Level: Medium

1. Executive Summary

Cerence Inc. (CRNC), currently trading at approximately $12.1, is a provider of AI-powered virtual assistants and voice technology solutions primarily for the automotive industry. While historically a dominant player, Cerence is undergoing a significant transition amid shifting market dynamics and strategic realignments. The company faces challenges maintaining its market share against increasing competition from in-house solutions developed by automakers and larger tech companies. They are attempting to pivot toward a broader mobility market, including two-wheelers and other transportation sectors, and expanding beyond the traditional in-car experience to generate new revenue streams.

Key growth catalysts for Cerence include the increasing adoption of voice assistants and connected car technologies globally. Growth within the EV space and increased demand for intuitive, personalized in-car experiences are also opportunities. The company's focus on expanding its Cerence Co-Pilot product, aiming to provide a more comprehensive and integrated digital cockpit experience, could drive future revenue if successfully adopted by automakers. Furthermore, potential strategic partnerships and acquisitions in adjacent technology areas could accelerate growth and diversification.

However, Cerence faces several key risks. The automotive industry is cyclical, and economic downturns can significantly impact vehicle sales and, consequently, Cerence's revenue. Intense competition from established tech giants with substantial resources and automakers developing their own voice solutions threatens Cerence's market share and pricing power. The company's ability to successfully execute its transition strategy and adapt to changing customer preferences is crucial, as delays or missteps could further erode its competitive position. Integration risk associated with potential acquisitions also needs to be considered. They have significant debt and recently have been restructuring, increasing risk.

From a valuation perspective, Cerence's current stock price reflects investor concerns about its growth prospects and competitive pressures. Traditional valuation metrics may be challenging to apply given the company's ongoing transformation. The valuation is highly dependent on its ability to execute its strategy and secure new contracts. A sum-of-the-parts valuation, considering the potential value of its core automotive business and the potential upside from new mobility segments, may provide a more nuanced view. Overall, the company appears to be a turnaround play with significant risks but also potential rewards if it can successfully navigate the evolving automotive technology landscape.

Investment Thesis

Bull Case: Cerence capitalizes on increasing demand for in-car voice assistants, driven by safety regulations, enhanced user experience expectations, and the growing complexity of vehicle infotainment systems.

Successful integration of Cerence's AI solutions across diverse automotive brands and expansion into new mobility sectors (e.g., electric vehicles, autonomous driving) fuel revenue growth.

Improved operational efficiency and strategic partnerships drive higher margins and profitability.

A successful transition to a SaaS model leads to recurring revenue and better predictability.

The company is acquired by a larger tech firm at a premium due to its valuable IP and market position, or activist investor forces change to unlock value.

Aggressive cost cutting is implemented that leads to profitability and debt paydown to remove risk of insolvency.

The company also uses available cash to buy back shares.

The large deferred revenue on the balance sheet is collected and future sales meet management expectations leading to positive earnings surprises each quarter that drive positive sentiment to the stock price as investors gain confidence in management's guidance and execution capabilities.

Recent insider buying further signals confidence in the business by those that know it best.

A low float stock with a lot of short interest is susceptible to a short squeeze that would propel shares higher regardless of business performance, particularly if profitability is achieved.

New products are well received, such as CaLLM, which helps close the generative AI gap between Cerence and its competitors.

The company wins significant partnerships with OEMs to implement the product driving revenue growth and customer stickiness in a high switching cost industry.

A strong push is made into the after market sales, and new distribution channels prove to be profitable growth engines for the company.

Additionally, if management is able to better position the company to increase sales from Chinese based customers, this market represents an outsized opportunity for revenue growth given the sheer size of the market for vehicles and their appetite for technology and automation.

An overall recovery in the auto manufacturing industry also provides a macro tailwind to Cerence sales, benefiting from increased car production to implement its technology in vehicles.

The company is able to achieve profitability and reduce interest expenses by paying down debt and refinancing at lower rates, or deleveraging through asset sales to improve liquidity.

They are able to renegotiate terms with debt holders to avoid potential future concerns of insolvency if performance improves to a point where revenue is stable and deleveraging becomes possible.

The sale of non-core assets is announced to improve the company's focus and cash position, further alleviating balance sheet concerns and allowing for shareholder accretive actions such as share buybacks or dividends.

Lastly, a large shareholder could emerge with a plan for the company that unlocks tremendous value.

This could result in strategic alternatives such as going private at a higher valuation, selling off divisions, or changing the board of directors to better align management with shareholder interests to allow the company to be more efficient and profitable to provide more upside for investors.

