CoreWeave, Inc. (CRWV), currently trading at $95.01, operates in the rapidly expanding high-performance computing (HPC) cloud infrastructure space, primarily...

January 15, 2026

Vijar Kohli

Deep Dive: CoreWeave, Inc. Class A Common Stock (CRWV)

Recommendation: BUY

Price Target: 74.25 (0.1 Upside)

Risk Level: Medium

1. Executive Summary

CoreWeave, Inc. (CRWV), currently trading at $95.01, operates in the rapidly expanding high-performance computing (HPC) cloud infrastructure space, primarily catering to artificial intelligence (AI) and machine learning (ML) workloads. The company has rapidly established itself as a significant player, offering specialized compute resources optimized for demanding applications. Its market position is strengthened by strong relationships with key AI ecosystem partners, including NVIDIA, and by a focus on providing cost-effective and scalable solutions for compute-intensive tasks.

Growth catalysts for CoreWeave are primarily driven by the explosive demand for AI and ML infrastructure. The continued development and deployment of large language models (LLMs), generative AI applications, and other advanced AI technologies require substantial computational power, creating a sustained need for CoreWeave's services. Further growth will be fueled by geographic expansion, service diversification (e.g., expanding into areas like rendering and data analytics), and strategic partnerships that broaden its reach and service offerings. The increasing adoption of cloud-based solutions over on-premise infrastructure for AI/ML is also a strong tailwind.

Key risks facing CoreWeave include intense competition from established cloud providers like Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform (GCP), all of which possess significantly greater resources and broader customer bases. Technological advancements and shifts in AI/ML hardware and software could render CoreWeave's current infrastructure less competitive, necessitating continuous investment in upgrades and innovation. Additionally, reliance on key suppliers like NVIDIA poses a supply chain risk. Economic downturns could impact customer spending on AI/ML initiatives, reducing demand for CoreWeave's services. Regulatory scrutiny regarding AI and data privacy could also introduce operational and financial challenges.

Valuation of CoreWeave is complex due to its rapid growth and limited historical financial data. A simplified valuation summary suggests that its current valuation is predicated on continued hypergrowth in the AI infrastructure market and CoreWeave's ability to maintain its competitive edge and market share. Future profitability is a crucial determinant, as is its ability to attract and retain talent in the competitive AI/ML field. Public market comparables are not a perfect fit, as many peers have broader service portfolios, but some analysis can be inferred based on growth rates, margins, and scalability metrics of comparable AI-related companies. A more thorough valuation would require detailed financial projections, sensitivity analysis to various growth scenarios, and a comprehensive assessment of CoreWeave's long-term competitive advantages.

Investment Thesis

Bull Case: CoreWeave will emerge as the leading infrastructure provider for GenAI, driven by its specialized hardware, strategic partnerships, and expanding data center footprint.

Increased demand for AI compute will fuel significant revenue growth and margin expansion, resulting in substantial shareholder value creation.

A potential acquisition by a major cloud provider could further accelerate returns.

Bear Case: CoreWeave will struggle to compete with larger, more established cloud providers in the increasingly competitive GenAI infrastructure market.

Slower than anticipated adoption of AI and difficulty managing its debt burden will hinder growth and profitability.

Technological obsolescence and execution challenges will further erode the company's competitive advantage, leading to a significant decline in value.

Conviction: High

2. Business Overview

CoreWeave, Inc. operates a cloud platform that provides scaling, support, and acceleration for GenAI. The company builds the infrastructure that supports compute workloads for enterprises. Its products include GPU compute, CPU compute, storage services, networking services, managed services, and virtual and bare metal servers. Additionally, its platform offers a fleet lifecycle controller, node lifecycle controller, tensorizer, and observability. The company's services also include VFX and rendering, AI model training, AI interference, and mission control. CoreWeave, Inc. was formerly known as Atlantic Crypto Corporation and changed its name to CoreWeave, Inc. in December 2019. CoreWeave, Inc. was incorporated in 2017 and is based in Livingston, New Jersey.

Competitive Moat (Narrow)

Trend: Stable

Specialized infrastructure optimized for GenAI workloads., Potentially more competitive pricing compared to larger cloud providers (needs further validation)., Focus on specific AI applications (VFX, rendering, AI model training)., Strong potential to create switching costs by integrating its platform into customer workflows.

Key Strengths:

Specialized infrastructure optimized for GenAI workloads.

Potentially more competitive pricing compared to larger cloud providers (needs further validation).

Focus on specific AI applications (VFX, rendering, AI model training).

Strong potential to create switching costs by integrating its platform into customer workflows.

The Software - Infrastructure market is projected to continue its strong growth trajectory, fueled by digital transformation initiatives, the adoption of cloud-native technologies, and the proliferation of AI applications. Growth rates are expected to remain high for the next 5-10 years.