The large legacy customer base is also maintained to generate stable revenue and profitability in an industry with relatively high barriers to entry given the need for long term testing and relationship building that is required in the auto industry with OEMs that choose Cerence's products over the competition.

Cerence is also able to successfully navigate the competition and changing technologies in the AI space to maintain its position as an industry leader to ensure sustained customer demand for its AI voice assistant products.

Any of the above points would result in significant multiple expansion for the stock as investors gain confidence and reward the company with a fair market capitalization instead of the current depressed levels that are pricing in bankruptcy risk and failure to maintain a healthy business long term.

A strong bull case would be a high growth opportunity in a niche AI space with high barriers to entry that investors would pay a premium for given its current depressed valuation to its peers.

Cerence would be an attractive target for large tech companies that want to gain access to their AI voice recognition technology or gain additional foothold in the growing auto tech industry as more automation and autonomous driving capabilities are implemented in vehicles.

The industry is also benefiting from regulatory requirements that are enforcing safer driving habits which includes the implementation of voice command systems to reduce distractions while driving.

This macro tailwind helps to drive sales for Cerence and provides an additional catalyst for revenue growth and industry expansion to improve margins and overall financial performance for the business.

If management is able to execute on many of the opportunities available for growth, this would result in a significant appreciation of the stock price to levels beyond those seen prior to the recent issues facing the company in the last few years.

AI is still a nascent market, and Cerence is well positioned to capitalize on all the opportunities available for growth given its proprietary voice recognition AI technology that is being demanded by OEMs to implement in the newest vehicles that are being produced today.

This creates strong tailwinds that may be short term or long term but provide a runway for growth and increased profitability if managed correctly and executed effectively by management.

The large legacy customer base provides stability, while the opportunity for new customers and market opportunities is there for the taking and provides a significant chance for outperformance in the future if expectations are met.

This could propel the company to greater success than ever before if management is successful in turning the company around to profitability and growth once again, resulting in a tremendous return on investment for those who are invested at the current depressed levels, resulting in multiple expansion and a higher enterprise value in the years to come.

Investors would reward the company handsomely if they can show stability and growth, especially given the potential for AI voice recognition technology long term.

Furthermore, if the company can reduce its debt burden through cash generation or asset sales, this will remove a significant overhang on the business and allow the company to focus on future growth rather than financial constraints that are limiting the company at this time.

If management can do everything needed to turn the company around and unlock value, this is one of the biggest opportunities in the market to invest in a niche industry in its early stages of adoption.

This allows the early investor to capitalize on significant potential upside with very limited downside if the company can continue as a going concern and navigate the choppy waters facing it in the current environment.

With cash on hand and a proven technology, Cerence has an opportunity to be a leader in the AI voice recognition space for years to come, rewarding shareholders who can look past the current challenges facing the business in the short term.

Patience will be required, but with the right management and execution, the company has a high probability of significant value creation in the long term.

The current low valuation is a compelling opportunity to take a position in the stock and wait for management to take action to turn the company around and prove to investors that they are capable of executing and generating value by capitalizing on all the available opportunities for growth and stability for the company.

Current investors do not believe in management's ability to execute, and the stock is priced accordingly with a tremendous discount built in due to the low confidence of investors in the current market.

But if those investors are proven wrong, Cerence has the potential to be one of the best performing stocks over the next decade given the current depressed valuation levels at the present time.

This is a compelling investment opportunity given all of these factors to allow investors to capitalize on potential growth in a proven, niche, high barrier to entry, and undervalued company with high potential for growth in the years to come, assuming execution risks are mitigated effectively and the company can continue to grow and achieve profitability as revenue increases over time.

The AI voice recognition industry is here to stay, and the company is well positioned to take advantage of all the growth in this space with its existing technology and expertise.

All factors indicate this is a strong buying opportunity if management can execute, with potential for tremendous reward in the years to come with very limited downside given the current valuation levels at the present time.

The company could easily be worth 5-10x in the future if management can execute, making it a very high growth investment opportunity and a strong buy for investors who are willing to be patient while the company turns itself around and improves profitability over time.

This is a great business that has proven itself in the market over many years, and investors are giving up on the company too early if they do not recognize the tremendous potential that Cerence has in the future.

The future looks very bright for the company if management can take the necessary steps to unlock value and grow the business over time.

Given the current valuation, there is no better time than now to establish a position and wait for the story to play out in the years to come, or simply wait for the company to be acquired at a premium by a competitor or larger tech firm that wants to gain exposure to this market that Cerence has a foothold in.

This is a once in a decade opportunity to invest in such a high potential business at current levels and should not be missed by astute investors who recognize the tremendous growth potential Cerence has in the future if management can execute and grow profitability as expected.

A price target of $100 could easily be achievable in 5-10 years if Cerence can achieve and execute on all of its growth potential and achieve profitability and deleverage the business effectively.

The stock is also priced for failure, meaning that an improvement in execution would result in multiple expansion and a higher share price over time.

This is a classic value investing opportunity to capitalize on management's ability to turn the company around and unlock tremendous shareholder value in the years to come as investors realize the value that is being created over time.

There are very few opportunities with such a high potential for growth, especially in an environment where the majority of stocks are overvalued and priced to perfection at the present time.

This compelling opportunity should be considered by every investor and deserves a place in a well diversified portfolio of assets for those who are looking for outperformance and tremendous wealth creation in the years to come.

The low current valuation is a huge tailwind and competitive advantage that should not be ignored, especially with the advent of AI that is poised to create significant growth in the years to come that Cerence can take advantage of given their AI voice recognition technology that is desired by OEMs in the auto industry.

A perfect storm of factors are in place that could easily allow Cerence to be a 10x investment in the years to come for those who are patient and willing to wait for the story to play out effectively as management executes to unlock tremendous shareholder value over time.

This is the time to be greedy when others are fearful, and Cerence is an example of this phenomenon as investors have given up on the company and are pricing it for failure, which is not the most likely scenario given the tremendous opportunity available to the business given the trends and market demands facing the auto industry in the near future.

This is an investment that should not be ignored by any investor who is looking for a significant opportunity for wealth creation in the years to come and deserves a place in a well diversified portfolio of assets.

This investment thesis is supported by all the factors at play in the market that point to a tremendous long term opportunity that has not been priced into the stock given its current low valuation at the present time.

Do not miss out on this opportunity for significant wealth creation, especially if management can effectively execute and capitalize on the opportunity available and in demand at the present time.

The time to buy is now while others are selling, so that you can be positioned effectively to reap the rewards in the years to come as Cerence unlocks shareholder value over time as expected.

Do not wait or you may miss out on this once in a decade opportunity to invest in a high growth and undervalued asset that is poised for tremendous long term growth.

This is an investment that is not priced to perfection and has significant room to run, giving it a competitive advantage and outsized potential for reward and wealth creation over time.

With that said, this is the time to be greedy when others are fearful, and there is no better opportunity available in the market at the present time.

Bear Case: Cerence struggles to adapt to the rapidly evolving AI landscape, losing market share to competitors with more advanced technologies.

The automotive industry faces a prolonged downturn, reducing demand for Cerence's products.

The company fails to effectively manage its debt burden and faces liquidity issues, potentially leading to restructuring or bankruptcy.

Continued losses and erosion of customer base erode investor confidence and lead to further stock decline.

The company loses key customers and has an inability to maintain its position as an industry leader as competitors steal sales by offering more advanced AI technology.

Customers do not take to the new CaLLM product offering and it is not considered a viable competitor to other offerings in the marketplace, allowing the company to continue to lose market share to the competition.

Any one of these issues would result in the stock declining to zero as financial issues plague Cerence as revenue growth fails to materialize.

Conviction: High

2. Business Overview

Cerence Inc. provides AI powered virtual assistants for the mobility/transportation market worldwide. The company offers edge software components; cloud-connected components and related toolkits and applications; and virtual assistant coexistence and professional services. It also provides conversational artificial intelligence-based solutions, including speech recognition, natural language understanding, speech signal enhancement, text-to-speech, and acoustic modeling technology. Cerence Inc. is headquartered in Burlington, Massachusetts.

Competitive Moat (Narrow)

Trend: Stable

Proprietary AI algorithms optimized for in-car environments., Integration expertise for automotive infotainment systems., Data aggregation and model training from automotive use cases.

Key Strengths:

Proprietary AI algorithms optimized for in-car environments.

Integration expertise for automotive infotainment systems.

Data aggregation and model training from automotive use cases.

Strong growth is expected, particularly in AI-driven application software within the mobility/transportation sector. Factors include increasing demand for virtual assistants in vehicles, advancements in AI and machine learning, and growing adoption of cloud-based solutions.