Regulatory Environment:

N/A

4. Financial Analysis

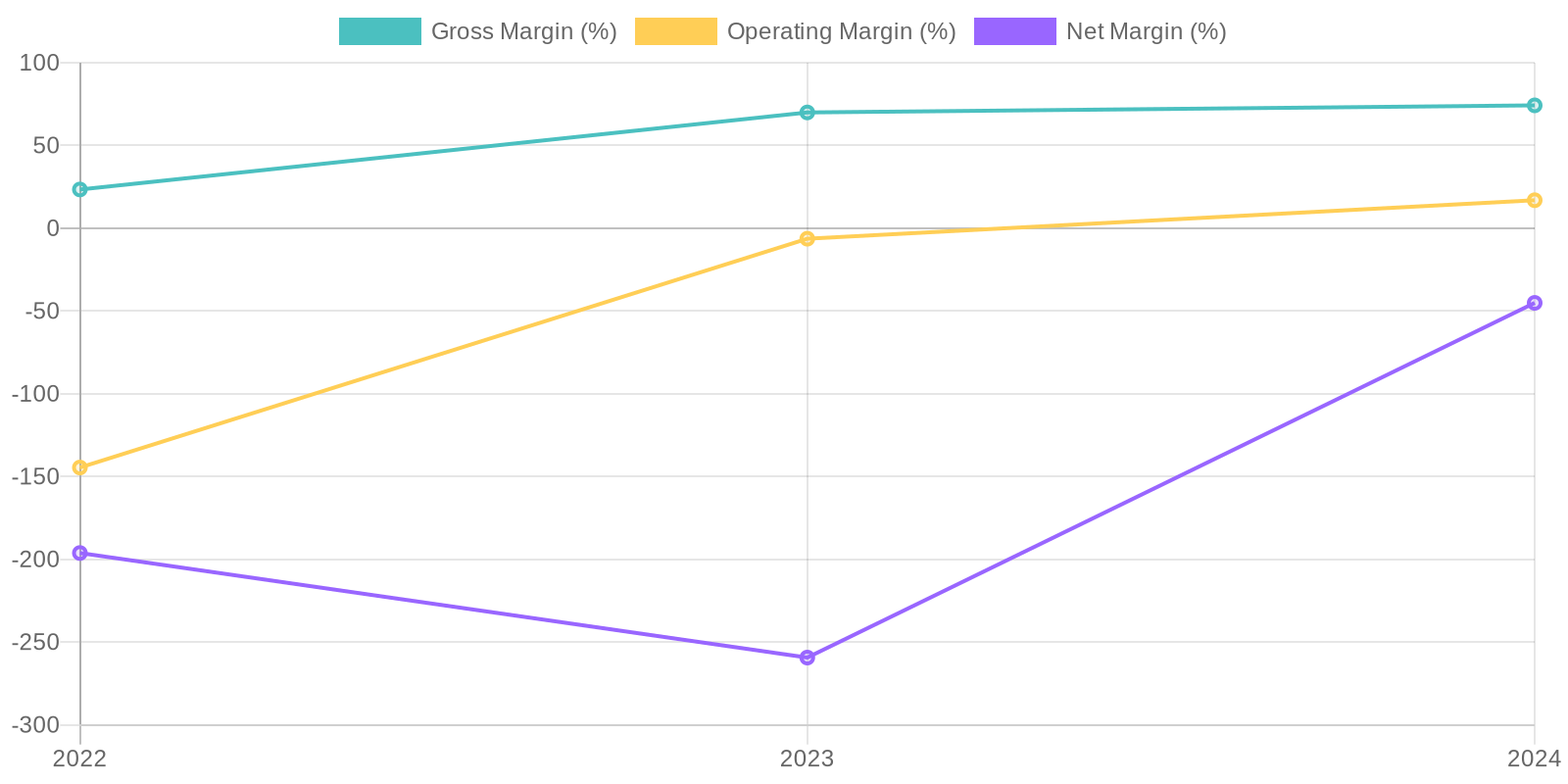

Margin Trend

Calculating ROIC and ROE is challenging due to the negative equity in both 2023 and 2024, rendering traditional ROE calculations meaningless. Return on Invested Capital (ROIC) also presents difficulties due to fluctuating profitability and significant changes in invested capital year to year, but given the current year's negative net income, the ROIC is definitely low. Further analysis on the efficiency of capital deployment and asset utilization is necessary to get a better understanding.

Revenue Quality

The company experienced substantial revenue growth in 2024, primarily due to a large increase compared to the previous two years. Further investigation would be required to understand the exact cause of this revenue boom, and if it's sustainable. Examining the revenue mix and contract terms with major clients would provide insight into the recurring nature and overall predictability of revenue streams.