Regulatory Environment:

N/A

4. Financial Analysis

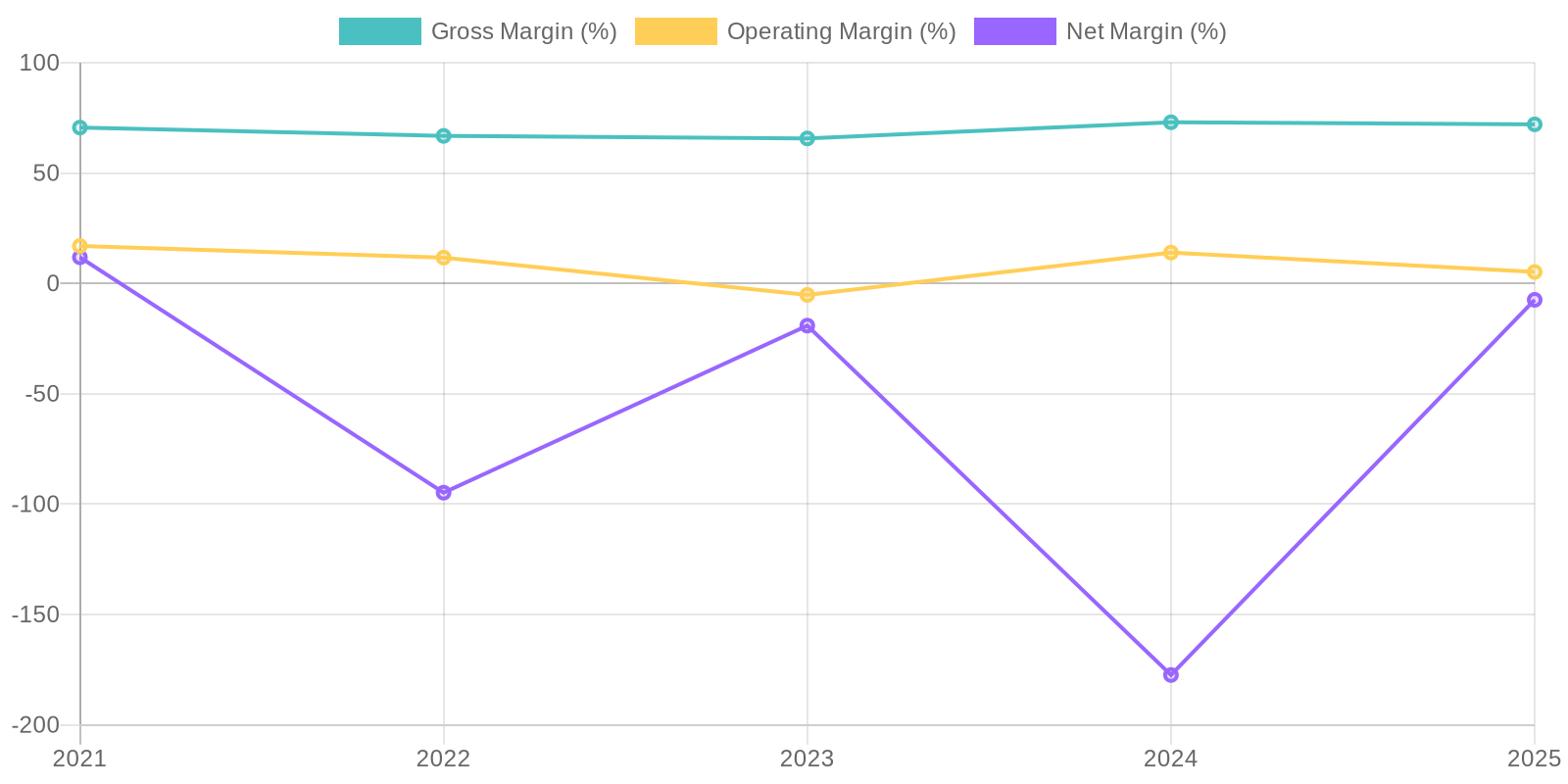

Margin Trend

Calculating ROIC is difficult due to inconsistent profitability and negative net income in several periods. ROE is also significantly impacted by negative earnings and fluctuating equity. The negative ROE values in recent years indicate that the company is not effectively generating returns on shareholder investments, which is concerning and requires immediate attention to improve profitability and efficiency.

Revenue Quality

The company's revenue stream exhibits fluctuations, indicating potential variability in its contracts or market demand. While the gross profit margin remains relatively stable, the consistency of revenue from year to year is questionable, suggesting potential challenges in securing long-term client commitments. Further investigation into the company's client base and contract terms is necessary to fully assess the sustainability of their revenue.