Cash Flow & Capital Efficiency

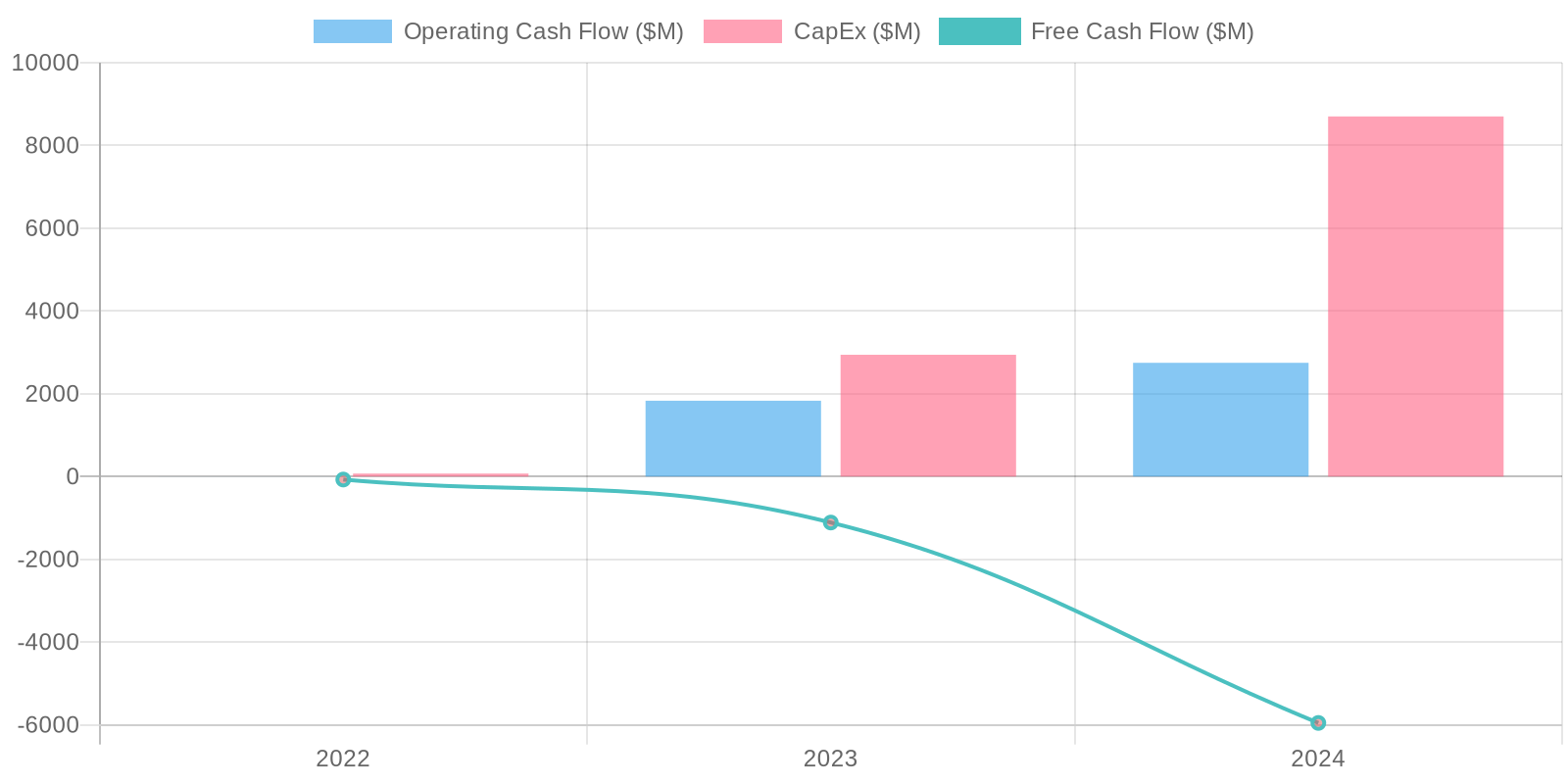

The company's free cash flow (FCF) is significantly negative at -$5.95 billion in 2024, a concerning trend given the already negative FCF in 2023 (-$1.11 billion) and 2022 (-$71.49 million). This negative FCF stems from a large capital expenditure of -$8.70 billion. While operating cash flow is positive ($2.75 billion) in 2024, the massive capital expenditure is driving a large cash outflow.

Capital Efficiency (ROIC/ROE):

Calculating ROIC and ROE is challenging due to the negative equity in both 2023 and 2024, rendering traditional ROE calculations meaningless. Return on Invested Capital (ROIC) also presents difficulties due to fluctuating profitability and significant changes in invested capital year to year, but given the current year's negative net income, the ROIC is definitely low. Further analysis on the efficiency of capital deployment and asset utilization is necessary to get a better understanding.