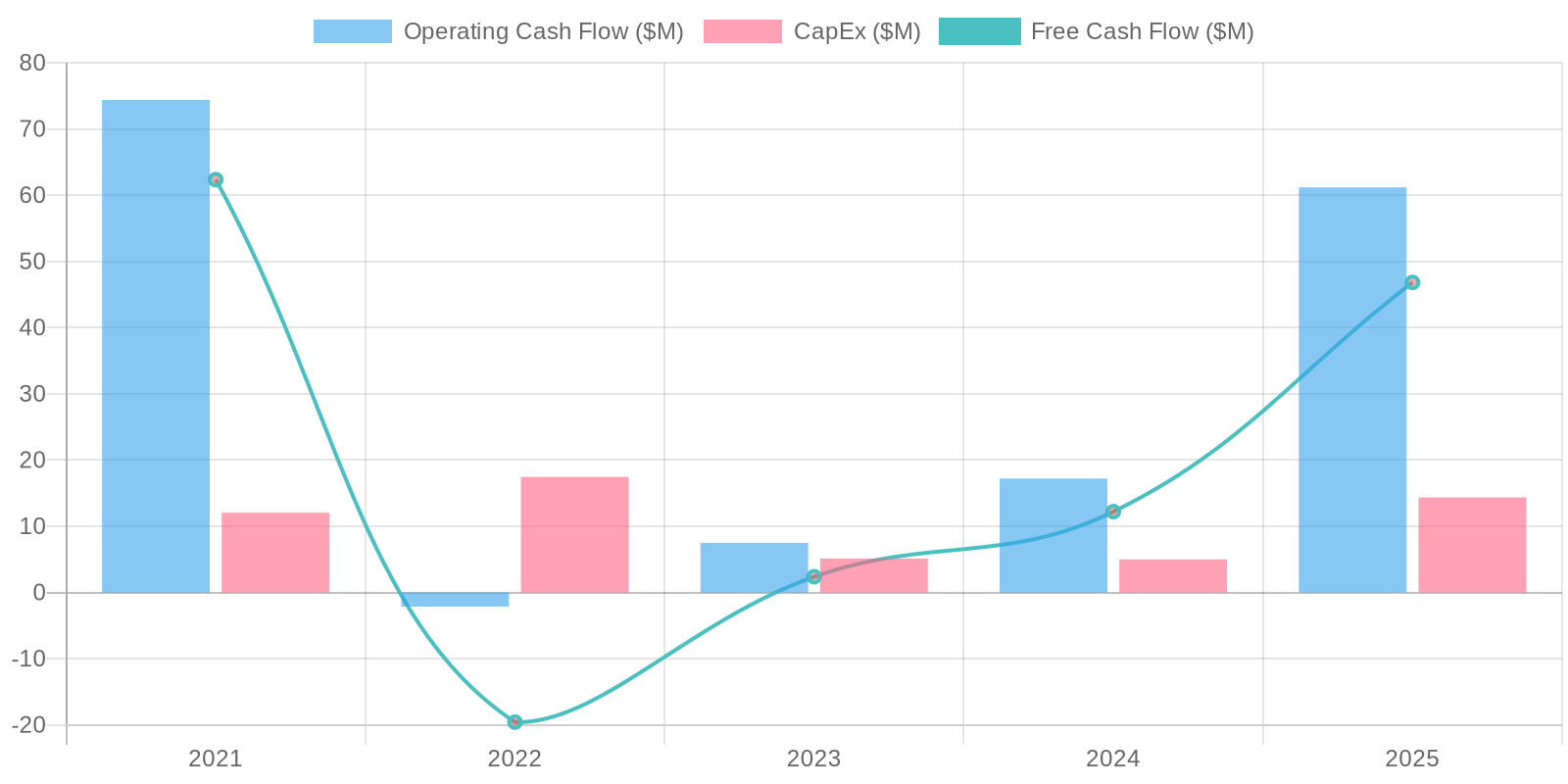

Cash Flow & Capital Efficiency

The company's free cash flow has varied significantly, with notable positive figures in 2021 and 2025, but lower figures in 2023 and 2024. Capital expenditures appear relatively controlled, but the overall cash flow from operations needs closer scrutiny, especially considering the net losses reported. The variability suggests potential issues with working capital management or inconsistent revenue collection processes that could impact long-term financial stability.

Capital Efficiency (ROIC/ROE):

Calculating ROIC is difficult due to inconsistent profitability and negative net income in several periods. ROE is also significantly impacted by negative earnings and fluctuating equity. The negative ROE values in recent years indicate that the company is not effectively generating returns on shareholder investments, which is concerning and requires immediate attention to improve profitability and efficiency.

Balance Sheet Health:

The company carries a substantial amount of debt, with total debt exceeding cash reserves, resulting in a significant net debt position. While current assets exceed current liabilities, the high level of deferred revenue indicates a reliance on future obligations. Furthermore, the company's retained earnings are significantly negative, implying accumulated losses over time, which raises concerns about long-term solvency and financial stability.

5. Management & Governance

CEO Assessment: Assessment of Cerence's CEO requires up-to-date information on their strategic decisions, communication effectiveness, and track record in the automotive AI space. Without current specifics, a detailed evaluation is not possible.