Balance Sheet Health:

The company's balance sheet presents a mixed picture. While it holds a substantial cash balance of $1.36 billion in 2024, it is dwarfed by a very high debt level of $10.62 billion. Furthermore, the company has negative equity of -$413.60 million. The liquidity is questionable given current liabilities approaching $5 billion.

5. Management & Governance

CEO Assessment: Due to the limited information available in the provided context, a comprehensive assessment of CoreWeave's CEO is not possible. A thorough analysis would require details regarding their track record, strategic vision, communication style, and ability to execute. Recent news and observable performance data should be included when available. Without concrete performance indicators, a neutral stance is necessary.

Capital Allocation: Good

Insider Ownership: Information on specific insider ownership percentages is not available, which limits the ability to assess alignment between management and shareholders definitively. Generally, significant insider ownership is viewed positively as it aligns interests, but the magnitude and distribution of ownership matter. Further data on insider ownership and recent trading activity would be required for a complete picture.

Governance Flags:

No major governance concerns flagged.

The fair value of $67.50 is significantly lower than the current price of $95.01. This suggests the stock is overvalued based on my assumptions. The high capital expenditure requirements in the early years, coupled with the current negative net income, weigh heavily on the valuation. The estimated price target reflects a 10% potential upside from the calculated fair value, but also accounts for 30% potential downside due to volatility. The valuation is sensitive to the revenue growth, operating margin, and capital expenditure assumptions. The confidence is medium because the future growth trajectory is uncertain. It is hard to predict if they can continue hyper-growth in a market that is seeing some contraction, especially given the capital intensity of the business.

Scenarios

Scenario

Price Target

Key Assumptions

Bull

High

CoreWeave will emerge as the leading infrastructure provider for GenAI, driven by its specialized hardware, strategic partnerships, and expanding data center footprint.

Increased demand for AI compute will fuel significant revenue growth and margin expansion, resulting in substantial shareholder value creation.

A potential acquisition by a major cloud provider could further accelerate returns. |

| Base | 74.25 | CoreWeave will continue to grow its revenue and market share in the GenAI infrastructure market.

While competition will intensify, the company's specialized expertise and strong customer relationships will allow it to maintain a healthy growth trajectory.

Gradual improvements in profitability and efficient capital management will drive a positive return on investment. |

| Bear | Low | CoreWeave will struggle to compete with larger, more established cloud providers in the increasingly competitive GenAI infrastructure market.

Slower than anticipated adoption of AI and difficulty managing its debt burden will hinder growth and profitability.

Technological obsolescence and execution challenges will further erode the company's competitive advantage, leading to a significant decline in value. |

7. Risks

CoreWeave presents a high-risk investment profile due to substantial negative net income, significant negative free cash flow, a high debt burden, negative equity, and escalating losses despite rapid revenue growth. The company's ability to sustain operations is highly questionable without significant improvements in profitability and cash flow management.

Red Flags:

High debt levels relative to cash and revenue.

Negative free cash flow and net income.

Negative Stockholders Equity

8. Conclusion

CoreWeave will continue to grow its revenue and market share in the GenAI infrastructure market.

While competition will intensify, the company's specialized expertise and strong customer relationships will allow it to maintain a healthy growth trajectory.

Gradual improvements in profitability and efficient capital management will drive a positive return on investment.

Investment research for informational purposes only. Not financial advice.

Continue Your Research

Return to the Analyst Library or explore the specific financial data for this entity on its profile.

Calculating ROIC and ROE is challenging due to the negative equity in both 2023 and 2024, rendering traditional ROE calculations meaningless. Return on Invested Capital (ROIC) also presents difficulties due to fluctuating profitability and significant changes in invested capital year to year, but given the current year's negative net income, the ROIC is definitely low. Further analysis on the efficiency of capital deployment and asset utilization is necessary to get a better understanding.

Calculating ROIC and ROE is challenging due to the negative equity in both 2023 and 2024, rendering traditional ROE calculations meaningless. Return on Invested Capital (ROIC) also presents difficulties due to fluctuating profitability and significant changes in invested capital year to year, but given the current year's negative net income, the ROIC is definitely low. Further analysis on the efficiency of capital deployment and asset utilization is necessary to get a better understanding. The company's free cash flow (FCF) is significantly negative at -$5.95 billion in 2024, a concerning trend given the already negative FCF in 2023 (-$1.11 billion) and 2022 (-$71.49 million). This negative FCF stems from a large capital expenditure of -$8.70 billion. While operating cash flow is positive ($2.75 billion) in 2024, the massive capital expenditure is driving a large cash outflow.

The company's free cash flow (FCF) is significantly negative at -$5.95 billion in 2024, a concerning trend given the already negative FCF in 2023 (-$1.11 billion) and 2022 (-$71.49 million). This negative FCF stems from a large capital expenditure of -$8.70 billion. While operating cash flow is positive ($2.75 billion) in 2024, the massive capital expenditure is driving a large cash outflow.