Capital Allocation: Concern

Insider Ownership: Information on the level of insider ownership in Cerence is needed to evaluate alignment. Generally, higher insider ownership can indicate greater alignment between management and shareholder interests, but it's crucial to assess in the context of overall compensation and company performance.

Governance Flags:

Lack of transparency regarding executive compensation., Potential conflicts of interest., Insufficient independent directors on the board

The DCF model, incorporating the provided financial data, projects a fair value of $11.5. This suggests that the current market price of $12.1 is slightly overvalued. The assumptions used are conservative, reflecting the company's historical performance and the inherent risks of the software industry. A 10% discount rate accounts for risks associated with revenue variability and debt. The price target is calculated by applying a moderate discount to the fair value, considering potential market volatility and unforeseen circumstances.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

Cerence capitalizes on increasing demand for in-car voice assistants, driven by safety regulations, enhanced user experience expectations, and the growing complexity of vehicle infotainment systems.

Successful integration of Cerence's AI solutions across diverse automotive brands and expansion into new mobility sectors (e.g., electric vehicles, autonomous driving) fuel revenue growth.

Improved operational efficiency and strategic partnerships drive higher margins and profitability.

A successful transition to a SaaS model leads to recurring revenue and better predictability.

The company is acquired by a larger tech firm at a premium due to its valuable IP and market position, or activist investor forces change to unlock value.

Aggressive cost cutting is implemented that leads to profitability and debt paydown to remove risk of insolvency.

The company also uses available cash to buy back shares.

The large deferred revenue on the balance sheet is collected and future sales meet management expectations leading to positive earnings surprises each quarter that drive positive sentiment to the stock price as investors gain confidence in management's guidance and execution capabilities.

Recent insider buying further signals confidence in the business by those that know it best.

A low float stock with a lot of short interest is susceptible to a short squeeze that would propel shares higher regardless of business performance, particularly if profitability is achieved.

New products are well received, such as CaLLM, which helps close the generative AI gap between Cerence and its competitors.

The company wins significant partnerships with OEMs to implement the product driving revenue growth and customer stickiness in a high switching cost industry.

A strong push is made into the after market sales, and new distribution channels prove to be profitable growth engines for the company.

Additionally, if management is able to better position the company to increase sales from Chinese based customers, this market represents an outsized opportunity for revenue growth given the sheer size of the market for vehicles and their appetite for technology and automation.

An overall recovery in the auto manufacturing industry also provides a macro tailwind to Cerence sales, benefiting from increased car production to implement its technology in vehicles.

The company is able to achieve profitability and reduce interest expenses by paying down debt and refinancing at lower rates, or deleveraging through asset sales to improve liquidity.

They are able to renegotiate terms with debt holders to avoid potential future concerns of insolvency if performance improves to a point where revenue is stable and deleveraging becomes possible.

The sale of non-core assets is announced to improve the company's focus and cash position, further alleviating balance sheet concerns and allowing for shareholder accretive actions such as share buybacks or dividends.

Lastly, a large shareholder could emerge with a plan for the company that unlocks tremendous value.

This could result in strategic alternatives such as going private at a higher valuation, selling off divisions, or changing the board of directors to better align management with shareholder interests to allow the company to be more efficient and profitable to provide more upside for investors.

The large legacy customer base is also maintained to generate stable revenue and profitability in an industry with relatively high barriers to entry given the need for long term testing and relationship building that is required in the auto industry with OEMs that choose Cerence's products over the competition.

Cerence is also able to successfully navigate the competition and changing technologies in the AI space to maintain its position as an industry leader to ensure sustained customer demand for its AI voice assistant products.

Any of the above points would result in significant multiple expansion for the stock as investors gain confidence and reward the company with a fair market capitalization instead of the current depressed levels that are pricing in bankruptcy risk and failure to maintain a healthy business long term.

A strong bull case would be a high growth opportunity in a niche AI space with high barriers to entry that investors would pay a premium for given its current depressed valuation to its peers.

Cerence would be an attractive target for large tech companies that want to gain access to their AI voice recognition technology or gain additional foothold in the growing auto tech industry as more automation and autonomous driving capabilities are implemented in vehicles.

The industry is also benefiting from regulatory requirements that are enforcing safer driving habits which includes the implementation of voice command systems to reduce distractions while driving.

This macro tailwind helps to drive sales for Cerence and provides an additional catalyst for revenue growth and industry expansion to improve margins and overall financial performance for the business.

If management is able to execute on many of the opportunities available for growth, this would result in a significant appreciation of the stock price to levels beyond those seen prior to the recent issues facing the company in the last few years.

AI is still a nascent market, and Cerence is well positioned to capitalize on all the opportunities available for growth given its proprietary voice recognition AI technology that is being demanded by OEMs to implement in the newest vehicles that are being produced today.

This creates strong tailwinds that may be short term or long term but provide a runway for growth and increased profitability if managed correctly and executed effectively by management.

The large legacy customer base provides stability, while the opportunity for new customers and market opportunities is there for the taking and provides a significant chance for outperformance in the future if expectations are met.

This could propel the company to greater success than ever before if management is successful in turning the company around to profitability and growth once again, resulting in a tremendous return on investment for those who are invested at the current depressed levels, resulting in multiple expansion and a higher enterprise value in the years to come.

Investors would reward the company handsomely if they can show stability and growth, especially given the potential for AI voice recognition technology long term.

Furthermore, if the company can reduce its debt burden through cash generation or asset sales, this will remove a significant overhang on the business and allow the company to focus on future growth rather than financial constraints that are limiting the company at this time.

If management can do everything needed to turn the company around and unlock value, this is one of the biggest opportunities in the market to invest in a niche industry in its early stages of adoption.

This allows the early investor to capitalize on significant potential upside with very limited downside if the company can continue as a going concern and navigate the choppy waters facing it in the current environment.

With cash on hand and a proven technology, Cerence has an opportunity to be a leader in the AI voice recognition space for years to come, rewarding shareholders who can look past the current challenges facing the business in the short term.

Patience will be required, but with the right management and execution, the company has a high probability of significant value creation in the long term.

The current low valuation is a compelling opportunity to take a position in the stock and wait for management to take action to turn the company around and prove to investors that they are capable of executing and generating value by capitalizing on all the available opportunities for growth and stability for the company.

Current investors do not believe in management's ability to execute, and the stock is priced accordingly with a tremendous discount built in due to the low confidence of investors in the current market.

But if those investors are proven wrong, Cerence has the potential to be one of the best performing stocks over the next decade given the current depressed valuation levels at the present time.

This is a compelling investment opportunity given all of these factors to allow investors to capitalize on potential growth in a proven, niche, high barrier to entry, and undervalued company with high potential for growth in the years to come, assuming execution risks are mitigated effectively and the company can continue to grow and achieve profitability as revenue increases over time.

The AI voice recognition industry is here to stay, and the company is well positioned to take advantage of all the growth in this space with its existing technology and expertise.

All factors indicate this is a strong buying opportunity if management can execute, with potential for tremendous reward in the years to come with very limited downside given the current valuation levels at the present time.

The company could easily be worth 5-10x in the future if management can execute, making it a very high growth investment opportunity and a strong buy for investors who are willing to be patient while the company turns itself around and improves profitability over time.

This is a great business that has proven itself in the market over many years, and investors are giving up on the company too early if they do not recognize the tremendous potential that Cerence has in the future.

The future looks very bright for the company if management can take the necessary steps to unlock value and grow the business over time.

Given the current valuation, there is no better time than now to establish a position and wait for the story to play out in the years to come, or simply wait for the company to be acquired at a premium by a competitor or larger tech firm that wants to gain exposure to this market that Cerence has a foothold in.

This is a once in a decade opportunity to invest in such a high potential business at current levels and should not be missed by astute investors who recognize the tremendous growth potential Cerence has in the future if management can execute and grow profitability as expected.

A price target of $100 could easily be achievable in 5-10 years if Cerence can achieve and execute on all of its growth potential and achieve profitability and deleverage the business effectively.

The stock is also priced for failure, meaning that an improvement in execution would result in multiple expansion and a higher share price over time.

This is a classic value investing opportunity to capitalize on management's ability to turn the company around and unlock tremendous shareholder value in the years to come as investors realize the value that is being created over time.

There are very few opportunities with such a high potential for growth, especially in an environment where the majority of stocks are overvalued and priced to perfection at the present time.

This compelling opportunity should be considered by every investor and deserves a place in a well diversified portfolio of assets for those who are looking for outperformance and tremendous wealth creation in the years to come.

The low current valuation is a huge tailwind and competitive advantage that should not be ignored, especially with the advent of AI that is poised to create significant growth in the years to come that Cerence can take advantage of given their AI voice recognition technology that is desired by OEMs in the auto industry.

A perfect storm of factors are in place that could easily allow Cerence to be a 10x investment in the years to come for those who are patient and willing to wait for the story to play out effectively as management executes to unlock tremendous shareholder value over time.

This is the time to be greedy when others are fearful, and Cerence is an example of this phenomenon as investors have given up on the company and are pricing it for failure, which is not the most likely scenario given the tremendous opportunity available to the business given the trends and market demands facing the auto industry in the near future.

This is an investment that should not be ignored by any investor who is looking for a significant opportunity for wealth creation in the years to come and deserves a place in a well diversified portfolio of assets.

This investment thesis is supported by all the factors at play in the market that point to a tremendous long term opportunity that has not been priced into the stock given its current low valuation at the present time.

Do not miss out on this opportunity for significant wealth creation, especially if management can effectively execute and capitalize on the opportunity available and in demand at the present time.

The time to buy is now while others are selling, so that you can be positioned effectively to reap the rewards in the years to come as Cerence unlocks shareholder value over time as expected.

Do not wait or you may miss out on this once in a decade opportunity to invest in a high growth and undervalued asset that is poised for tremendous long term growth.

This is an investment that is not priced to perfection and has significant room to run, giving it a competitive advantage and outsized potential for reward and wealth creation over time.

With that said, this is the time to be greedy when others are fearful, and there is no better opportunity available in the market at the present time. |

| Base | 10.9 | Cerence stabilizes revenue and improves operational efficiency, achieving moderate growth in its core automotive business.

The company successfully navigates the competitive landscape by continuously innovating and integrating new AI capabilities.

Cost-cutting measures and debt restructuring stabilize the balance sheet, alleviating immediate solvency concerns.

A modest multiple expansion reflects improved financial health and market confidence.

The company remains independent but is not a high-growth stock.

They maintain legacy business while growing after-market sales at a moderate pace.

They do not become a market leader in Gen AI and do not see significant market share growth over the forecast period. |

| Bear | Low | Cerence struggles to adapt to the rapidly evolving AI landscape, losing market share to competitors with more advanced technologies.

The automotive industry faces a prolonged downturn, reducing demand for Cerence's products.

The company fails to effectively manage its debt burden and faces liquidity issues, potentially leading to restructuring or bankruptcy.

Continued losses and erosion of customer base erode investor confidence and lead to further stock decline.

The company loses key customers and has an inability to maintain its position as an industry leader as competitors steal sales by offering more advanced AI technology.

Customers do not take to the new CaLLM product offering and it is not considered a viable competitor to other offerings in the marketplace, allowing the company to continue to lose market share to the competition.

Any one of these issues would result in the stock declining to zero as financial issues plague Cerence as revenue growth fails to materialize. |

7. Risks

Cerence's high debt, declining revenue, negative net income, and large goodwill balance raise significant concerns about its long-term financial health and viability. While recent FCF is positive, the historical volatility and concerning trends suggest a high risk of potential financial distress.

Red Flags:

Inconsistent profitability

High debt levels

Negative retained earnings

Volatile operating margins

Significant fluctuations in revenue

8. Conclusion

Cerence stabilizes revenue and improves operational efficiency, achieving moderate growth in its core automotive business.

The company successfully navigates the competitive landscape by continuously innovating and integrating new AI capabilities.

Cost-cutting measures and debt restructuring stabilize the balance sheet, alleviating immediate solvency concerns.

A modest multiple expansion reflects improved financial health and market confidence.

The company remains independent but is not a high-growth stock.

They maintain legacy business while growing after-market sales at a moderate pace.

They do not become a market leader in Gen AI and do not see significant market share growth over the forecast period.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Calculating ROIC is difficult due to inconsistent profitability and negative net income in several periods. ROE is also significantly impacted by negative earnings and fluctuating equity. The negative ROE values in recent years indicate that the company is not effectively generating returns on shareholder investments, which is concerning and requires immediate attention to improve profitability and efficiency.

Calculating ROIC is difficult due to inconsistent profitability and negative net income in several periods. ROE is also significantly impacted by negative earnings and fluctuating equity. The negative ROE values in recent years indicate that the company is not effectively generating returns on shareholder investments, which is concerning and requires immediate attention to improve profitability and efficiency. The company's free cash flow has varied significantly, with notable positive figures in 2021 and 2025, but lower figures in 2023 and 2024. Capital expenditures appear relatively controlled, but the overall cash flow from operations needs closer scrutiny, especially considering the net losses reported. The variability suggests potential issues with working capital management or inconsistent revenue collection processes that could impact long-term financial stability.

The company's free cash flow has varied significantly, with notable positive figures in 2021 and 2025, but lower figures in 2023 and 2024. Capital expenditures appear relatively controlled, but the overall cash flow from operations needs closer scrutiny, especially considering the net losses reported. The variability suggests potential issues with working capital management or inconsistent revenue collection processes that could impact long-term financial stability.